Krishca Strapping Solutions Ltd Share Analysis

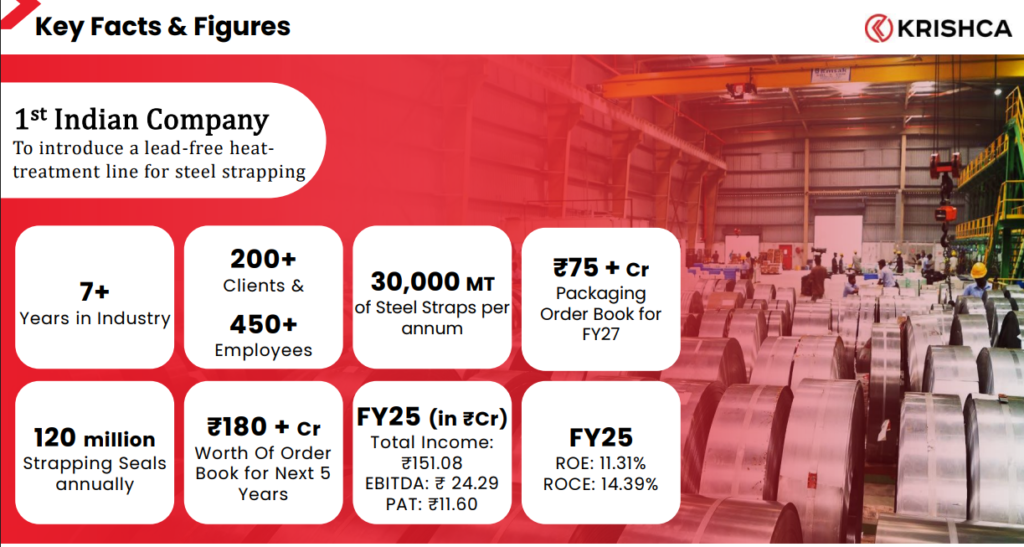

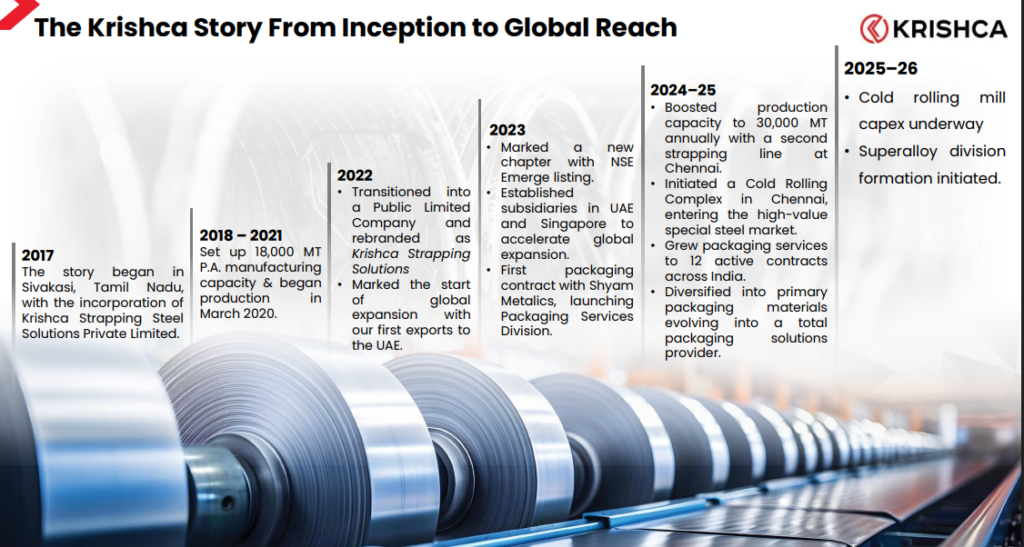

Incorporated in December 2017 and commencing commercial production in March 2020, Krishca Strapping Solutions Ltd is a leading Indian industrial packaging solutions company

Krishca Strapping Solutions Ltd presented to us an interesting proxy to play the enhanced outlook of India’s steel industry. While steel strapping is not as known a segment within steel as primary steel making or steel pipes & tubes, our intent behind this note is to explore if the business can offer the prospects that get us excited about microcaps – large market size, sizable market share, good unit economics & improving prospects. Krishca Strapping Solutions Ltd was also in the news through 2023 and 2024 following the IPO and QIP process which communicated an ambitious outlook for the business. In this note, we explore if we see enough positive possibilities in this unexplored and undiscovered business.

Krishca Strapping Solutions Ltd Company Summary

Krishca Strapping Solutions Ltd is a leading Indian industrial packaging solutions company, primarily engaged in the manufacturing of steel strapping and the supply of a broader basket of primary packaging and preservation products to the steel and allied industrial sectors. Krishca Strapping Solutions Ltd manufactures high-tensile and ultra-high tensile steel strapping designed for automated packaging machines, strapping tools and sharp-edged steel products, where consistency, tensile strength and reliability are critical from a safety and operational standpoint.

Over the years, Krishca Strapping Solutions Ltd has positioned itself as a quality-focused alternative supplier in a highly concentrated industry, catering to large steel producers such as Tata Steel, JSW Steel and SAIL, as well as several secondary steel manufacturers.

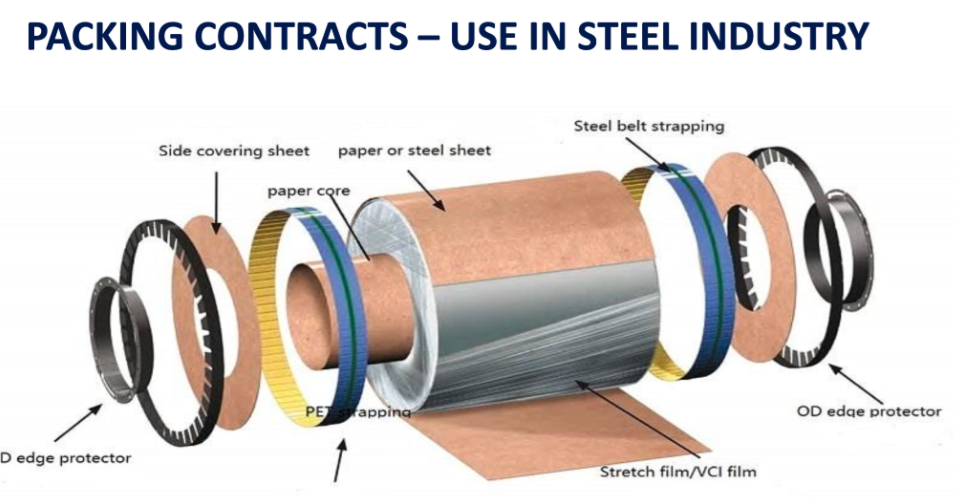

With a state-of-the-art manufacturing facility located in Chennai (Thiruvallur district), Krishca Strapping Solutions Ltd services customers across India and select export markets through a combination of direct strapping supplies and long-term packing contracts, where Krishca Strapping Solutions Ltd provides end to end packaging solutions including strapping material, tools, manpower and maintenance. To deepen wallet share and evolve from a product supplier to a solutions provider, Krishca Strapping Solutions Ltd has expanded its primary packaging portfolio to include tarpaulins, dunnage air bags, HDPE/LDPE films, desiccants and VCI-based corrosion protection products, which are increasingly critical in export packaging and moisture-sensitive steel logistics.

Krishca Strapping Solutions Ltd is also in the process of backward integrating into the cold rolling mill (CRM) segment, enabling in-house processing of medium and high-carbon steel and select stainless-steel strips. This backward integration is expected to improve raw material security, reduce procurement lead times and partially insulate margins from volatility in specialty steel availability, while also opening up an additional revenue stream through the sale of value-added special steel products to external customers. Over the medium term, this integration strengthens Krishca Strapping Solutions Ltd’s positioning as a more vertically integrated, solutions-oriented packaging and materials platform rather than a standalone consumables manufacturer.

Krishca Strapping Solutions Ltd Company Genesis

The inception of Krishca Strapping Solutions Ltd was driven by a fundamental macro-analysis of the Indian industrial landscape. Bala Manikandan, a young promoter with a Master’s in Cyber Security from University of Westminster, UK. returned to India with a clear intent to pivot away from his family’s legacy business in Sivakasi, Tamil Nadu. The family operated in the fireworks industry (a sector the promoter identified as a ‘dying industry’ with limited long-term terminal value)

The promoter Bala Manikandan, conducted a top-down analysis of the Indian Steel Industry. He observed that while India’s steel production was projected to grow aggressively from 100 million tons to a projected 300 million tons within 5-7 years (a CAGR of 15%) and the ancillary support ecosystem was lagging. Specially steel strapping used for securing steel coils (the heavy-duty packaging required to hold steel coils). At the time, the market was an oligopoly serviced by only three manufacturers catering to the entire nation. Seeing a clear supply deficit and a growing addressable market, the promoter deployed initial family capital to set up Krishca Strapping Solutions Ltd in 2017, with a strategy focused on technical differentiation, consistency, and long-term customer stickiness rather than price-led competition.

Between 2017 and 2019, Krishca Strapping Solutions Ltd grappled with technology absorption challenges, sourcing specialized machinery and know-how from China and Korea to establish a heat-treated steel strapping line (a process far more complex than standard metal processing). Commercial production commenced in March 2020, only to be immediately disrupted by the COVID-19 lockdown. The plant became operational just one week before the national lockdown. This left Krishca Strapping Solutions Ltd burdened with high operating leverage (fixed costs and debt service obligations) against a backdrop of zero revenue. Furthermore, the product itself steel strapping is a critical consumable. Steel mills are historically risk-averse regarding strapping because a failure can lead to catastrophic operational downtime or safety hazards.

The first year was a battle for survival, with the promoter admitting they considered exiting the business entirely. However, the supply crunch in the market eventually worked in their favor. The existing oligopoly could not service all demand, leading smaller players to trial Krishca Strapping Solutions Ltd’s product, which allowed the company to generate initial cash flow and to establish its first operating track record. The inflection point came in FY21 with vendor validation from JSW Steel, which awarded Krishca Strapping Solutions Ltd a large long term order (~₹36 crore). Interestingly, this was a case of backward integration driving demand. JSW Steel, aware that Krishca Strapping Solutions Ltd was purchasing raw materials from them and recognized Krishca as a potential vendor for their own packaging needs. This contract acted as an industry wide quality endorsement as once a Tier-1 major like JSW validated the technical specifications, it triggered a network effect, which allowed Krishca Strapping Solutions Ltd to onboard other industry majors like Tata Steel and ArcelorMittal, Nippon Steel. Over time, management consciously strengthened its competitive moat by emphasizing process consistency, lead-free production, and reliability (critical in a segment where the cost of failure far outweighs marginal price differences, often by 10-20x)

To deepen its integration with customers, Krishca Strapping Solutions Ltd evolved its business model from a pure manufacturing play to a service-oriented Packaging Contract model. Large steel plants prefer to outsource non-core activities. Krishca Strapping Solutions Ltd began offering end-to-end solutions where they supply the straps, manpower, tools, and maintenance for a per ton packing cost. As These contracts run for 6 months to 5 years (e.g., a 3-year deal with Vedanta), providing high visibility on future earnings and By taking over the entire packaging headache, Krishca Strapping Solutions Ltd makes it incredibly difficult for a client to switch vendors, effectively locking in the customer

Krishca Strapping Solutions Ltd Management details

Lenin Krishnamoorthy Balamanikandan (Managing Director & Chairman) as the founder and promoter, he drives the overall vision and strategy, He remains the primary executive leader, often leading earnings calls and strategic announcements.

Mrs. Navaneethakrishnan Saraladevi is a key promoter and the spouse of Mr. Lenin Krishnamoorthy Balamanikandan. Aged ~35, she holds an MBA (Marketing) degree from Madurai Kamaraj University and brings over 5 years of prior experience in sales and finance. As Whole-Time Director & CFO (appointed CFO in December 2022), she oversees financial strategy, capital allocation, compliance, and risk management. Holding ~8.9% equity in the promoter category.

Mr. Jagajyoti Naskar (Whole-Time Director & CEO) – Recently appointed as Chief Executive Officer effective November 12, 2024. This marks a key professionalization step for Krishca Strapping Solutions Ltd, bringing external expertise to handle growing scale, diversification, and execution of multi-year contracts. With over 24 years of experience in the packaging and industrial materials sector, Mr. Naskar was brought on board to strengthen operational leadership amid rapid growth. His appointment followed Krishca Strapping Solutions Ltd’s maturation post-IPO (2023). Prior roles likely involved senior positions in similar B2B industrial segments (steel/allied packaging ecosystem).

Krishca Strapping Solutions Ltd – Funding History

Krishca Strapping Solutions Ltd funding journey began with a successful maiden IPO in May 2023, followed by a substantially larger preferential allotment in August 2024, both executed at progressively higher valuations and attracting strategic ecosystem players.

IPO

Krishca Strapping Solutions Ltd IPO completed on May 19, 2023, raised ₹17.93 Cr through a 100% fresh issue of 33,20,000 equity shares at ₹54 per share on the NSE Emerge platform.Prior to the public offer, Krishca Strapping Solutions Ltd secured ₹4.88 Cr from anchor investors i.e Rajasthan Global Securities Private Limited (₹3.88 Cr) and Saint Capital Fund (₹1 Cr). IPO Proceeds were prudently deployed – ₹12 Cr toward establishing a new high-tensile steel strapping production line, ₹3.75 crore for debt repayment to strengthen the balance sheet, and the balance for general corporate purposes. Krishca Strapping Solutions Ltd got Listed on May 26, 2023 and delivered an impressive ~120% gain.

Preferential allotment & Convertible warrants

Krishca Strapping Solutions Ltd executed a significantly larger fundraise in August 2024, raising ₹68.04 Cr via preferential allotment of equity shares and fully convertible warrants at ₹233 per share/warrant. This comprised ₹49.40 crore from 21,20,000 equity shares allotted to 27 non-promoter entities and ₹18.64 crore from 8,00,000 warrants, with the promoter (Mr. Lenin Krishnamoorthy Balamanikandan) participating via 2,50,000 warrants to maintain alignment. The allotment attracted strategic investors closely linked to the steel industry, including entities associated with APL Apollo Group (S Gupta Family Investments), Shyam Metallics & Energy Ltd. (Subham Buildwell and Narantak Dealcomm), Real Ispat and Power (Real & Sons), and Shri Bajrang Power & Ispat (Shri Bajrang Commodity).

Utilization of the ₹68 crore of which ₹46.50 Cr has been earmarked for manufacturing facility expansion (primarily funding the 60,000 TPA cold rolling mill complex and related backward integration) and ₹12.50 Cr for working capital to support packaging contracts and setting up new product lines for primary packaging (tarpaulins, dunnage bags, VCI films, etc.), and ₹9.04 crore for general corporate purposes.

Krishca Strapping Solutions Ltd Industry Landscape

Steel Industry

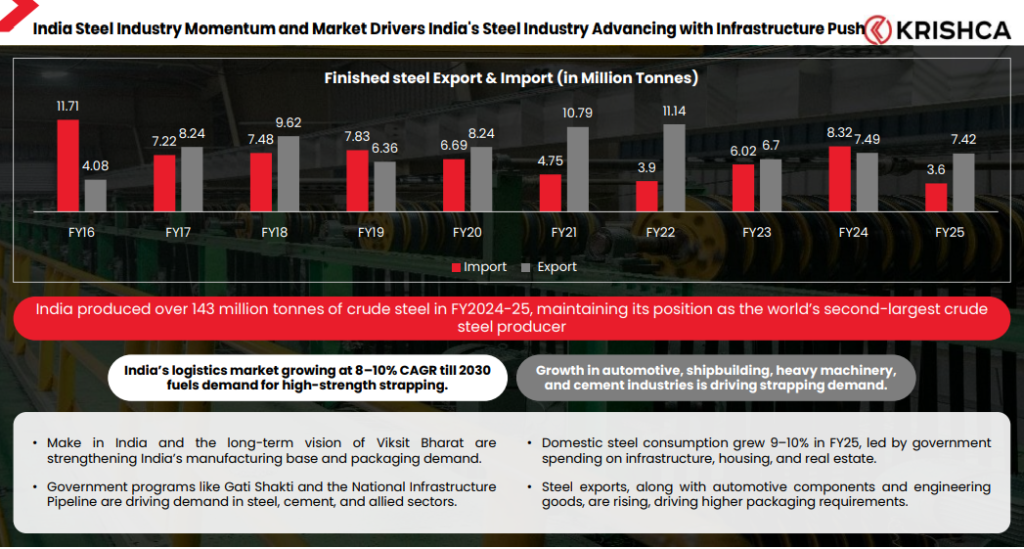

India’s steel industry stands as one of the brightest spots in the global metals landscape, and it is positioned as the world’s 2nd largest crude steel producer. In FY2024-25, the country achieved a record crude steel production of approximately 151 million tonnes (provisional data from Ministry of Steel), up ~6-7% YoY, with finished steel consumption reaching ~150 million tonnes. Which reflects 9-11% growth in recent periods driven by infrastructure push and industrial recovery. Installed crude steel capacity has expanded rapidly to ~200 million tonnes as of 2025, supported by aggressive brownfield expansions and greenfield projects from majors like Tata Steel, JSW, SAIL and AM/NS India.

This momentum aligns closely with the National Steel Policy 2017, which targets a crude steel capacity of 300 million tonnes by 2030-31, with projected production of 255 million tonnes and per capita finished steel consumption rising to ~158 kg (from current levels of ~97-100 kg). Steel demand is expected to grow at 7-10% CAGR over the next 5-10 years, fueled by:

- Massive infrastructure spending (e.g., Gati Shakti, National Infrastructure Pipeline, Bharatmala, Sagarmala, and housing/urbanization initiatives).

- Strong tailwinds in key consuming sectors: automotive (Make in India, EV push), shipbuilding, heavy machinery, cement, and engineering goods.

- Rising exports of steel and value-added products, alongside domestic logistics growth (8-10% CAGR to 2030), amplifying needs for secure bulk handling.

For ancillary players like Krishca Strapping Solutions Ltd this steel capex cycle translates into a great opportunity in steel strapping and packaging solutions. With India’s steel output and consumption scaling aggressively, demand for consistent, high-quality strapping (including automated lines, tools, and end-to-end packaging contracts) is set to grow in tandem or at least mirroring steel’s 8-10%+ annual expansion.

Steel Strapping Global Market

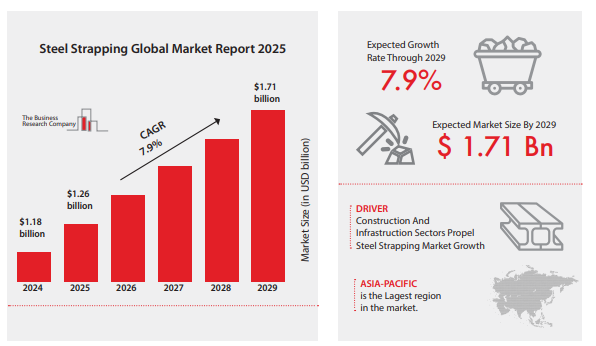

The global steel strapping market is a specialized, high-margin niche within industrial packaging, driven by the need for secure, high-strength bundling of heavy loads in steel, metals, construction, logistics, and manufacturing. High-tensile steel strapping offers superior durability and reliability compared to plastic or composite alternatives, making it indispensable where failure risks operational downtime or safety hazards.

According to The Business Research Company, the market reached $1.26 bn in 2025 (up from $1.18 bn in 2024) and is projected to grow to $1.71 billion by 2029 at a CAGR of 7.9%, with further extension toward $1.82 bn by 2030. Key drivers include robust expansion in construction and infrastructure sectors, rising global logistics volumes, and growth in metal, paper, glass, and building materials industries. Asia-Pacific dominates as the largest region in 2025, fueled by rapid industrialization, massive steel production (led by China and India), infrastructure megaprojects, and expanding manufacturing/export bases.

India Steel Strapping Industry

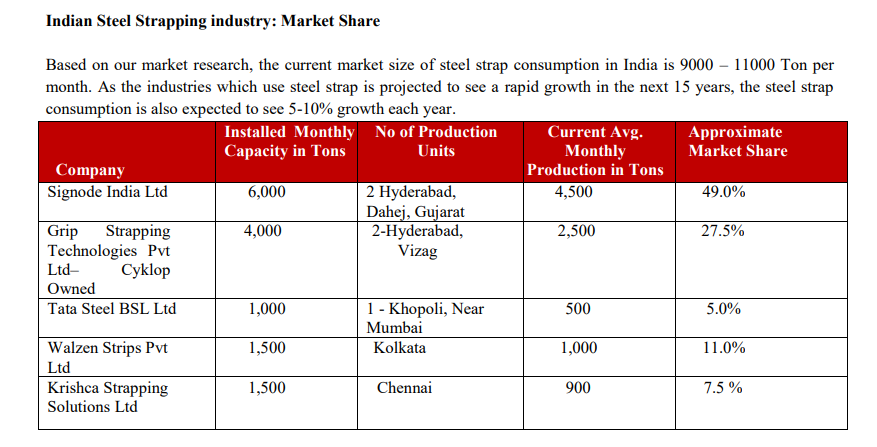

India’s steel strapping consumption stands at approximately 9,000–11,000 tonnes per month (~108,000–132,000 tonnes annually) as per Krishca Strapping Solutions Ltd DHRP. This aligns with India’s finished steel production and consumption scaling toward 150+ million tonnes in FY25.

The addressable market in value terms is estimated at ₹1,400-1,500 Cr annually (FY25 basis), The broader Indian steel packaging contract market (including end-to-end services) is pegged at ₹2,000-2,500 Cr per annum.

The Indian steel strapping industry is characterised by high entry barriers and concentrated profit pools, with only four meaningful manufacturers operating at scale. For nearly two decades, the industry effectively functioned as an oligopoly with just three players, reflecting the technical complexity, customer qualification requirements, and safety critical nature of the product. The structure has stayed broadly consistent since the Krishna Strapping Solutions Ltd’s Draft Red Herring Prospectus in early 2023, though Krishca has gained share through capacity expansion, quality differentiation now reflecting ~10% market share in recent investor materials (up from the ~7.5% cited in the DRHP and early estimates).

Key players and approximate shares (based on DRHP disclosures, management commentary, and cross-verified sources):

- Signode India Ltd (part of global leader Signode/Crown Holdings): ~49% market share, with ~6,000 tonnes/month installed capacity across units in Hyderabad and Dahej (Gujarat), producing ~4,500 tonnes/month on average. It remains the clear market leader with a strong legacy presence.

- Grip Strapping Pvt Technologies Ltd (subsidiary/associate of Germany-based Cyklop Group, a leading global player in packaging systems and materials since 1912): ~27.5% share, ~4,000 tonnes/month capacity across Hyderabad and Vizag, averaging ~2,500 tonnes/month production.

- Walzen Strips Pvt Ltd (Kolkata-based group, founded in 1989 by technocrat Mr. Tejomoy Roychowdhury and family-owned/operated entity focused on high-tensile steel strips and strapping): ~11% share, ~1,500 tonnes/month capacity in Kolkata, ~1,000 tonnes/month output.

- Tata Steel BSL Ltd – ~5% share, captive-focused (primarily internal use) with ~1,000 tonnes/month capacity near Mumbai/Khopoli, ~500 tonnes/month production.

- Krishca Strapping Solutions Ltd – ~7.5% share as per DRHP-era estimates (~1,500 tonnes/month installed capacity at Chennai facility, averaging ~900 tonnes/month production). Recent investor presentations and company overviews now show ~10% market share, reflecting gains from new lines (e.g., hardening/tempering for ultra-high tensile).

Management noted that the market itself is expanding at a healthy pace, with estimated industry growth of ~10-15% annually, driven by rising steel production, capacity expansions across major steel mills, and increasing adoption of packing contracts. Importantly, even as new capacity is added, customers continue to seek alternative suppliers beyond the incumbent multinational players, creating room for newer domestic manufacturers to scale without triggering aggressive price competition.

Indian Steel Strapping Industry – Key Dynamics & Krishca Strapping Solutions Ltd’s Positioning

What are the major entry barriers in the steel strapping industry?

The primary entry barrier is the rigorous product approval process, driven by the safety-critical nature of steel strapping. Coils weighing 10-25 tonnes (e.g., HR/CR coils) are secured using strapping; even a minor crack or failure can cause catastrophic accidents, fatalities, or severe mill downtime. Steel mills therefore treat vendor qualification with extreme caution. Approval typically takes 6-12 months (or up to 3 years for new entrants), involving extensive testing, trial supplies, and proven performance history. For public-sector undertakings (PSUs) such as SAIL or RINL (Vizag Steel), the bar is even higher. New suppliers must demonstrate private-sector purchase orders worth ₹10-15 Cr over the prior 2 years to even participate in tenders. Krishca Strapping Solutions Ltd supplied only to private mills until recently, when it participated in its first PSU tender in August 2025, having built the necessary credentials and track record. It successfully won the tender and began supplying to SAIL . This slow, credential-heavy qualification cycle creates a high moat, limiting new entrants and protecting incumbents.

Are there viable alternative materials to steel strapping in the steel industry?

No meaningful alternative exists for primary steel mill applications in the foreseeable future. Steel coils exit ovens at 200–300°C, requiring strapping that can withstand extreme heat without degrading. Plastic or composite strapping cannot handle these temperatures. In secondary/tertiary markets (smaller loads up to ~500 kg), touch-strapping or plastic bands are used, but they are unsuitable for heavy, hot-rolled, or high-value steel coils. Steel strapping remains the only reliable, high-tensile solution for mill-to-customer transport in the primary steel sector.

Why don’t large steel mills produce steel strapping in-house?

Steel mills have little incentive to backward-integrate into strapping due to complexity, scale mismatch, and focus on core competencies. Major players like JSW Steel operate 11-12 sites across India, each with unique packing needs i.e strapping thickness ranges from 0.4 mm to 1.27 mm, with 500+ combinations of width, finish, coating, and temper. A single site might consume only 10–20 tonnes/month of specific grades. Setting up dedicated lines for such fragmented, low-volume requirements would demand significant capex and management attention for marginal cost savings. Steel companies prioritize multi-crore projects; strapping is a small consumable relative to their ₹10+ lakh crore revenues.

Management draws a clear analogy – Just as a factory routinely purchasing cardboard boxes or packing tape (₹10-20 lakhs/month) would never invest in its own cardboard or tape manufacturing unit because it’s non-core, uneconomical, and diverts resources from the main business a steel mill treats strapping similarly. Their primary aim is steel production, not ancillary consumables. Outsourcing to specialized vendors ensures efficiency, competitive pricing, and supply reliability without distracting from core operations.

How is Krishca Strapping Solutions Ltd positioned versus peers?

Krishca Strapping Solutions Ltd is structurally differentiated through technology and cost leadership. It is currently the only lead-free steel strapping manufacturer in India and operates the country’s only fully automated, single-line, end-to-end production process (vs. competitors’ 2-3 step processes with higher manual intervention). This automation delivers the industry’s lowest production and labour costs. The Chennai facility’s proximity to the port provides logistical advantages and faster export turnaround compared with inland peers. Krishca Strapping Solutions Ltd’s backward integration into cold rolling (captive high/medium-carbon and stainless strips) will further strengthen raw material security and cost flexibility.

Why are Krishca Strapping Solutions Ltd’s margins higher than peers?

Krishca Strapping Solutions Ltd Superior margins are derived from automation, process efficiency, and raw material innovation. Production costs are reportedly less than 50% of competitors’, driven by lower labour intensity, energy-efficient induction-based furnaces (precise control from 300–700°C, allowing multi-grade processing on one line), and energy costs of ~₹2,000/tonne (vs. ~₹4,000/tonne for muffle-furnace peers). During COVID, focused R&D enabled qualification of alternate, structurally cheaper steel grades, delivering ~5-6% raw material cost savings. These factors combine to support consistently higher EBITDA margins.

What is Krishca Strapping Solutions Ltd’s pricing differential versus incumbent MNC players?

Krishca Strapping Solutions Ltd typically offers a ~5–6% discount versus multinational incumbents (especially outside PSU contracts, where legacy players historically command higher pricing). This advantage is rooted in Krishca Strapping Solutions Ltd’s lower structural cost base i.e automation, energy efficiency, reduced labour, and raw material flexibility.

What import barriers protect the domestic steel strapping market?

Imports are heavily restricted by mandatory BIS certification (under IS 5872 and the Steel QCO framework), required for any supplier to sell in India. Only one Korean company currently holds valid BIS certification globally, blocking most overseas players (especially from China). Additionally, an entry/Basic Customs Duty of ~7.5-10% applies, which creates a combined effective burden of ~18% (duty + compliance costs). This results in a ~20% price disadvantage for Chinese imports versus domestic levels,thus limiting imports to just 1-2% of the market . These barriers strongly favor local manufacturers and reduce substitution risk from cheap foreign supply.

Does Krishca Strapping Solutions Ltd have advantages in export markets?

Yes, Krishca Strapping Solutions Ltd enjoys greater geographic flexibility than incumbents. Signode’s regional allocation (e.g., Turkey/Korea plants restrict Indian operations from certain Middle East markets) and German competitors’ internal policies limit their reach, while Krishca Strapping Solutions Ltd, based near Chennai port, can price more competitively in regions like the Middle East. This enables selective export wins without intra-company restrictions.

However, aggressive competition from Chinese and Korean exporters in 2025 has created significant pricing pressure in key markets, leading Krishca Strapping Solutions Ltd to deliberately slow aggressive export plans. Management noted in H1 FY26 that competing with China/Korea is very difficult abroad, with export margins lower (10–12%) than domestic. As a result, the company has de-prioritized volume chase in exports and focusing instead on domestic growth.

Krishca Strapping Solutions Ltd Business Details

Historically (FY21-FY23), Krishca Strapping Solutions Ltd business was almost entirely driven by standalone steel strapping sales. Over the last 2 years, Krishca Strapping Solutions Ltd has evolved into a more integrated model with two distinct but synergistic verticals: steel strapping (core manufacturing) and packing contracts (service-led forward integration). Backward integration into cold-rolled coils (CRC) and diversification into primary packaging products (tarpaulins, dunnage bags, VCI films, desiccants, etc.) represent newer growth levers.

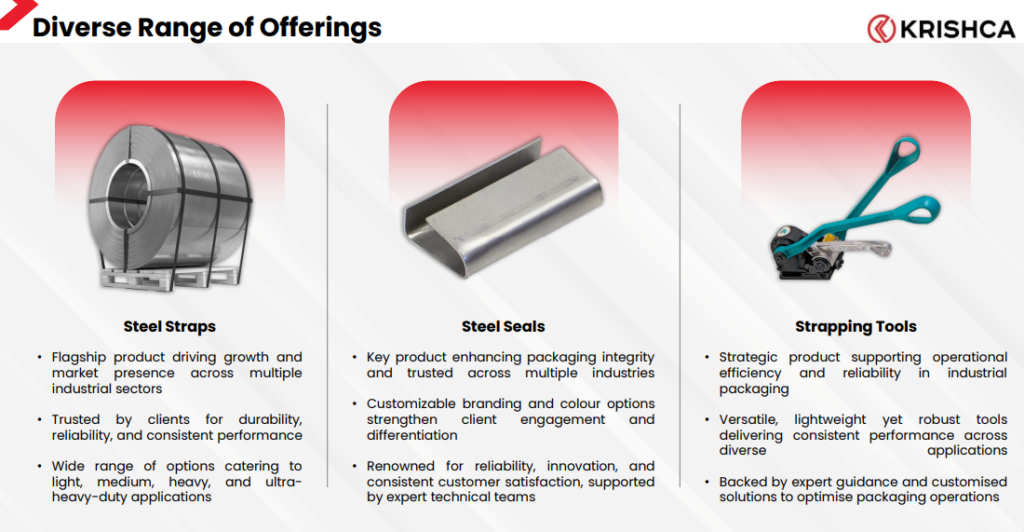

Steel strapping – Steel strapping is Krishca Strapping Solutions Ltd largest business segment, accounting for the bulk of revenues since inception and forming the base on which Krishca Strapping Solutions Ltd has built its customer relationships with primary and secondary steel producers.

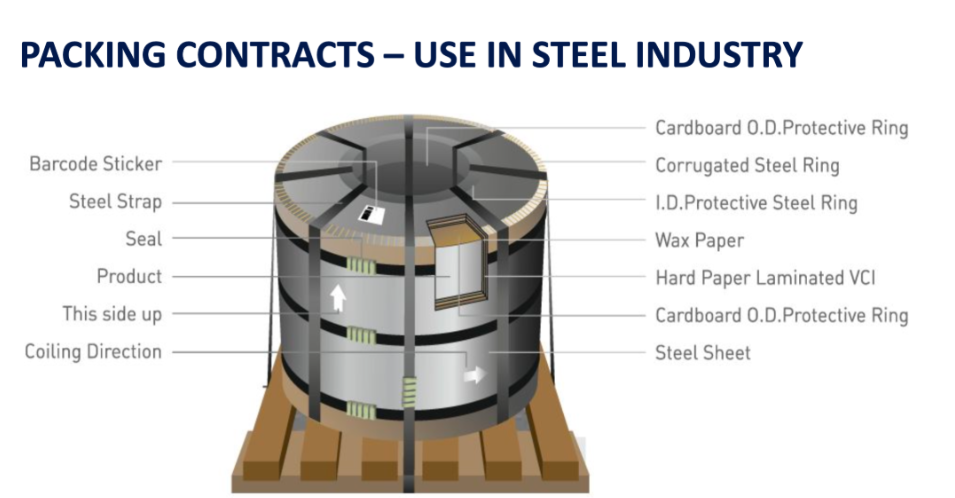

Krishca Strapping Solutions Ltd manufactures high-tensile steel strapping used for securing heavy loads in steel coils, TMT bundles, glass and construction materials, where product consistency and tensile performance are mission-critical.

Krishca Strapping Solutions Ltd operates a state-of-the-art integrated manufacturing facility in Chennai with an installed steel strapping capacity of ~30,000 MT per annum (increased from the initial ~18,000 MT through phased expansions and new hardening/tempering lines), along with in-house production of strapping seals and supply of strapping tools. This enables the company to offer customers a complete securing system rather than a standalone consumable product.

While reported utilisation of the existing strapping line was ~65% in H1FY24, management’s decision to add new capacity has been driven more by product capability constraints than by volume saturation. The earlier production line was not technically configured to manufacture ultra-high-tensile steel strapping with Ultimate Tensile Strength (UPS) exceeding 110, which is the fastest-growing segment of the market as steel producers increasingly migrate to higher-strength strapping to optimise logistics efficiency and reduce breakage risk. Management has indicated that ~30-40% of industry demand has already shifted to ultra-high-tensile grades, and this share is expected to increase further. The newly commissioned line is specifically designed to address this technology gap, allowing Krishca Strapping Solutions Ltd to participate in a structurally expanding sub-segment rather than merely adding incremental capacity to existing grades.

From a manufacturing standpoint, Krishca Strapping Solutions Ltd differentiates itself through its lead-free, environmentally compliant heat treatment process, which replaces conventional lead baths with a fluidized bed process using aluminum oxide, making the process safer, cleaner and more energy efficient. The production line is PLC-controlled and fully automated, allowing for tighter control over metallurgical properties and consistent grain structure, which is critical for ensuring tensile strength, elongation and shock resistance in high-load applications. The product portfolio spans multiple grades across regular duty, medium duty, high-tensile and ultra-high-tensile steel strapping, with finishes ranging from blued tempered and painted to zinc-coated variants depending on corrosion protection and end-use requirements.

On customer stickiness, management acknowledged that in certain TMT segments, particularly in central India, buyers may not exhibit strong brand preference as long as quality standards are met. However, Krishca Strapping Solutions Ltd has differentiated itself in the southern markets Tamil Nadu, Kerala, and Karnataka by offering custom-branded and coloured steel strapping along with branded seals, a capability currently limited to only a few manufacturers in India. This value-added offering has enabled the Company to build stronger relationships with secondary TMT manufacturers that place higher emphasis on branding, thereby enhancing customer retention.

Capacity & Manufacturing Footprint of Steel Strapping –

Krishca Strapping Solutions Ltd’s steel strapping operations are currently supported by two fully operational production lines at its Chennai facility, with the new strapping line commissioned and stabilised. The combined installed capacity stands at ~30,000 metric tonnes per annum, which management has indicated is sufficient to support ₹300-350 Cr of annual steel strapping revenue at steady-state utilisation, even without factoring in contributions from packing contracts or allied businesses. Importantly, the new line functions primarily as a dedicated heat-treatment line, while the existing line operates as the finishing line, implying that the two lines are operationally integrated and must run together to produce finished steel strapping. This configuration enhances metallurgical consistency and throughput but also means capacity utilisation is effectively governed at the integrated system level rather than as two independent lines.

In parallel ,Krishca Strapping Solutions Ltd has undertaken workflow optimisation initiatives, including relocation of certain strapping manufacturing activities to an adjacent facility to improve material movement, layout efficiency and throughput. To strengthen last-mile execution and customer servicing,Krishca Strapping Solutions Ltd has expanded its regional presence through branch offices and small warehousing setups in Jharkhand and Chhattisgarh, strategically aligned with key steel-producing clusters such as Odisha and the Raipur secondary steel market. These regional nodes support faster tool servicing, availability of critical spares and on-ground execution for packing contracts, thereby improving service reliability and response times for both standalone steel strapping customers and contract-based packaging clients.

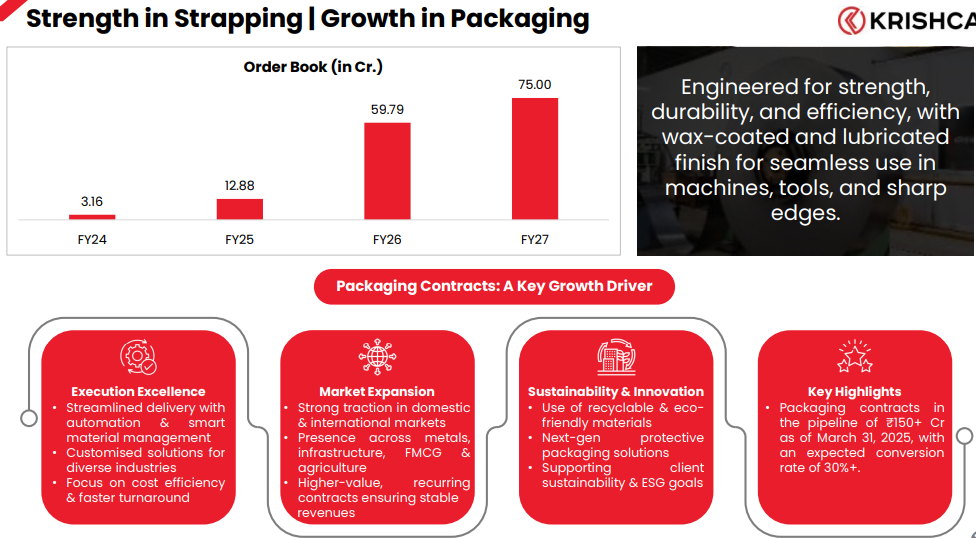

Packing Contracts – Krishca Strapping Solutions Ltd entered the packing contract business as a forward integration to structurally strengthen revenue visibility and protect its core steel strapping volumes as the steel industry increasingly migrates towards outsourced, end-to-end packaging solutions.

The packing contract market in India has historically been dominated by integrated steel strapping manufacturers such as Signode, given that steel strapping is the primary consumable in steel packaging. With in-house steel strapping manufacturing and an established strapping tools portfolio, Krishca Strapping Solutions Ltd identified packing contracts as an extension of its value chain, requiring incremental investment largely in manpower deployment, on-site execution and service management rather than in new manufacturing infrastructure.

A typical packing contract involves three key components i.e steel strapping, strapping tools and manpower deployed across multi-shift operations at steel plants. While Krishca Strapping Solutions Ltd already supplies the material and tools, the contract model allows Krishca Strapping Solutions Ltd to monetise manpower deployment, tool maintenance and site-level execution, i.e materially expanding the addressable revenue pool. Importantly, once a packing contract is secured, steel strapping offtake is assured for the contract tenure at pre-agreed commercial terms which reduces monthly volume volatility and dependence on frequent price renegotiations that characterise standalone strapping sales.

Packing contracts are typically long-term in nature, ranging from one to five years, providing improved revenue visibility and order-book stability. Management has indicated that an estimated ~50-60% of steel packaging volumes in the industry are increasingly being executed through contract models, which implies that participation in this segment is necessary to defend and grow core strapping market share.

From a financial perspective, packing contracts currently operate at margins broadly comparable to the steel strapping business, while offering a structurally larger revenue opportunity as steel strapping typically constitutes only ~50–60% of the total contract value, with the balance coming from manpower services, tool usage and maintenance. While initial margins may be similar due to higher manpower costs and site mobilisation expenses, management expects scope for gradual margin improvement as operations stabilise, learning curves improve and repeat contracts drive operating efficiencies. However, this model is structurally more working capital intensive due to higher receivables and on-site inventory, which is likely to lower the ROCE

Krishca Strapping Solutions Ltd began actively participating in packing contract tenders in FY24, acknowledging that early entry required building execution credentials. Following initial wins with Shyam Metallics (~₹2 crore) and its first PSU contract with SAIL Bokaro (~₹2.48 crore), Krishca Strapping Solutions Ltd secured a significantly larger contract with Vedanta (~₹20 crore) and subsequently added wins with APL Apollo (~₹3 crore) and CTEC, thus establishing a credible operating track record. Krishca Strapping Solutions Ltd is currently participating in multiple larger tenders, including contracts exceeding the Vedanta order value, which management expects to support meaningful scaling of this segment over the medium term.

Over the next three to four years, management aspires for packing contracts to contribute ~40-50% of consolidated revenues, reflecting both structural industry migration and Krishca Strapping Solutions Ltd’s expanding execution capability. As the contract business scales, management expects a moderate increase in working capital intensity, with receivable cycles extending by ~30 days due to longer billing timelines inherent in service-led contracts. Within the packing contract mix, non-strapping consumables are expected to account for an increasing share over time (~60–70%), with steel strapping contributing the balance.

Sourcing & Raw Material Risk Management

Krishca Strapping Solutions Ltd follows a diversified sourcing strategy comprising long-term, quarterly, spot, and import-based contracts, which provides flexibility across different commodity price cycles. A portion of raw material is secured under 6 month fixed-price contracts, while select suppliers operate on quarterly pricing arrangements where prices are locked for 3 months. In addition, Krishca Strapping Solutions Ltd maintains import relationships and selectively books volumes when global prices are favourable, while also utilising spot purchases during periods of soft domestic pricing. This sourcing approach allows management to optimise procurement costs across varying market conditions and partially smoothen raw material volatility.

On the sales side, Krishca Strapping Solutions Ltd manages raw material price volatility through industry-standard price variation clauses embedded in customer purchase orders. These clauses are typically linked to benchmark steel prices (such as hot-rolled coil prices) on a monthly or quarterly basis, which enables systematic pass-through of input cost fluctuations to customers. Management indicated that ~70% of contracts operate under variable pricing mechanisms, while the balance comprises smaller fixed-price contracts where the strapping component is relatively limited.

In fixed-price contracts, raw material exposure is structurally lower, as steel typically constitutes only ~30% of the overall contract value, with the remaining ~70% comprising fixed components such as manpower, tools, pallets, and service elements. In such cases, Krishca Strapping Solutions Ltd builds in a margin cushion at the bidding stage to absorb potential raw material price volatility. Labour costs are also contractually protected, with minimum wage revisions under state labour laws included as pass-through clauses in customer agreements, which ensures cost recovery in the event of statutory wage hikes.

Management acknowledged that in a declining steel price environment, reported revenues may moderate due to lower billing values, as pricing is linked to steel benchmarks. However, despite revenue volatility, operating margins are expected to remain broadly stable, as the business operates on a fixed-margin framework with systematic pass-through of raw material and labour cost variations.

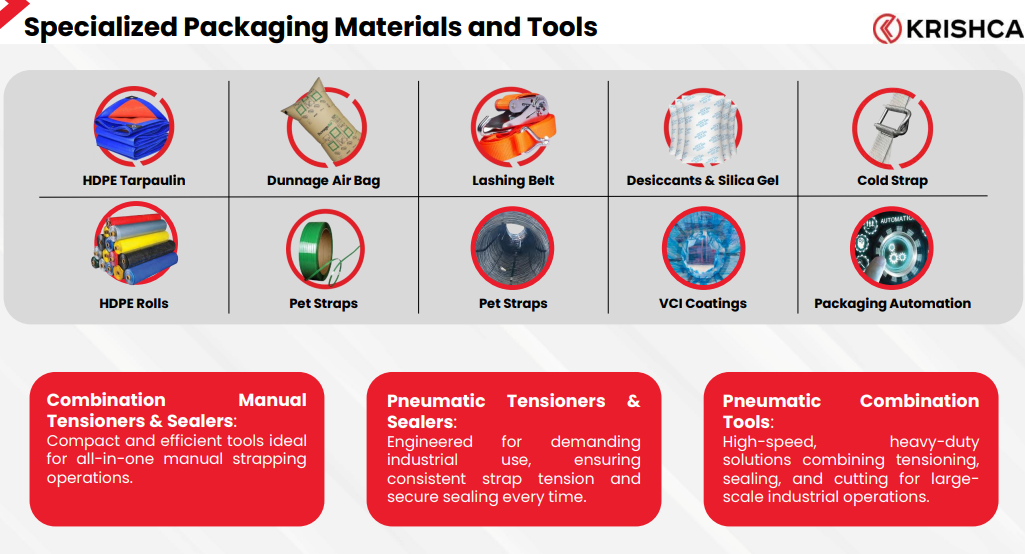

Primary Packaging – Primary packaging represents Krishca Strapping Solutions Ltd’s next leg of diversification beyond steel strapping and packing contracts. While Krishca Strapping Solutions Ltd’s core exposure remains linked to steel packaging, management has articulated a clear intent to expand into preservation-oriented primary packaging solutions that are complementary to steel strapping and deepen its engagement with existing customers.

Within steel mill packaging, steel strapping is only one component of the overall packaging requirement. A wide range of primary packaging materials such as HDPE and LDPE films, VCI (volatile corrosion inhibitor) packaging, desiccants, tarpaulins, lashing materials, and other protective plastics are required to prevent corrosion and physical damage during storage and transportation.

Since customers consuming steel strapping also require these allied products, primary packaging is a natural extension of Krishca Strapping Solutions Ltd’s product basket. Krishca Strapping Solutions Ltd has already begun offering several of these products, including through its export-facing operations, and leverages the same sales and technical teams to provide solution-led engagement with customers.

Management has highlighted that several primary packaging products offer superior margin potential compared to steel strapping, particularly where formulation-led value addition is involved. While commoditised plastic products such as standard LDPE films offer limited differentiation, the incorporation of corrosion-protection features such as VCI significantly enhances pricing power. VCI-based products, which require polymer engineering and chemical formulation capabilities, can generate operating margins of ~20%, materially higher than basic plastic packaging.

Krishca Strapping Solutions Ltd is currently investing in seven to eight different primary packaging product lines, supported by dedicated machinery. Management has indicated that with cumulative capex of ~₹8 crore, this portfolio has the potential to scale up to ~₹100 crore of annual revenue at full utilisation, with operating margins of around 20% over the medium term. A key growth driver within this segment is export-oriented packaging, where packaging intensity is structurally higher due to greater requirements for corrosion protection, lashing, and fabric-based protective solutions, which enables better value realisation per tonne of steel handled.

In terms of current scale, during H1 FY26, Krishca Strapping Solutions Ltd generated ~₹4.26 Cr of revenue from domestic primary packaging, accounting for ~5% of domestic revenues. Export primary packaging contributed an additional ~₹2 crore, taking total primary packaging revenue to ~₹6-6.2 Cr. At present, this business is largely trading-led with limited job work and minimal in-house manufacturing. To initially start, Krishca Strapping Solutions Ltd is setting up a desiccant manufacturing facility with ~₹2 crore capex and installed capacity of ~200 tonnes per month. Management expects the desiccant line to scale gradually, with revenue potential of ~₹20-25 Cr annually by the 3-4 year of operations.

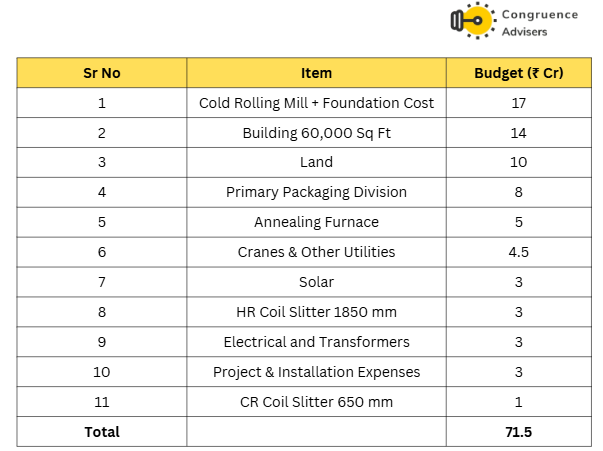

Cold Rolling Mill (CRM) – Backward Integration – Krishca Strapping Solutions Ltd is undertaking a major backward integration project through the commissioning of a Cold Rolling Mill (CRM) complex at its Chennai facility, marking an entry into steel manufacturing. with management guiding the installation starting in January 2026 and commercial operations by Q1FY2027. The CRM will have an installed capacity of ~5,000-6,000 tonnes per month, backed by an initial capex of ~₹60 Cr and 2 MW solar power plant to improve energy efficiency and operating economics.

The CRM is designed to serve a dual strategic purpose. First, it will support captive consumption for the steel strapping business, which currently consumes ~1,000-1,500 tonnes per month of medium-carbon steel. Management expects ~20-40% of CRM output to be used internally, translating into raw material cost savings of ~₹4,000 per tonne and a structural margin uplift of ~4-5% for the strapping segment, alongside lower inventory holding and reduced supplier dependency. Second, the balance ~60% of capacity will be directed toward external sales, focused on medium-carbon, high-carbon alloy steel and stainless steel, segments where domestic availability is limited, particularly in South India, and margins are structurally higher.

Given the wide price dispersion across steel grades (carbon steel at ~₹80–90/kg versus stainless steel at ~₹350–500/kg), management has guided that the CRM can potentially generate incremental revenues of ~₹250-350 Cr at steady-state utilisation. The ramp-up is expected to be gradual, with ~20% utilisation from the first month driven by captive demand and ~35–40% utilisation by the end of the first year, followed by phased debottlenecking and incremental capex to scale capacity over time. Importantly, the CRM is being built as a flexible platform rather than a one-time project, with scope to add downstream processing equipment and expand into higher-value product categories on a staggered basis.

Forward Integration into Specialty & Super Alloys (Vajra Alloys)

Building on the CRM platform, Krishca Strapping Solutions Ltd is also pursuing measured forward integration into specialty and super alloys through a newly approved subsidiary, Vajra Alloys. The initial investment is modest at ~₹7 crore, funded largely at the subsidiary level through a mix of debt and equity capital. Over the first 1-2 years, the focus will be on commercial and industrial applications, where qualification timelines are shorter and technical criticality is lower, before gradually moving into higher-end defence, aerospace and space applications.

Management highlighted that the CRM infrastructure is already capable of processing thin precision strips (up to ~0.1 mm thickness) in high-carbon and stainless steel, a segment where India remains structurally import-dependent. Over time, the same rolling infrastructure can also be used to cold-roll super alloy plates into precision strips without major equipment modifications. While the overall super alloy market in India exceeds ₹10,000 Cr annually, Krishca Strapping Solutions Ltd has initially identified a ~₹1,000 Cr addressable sub-segment with confirmed customer interest. Krishca Strapping Solutions Ltd has already engaged with potential customers over the past 6-12 months and onboarded industry experts with 30+ years of experience in stainless steel and high-carbon alloys to de-risk execution and accelerate capability building.

Exports and Global Expansion

Krishca Strapping Solutions Ltd’s initial bullishness on global expansion, particularly in the Middle East (Dubai) was driven by the structural characteristics of the regional steel ecosystem. The Middle East is largely import-dependent for packaging consumables such as steel strapping and primary packaging materials, with most supplies coming from China and Korea. Management identified a gap for a local, solution-oriented packaging partner, as opposed to pure commodity exporters. The Dubai subsidiary, incorporated in September 2023, was set up as an asset-light trading and sales-support platform to diversify offerings beyond steel strapping into primary packaging and preservation solutions. The low cost nature of the Dubai setup (free-zone entity, minimal fixed assets) allowed Krishca Strapping Solutions Ltd to test demand without committing large capital, and management had initially guided for the Dubai entity to contribute ~20% of revenues, supported by perceived advantages of local presence and India-UAE CEPA duty benefits.

In parallel, management explored the possibility of setting up overseas manufacturing in the Middle East to address two key structural issues: long lead times from China and the absence of an integrated local packaging solutions provider. Customers in the region typically face waiting periods of up to two months after advance payments to Chinese suppliers, which creates operational and working-capital challenges. A local manufacturing presence, potentially through a joint venture, was envisaged to offer faster turnaround, on-ground service support, consulting, and automation-led packaging solutions. Management had indicated a Middle East steel strapping market size of ~₹300-400 Cr and a potential gateway for future expansion into the US market.

However, over the last 12-18 months, export market economics have deteriorated materially, leading management to adopt a more cautious stance on global scale-up. Chinese and Korean competitors have become increasingly aggressive on pricing due to lower raw material costs and excess capacity, along with higher shipping costs due to disruptions in the Red Sea, which directly compressed export margins. Management acknowledged that despite having customer demand, Krishca Strapping Solutions Ltd is either losing orders or consciously walking away from business purely on pricing grounds, not due to demand constraints. As a result, export EBITDA margins in exports are currently in the ~10-12% range, significantly lower than domestic margins.

Reflecting this margin pressure, exports declined to ~₹8.8 crore in H1 FY26 compared to ~₹23 crore in FY25. Management has guided for only ~15–20% organic growth in exports and has clarified that it is not aggressively pursuing export-led volume expansion at the cost of profitability. Additionally, unlike India, the Middle East does not operate on a packing contract model due to high manpower costs and visa constraints, which further limits Krishca Strapping Solutions Ltd’s ability to replicate its higher-visibility, service-led domestic business model in the region.

Going forward, Krishca Strapping Solutions Ltd plans to remain selective in exports, participating only where pricing is viable. Management expects incremental cost support from the upcoming Cold Rolling Mill (CRM), which could improve raw material economics and competitiveness in certain export markets. Krishca Strapping Solutions Ltd is also exploring a distribution-led approach in smaller overseas markets such as Bangladesh, Sri Lanka, Africa, Australia, and parts of Europe for low-ticket orders, while retaining direct engagement for large-volume customers. In the US, despite a steep 45% anti-dumping duty, Krishca has already executed ~₹1 Cr of exports with repeat orders, though large-scale US expansion remains constrained by pricing and trade barriers.

Krishca Strapping Solutions Ltd Financial Performance

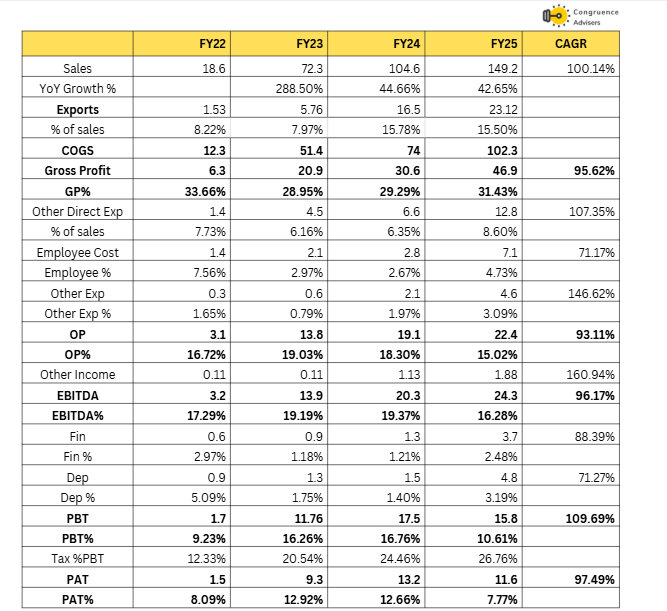

Krishca Strapping Solutions Ltd has scaled well from FY21 to ₹150 Cr in FY25, This growth has been driven by rapid volume ramp-up in steel strapping, onboarding of large customers, and gradual scaling of packing contracts and exports.. Exports contributed steadily, growing at 33.3% CAGR to ₹23.12 Cr in FY25 (15.5% of sales), though management noted in H1 FY26 investor call that aggressive Chinese/Korean competition subdued volumes, leading to prioritization of domestic markets. Gross profit expanded at 95.6% CAGR to ₹46.9 crore in FY25, with gross margins holding stable at 29-33%, supported by operating leverage, R&D led raw material optimizations (5-6% cost savings from alternate steel grades, as highlighted in FY24 concall).

At the operating level, EBITDA increased from ₹3.2 Cr in FY22 to ₹24.3 Cr in FY25, translating into a ~96% CAGR. EBITDA margins, however, show a mild compression from 19-19.4% in FY23-FY24 to ~16.3% in FY25. This moderation is due to a combination of higher employee costs (employee cost rising to ~4.7% of sales in FY25 from ~2.7% in FY24), increased operating overheads associated with scaling packing contracts, branch expansion and organisational build-out, as well as relatively lower-margin export contribution.

PAT grew from ₹1.5 Cr in FY22 to ₹11.6 Cr in FY25, representing a ~97% CAGR. However, PAT margins declined to ~7.8% in FY25 from ~12-13% in FY23-FY24, primarily due to higher depreciation, higher finance costs and higher tax outgo as the Krishca Strapping Solutions Ltd transitioned into a stable profitability phase. Despite this, absolute profit growth remains healthy, which indicates that the underlying operating engine continues to scale.

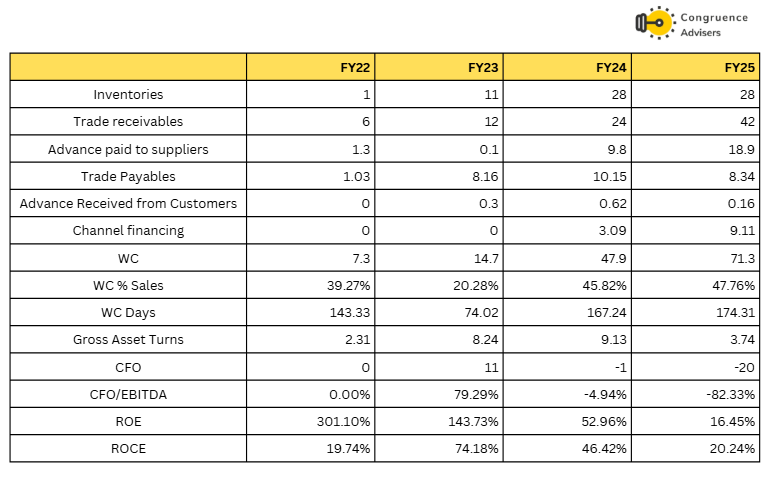

Krishca Strapping Solutions Ltd Working Capital, Return ratio and Cash conversion

Krishca Strapping Solutions Ltd working capital intensity has increased sharply with WC days rising to ~174 days in FY25, driven by both higher receivables from packing contracts and a deliberate build-up of inventory. Management has indicated that inventory levels were elevated as they opportunistically stocked steel during periods of lower prices to protect margins and also maintained buffer inventory to support multi-site packing contracts, which require material availability at customer locations. This has also adversely impacted cash conversion, with CFO turning negative in FY24-FY25 despite healthy EBITDA growth, as cash is locked in inventory and receivables. Return ratios have moderated in the near term, with ROCE declining to ~20% in FY25 because of low gross asset turn due to new capacities. Management expects partial normalisation of inventory intensity post backward integration (CRM), which should enable on-demand processing and reduce the need to hold multiple finished-strip variants.

Krishca Strapping Solutions Ltd Comparative Analysis

To understand Krishca Strapping Solutions Ltd investment potential, we have conducted a comprehensive analysis. This analysis includes comparing Krishca Strapping Solutions Ltd to its competitors (peer comparison) on various fundamental parameters and Krishca Strapping Solutions Ltd share performance relative to relevant benchmark and sector indices.

Krishca Strapping Solutions Ltd Peer Comparison

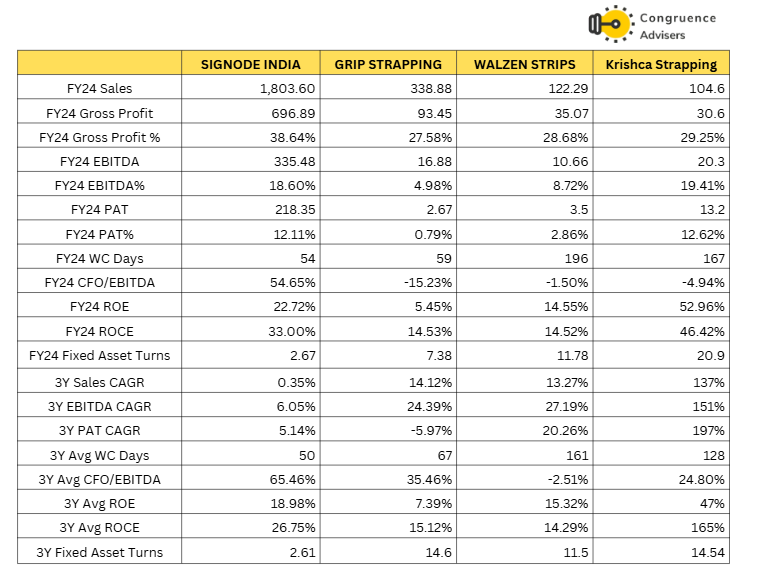

To benchmark Krishca Strapping Solutions Ltd’s performance and positioning, we have compared it with the key unlisted peers in the Indian steel strapping market – Signode India (market leader), Grip Strapping, and Walzen Strips. Since these peers are unlisted, detailed financials are available only up to FY24; hence, the comparison uses FY24 numbers for consistency.

Signode India is the largest player with an estimated topline of ~₹1800 Cr ( approx 900-1000 cr for steel strapping and packaging contract business) and pioneered the packing contract model in India. It operates as a diversified packaging solutions provider (strapping, plastics, automation, contracts), with broader exposure than pure strapping players. Most other competitors generate revenues in the ₹200-400 cr range

Signode India is part of the global Signode Industrial Group (industrial packaging division), which was earlier owned by Illinois Tool Works (ITW, USA) and subsequently acquired by Crown Holdings Inc. from The Carlyle Group in April 2018. Crown is a large global packaging major with a diversified portfolio across consumer and transit packaging, and Signode operates as Crown’s industrial packaging arm, with a broad product suite spanning steel strapping, PET strapping, tools, automation and transit packaging solutions (airbags, edge protectors, etc.). As a result, Signode’s India business benefits from strong parentage, global technology access which is reflected in its scale (FY24 sales ~₹1,800 Cr), superior gross margins (~39%) and stable working capital profile (~50–55 WC days). Importantly, Signode India is not a pure-play steel strapping company only 50% of revenues is derived from steel strapping and packaging contract business

Grip Strapping Technologies (GSTPL) is an associate of the Germany-based Cyklop Group, one of the leading global players in packaging systems and consumables. GSTPL benefits from technical know-how and long operating history of its promoter-management team, with deep domain expertise in packaging machinery and materials. However, at the India level, Grip remains relatively smaller in scale compared to Signode and has structurally lower margins, which reflects a more limited product breadth.

Walzen Strips Pvt. Ltd. (WSPL), part of the Kolkata-based Lyka Group, operates as a domestic, privately-held manufacturer of high-tensile and hardened tempered steel strips, with limited presence beyond steel strapping and job work. Based on publicly available credit rating commentary, the promoter group appears relatively conservative in capital deployment, and the business has not pursued aggressive capacity expansion or product diversification over the years, which is reflected in lower scale, weaker cash flow conversion and periodic non-cooperation remarks in credit reports.

Krishca Strapping Solutions Ltd, while still a young company (operational scale-up largely over the last 4-5 years), has achieved revenue growth and margin metrics that are directionally comparable to global peers at the operating margin level. However, Krishca Strapping Solutions Ltd’s key differentiator is its high-growth phase, reflected in significantly higher CAGR metrics, albeit at the cost of stretched working capital and weak operating cash flow conversion relative to incumbents. Krishca Strapping Solutions Ltd’s financial profile currently reflects a scaling domestic platform, where profitability growth is visible but cash conversion and working capital discipline remain key execution variables.

Why You Should Consider Investing in Krishca Strapping Solutions Ltd ?

Krishca Strapping Solutions Ltd offers some interesting reasons to track closely and to consider investing if one is looking to play India’s steel capex cycle.

Proxy on India’s Steel Capex Supercycle – India is the world’s 2nd largest steel producer (~151 MT crude in FY25) and is targeting 300 MT capacity by 2030 under the National Steel Policy. This implies a sustained 7-10% CAGR in steel production and consumption for the next 5-10 years, driven by infrastructure (Gati Shakti, NIP), housing, automotive, exports, and manufacturing localization. Steel strapping and packaging are non-discretionary consumables tied directly to finished steel output and movement. Krishca Strapping Solutions Ltd sits in the sweet spot of this chain. Every additional tonne of steel produced/consumed requires reliable strapping and packaging. With domestic consumption already at ~150 MT and growing 9-11% YoY, ancillary demand (strapping + contracts) is structurally expanding at similar or higher rates, which provides Krishca Strapping Solutions Ltd with a medium term, high-visibility growth runway without needing to chase new end-markets.

Forward Integration into Total Packaging Solutions – The Indian steel packaging market is rapidly moving toward outsourced end to end contracts (already ~50–60% of volumes), led by integrated players like Signode. Krishca Strapping Solutions Ltd has executed this transition exceptionally well as packing contracts scaled from ₹3.16 cr in FY24 to ₹12.88 cr FY25 and now at ~₹30 cr as on H1 FY26 (~33% of revenue). Packaging contracts lock in strapping offtake for 1-5 years, expand wallet share 3-5x (manpower + tools + maintenance contribute 50-70%), and provide recurring revenue, order-book at ₹180 cr+ as of Nov 2025. Management targets 40-50% revenue contribution from Packaging contracts in 3-4 years, which should improve revenue predictability, reduce cyclicality, and lift blended ROCE as execution matures. This is classic forward integration by leveraging the core product to capture higher-margin services.

High Barriers to Entry – Steel strapping is not a commoditized product. It is safety-critical. A single strap failure on a 10-25 tonne coil can cause fatalities, mill downtime costing lakhs per hour, or massive product damage. This creates an extremely high bar for vendor approval (6-36 months of trials, proven track record, private-sector POs for PSU entry). The market remains oligopolistic (Signode ~49%, Grip/Cyklop ~27.5%, others smaller), with minimal imports risk (1-2%) due to mandatory BIS certification and ~7.5-10% import duties with compliance costs creating an effective ~18-20% landed disadvantage for Chinese material. Krishca Strapping Solutions Ltd has already crossed this moat, it is the only lead-free manufacturer, operates the only fully automated single-line process, and has now entered PSUs (SAIL Bokaro, RINL) after years of private-sector validation. This combination of technical reliability, cost leadership, and credential accumulation makes customer switching very difficult and new entrant success rare.

Diversification into Primary Packaging – Beyond its core steel strapping franchise, Krishca Strapping Solutions Ltd is strategically expanding into complementary primary packaging and preservation products to position itself as a one-stop solution provider for industrial packaging needs. Krishca Strapping Solutions Ltd is investing in the manufacturing and sourcing of desiccants, VCI-based corrosion protection covers, tarpaulins and dunnage air bags. Products that are increasingly critical in steel logistics, export packaging and moisture-sensitive applications. This broadening of the product basket enables Krishca Strapping Solutions Ltd to meaningfully increase its share of wallet with existing customers as procurement increasingly shifts from multiple vendors to integrated solution providers. Over time, this diversification is expected to deepen customer stickiness, improve revenue visibility and support margin resilience, as value-added preservation products typically carry higher realisations and are less commoditised than plain steel strapping.

Backward Integration into Cold Rolling Mill – Krishca Strapping Solutions Ltd is undertaking a meaningful capacity addition through backward integration through the commissioning of a ~60,000 TPA Cold Rolling Mill complex at its Chennai facility (commercial operations targeted by Q1 FY27), which will meaningfully strengthen its competitive moat by lowering input costs through partial captive sourcing. Beyond improving the economics of its core steel strapping business, the CRM enables Krishca Strapping Solutions Ltd to enter higher value-added segments such as precision-gauge specialty steel and select stainless-steel strips which will open a new revenue stream from automotive, engineering and tooling customers who currently rely on imports or premium domestic suppliers. In parallel, through its subsidiary Vajra Alloys, Krishca Strapping Solutions Ltd is selectively entering the super alloys and special steels segment initially targeting commercial and industrial applications (later moving into moving into more critical end-markets over time), which we believe will materially expands the addressable market and provides value migration optionality

What are the Risks of Investing in Krishca Strapping Solutions Ltd ?

Investors need to keep the following risks in mind if they choose to invest into this business. Risks needs to be weighed in combination with the advantages listed above to arrive at a decision that is optimal for your portfolio construct

High Dependency on the Steel Industry – Krishca Strapping Solutions Ltd’s revenue is almost entirely linked to the Indian steel sector (major customers: Tata Steel, JSW Steel, SAIL, Vedanta, APL Apollo, etc.). Any slowdown in steel production, consumption or capex (due to global slowdown, weak infrastructure spending, real estate downturn, or monetary tightening) directly impacts strapping and packaging contract volumes. Steel is a highly cyclical industry, even moderate demand softness can lead to sharp order deferrals or inventory correction at mills, which could impact Krishca Strapping Solutions Ltd’s.

That said, the probability of this risk crystallizing in a severe way over the next 3-5 years appears very low given the current health and structural outlook for the Indian steel industry.

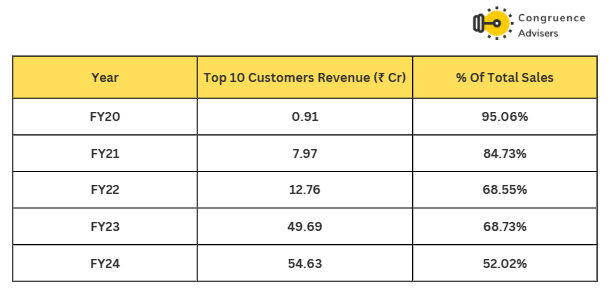

Customer Concentration Risk – A significant portion of Krishca Strapping Solutions Ltd revenue comes from a handful of large steel producers (top 10 account for 50%+ of sales). Any loss of a key contract, reduction in offtake, vendor re-rating, or shift to competitor supply by a major client would have an outsized impact on revenue and profitability. While packing contracts increase stickiness, they are still concentrated among a few large steel plants.

That said, Krishca Strapping Solutions Ltd has steadily reduced this concentration over the years from ~95% top-10 contribution in FY20 to 52% in FY24, and an estimated ~50% in FY25. However, further meaningful reduction beyond ~40-50% is unlikely in the medium term, as the Indian steel industry is inherently concentrated with the top 5-6 producers accounting for ~55-60% of total crude steel output . Majority volumes are dominated by these giants, which limits Krishca Strapping Solutions Ltd’s ability to fully de-risk without sacrificing access to the largest demand pools

Execution Risk with capex – Krishca Strapping Solutions Ltd is undertaking a capex of ₹70 Cr+ for the Cold Rolling Mill (CRM) complex and primary packaging diversification. This represents a substantial commitment relative to the Krishca Strapping Solutions Ltd’s existing gross block of ~₹40 Cr as of FY25.

Any delay in commissioning the CRM, capex overruns, technical challenges in achieving desired quality/grades, or slower-than-planned ramp-up could materially erode the expected cost savings, product expansion, and new revenue streams currently anticipated. Parallel execution risks exist in primary packaging diversification (desiccants, VCI covers, tarpaulins, dunnage airbags,), where the company is investing in manufacturing/sourcing and integration. Although capex here is smaller, risks include integration delays, higher than expected setup costs, slower client adoption for bundled solutions, or quality/market acceptance issues. All of which could dilute near-term performance.

These execution risks are typical for a fast-growing SME undergoing major capex and diversification, but they are critical to monitor through quarterly updates on progress, timelines, and capex utilization. Any meaningful slippage would directly impact the growth and thesis.

The CRM project also introduces material market risk. While the stated strategic intent is backward integration for captive consumption, management has indicated that ~60% of CRM output is targeted for external sales, effectively turning them into a merchant supplier of special steels. This exposes them to cyclicality and pricing volatility in the broader steel market.

Working Capital Intensity from Packing Contracts – As packing contracts scale (target 40-50% of revenue), working capital requirements will increase significantly due to higher receivables (billing cycles ~90 days vs. 45–60 days for standalone strapping) and manpower related advances. This could pressure cash flows and return ratios in the near-to-medium term, especially if contract wins accelerate faster than collections or if customers delay payments (common in PSU contracts).

Liquidity Risk – As a relatively microcap company listed on NSE Emerge (SME segment), Krishca Strapping Solutions Ltd has limited trading liquidity and higher price volatility compared to mainboard stocks. Any negative news, broader market correction can lead to sharp drawdowns, even if fundamentals remain intact.

Export Market Risk – While exports are currently small ( at 9.5% in H1FY26 vs 15% in FY25), aggressive Chinese and Korean competition has already forced Krishca Strapping Solutions Ltd to slow its international push. Export realisations and margins are structurally lower than domestic business, with management indicating EBITDA% of 10-12% in exports vs materially higher margins in the domestic segment. Any renewed strategic push to scale exports could therefore dilute blended margins and expose Krishca Strapping Solutions Ltd to heightened competitive intensity, freight cost volatility and geopolitical/logistics risks. In addition, export volumes are more sensitive to global steel cycles and pricing arbitrage, which may introduce incremental volatility to earnings quality if the export mix increases meaningfully over time.

Promoter led Strategy & Capital allocation risk – Krishca Strapping Solutions Ltd remains a promoter-led and promoter-driven enterprise, with the founder playing a central role in strategy formulation and capital allocation. While the promoter has shown credible execution by scaling the Company from near-zero revenues in FY20 to ~₹151 cr in FY25 and securing Tier-1 customers, his entry into the steel strapping and industrial packaging space was without prior domain experience. This introduces a risk around strategic consistency and capital deployment, particularly in a capital intensive manufacturing context. The direction has shifted multiple times post IPO for example the welding electrode plant and a plan for a steel strapping facility in the Middle East were dropped, while the current focus is on CRM backward integration and primary packaging diversification. Frequent changes in announced initiatives, though common in young companies adapting to markets, raise questions about long term clarity and execution discipline.

Competitive Intensity & Pricing Pressure Risk – Krishca Strapping Solutions Ltd operates in a highly concentrated market dominated by established multinational players such as Signode and Grip, which possess strong customer relationships, global brand and the ability to bundle products and services. As Krishca Strapping Solutions Ltd continues to target incremental market share gains over the medium term, these incumbents may respond through more aggressive pricing or bundled offerings to defend their positions. Such competitive responses could trigger pricing pressure or localised price wars. Which can potentially compress margins and slow the pace of profitable market share expansion. While Krishca Strapping Solutions Ltd’s structurally lower cost base provides some buffer, sustained competitive intensity remains a key risk to monitor.

Krishca Strapping Solutions Ltd Future Outlook

Krishca Strapping Solutions Ltd management guiding for a minimum 25% YoY revenue growth in FY26 (moderated from earlier 40%+ estimates in H1 FY26 concall, reflecting cautious export assumptions and capex ramp-up),revenue growth in the near term will be driven by higher utilisation of the expanded steel strapping capacity, onboarding of new packaging contracts and incremental contribution from primary packaging. In steel strapping, management expects ~20-25% volume growth over the next 1–2 years, driven by increased penetration across Tier-1 and secondary steel mills and gradual migration to higher-tensile grades. With installed capacity of ~30,000 TPA, the strapping business alone has the potential to support ₹300Cr+ of annual revenue at steady-state utilisation, which provides a visible medium-term scaling runway as utilisation moves up from current levels.

Packaging contracts are expected to remain a key growth lever, with management indicating an aspiration for contracts to contribute ~40-50% of consolidated revenue over the next few years which will be supported by multi-year tenders from large steel producers. While this provides revenue visibility, it also structurally increases working capital intensity, making execution and collections key monitorables.

Primary packaging (desiccants, VCI covers, tarpaulins, dunnage air bags) is currently a small but fast-growing vertical. Management has indicated that, with ongoing investments in manufacturing (including desiccants) and broader product rollout, this vertical has the potential to scale to ₹80-100 Cr of annual revenue over the medium term at maturity, supported by cross-selling into the existing steel customer base and higher usage in export packaging and corrosion-sensitive applications. This segment also carries relatively better realisations than plain steel strapping.

The commissioning of the CRM complex is expected to be the next structural growth and margin inflection point. Management has guided that the CRM can support ₹250-350 Cr of incremental revenue potential at steady state, with ~30–40% captive consumption for steel strapping inputs and the balance targeted at external sales of medium/high-carbon and select stainless-steel precision strips to automotive and engineering customers. Over time, backward integration is expected to support margin stability through cost savings and lower inventory intensity, while also creating a new materials-led growth engine beyond packaging.

While the growth narrative is compelling, the strategic roadmap has evolved post-IPO with certain initiatives (welding electrodes and overseas strapping manufacturing in the Middle East) being de-prioritised. This introduces a risk around strategic consistency. Our channel checks suggest that overseas manufacturing in the Middle East remains still in promoter mind.

The key to value creation over FY26-FY28 will be disciplined execution across the current pillars i.e steel strapping scale-up, packaging contract monetisation, primary packaging ramp-up and timely CRM commissioning along with improvement in cash flow conversion as the heavy capex phase tapers.

Krishca Strapping Solutions Ltd Technical Analysis

We consider technical analysis to be a useful input in taking medium-term investment decisions. Many a time price action tends to lead to fundamental developments; this is too important an aspect to be ignored by retail investors who do not have access to management outside of common forums like investor calls & AGM.

At Congruence Advisers we like to consider both the long-term weekly chart and the daily chart to arrive at a view on price action. Combined with our understanding of fundamentals, we usually end up being better placed to be able to judge both the business cycle and the stock cycle. Playing the stock cycle right is extremely important for investors looking to extract significant alpha over the medium term.

Krishca Strapping Solutions Ltd Price charts

Krishca has a listed history of less than 3 years, so taking a look at the weekly chart should give us the entire picture. After consolidating between 200-285 for close to a year between H2 CY23 and H1CY24, the stock went up 70% in a couple of weeks in June 2024 following the H2 FY24 conference call, presumably due to optimism around rapid business growth which was being projected by management. The stock peaked with the broader markets in Sep ‘24, managed to stay above the support level of 285 till Jan ‘25, when it broke in line with a huge downturn in the Indian markets. Since then the stock bounced between the two levels of 200-285 for most of CY25 before breaking the support level of 200 in November 2025, again with a downturn in the Indian markets. It has since been trading in a tight band between 180-200 levels. With the market now paying attention to balance sheets and cash flows, the stock may not move up very swiftly unless cash flows improve significantly and growth returns. While the immediate resistance level of 200 might get taken out with positive H2 FY26 earnings, the next resistance level of 285 will be breached only when the market is convinced that there is clarity on medium term growth and balance sheet health.

Krishca Strapping Solutions Ltd Latest Latest Result, News and Updates

Krishca Strapping Solutions Ltd Quarterly Results

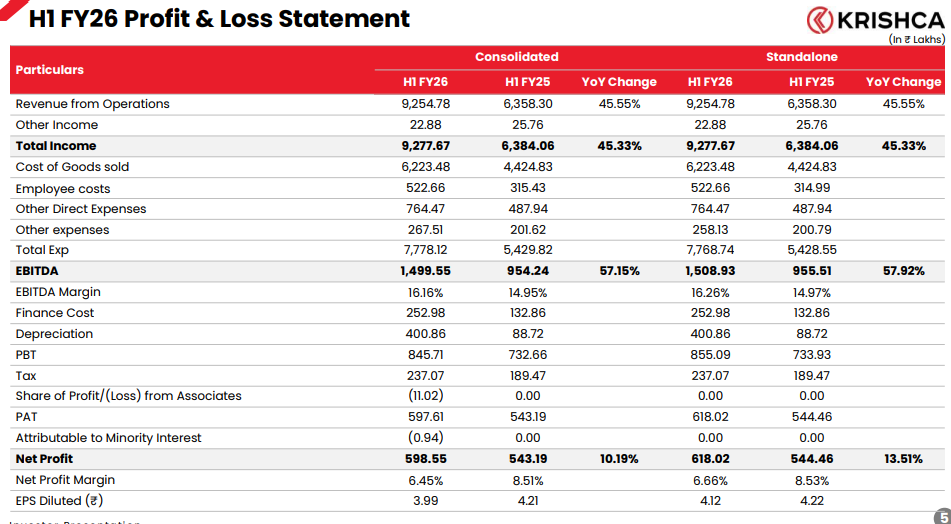

Krishca Strapping Solutions Ltd printed a robust performance in H1FY26 with consolidated total income growing 45.3% YoY to ₹92.78 crore from ₹63.84 crore in H1 FY25. (Standalone results were similar, as there was no material subsidiary contribution yet) Revenue from, while EBITDA surged 57.2% to ₹14.99 crore with margins expanding to 16.2% from 14.95%. Net profit grew 10.2% to ₹5.99 crore, though margins dipped slightly to 6.45% due to higher depreciation and finance costs from ongoing capex.

Operational and strategic updates from the H1FY26 concall

- Packing contracts scaling sharply to ~₹30 Cr (33% of revenue), up significantly YoY, with an order book exceeding ₹180 Cr.

- PSU entry is progressing well, with contributions from SAIL Bokaro and RINL/Vizag Steel contracts.

- The CRM project remains on track, with installation starting in January 2026 and commercial production expected in Q1FY27.

- Primary packaging (desiccants, VCI, tarpaulins, airbags) is ramping up to increase wallet share in contracts.

- Exports remain subdued at >10% due to aggressive Chinese/Korean competition, with management prioritizing domestic growth through contracts and CRM.

- Guidance has been moderated to a minimum 25% YoY revenue growth for the full year (down from earlier 40-50% expectations), with packing contracts targeting 40-50% of total revenue in 3-4 years and CRM delivering margin/ROCE uplift from FY27.

Final Thoughts on Krishca Strapping Solutions Ltd

Krishca Strapping Solutions Ltd is a great example of an enterprising, young promoter with no business background identifying a niche gap in the market and successfully executing to capture a sizable share of the market. What the young promoter has been able to do since founding Krishca Strapping Solutions Ltd in 2017 is commendable. He and his team have managed to put Krishca Strapping Solutions Ltd on the same level as decades old multinationals in the steel strapping industry.

However, as is often the case with young, ambitious promoters who have tasted success, it is easy to overreach. It appears to us that they are trying to do too many things too soon and all at once. Getting into packaging contracts from steel strapping was a natural step. Although ROCE dilutive, it would allow them to capture additional profits that would otherwise go to 3rd party service providers. The entry into plastic packaging items can also be justified owing to the fact that the packaging items are consumables used in steel packaging contracts and the fact that the quantum of capex needed is small (< 10Cr). However, we find it really tough to get behind their backward integration into steel. The capex risk is sizable (The capex itself is 150% of their FY25 gross block), Krishca Strapping Solutions Ltd does generate positive operating cash flows and only 20-40% is backward integration with the rest of the output being exposed to the volatile open market of steel products. We feel this is a risk that could have easily been avoided. The promoter’s persistent vision to set up capacity in the Middle East (Although not in the plans immediately) also feels like a potential overreach to us at this stage and size of their journey.

At the size Krishca Strapping Solutions Ltd is at, a couple of big mis-steps in capital allocation can put the future of the company at risk. While it is true that there can be no big winners without taking big risks, when these risks could potentially be existential, one should be very careful. Their constant search for new avenues of growth also suggests to us that the TAM in their core business of steel strapping may not be very big. We believe that the competitive landscape in the steel strapping segment is not conducive to aggressive market share gain by Krishca Strapping Solutions Ltd. There are well entrenched players who are much older and operate at larger scale compared to Krishca Strapping, this puts a lid on the revenue growth of the business in its core segment.

Krishca Strapping Solutions Ltd may have to go fishing in uncharted waters if it wants to grow aggressively, which is not the ideal setup when investing in microcaps in our opinion. Microcap investing works best when the business in question has already hit upon a reliable growth template that can be replicated over the next 3-5 years at low risk. This unfortunately does not seem to be the case with Krishca Strapping Solutions Ltd, though we may turn out to be wrong in our assessment.

Disclaimer – This note is part of a business research & analysis series on small companies, there is no BUY/SELL recommendation or target price issued as part of this to a general audience. There is no assurance that this stock makes for a good investment, there is no guarantee that this stock will continue/be included in the coverage universe of Congruence Advisers. The note contains some forward-looking statements and insights drawn from the historical results, annual reports and investor presentations; they are to be viewed only within this context and not as a prediction of future performance of the business or the stock covered.

While due care has been taken to ensure that the information here is as accurate as possible, Congruence Advisers disclaims any liability in case of any unintentional inaccuracies.

The content does not constitute investment advice.