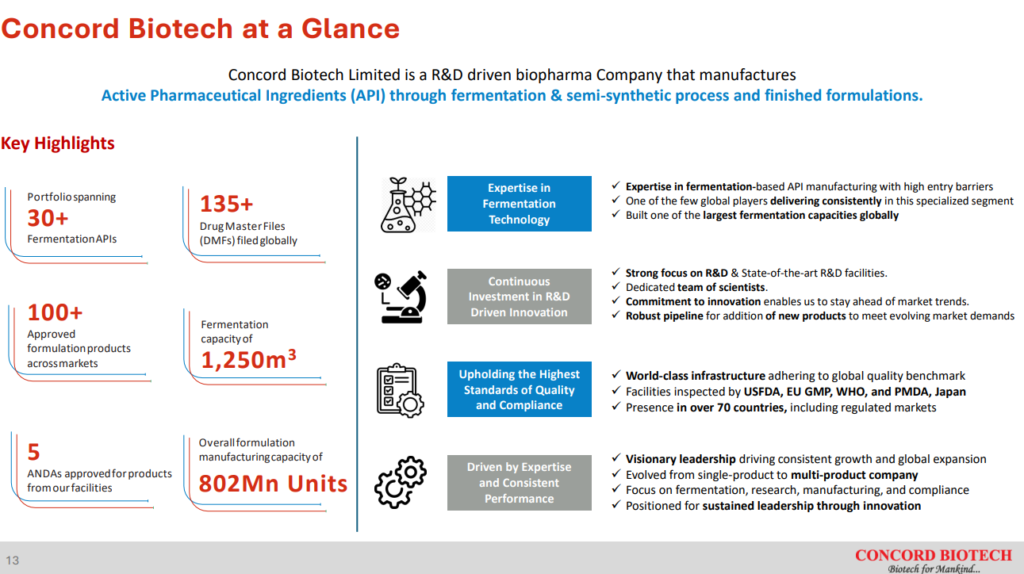

Concord Biotech Limited is a leading, R&D driven biopharmaceutical company focused on driving sustainable growth through manufacturing fermentation based Active Pharmaceutical Ingredients (APIs) and formulations.

Depending on how the growth trajectory evolves from here, Concord Biotech Ltd may turn out to be an interesting play in the overall pharma industry. It is one of the very few fermentation based API makers in the country which has recently built capacity in the injectables segment and is looking forward to seeing a healthy scale up in the utilization of its new facilities from here. Unit economics and ROCE profile are excellent for this business and give comfort on the balance sheet and cash flow situation.

Concord Biotech Ltd Company Summary

Concord Biotech Ltd. is a smallcap company headquartered in Ahmedabad, India. Concord Biotech Ltd makes fermentation based APIs and formulations for the Indian market and exports.

Concord Biotech Ltd’s origins go back to 1984, when it was first set up as Servomed Pharmaceuticals Pvt. Ltd. in Ahmedabad. The company changed hands a few times in the early years. It began as a subsidiary of Hoechst, later came under Vijay Mallya’s UB Group (1989), then Ranbaxy’s Max GB (1994), and finally DSM of the Netherlands. DSM eventually shut down the unit in 2000 after running into heavy losses.

That’s when Sudhir Vaid, a fermentation scientist who had built his career at Ranbaxy stepped in. In May 2000, he acquired the company for just about ₹3.6 crore, even though it had accumulated losses of nearly ₹4 crore. He renamed it Concord Biotech Ltd in 2001 and started focusing on biotechnology and fermentation based APIs

Sudhir Vaid literally restarted from the scratch, operating out of the plant in Dholka working with just two chemists. From here, Concord Biotech Ltd’s transformation began. Concord Biotech Ltd first made a mark by developing statins (pravastatin, lovastatin, simvastatin) using fermentation processes and supplying them to global generic players like Teva. The real breakthrough came when Concord Biotech Ltd became one of the first Indian companies to master the production of tacrolimus, a critical and high value immunosuppressant API used in organ transplants. This put Concord on the global biotech map as a niche fermentation specialist.

Around 2004 Sudhir Vaid sold about 30% stake to raise growth capital, 18% went to Rakesh Jhunjhunwala’s RARE Enterprises and 12% to Ontario Inc., Canada. Sudhir Vaid admitted openly that he was a researcher, not a finance or marketing person and bringing in strategic investors gave him the resources to scale.

In 2005-06, Matrix Laboratories acquired a majority stake (~55%), giving Concord access to more funding and markets. But when Matrix (later part of Mylan) exited in 2009, the shares were bought back by Sudhir Vaid and RARE Enterprises, (which significantly increased Rakesh Jhunjhunwala’s holding). This marked the second phase of Concord Biotech Ltd’s growth.

Over the next decade, Concord Biotech Ltd expanded capacities and earned regulatory approvals from USFDA, EU-GMP, PMDA Japan, ANVISA Brazil, among others, establishing credibility as a global fermentation player. In 2016, private equity firm Quadria Capital (through Helix Investment Holdings) came on board as a large shareholder, while Concord Biotech Ltd also diversified into formulations, building its presence in therapies such as nephrology, oncology, and critical care

In August 2023, Concord Biotech Ltd listed on the Indian stock exchanges through a ₹1,550 Cr IPO, which was entirely an Offer for Sale by Helix.

Major Milestones in the journey of Concord Biotech Ltd.

- 2000-2001: Acquisition by Sudhir Vaid; renamed Concord Biotech; biotech pivot

- 2005: First USFDA clearance for Dholka unit; launch of tacrolimus and sirolimus

- 2009-2010: Expanded global immunosuppressant footprint; became supplier to top 10 generic players

- 2011-2015: Entry into oncology APIs and antifungals; multiple DMF filings in regulated markets

- 2016: Forward integration into formulations; APIs remain anchor business

- 2021: Commissioning of Unit III (Limbasi); fermentation capacity doubled

- 2023-2025: Strengthened oncology and antibacterial basket; 30+ APIs across four therapy areas comprising ~78% of Concord’s FY25 revenue base.

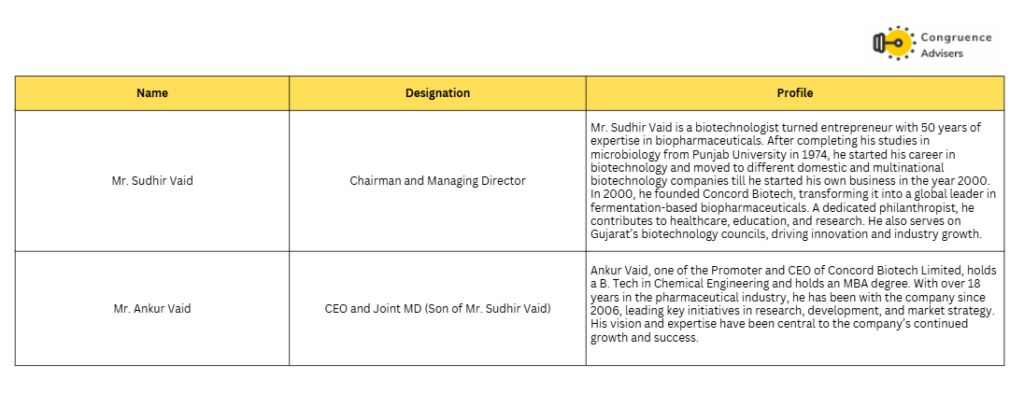

Concord Biotech Ltd Management Details

Concord Biotech Ltd’s is run by a technocrat management. Sudhir Vaid is a hands on fermentation builder who bought a shut DSM unit in 2000, turned it around in two years and with a five-member team he developed pravastatin tech and sold it to Teva, then won repeat business from Teva, Aurobindo, Lupin, Orchid, Biocon. In 2004 he pioneered an India-first tacrolimus process and pushed for USFDA inspection, reinforcing a “high value /low volume” discipline rather than commodity scale. From early days he also ran the balance sheet conservatively (famously prepaying a UTI loan), signaling control over both quality and capital. That’s why early investors viewed Concord Biotech Ltd as a “bet on Vaid” and why the franchise has held ground in hard fermentation niches.

Ankur Vaid (JMD & CEO) son of sudhir vaid carries the same DNA and scales it. His operating frame is direct: keep APIs as the cash engine and lift utilization , back-integrate into formulations especially hospital injectables where Concord Biotech Ltd’s own fermentation APIs confer cost and supply advantage and build a CDMO leg that monetizes the same fermentation/validation muscle for global customers.

Concord Biotech Ltd – Industry Analysis

What are fermentation based APIs

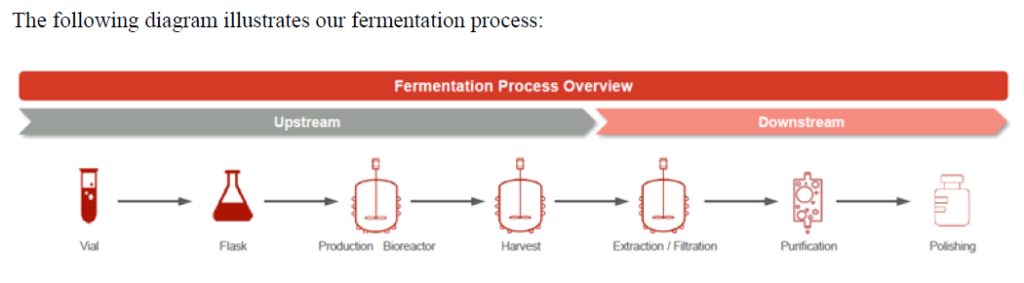

Fermentation-based APIs are active pharmaceutical ingredients whose core structure is produced by living cells in bioreactors rather than built purely through synthetic chemistry. Engineered bacteria, yeasts or fungi are grown in controlled tanks, where they secrete complex molecules that are then purified and sometimes further modified by organic synthesis (semi-synthetic APIs). This route is essential for intricate structures that are hard or uneconomic to make synthetically, such as many antibiotics (penicillins, cephalosporins, rifamycins), immunosuppressants (tacrolimus, sirolimus, cyclosporine, mycophenolate), certain oncology and cholesterol-lowering drugs, vitamins and amino acids.

In the pharmaceutical industry, these APIs underpin anti-infective, transplant, oncology, metabolic and rare-disease therapies, and the same fermentation platforms are used to make enzymes and biocatalysts that enable greener, more selective synthesis of other drugs.

In the broader chemical industry, related fermentation processes produce industrial enzymes, food ingredients, organic acids, solvents and bio-based intermediates, allowing companies to replace petrochemical routes with more sustainable, biology-driven manufacturing.

Commercial scale, high-yield fermentation is a tough nut to crack for the following reasons

- Strain engineering and selection – Building genetically stable, high yielding microbial strains is not easy. It requires significant microbiology and strain engineering work

- Very selective reaction environment – Large stainless-steel fermenters are very sensitive: small slips in sterility, pH value, temperature, oxygen or feed can contaminate a 10,000–100,000 L batch and ruin yields

- Lab to commercial scale up is challenging – Lab to commercial scale up for fermentation APIs is a non-linear process and quite challenging. Success at lab scale and success at reactor scale are two different things

- Downstream processing to filter from “broth” – Once the reaction is over, downstream separation of the API from the “biochemical broth” is not easy. The product is usually present in low concentration in a dirty broth, so one needs complicated separation and purification trains – centrifugation, filtration, extraction, multiple chromatography steps, crystallisation – plus strong analytical control just to get to the GMP-grade API

For this reason, there are not many fermentation players at scale in India or globally.

Fermentation based small molecule API market size

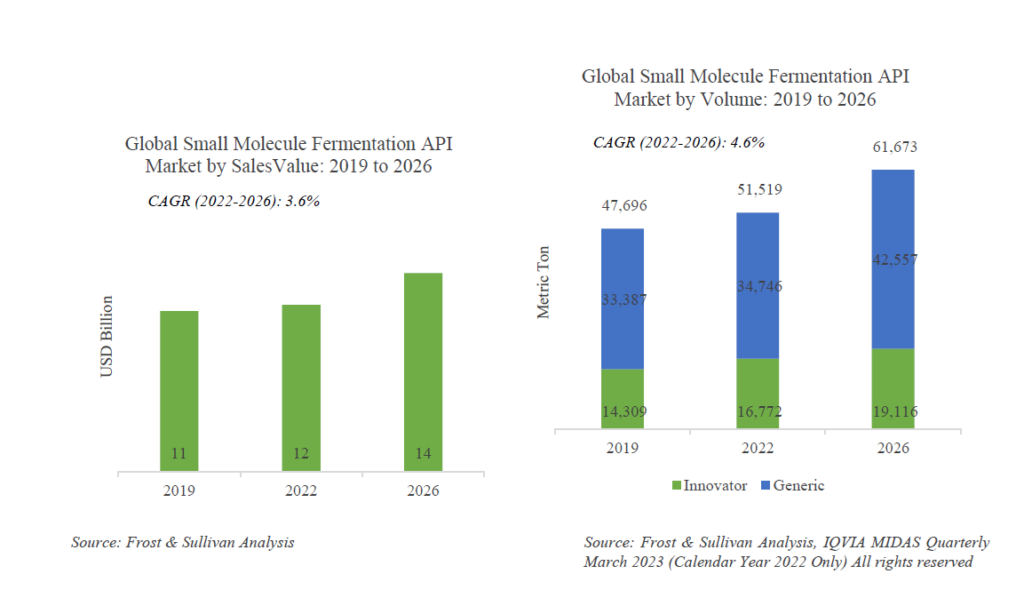

The global fermentation based small molecule API market is expected to be ~14bn USD in size by 2026. The market is expected to grow at a CAGR of 3.6% between 2022-2026. The total volume of fermentation based small molecule APIs is expected to be ~61.7k MT by 2026. The average realization of these APIs is ~227$/kg. Within this, about 70% by volume is generic APIs.

The share of generic APIs is expected to further increase with more patent expiries for fermentation based APIs in the near future as depicted in the graphic below.

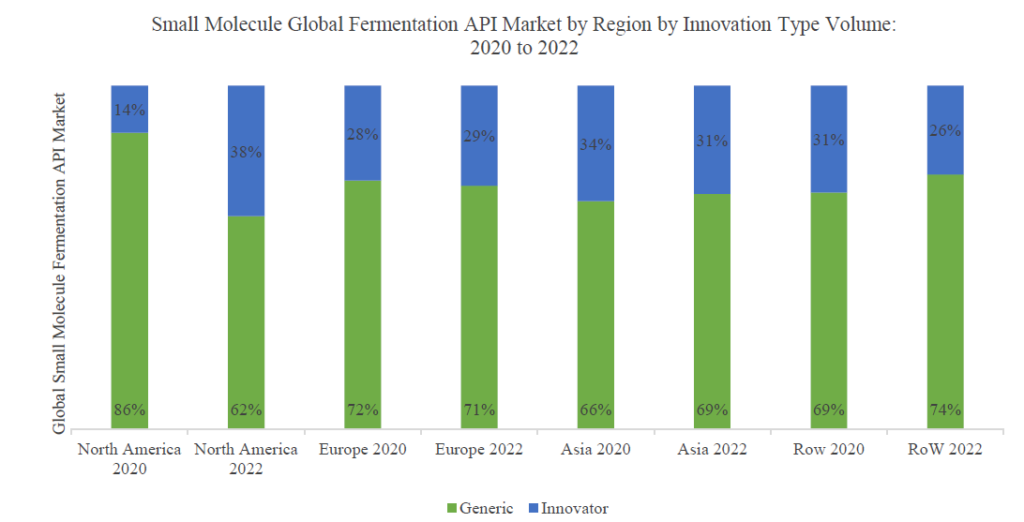

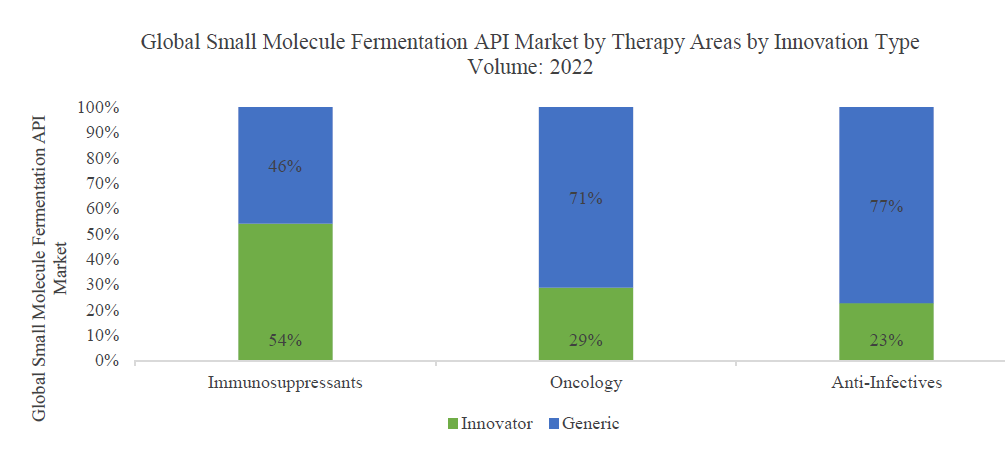

The global fermentation based small molecule API market is driven primarily by three therapeutic areas – immunosuppressants, oncology and anti-infectives

Let us take a detailed look at some of the largest fermentation based APIs in these three therapeutic areas where Concord Biotech has substantial market share

Fermentation based small molecule immunosuppressant APIs

The fermentation‐based APIs for immunosuppressant drugs accounted for only 2% of the share by volume but are estimated to have contributed 9% to 11% (approximately USD 1 billion) of the market by value owing to the higher price of the immunosuppressant APIs. In line with the global market trends, there has been an increasing shift in favor of generic drugs in the past few years, thus leading to an increasing proportion of generics in the overall market. The increasing genericization leading to increased affordability of drugs, combined with a growing number of organ transplants and autoimmune disorders is expected to drive a volume growth of 9% to 11% for this segment between 2022 and 2026. Some of the largest fermentation based immunosuppressant APIs are

- Tacrolimus – Tacrolimus based global drug market size is ~3bn USD and the API market size is ~121mn USD with a volume contribution of ~1923 Kg. The average realization of tacrolimus API is USD 63000/kg, almost 227x the average realization of fermentation based APIs (USD 227/kg). This is a very high value API and Concord Biotech is only one of three global suppliers including Teva Pharma who have DMFs in all key global markets. Concord Biotech Ltd is estimated to have a volume market share of 40% in this API segment.

- Mycophenolate Sodium – The mycophenolate sodium formulation market was valued at USD 364 mn in 2022 and the API market was valued at USD 26 mn with a volume consumption of 102,918 kg in the same year. The API market by volume is expected to witness a CAGR of 7.1% between 2022 and 2026 as demand from Asia and the Rest of World increases owing to the growing number of transplants. Novartis (Innovator), Apotex, Lupin and Intas Pharma dominate the formulation market. Concord Biotech Ltd has a ~22% market share by volume in this API

- Cyclosporine – Cyclosporine is an immunosuppressant for preventing organ rejection in kidney, liver, and heart allogeneic transplants. It is also prescribed for psoriasis, rheumatoid arthritis, and uveitis. The cyclosporine formulation market generated USD 3 bn in sales in 2022. The API market in the same year was valued at USD 36 mn with sales of 26,109 kg. The market was split slightly in favor of generic, which accounted for 57%, while innovators accounted for 43% of the volume share. The cyclosporine API market is expected to grow at a CAGR of 2.4% between 2022 and 2026 by volume. Concord Biotech Ltd is the largest supplier of cyclosporine API from India with a global volume market share of ~30%.

- Mycophenolate Mofetil – Mycophenolate Mofetil is indicated for prophylaxis of organ rejection in patients and treatment of primary and secondary glomerulopathies, uveitis, Crohn’s disease, rheumatoid arthritis, and lupus. Mycophenolate mofetil based formulations generated approximately USD 973 mn in sales in 2022 and the corresponding API market was valued at USD 116 mn with volume sales of 489 metric tons. There are only two companies – Concord Biotech Ltd and Teva Pharma – with active DMFs across all three highly regulated regions. Concord Biotech globally accounted for nearly 15% volume share in the Mycophenolate Mofetil API market

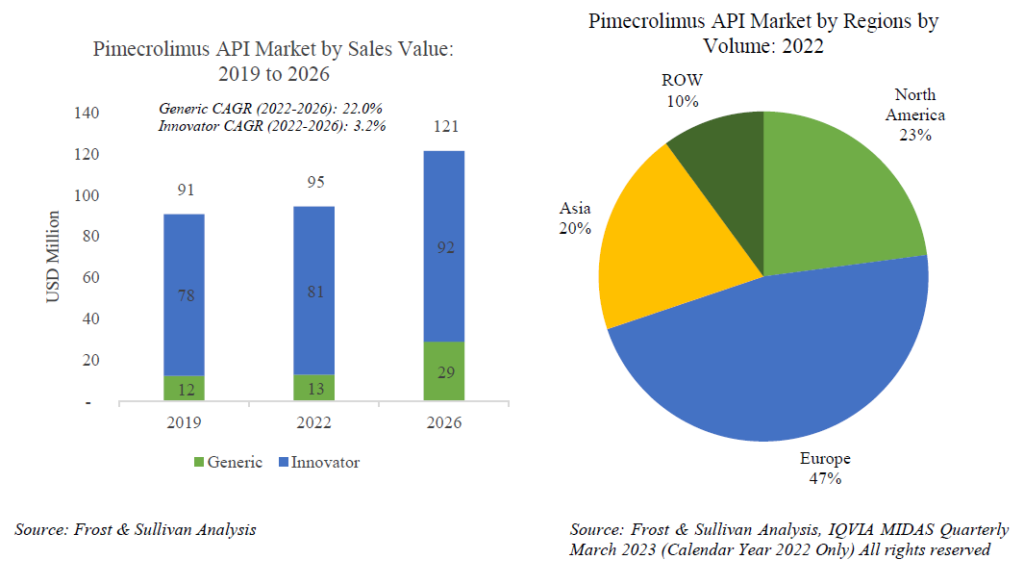

- Pimecrolimus – Pimecrolimus is prescribed as a second-line therapy to treat mild to moderate atopic dermatitis (eczema) in patients who have already been treated with other medicines that did not work well. The total Pimecrolimus formulation market was valued at USD 228 mn in 2022. In 2022, the API volume consumed was 1,554 kg, worth USD 95 mn. Given the recency of generic launches for this API, Concord Biotech Ltd has managed to capture 4% by volume of the global market.

Fermentation based small molecule oncology APIs

Though the global oncology fermentation API market accounted for only approximately 1% of the market by volume, the higher cost of APIs led to a sales value contribution of nearly 12% to 14% (approximately USD 1.4 billion) in 2022. The growing incidence of cancer and rapidly increasing R&D activity pertaining to anti-cancer drugs are primarily driving the market for oncology products. The increasing demand for more targeted, curative and safer drugs is further propelling the R&D pipeline. Many anti-cancer drugs (approximately 60%) approved since 1981 are natural products derived from microorganisms

- Everolimus – The total formulation sales for everolimus-based products were nearly USD 1 bn in 2022. The Everolimus API market in the same year is estimated to be USD 25 mn with volume sales of 118kg. The Everolimus API realization is extremely high at ~USD 211k/kg. Concord Biotech Ltd held 9% volume market share in the non-captive merchant market for Everolimus.

Fermentation based small molecule anti-infectives APIs

Since several anti‐infective drugs, particularly the antibacterial and antifungals, are fermentation‐derived, the antiinfective drug APIs accounted for the lion’s share of 74% in 2022 by volume but only 28‐30% (approximately USD 3.2 billion) by value. The average realization of fermentation based anti-infective APIs is only ~USD 90/kg versus the average fermentation based API realization of USD 227/kg. Anti-infective APIs are low margin, high volume and are dominated by Chinese producers

- Mupirocin and Mupirocin calcium – Mupirocin is an anti-bacterial ointment used to treat superficial skin infections such as impetigo caused due to bacteria such as Staphylococcus aureus and Streptococcus pyogenes. The total mupirocin and mupirocin calcium formulation market was valued at USD 291 mn in 2022. The total mupirocin API market by volume was 24 metric tons in 2022. Concord Biotech Ltd has a volume market share of ~22% in this API.

- Teicoplanin – Teicoplanin is an antibiotic used to treat severe bacteremia, complicated skin and soft tissue infections, bone and joint infections, infective endocarditis, peritonitis, community-acquired pneumonia, and community-acquired urinary tract infections. Due to its efficacy and low cytotoxicity, teicoplanin has also been used for patients with complications, including pediatric and immunocompromised patients. The teicoplanin formulation market was valued at USD 172 mn in 2022. The teicoplanin API market was valued at USD 20mn in 2022, with a volume consumption of 3,268kg

Concord Biotech Ltd Business Details

Concord Biotech Ltd operates across two segments

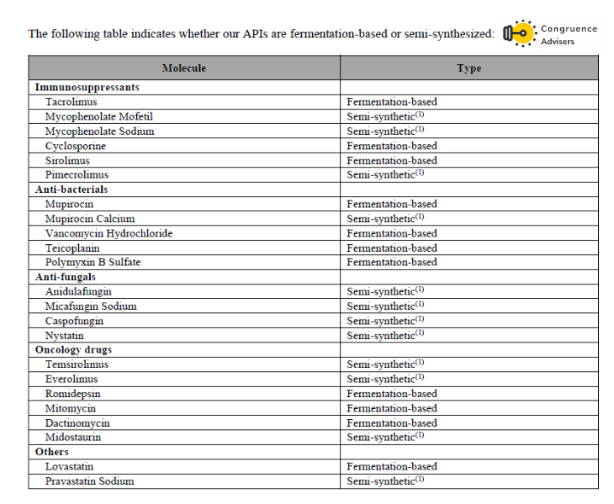

- API segment – This is Concord Biotech Ltd’s traditional business unit where Concord Biotech Ltd largely makes fermentation based APIs complimented by semi-synthetic APIs. Semi-synthetic APIs are APIs where the final API involves a mix of fermentation based as well as chemical synthesis.

- Formulation segment – This segment was established in 2016 as a forward integration of APIs. The forward integration helps them capture more value in the fermentation based therapeutics value chain

Concord Biotech Ltd has over 200 customers spread over 70+ countries. The top 10 customers comprise ~40% of Concord Biotech Ltd revenues and have had an average relationship tenure of 8 years with the company.

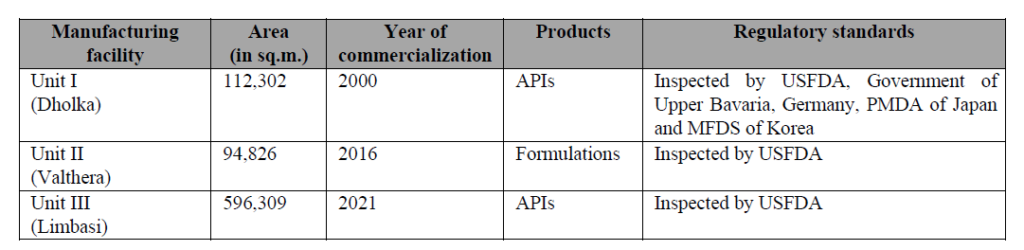

Concord Biotech Ltd operates across 3 plants located in Gujarat

API Segment

The API segment is the traditional business segment of the company. Under this segment, Concord Biotech Ltd manufactures 30+ fermentation based APIs. Concord Biotech Ltd has filed 135+ DMFs (Drug Master files) for these 30+ APIs globally, which enables them to sell these APIs in various geographies. Most of these DMFs have been filed in Europe, USA and Japan amongst other regulated markets. Most of the API business is export focused – even domestic supplies to Indian formulators are deemed exports. Apart from the 30+ commercial APIs, Concord Biotech Ltd has 8-10 APIs in the development pipeline which are likely to get commercial soon.

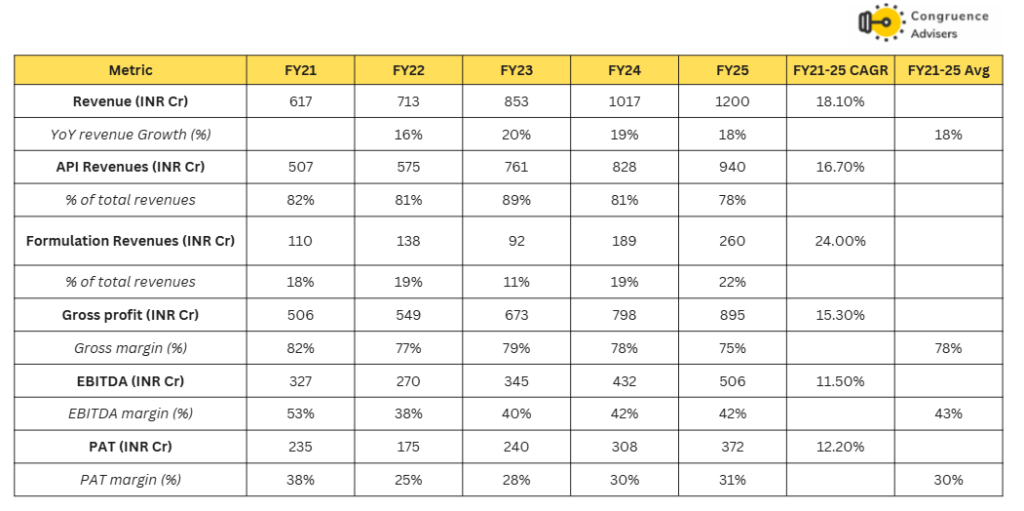

API revenues constitute 78% of Concord Biotech Ltd’s FY25 revenues and they have grown at a CAGR of 16.7% between FY21-25.

Concord Biotech Ltd. is exclusively present in generic fermentation based APIs. However it counts innovator pharma companies also amongst its clients. Concord Biotech Ltd. has a business strategy of focusing on high value APIs where they can make high gross margins. For this reason, they don’t manufacture too many fermentation based antibiotics because China has a large manufacturing presence here which drives realisations and margins down.

Instead, Concord Biotech Ltd. chooses to focus on relatively more niche areas such as fermentation based immunosuppressants, oncology molecules and select anti-infectives. Immunosuppressants are Concord Biotech Ltd’s largest portfolio constituent and comprise as much as 70-75% of its total API revenues. Immunosuppressants are used for managing patients undergoing organ transplants among other use cases. Concord Biotech Ltd. manufactured 6 immunosuppressant APIs as of 2023 including tacrolimus, sirolimus, mycophenolate sodium and mofetil, cyclosporine and pimecrolimus. In the oncology, anti-bacterial and anti-fungal therapeutic areas they had six, five and three commercialised APIs as of 2023. Mupirocin is an important anti-bacterial API and everolimus and romidepsin are important oncology APIs in Concord Biotech Ltd’s portfolio.

The total installed fermentation reactor capacity available with Concord Biotech Ltd. is 1250 KL. This is very likely the largest small molecule fermentation reactor capacity in India. Concord Biotech Ltd has two API manufacturing plants – Unit I in Dholka and Unit III in Limbasi. Dholka is a very old unit whereas Limbasi was commissioned in FY21. In H1 FY26, Dholka operated at a capacity utilisation of 76% whereas Limbasi operated at a capacity utilisation of 52%. The API manufacturing facilities in Dholka and Limbasi are divided into a total of 41 manufacturing blocks to process different classes of APIs, which provides flexible plant configuration and allows them to scale up production volumes to meet increased demand. The API facilities are inspected and approved by USFDA, EUGMP, Japanese PMDA and Brazilian ANVISA amongst others.

List of fermentation based vs semi-synthetic APIs manufactured by Concord Biotech Ltd

Concord Biotech Ltd. has recently forayed into the CDMO segment. In Q1 FY26 they started commercial supplies for their first innovator CDMO molecule which is a veterinary one. Right now the CDMO segment is < 1% of consolidated revenues but the management is optimistic that as a segment CDMO can scale to a 40-50mn USD contributor for Concord Biotech Ltd. across 5-6 molecules over the medium term.

Formulation segment

Concord Biotech Ltd entered the formulation segment in 2016 as a forward integration of its fermentation based API business. The rationale for entering the formulation business was to increase the value captured in the therapeutic area by capturing the value associated with formulations manufacturing in addition to API manufacturing. The formulation segment has lower gross margins than the API segment but is more or less the same as API segment at EBITDA margin levels. Concord Biotech Ltd mainly caters to the therapeutic areas of immunosuppressants, nephrology, critical care and rheumatology in formulations.

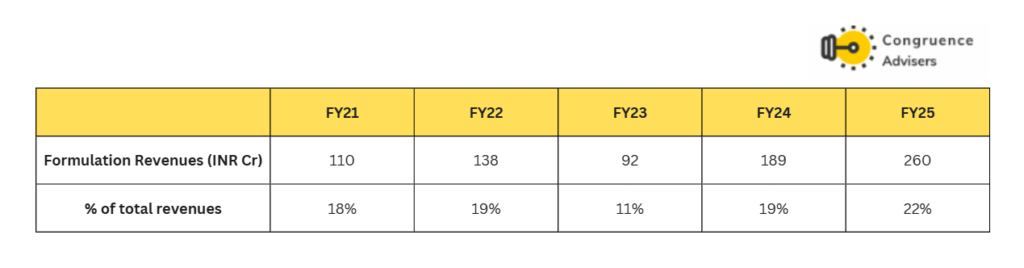

Formulation revenues have grown at a CAGR of 24% between FY21-25, almost 730 bps higher than API revenues. The formulation segment caters to both domestic and export sales. 50% of formulation sales are domestic, 33% to emerging markets and 17% to the USA. Formulation segment sales happen both to hospitals as well as to Government agencies via tenders. The Government business has higher working capital requirements but doesn’t require marketing spends, resulting in similar EBITDA margins to the hospital business.

The formulation segment is catered from the Valthera plant which was established in 2017. At present, the Valthera plant has a capacity of 800mn oral solid dosages (OSDs) , 13mn liquid vials, 2 Mn Dry Power Filling & 2,200 Kgs Sterile Lyophilized API. The H1 FY26 capacity utilisation of the OSD plant was only 24% and the newly commissioned injectable plant was barely utilised.

New injectables facility

The injectables facility was commissioned in CY25 at a cost of ~INR 180 Cr in Valthera Plant. The total installed capacity in this Unit is 13mn liquid vials, 12 Mn Dry Power Filling & 2,200 Kgs Sterile Lyophilized API. The management believes this facility can deliver revenues of INR 400-500Cr at peak capacity at better margins than OSD. As of Q2 FY26, two injectables products have been commercialised, two are on the cusp of commercialisation and 10 other products will get launched as part of Phase I. The initial ramp-up will be via domestic sales whereas emerging market sales will scale up in FY27.

R&D

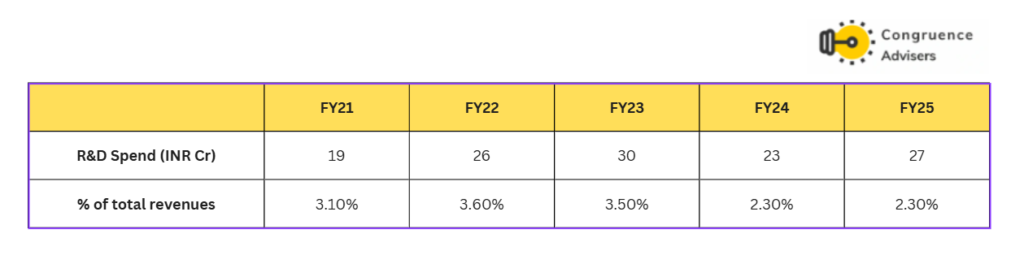

Concord Biotech Ltd employs 180+ employees in the R&D department. Concord Biotech Ltd has historically invested between 2-4% of its revenues in R&D.

For fermentation-based APIs the Concord Biotech Ltd. R&D team strives to improve fermentation technology through processes such as strain improvement and media optimization. For semi-synthetic APIs, the R&D team works on developing non-infringing downstream processes such as yield improvements, validation and impurity profiling.

Concord Biotech Ltd Corporate Governance Analysis

- Board Composition – The Board of Directors of Concord Biotech Ltd. comprises 9 members of whom 5 are Independent Directors. The Board is chaired by the promoter Mr. Sudhit Vaid.

- Promoter remuneration – The sum total of remuneration paid to promoters via salaries, perquisites, rent, professional charges etc. amounted to INR 16.7Cr in FY25, amounting to 4.5% of the total consolidated PAT of the company for FY25 and thus well within suggested limits. Dividends paid haven’t been considered as minority shareholders are also entitled to the same.

- Related Party Transactions – Other than the ones reported in promoter remuneration above, there are no significant reportable related party transactions

- Contingent Liabilities – The total contingent liabilities outstanding amount to INR 4Cr which is a miniscule % of Concord Biotech Ltd’s net worth of 1817Cr and hence immaterial.

- Dividend Policy – Concord Biotech Ltd has been paying dividends at the rate of 25-30% of PAT for the last 3 years

Concord Biotech Ltd Financial Performance

Concord Biotech Ltd has grown revenues at a CAGR of 18% since FY21. While API revenues have grown at 16.7% CAGR, formulations have grown at 24% CAGR. The % revenue contribution of formulations has increased from 18% in FY21 to 22% in FY25. Gross margins have reduced by 700bps during the period but still remain very high at 75% in FY25. EBITDA margins and PAT margins have remained stable around the 40-43% mark and 28-31% mark respectively over the last 3 years.

Concord Biotech Ltd Debt, Working capital, Cashflow and Return ratios

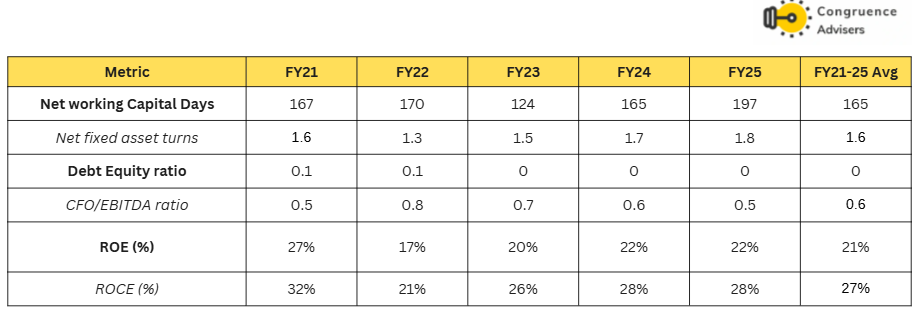

Concord Biotech Ltd balance sheet remains absolutely debt free, working capital intensity has increased from 167 days in FY21 to 197 days in FY25. This is primarily due to an increase in debtor days, presumably due to the growth of the formulations business, part of which is tender driven Government business where debtor days tend to be high. Overall, average ROEs and ROCEs have remained extremely healthy over this period at 21% and 27% respectively.

Going forward, the key monitorables in this story will be revenue growth i.e whether management is able to keep up with historical growth CAGRs; margin trends – will EBITDA margins hold as share of formulations increases in revenue; debtor days – will there be any more worsening of debtor days as formulations business scales up. Of the three, revenue growth is by far the most important factor here – the business has everything else in place.

Concord Biotech Ltd Comparative Analysis

To understand Concord Biotech Ltd investment potential, we have conducted a comprehensive analysis. This analysis includes comparing Concord Biotech Ltd to its competitors (peer comparison) on various fundamental parameters and Concord Biotech Ltd share performance relative to relevant benchmark and sector indices.

Concord Biotech Ltd Peer Comparison

Concord Biotech Ltd does not have too many listed peers. The closest peer is Gujarat Themis Biosyn Ltd., a fermentation based API manufacturer. Compared to Concord Biotech, Gujarat Themis Biosyn has a very narrow portfolio and most of its revenues come from the API Rifamycin which is used to make tuberculosis medicines. The other related peer is Advanced enzymes Tech Ltd which manufactures fermentation based enzymes for various pharmaceutical, chemical and industrial use cases.

Concord Biotech Ltd Index Comparison

Concord Biotech Ltd share performance vs S&P BSE Small Cap Index, as the index benchmark comparison is a fundamental tool for understanding the investment potential and making informed decisions in the context of the broader market

Why you should consider investing in Concord Biotech Ltd ?

- Largest fermentation based pharma API maker in India – Concord Biotech Ltd has the largest fermentation reactor capacity in India at ~1.25mn Litres. It is the largest fermentation based small API maker in India for pharmaceuticals and also one of the larger ones globally

- Very high business quality – Making fermentation based APIs at large scale is not easy – it is highly energy intensive and getting high enough reaction yields is not only a matter of science but of skill and experience. Therefore, Concord Biotech Ltd’s fermentation capabilities at scale are a de-facto moat for the business. This moat is reflected well in Concord Biotech Ltd’s margins and return ratios.

- Technocrat promoters with skin in the game – Mr. Sudhir Vaid founded Concord Biotech Ltd from scratch more than 2 decades ago. Before founding Concord Biotech Ltd as a fermentation company, he spent several years working as an employee in the Indian pharma industry with companies such as Lupin and Ranbaxy. In his last role before founding Concord Biotech Ltd, Mr. Vaid was the Head of Fermentation and Biotechnology at Ranbaxy for 8 years. Therefore, this is a promoter who is the whole and soul behind the science on which Concord Biotech Ltd is built – that’s as technocratic as they come. The promoter family continues to own 44% of Concord Biotech Ltd and did not sell a single share in the IPO. This should give investors strong confidence about the promoter’s skin in the game and belief in Concord Biotech Ltd.

- Formidable growth ambitions – Concord Biotech Ltd sees the potential to keep growing revenues at high-teens or mid-twenties for several years. As the API business grew large and pace of growth slowed down, they forward integrated into formulations to capture a larger slice of revenues in the same value chain. Recently they have forayed into injectables within formulations and have started CDMO business in the fermentation space as well. Thus, this is a promoter group which is not satisfied to sit on its laurels but is keen to push for growth

- No incremental capex required for medium term growth – The management has indicated that there is no capex needed apart from yearly maintenance capex of INR 20-25Cr for the medium term. They can grow at 18-20% comfortably without the need for additional capex. This is a nice setup which can provide appreciable operating leverage.

What are the Risks of investing in Concord Biotech Ltd.

- Valuations are not cheap – Since listing, Concord Biotech Ltd hasn’t traded below 40x TTM PE. Even now, in spite of a year of sluggish growth, Concord Biotech Ltd stock trades at 45x TTM PE. If growth slows down, there is a material downside risk to valuations

- High therapeutic concentration – 70-75% of Concord Biotech Ltd’s API revenues come from the therapeutic area of immunosuppressants. While Concord Biotech Ltd has built this portfolio and client relationships here over 2 decades, any unexpected disruption in these key IMSP APIs may have a significant negative impact on Concord Biotech Ltd.

- Fermentation APIs are a niche space – Fermentation APIs are a niche market within the overall API space, constituting ~5% of global API demand at $14bn per annum. While $14bn sounds huge (INR 1.2 Lakh Cr) in the context of Concord Biotech Ltd, it is important to note that only 10% of this market belongs to immunosuppressants, which is Concord Biotech Ltd’s primary API category. In the IMSP category, Concord Biotech Ltd already enjoys 6-7% market share, which is formidable in the global context. The bulk of the market is low-value antibiotic APIs, a space completely dominated by China.

- Slowdown in API segment revenue growth – Recently, there has been a slowdown in the API segment revenue growth for Concord Biotech Ltd. H1 FY26 API segment revenue growth was -14%. Even in FY25, before a big Q4 made FY25 API growth nos. look respectable (It came at the cost of gross margins), 9M FY25 API segment sales was up only 3%. Part of the sluggishness of API segment growth may be explained by higher utilisation of APIs to make formulations whose sales get captured in the formulations segments. Notwithstanding that, since APIs make up 80% of Concord Biotech Ltd’s revenues, if the segment fails to grow at mid to high teens, the overall growth target of the company may not materialise.

Concord Biotech Ltd Future Outlook

While the Concord Biotech Ltd management does not give explicit growth guidance, they have affirmed multiple times that they expect Concord Biotech Ltd to grow at least at the historical growth rates of ~18% with a chance to increase growth rates to 20-25% in the medium term.

Management expects the base API + formulations business to grow at the historical rates of ~18%

The key factors driving incremental growth beyond 18% as per management are – injectables scale-up, CDMO scale-up and the pipeline of 8-10 APIs getting commercial.

Concord Biotech Ltd Technical Analysis

We consider technical analysis to be a useful input in taking medium-term investment decisions. Many a time price action tends to lead to fundamental developments; this is too important an aspect to be ignored by retail investors who do not have access to management outside of common forums like investor calls & AGM.

At Congruence Advisers we like to consider both the long-term weekly chart and the daily chart to arrive at a view on price action. Combined with our understanding of fundamentals, we usually end up being better placed to be able to judge both the business cycle and the stock cycle. Playing the stock cycle right is extremely important for investors looking to extract significant alpha over the medium term.

Concord Biotech Ltd Price chart

Looking at the daily chart of Concord Biotech Ltd. over the last one year, it is very delicately poised. Concord Biotech Ltd. has struggled for revenue growth over the last year and that is reflected in its chart. The current price is right at the corner of the triangle formed by the downward sloping resistance line and the support line at 1384. From here, Concord Biotech Ltd stock either jumps back up and stays above the support or breaks the support line and goes down sharply. H2 FY26 results should determine which of these two possibilities play out. H1 FY26 has seen a big YoY decline in profitability. Management has guided for H2 FY26 to handsomely beat H2 FY25 profitability. If that does not materialise, one should expect a decisive break below the support line, probably on decent volumes. Even after significant price correction through CY25, Concord Biotech Ltd stock is still priced for 15-20% revenue growth.

The weekly chart covers price action for Concord Biotech Ltd stock since its IPO. The weekly chart is similar to the daily chart in so far as we get to see a downward sloping resistance line and the current price getting boxed in near the support zone of 1300-1380. In the event of a price breakdown below the key support of 1384 on the daily chart, one would have to observe if the weekly chart support zone of 1300-1384 holds or not. Unless management is decisively off about its assessment of medium term growth of the business, Concord Biotech Ltd stock price should not decisively break the support band and stay below it, we think.

Concord Biotech Ltd Latest Latest Result, News and Updates

Concord Biotech Ltd Quarterly Result

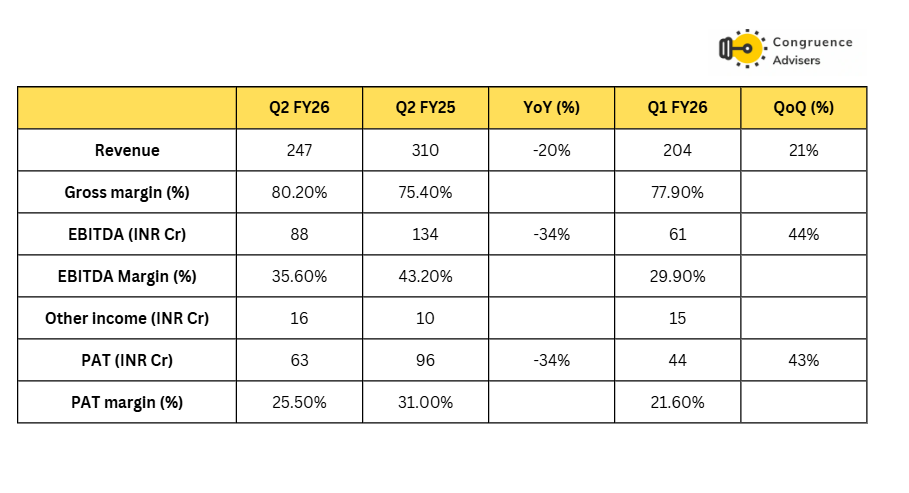

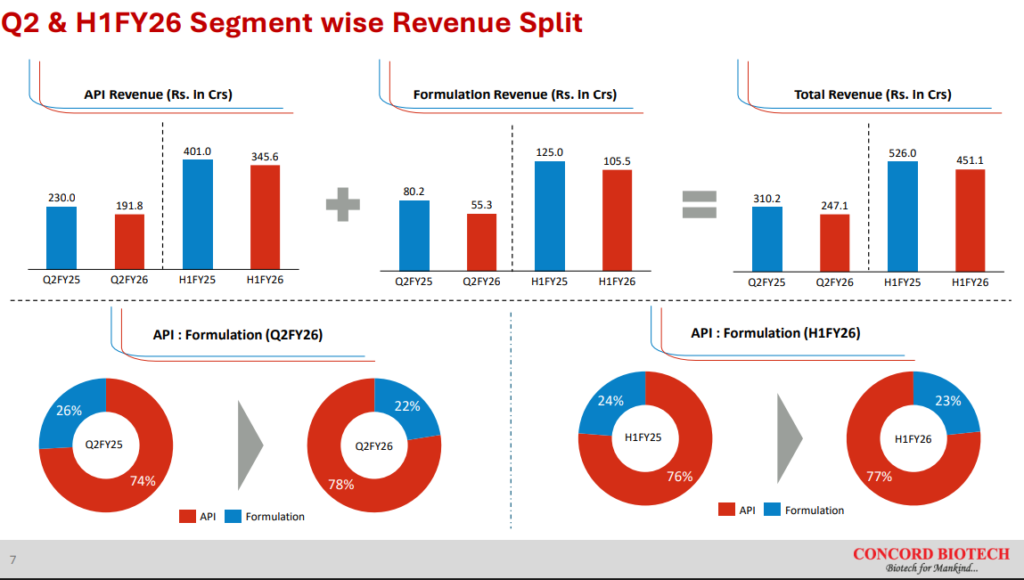

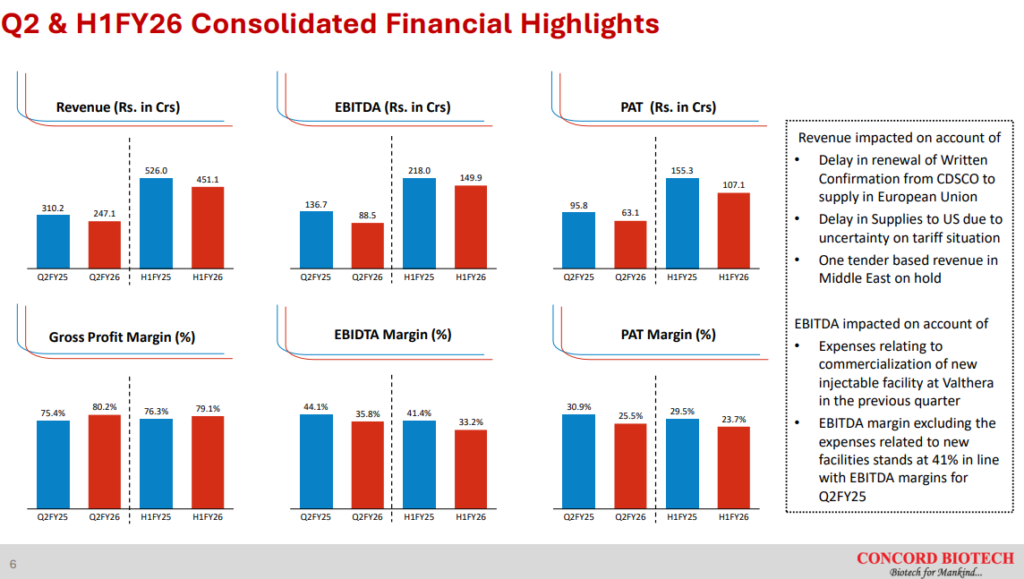

Concord Biotech Ltd. had a tough Q2 FY26. Revenue dropped 20% YoY and PAT and EBITDA were each down 34% YoY.

API revenues were down 17% YoY and formulation revenues were down 31% YoY. The management said that it faced a unique set of challenges in Q2 FY26 which set them back. On the API side, Concord faced a delay in CDSCO approval for exports to the European Union which delayed their export sales to Europe. There was also some postponement of orders from US customers on the back of tariff related concerns. On the formulation side, there was deferment of a Government tender in the Middle East that hit revenues.

EBITDA margins were impacted due to startup costs incurred for the injectables facility in Valthera. Ex of the one time costs, management said EBITDA margins would have been 41% for Q2 FY26, implying INR 13Cr cost incurred towards the injectables facility in Q2 FY26 without offsetting revenues. This is expected to settle down as the facility scales up.

Management said it was confident about delivering growth in H2 FY26 over H2 FY25. Considering H2 FY25 was a big half (Due to a huge Q4 FY25), delivering growth over it would require Concord Biotech Ltd doing ~INR 700Cr revenues in H2 FY26 vs only INR 451Cr revenues in H1 FY26. If the delays faced in Q2 FY26 spillover to H2 FY26 rather than turning into lost revenue, this guidance seems achievable.

Final Thoughts on Concord Biotech Ltd

Concord Biotech Ltd is a high quality business in the pharmaceutical industry. In the pharmaceutical API manufacturer landscape, Concord Biotech Ltd lies in the middle of the spectrum leaning towards the high quality side. While it does not work with novel, patented APIs like innovator CRDMO companies such as Laurus Bio, Sai Life Sciences, Divis Labs etc. do, but at the same time its quality of business and science moats are far stronger than generic small molecule API manufacturers. Fermentation at commercial scale is not an easy business to do – a lot of skill and experience is needed to make sure the microbes are working under optimal conditions needed to produce the end chemicals in the required yields. This is borne out by the stellar margins and return on capital economics that Concord Biotech Ltd enjoys.

In order to make high margins and good returns on capital, Concord Biotech Ltd. chooses to avoid the commoditised end of the fermentation API market i.e. antibiotics, which is dominated by Chinese companies producing at scale. Instead, Concord Biotech Ltd chooses to focus on high realisation fermentation APIs such as immunosuppressants, oncology APIs, select anti-infectives and select antibiotics.

While this strategy has served them very well since inception, it remains to be seen whether they can keep growing revenues at 15-20% per annum with the present TAM. Management has reiterated multiple times that they believe Concord Biotech Ltd has the potential to grow at 20%+ per annum for several years via a mix of organic growth in existing molecules, increasing wallet share in existing molecules, novel molecules going generic and coming into Concord Biotech Ltd’s addressable basket etc. However, the fact that Concord Biotech Ltd has forward integrated into formulations (lower margins than API) and is now striving to get into fermentation API CDMO, may point to signs that they believe they need to increase their addressable market to retain their historical growth rates or improve them.

For us, at this point, growth is the most important forward looking variable for Concord Biotech Ltd. As discussed earlier in the piece, API revenue growth has been tepid for a few quarters now (Except Q4 FY25). If API growth resumes and the market regains confidence on that count, then the stock is unlikely to trade at cheaper valuations than present (45x TTM PE) given the stellar unit economics, strong promoter pedigree and the long track record. If growth falters however (Below 15% on a sustainable basis) or margins stumble significantly in a bid to chase lower margin revenues, then there is a de-rating risk for the stock. Right now, we believe Concord Biotech Ltd stock is at a pivot point, where the market is waiting for more information to decide how to price the company.

Disclaimer – This note is part of a business research & analysis series on small companies, there is no BUY/SELL recommendation or target price issued as part of this to a general audience. There is no assurance that this stock makes for a good investment, there is no guarantee that this stock will continue/be included in the coverage universe of Congruence Advisers. The note contains some forward-looking statements and insights drawn from the historical results, annual reports and investor presentations; they are to be viewed only within this context and not as a prediction of future performance of the business or the stock covered.

While due care has been taken to ensure that the information here is as accurate as possible, Congruence Advisers disclaims any liability in case of any unintentional inaccuracies.

The content does not constitute investment advice.