Yatra Online Ltd. is a leading Indian Online Travel Aggregator (OTA) company. Yatra Online Limited provides B2C as well as B2B travel booking related services.

Yatra Online Ltd offers the prospect of a differentiated business in the listed travel OTA segment, one that prioritizes the SME business travel segment as opposed to the consumer travel, data analytics & discovery segments that the other, better known listed players focus on. As we set out to build an industry view on the travel OTA space, improved numbers led us to do a deep dive into Yatra Online Ltd’s differentiated approach to this sector.

While the business numbers have been coming in well and are likely to come in well going forward, we found ourselves asking if Yatra Online Ltd has been successful in creating switching costs for its SME customers?

Won’t the bigger players eventually enter their turf?

If so, how can investors take a long term view of this business?

Will M&A be the primary growth mode for this business from here? Given the plethora of legacy B2B travel businesses that exist in India?

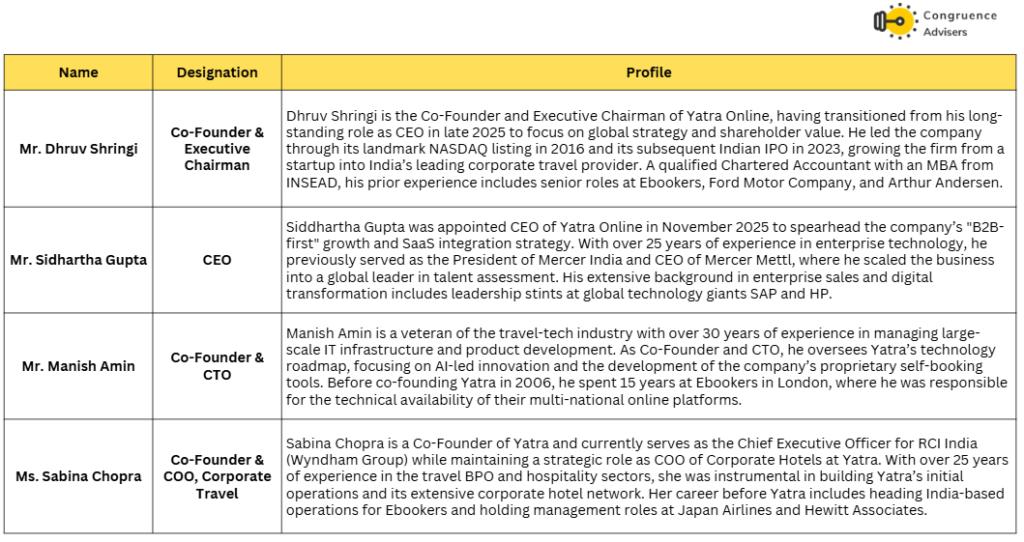

Yatra Online Ltd Company Summary

Yatra Online Ltd was founded in 2006 by three senior executives of eBookers, a Europe focused travel company. The founding trio were Mr. Dhruv Shringi (Director of Group Operations at eBookers), Mr. Manish Amin (Head of Infra at eBookers) and Ms. Sabina Chopra (Head of India Ops at eBookers). Mr. Dhruv Shringi has operated as the CEO of Yatra Online Ltd. since inception till 2025, when he was elevated to the position of Executive Chairman. Mr. Manish Amin has operated as the CIO since inception and Ms. Sabina Chopra serves as the COO, Corporate Travel.

Yatra Online Ltd started life in 2006 in the early stages of the Indian startup boom. It wanted to benefit from the impending travel boom in India led by the introduction of low cost carriers in the country. The early cohort of competitors in the Indian travel space were MakeMyTrip Ltd (2000), Yatra (2006), Goibibo (2007), Cleartrip (2006), Via.com (2006) etc. Goibibo and MakeMyTrip Ltd went on to capture the lion’s share of the Indian B2C OTA market backed by significant PE/VC capital in the early stages and public capital in the case of MakeMyTrip Ltd in 2010 (Nasdaq listing). Goibibo and MakeMyTrip Ltd eventually merged in 2016 to prevent cut-throat competition. Yatra Online Ltd remained relatively capital starved and although it also made a string of acquisitions during the time, it could never reach the scale of MakeMyTrip Ltd and Goibibo. Yatra Online Ltd then successfully pivoted its attention towards the B2B corporate travel space while also maintaining a B2C presence. The B2B pivot turned out to be successful and the current avatar of Yatra Online Ltd is distinctly B2B first. The reason we are interested in Yatra Online Ltd is also because of their market standing and capabilities in the B2B corporate travel segment.

Timeline of key events in Yatra Online Ltd’s history since inception

Phase I: Inception and Consolidation (2006-2015)

- 2006: Launched in August with a focus on the nascent Indian online consumer market

- 2010-2012 (The Acquisition Spree): To build a moat, Yatra Online Ltd acquired TSI (B2B focus) in 2010, Magicdom, and Travelguru (2012) from Travelocity. These acquisitions established Yatra Online Ltd as the leader in India’s hotel aggregation and B2B flight distribution.

- 2013: Faced a significant crisis with a data breach affecting 5 million users, leading to a massive overhaul of their security and tech infrastructure.

Phase II: The Global Public Debut (2016–2020)

- 2016 (NASDAQ Listing): Yatra Online Ltd became the second Indian OTA to list in the US via a reverse merger with Terrapin 3 Acquisition Corp (a SPAC). This finally provided them with the capital to compete with MakeMyTrip Ltd which got listed much earlier in 2010.

- 2017 (ATB Acquisition): Yatra Online Ltd acquired ATB for ~INR 130-150 Cr over a period of 2017-2020, in tranches. This was a significant moment in Yatra Online Ltd’s B2B pivot as ATB was one of India’s oldest, offline corporate travel management companies with 400 clients and a GBV of ~INR 1500Cr

- 2019-2020 (The Ebix Merger Saga): A pivotal what-if moment. Ebix Inc. signed a deal to acquire Yatra Online Ltd for ~$338M. However, following the COVID-19 travel collapse and legal disputes, Yatra Online Ltd terminated the merger in June 2020 and filed for damages, leading to a period of lean operations and strategic re-evaluation.

Phase III: The B2B Pivot and Indian market Listing (2021-2024)

- The Corporate Shift: Recognizing the low margins in B2C, Yatra Online Ltd doubled down on its Self-Booking Tool (SBT) for corporates. By 2023, it became India’s largest corporate travel player by client count (>800 large firms)

- 2023 (Indian IPO): In September 2023, Yatra Online Ltd successfully listed on the NSE and BSE in India. This was a strategic move to tap into local retail and institutional capital, as its NASDAQ valuation was suffering from a holding company and illiquidity discount

- 2024: Acquired Globe All India Services (Globe Travels) for ~$15M, adding over 400 corporate clients and solidifying its lead in the B2B sector.

Phase IV: Innovation & Restructuring (2025 – Jan 2026)

- AI Integration (Mid-2025): Launched “DIYA,” an AI-powered assistant designed to handle complex corporate travel workflows and reduce manual support costs.

- Leadership Transition (Nov 2025): Dhruv Shringi moved to Executive Chairman; Siddhartha Gupta took the helm as CEO of Yatra Online Ltd

. - Corporate Restructuring (Dec 2025) – On the verge of amalgamating 6 subsidiaries into the standalone entity

MakeMyTrip Ltd vs Yatra Online Ltd – A tale of two divergent paths

MakeMyTrip Ltd was founded in 2000 by Deep Kalra who wanted to tap into the lucrative US-India travel corridor which was driven by the growing IT industry in India. MakeMyTrip Ltd’s key founder, Deep Kalra, chanced upon travel as a viable online business after stints at PE/VC companies and after failing in his first entrepreneurial venture. MakeMyTrip Ltd, thus, had a 5-6 year headstart vs Yatra Online Ltd which was founded in 2006. MakeMyTrip Ltd managed to attract significant PE/VC investments as the incumbent, listed in Nasdaq in 2010, gained access to public market capital and was able to acquire its fierce competitor – the Naspers backed Goibibo – in 2016 which gave it 60% Indian market share and cemented its position as the behemoth of the Indian online travel industry.

Yatra Online Ltd, in comparison, also attracted PE/VC capital, but not at the scale of MakeMyTrip Ltd. Hence Yatra Online Ltd couldn’t capture market share as fast asMakeMyTrip Ltd. Yatra Online Ltd initially had intended to list on Nasdaq in 2012 (2Ys after MakeMyTrip Ltd). However that got delayed due to Kingfisher airlines’ collapse in 2012. Yatra Online Ltd had significant receivables and advances with Kingfisher airlines. Sorting this out, delayed their listing till 2016. When they listed, it was through a reverse merger (SPAC listing), which depressed their valuations. With a much smaller capital kitty than MakeMyTrip Ltd, Yatra Online Ltd decided to conserve cash and not fight the bleeding B2C wars and instead decided to pivot towards B2B corporate travel.

Thus, luck had a large role to play in the divergence of paths and relative success of MakeMyTrip Ltd and Yatra Online Ltd.

Yatra Online Ltd Management Details

Yatra Online Ltd – Industry Landscape

Global Travel and Hospitality Industry

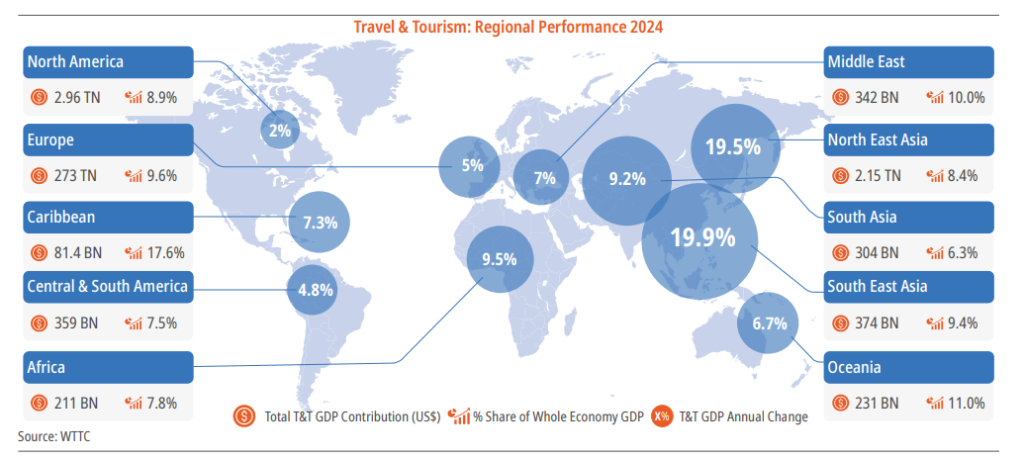

The global travel and tourism industry contributed ~USD 11Tn to the global economy, accounting for almost 10% of global GDP and growing by 8.5% over 2023. International visitor spending reached $1.87 trillion, nearly a 12% increase from the previous year, while domestic visitor spending grew by 5.4% to $5.3 trillion.

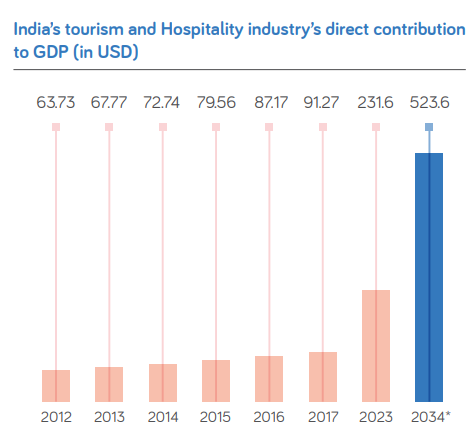

India’s tourism and hospitality industry’s direct contribution to GDP in 2023 was estimated to be ~USD 232bn (~6% of GDP). This is expected to grow at a 7.5% CAGR over the next decade to reach ~USD 524bn by 2034.

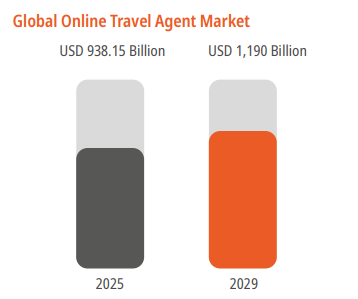

The global OTA industry is experiencing strong growth, due to evolving consumer preferences and a resurgence in global travel demand. The market is valued at approximately USD 938 billion in 2025 and is projected to reach USD 1.19 trillion by 2029 at a compound annual growth rate (CAGR) of 6.2%.15 This expansion is supported by rising disposable incomes, strong economic growth in emerging markets, rapid urbanization and the widespread adoption of smartphones and high-speed internet, which are fundamentally reshaping how travellers plan and book their journeys.

Indian Travel and Hospitality Industry

The Travel & Tourism market in India is projected to generate approximately USD 25 Bn in revenue by 2025, with an expected CAGR of 8%, leading to an estimated market size of USD 34 Bn by 2029. The Package Holidays sector is forecasted to lead the market with an expected volume of USD 11.2 Bn in 2025.

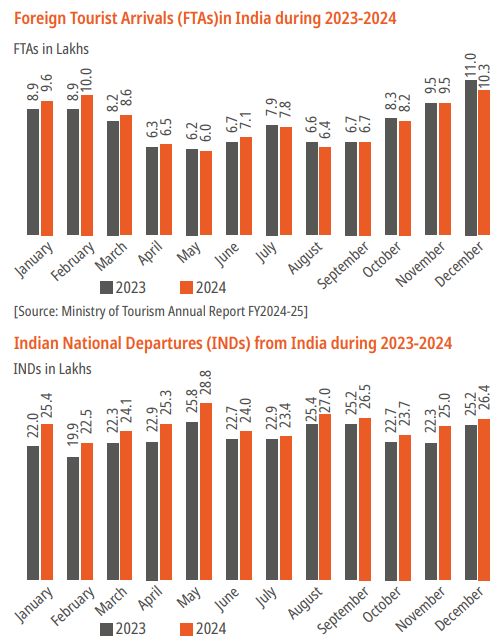

According to provisional estimates from the Ministry of Tourism, India recorded 9.66 million foreign tourist arrivals in 2024, contributing over ₹2.77 lakh crore in foreign exchange earnings with a strong 19.8% growth over the previous year.

Outbound travel is also gaining ground. As of 2024, India is among the top five fastest-growing outbound markets globally, with international departures crossing 27 million. Travel budgets are expanding and preferences are shifting toward curated, experience-rich itineraries.12 Digital tools, visa relaxations and the launch of the Incredible India Digital Portal are further enhancing the travel experience and facilitating seamless planning for both Indian and foreign tourists

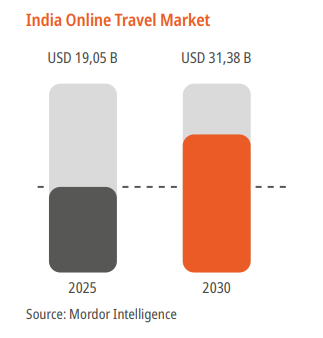

In 2025, the Indian online travel market is estimated to reach USD 19.05 billion, with projections indicating robust growth to USD 31.38 billion by 2030, with a CAGR of 10.5% over the forecast period

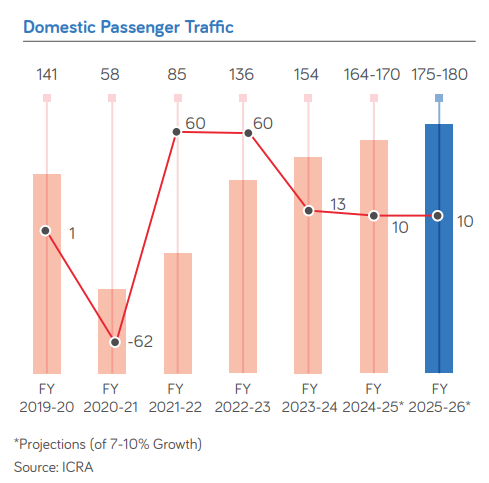

Domestic airline traffic has rebounded impressively post Covid and in FY25 was expected to reach ~164-170mn passengers, comfortably surpassing the pre Covid peak.

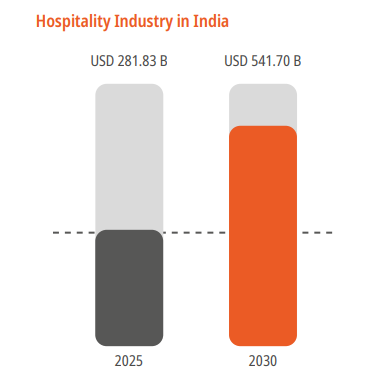

India’s hospitality industry has entered a robust growth phase in FY2025, driven by the resurgence of both domestic and international travel, rising disposable incomes and the growing preference for leisure and spiritual tourism. The market size reached to USD 281.8 billion in 2025 and is expected to grow at a strong 13.96% CAGR to USD 541.7 billion by 2030. This impressive growth is supported by a surge in domestic tourism, a rebound in business travel, rising disposable incomes and significant government-led infrastructure development

Indian Corporate Travel Industry

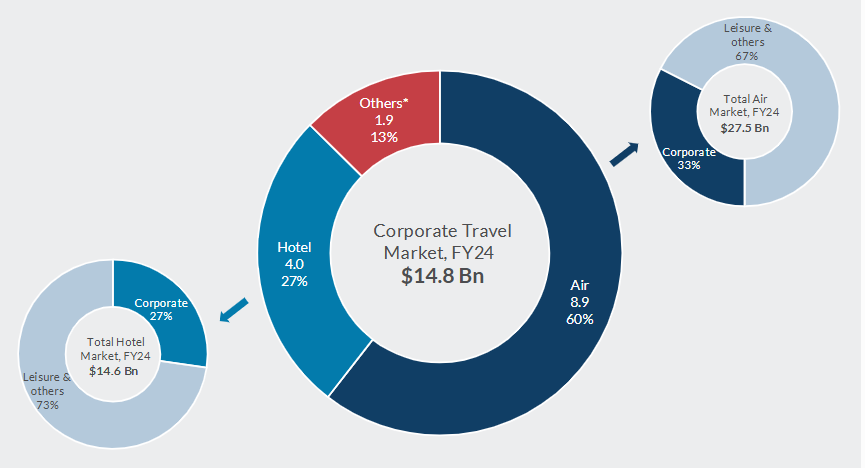

India’s Corporate Travel market in FY24 was estimated to be ~USD 14.8bn in size with ~60% coming from air travel and ~27% coming from Hotels. Corporate travel accounts for ~33% of India’s air travel market and 27% of India’s hotels market.

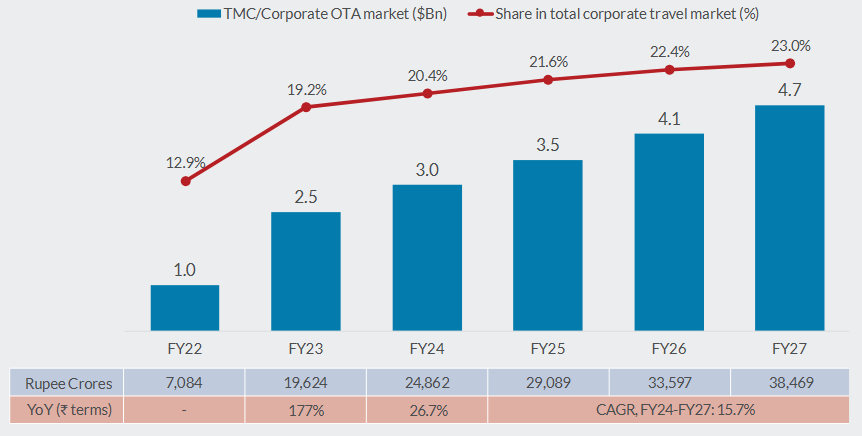

Managed corporate travel is increasing in penetration as more and more corporates outsource their travel ops to Travel Management Companies and Corporate OTAs. As of FY24, it is estimated that the Corporate OTA penetration is at ~20%, accounting for ~USD 3bn of corporate travel spend. This penetration is expected to only increase in coming years as more and more corporates turn to online and SaaS based travel management services. The corporate managed travel industry is expected to grow at 15-16% over the next few years.

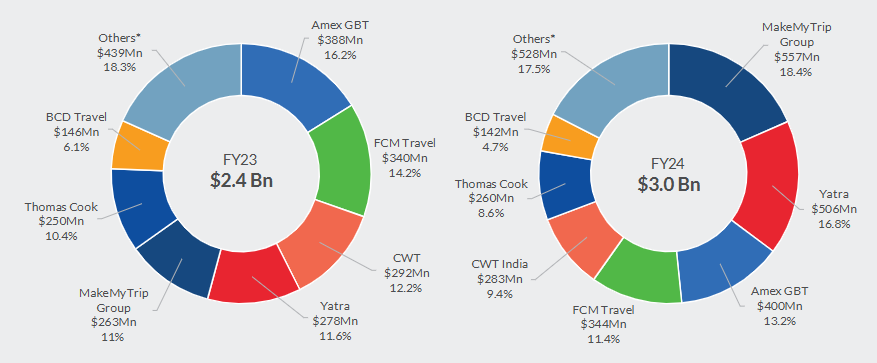

The key players in the corporate TMC and OTA market are MakeMyTrip Ltd (via MyBiz and Quest2travel captures both SME and mid/large corporates), Yatra Online Ltd(mid/large corporate leader), Amex GBT (Global leader with high MNC share), FCM Travel (Strong contender in SME Corporate space) and Thomas Cook (legacy TMC with physical touch).

In FY24, MakeMyTrip Ltd enjoyed ~18.4% market share in this space, with a big lead in the SME category. Yatra Online Ltd had a ~16.8% market share with a big lead in the mid-to-large corporate segment where it had 1300 customers vs ~600 customers for MakeMyTrip Ltd. Amex GBT accounted for ~13.2% of the market and FCM Travel accounted for ~11.4% of the market in FY24.

There has been significant M&A activity in the Corporate TMC and OTA space. Some noteworthy deals are mentioned below

- MakeMyTrip Group, India’s OTA market leader, made a slew of acquisitions to reinforce its position in the managed travel space. It acquired Happay in 2024 to strengthen its expense management capabilities. Additionally, as part of a phased acquisition strategy, the group secured Quest2Travel in 2019 to boost its standing as an all-in-one corporate travel platform. It enhanced its fintech capabilities and hotel tech SaaS solutions capabilities through the acquisitions of BookMyForex and Simplotel in 2022

- Yatra Online Ltd strengthened its market presence by acquiring Globe All India Services Limited (Globe Travels) in 2024, expanding its client base and establishing a foothold in the meetings, incentives, corporate, and events (MICE) segment. Additionally, it completed the acquisition of Air Travel Bureau (ATB) in 2020, further consolidating its position in the corporate travel space

- In 2024, Amex GBT acquired CWT, bolstering its brand portfolio, eyeing greater choices and value for customers and suppliers. Earlier, in 2021, it strengthened its corporate travel management portfolio by acquiring Egencia (from Expedia) and Ovation Travel Group, enhancing its visibility in the high-touch corporate travel segment. Amex GBT is a global heavyweight and has high market share amongst the Fortune 500, thus dominating the MNC space in India.

Yatra Online Ltd Business Details

Before we get into understanding Yatra Online Ltd’s business model, it will be useful to understand a few industry terminologies

- Gross Transaction Value (GTV/GBV) – This is the value of the transaction done by the consumer on the platform. E.g. If a consumer buys tickets worth INR 10000 on Yatra.com, then GBV of the transactions is INR 10000

- Gross Take Rate/Net Take Rate – Gross take is the OTA’s gross earnings from a booking on the platform. For e.g. for every flight booking on its platform, an OTA earns via commissions earned from the airline and/or convenience fees charged to the consumer. Together these form the gross take. Net take is gross take adjusted for any promotions or discounts that the OTA offers the consumer to induce them to transact on their platform.

Gross and net take rates are calculated by dividing gross and net takes respectively by the GBV. - MICE (Meetings, Incentives, Conferences, Exhibitions) – MICE comprises corporate or industry events that involve bulk travel and stay in a location. For example, a corporate’s annual employee retreat where many employees travel to a city/location in India and stay in luxury hotels while having a conference or meeting is an example of MICE.

- Gross profit – This is the net value added by an OTA after adjusting for pass through costs from the revenue. In certain transactions such as holiday package bookings or MICE bookings, the GBV is recognized as revenue by the OTA. The pass through costs (Flight costs + Hotel costs) are then aggregated as service costs and subtracted from revenue to arrive at gross profit.

Note: Yatra Online Ltd considers Gross Profit to be a more accurate representation of its value added than revenue and hence calculates EBITDA margins on gross profit and not on revenue. - Adjusted EBITDA – A typical SaaS company metric where EBITDA is adjusted for one off costs or incomes such as ESOP costs, restructuring costs, one time gains etc. It is supposed to be a more accurate representation of persistent earnings but one has to be careful in assessing how Adjusted EBITDA is calculated as it can be prone to manipulation to embellish company performance.

Now that we understand basic industry terminology, let’s look at Yatra Online Ltd’s business model in detail. Yatra Online Ltd operates across B2C and B2B segments

B2C Segment

OTA services in the B2C segment are provided via their website Yatra.com where customers can book flights, hotels, holiday packages, trains and cabs. B2C services are standardized and not customised. The B2C segment is characterized by extremely high competition between key players such as MakeMyTrip Ltd, Goibibo (MakeMyTrip Ltd company), Cleartrip, Yatra Online Ltd, Ixigo, EaseMyTrip with the MakeMyTrip Ltd Group having ~60% market share.

The domestic flights segment is the most competitive due to a very concentrated supply landscape with Indigo having 60-65% domestic market share. Net take rates here can be as low as 2-3%. The hotels segment on the other hand can generate net take rates in high-single-digit to low-teens % owing to a much more fragmented supplier base and a much more non-standardised product compared to airline seats.

There is no customer loyalty in the B2C segment and customers regularly shop around across OTAs to get the best deals.

Yatra Online Ltd has low single digit market share in the B2C OTA space. This is a space Yatra Online Ltd has intentionally vacated over the years due to low profitability and because it wasn’t able to keep up with cash burn requirements in the face of well capitalised competitors like MakeMyTrip Ltd.

B2B Segment

In the B2B segment, Yatra Online Ltd provides customised travel booking services for corporates – both SMEs and mid-to-large corporates. Yatra Online Ltd claims to be the largest B2B Corporate Travel services provider in India. Industry reports also peg it at the top along with MMT’s B2B business division.

Under its corporate OTA services, Yatra Online Ltd provides a Self Booking Tool (SBT) to the corporate’s employees using which they can book their travel and stay requirements as per individual employee eligibility limits. Yatra Online Ltd tailors SBT rules to take into account employee eligibility for hotel and travel expenses in accordance with seniority. Any booking requests which are in violation of this logic, get auto rejected. Yatra Online Ltd’s SBT tool is integrated with the corporate’s HRMS (Human Resources Management System) and ERP (Enterprise Resource Planning) software to enable smooth data logging and reconciliations at every step of the way. Yatra Online Ltd is also trying to bundle an expense management tool along with its SBT, more on that later.

Thus, unlike B2C, in the B2B segment Yatra Online Ltd provides highly customised services which are tightly integrated with the customer’s internal data processing systems. This gives rise to customer stickiness and switching costs.

The solution provided for SME customers is much simpler than what is described above as their needs are also much simpler. Barriers to entry and customer stickiness in the SME segment are thus much lower than in the mid-to-large corporate space.

Yatra Online Ltd started pivoting towards B2B from B2C in the late 2010s. Since Covid, the tilt in favour of B2B has further intensified with B2B now comprising 70% of the GBV mix.

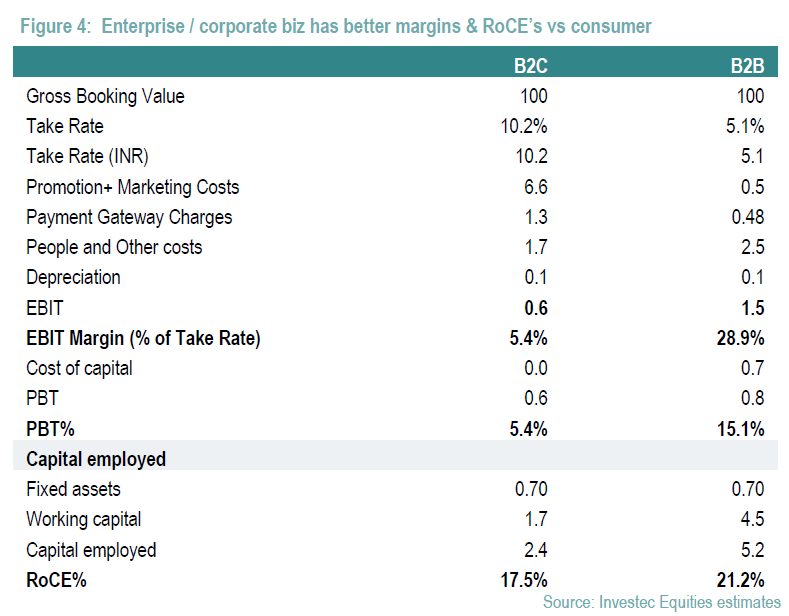

Below is a rough comparison of the economics of a B2C transaction versus a B2B transaction. While gross take rates in B2C are much higher than B2B, by the time customer inducement costs and payment gateway charges are accounted for, B2B transactions tend to have a much higher EBIT margin. B2B transactions require higher capital deployed because corporates have to be given credit terms for payments versus instant payments received in the B2C segment. In spite of the larger capital requirements, on an ROCE basis, B2B transactions tend to make more than B2C transactions.

Recent Acquisition history

ATB (2017-2020)

Yatra Online Ltd’s 2017 acquisition of Air Travel Bureau (ATB) was a key pivot moment in its journey from a B2C OTA to India’s dominant B2B player. By acquiring 100% of ATB for approximately INR 130-150 Crore, Yatra Online Ltd absorbed a legacy powerhouse with over INR 1,500 Crore in annual gross bookings and 400+ large corporate clients. This deal provided the critical scale needed to bypass the expensive B2C discount wars and secure a high-margin MICE portfolio. Strategically, it allowed Yatra to deploy its proprietary Self-Booking Tool (SBT) across a massive, established client base, creating a technology-led lock-in that traditional travel agents could not replicate

Globe Travels (2024)

The September 2024 acquisition of Globe Travels for INR 128 Crore (a 100% cash deal) further cemented Yatra Online Ltd’s B2B positioning by adding 360 corporate accounts, representing a 40% jump in Yatra Online Ltd’s enterprise client base. Yatra Online Ltd used the cash raised from its 2023 IPO to do a cash acquisition of Globe Travels.

Acquired at an attractive 7.5x trailing EBITDA, Globe brought $90 million in annual gross bookings and specialized strength in the mid-market manufacturing and cement sectors. This move was a repeat of the ATB playbook, aimed at defensive consolidation against MakeMyTrip’s myBiz and Quest2Travel led B2B expansion. By integrating Globe’s predominantly offline clients into its platform, Yatra Online Ltd is positioned to drive margin expansion through digital migration and customer stickiness through enhanced technology level integration.

Yatra Online Ltd Corporate Governance Analysis

- Board Composition – As of FY25, Yatra Online Ltd’s Board of Directors comprised 5 members of whom 3 were Independent Directors. The Chairman of the Board is a Non Independent Director and the role of Chairman was separate from the role of CEO.

- Promoter remuneration – The total remuneration paid to promoters by virtue of remuneration was INR 5.6Cr in FY25, amounting to ~15% of Yatra Online Ltd’s PAT

- Related Party Transactions – There are no related party transactions worth flagging

- Contingent Liabilities – There are significant contingent liabilities amounting to INR 102Cr as of FY25 outstanding for Yatra Online Ltd’s. Of this amount, INR 10Cr are claims by 3rd parties which Yatra Online Ltd’s does not recognize and the remaining INR 92Cr is tax demands under income tax, service tax and GST. The total contingent liabilities amount to 12.5% of Yatra Online Ltd’s consolidated net worth as of Sep 2025 and are thus material. Yatra Online Ltd’s has made no provisions against these contingent liabilities as it believes the probability of such claims getting recognized are minimal.

- Dividend Policy – Yatra Online Ltd’s does not pay dividends.

Yatra Online Ltd Financial Performance

Yatra Online Ltd does not report its financials along the B2C vs B2B axis however. It reports its financials across three segments – Air, Hotels and Others. Let’s understand the dynamics in each of these segments

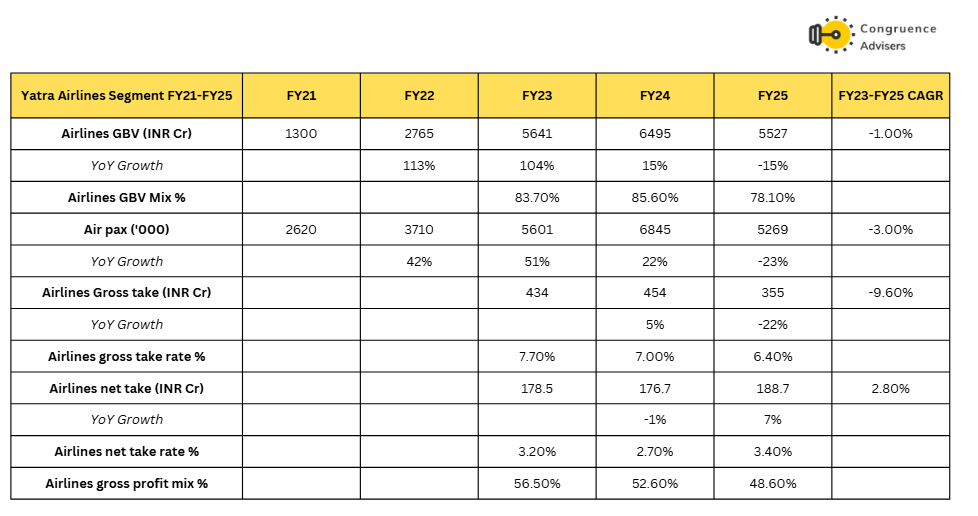

Air – The air segment is by far the largest contributor to GBV, at 78% in FY25. However its contribution to FY25 gross profits is only ~49%, demonstrating the low profitability in this segment versus Hotels and Others. You can see from the table below that between FY23-FY25, Air GBVs are flat, gross take rates are sharply down and net take rates have only improved in FY25.

This data clearly shows the stress in the Air segment in India where Indigo’s absolute market domination and its nudge to move customers to book directly via its website, has put tremendous pressure on OTA margins.

In FY25, Yatra Online Ltd stopped chasing B2C Air GBV by offering customer inducements and instead started focusing on profitability in the segment by optimising spends and margins. Increasing mix of B2B air has also resulted in higher commissions received from airlines as corporate tickets are more lucrative for airlines. The net result has been a 15% YoY decline in Air GBV but a 7% YoY increase in Air net take.

Going forward, Yatra Online Ltd expects the Air GBV to grow 10% with increasing Air net take rates from the 3.4% base in FY25.

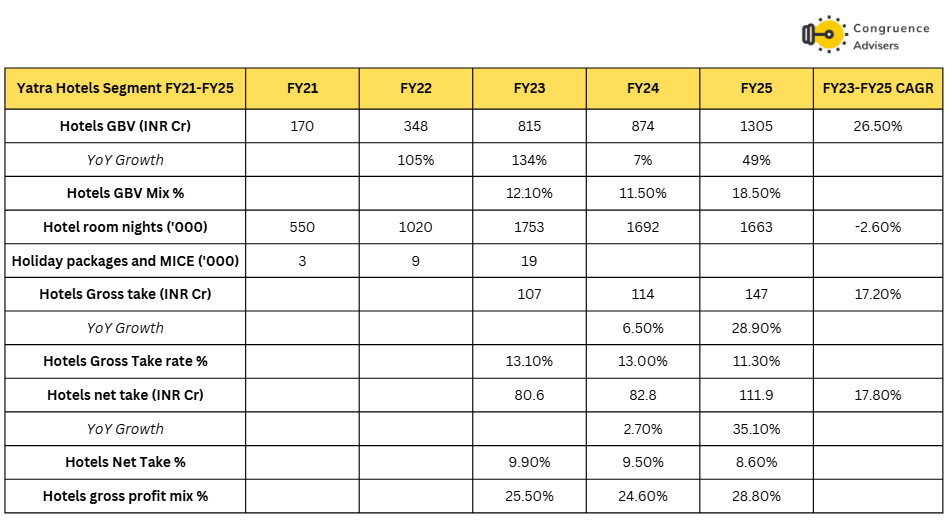

Hotels – This is by far the more profitable business segment for Yatra Online Ltd While Hotels contributed only ~19% of Yatra Online Ltd’s FY25 GBV, it contributed ~29% of Yatra Online Ltd’s gross profit in FY25. The Hotels segment had a net take rate % of 8.6% in FY25 versus Air’s 3.4% highlighting the difference in profitability.

About 30-35% of the Hotels GBV comes from MICE business, which started in earnest only in FY25. That’s why GBV has increased by 49% in FY25 whereas hotel room nights haven’t increased at all. Most of the Hotels GBV growth in FY25 seems to have come from hotel ADR (Average daily rate) hikes and MICE business. While this is great execution on the MICE front by Yatra Online Ltd, hotel room nights staying flat YoY for 2 FYs straight is not good news and needs to be monitored closely.

The gross and net take rates have inched down from 13.1% and 9.9% in FY23 to 11.3% and 8.6% respectively in FY25 due to a pivot in mix towards B2B, where take rates are lower. Going forward management expects Hotels GBV to grow at 20% YoY.

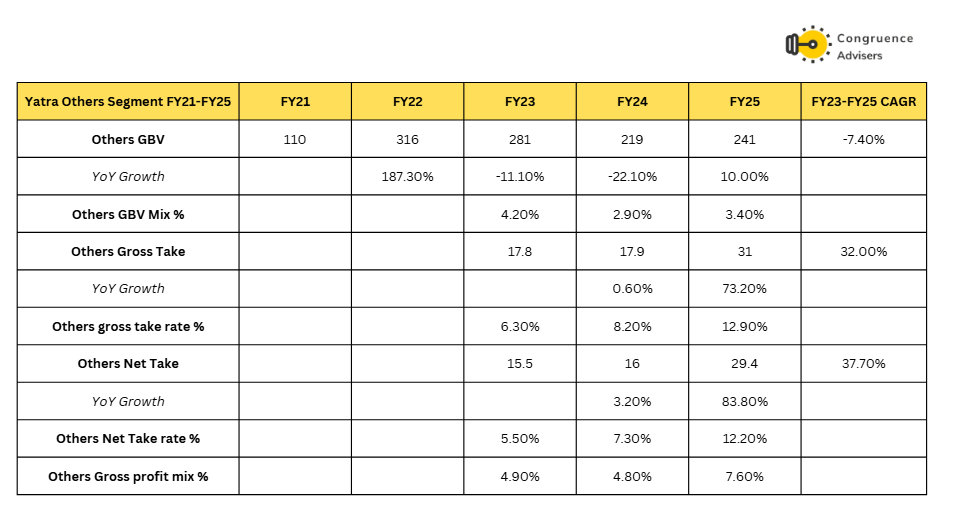

Others – The Others segment comprises everything other than Air, Hotels, MICE and Holiday packages i.e. train, bus, taxis and car rentals, visa processing and digital freight forwarding. This is the smallest segment with only 3% GBV contribution in FY25 but quite profitable as evidenced by 7.6% gross profit contribution in FY25.

In FY25, these 3 segments together contributed 85% of Yatra’s gross profits. The remaining 15% came from advertising revenues. Between FY23-FY25, advertising revenues have grown at a healthy CAGR of 16%.

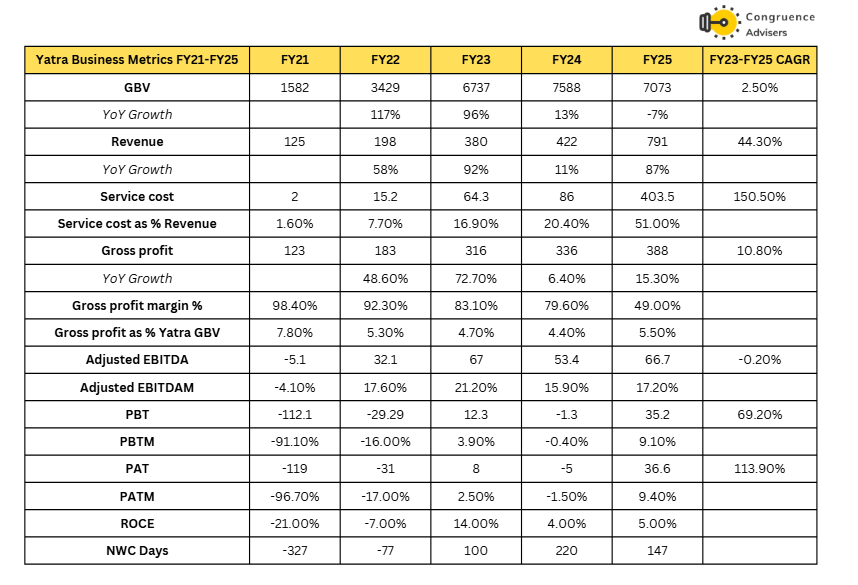

Putting all the segments together, the consolidated picture for Yatra over FY21-FY25 is presented in the table below.

Between FY23-FY25, GBV has grown at a sedate pace of 2.5% but revenues have grown at 44%. This is in large part due to increased MICE business from FY25 where revenues are recognized on a gross basis and service costs are then netted off.

Please note: EBITDA, PBT and PAT margins in the table are calculated with gross profit as the base, not revenues

Therefore revenue is not the right metric to track for Yatra, gross profit is. Gross profit has grown at ~11% between FY23-FY25 versus GBV growth of 2.5% suggesting better take rates, driven by mix change towards Hotels and Others segments versus Air segment. Adjusted EBITDA has remained flat whereas reported EBITDA has increased quite well between FY23 and FY25. ROCEs have been in the 4-5% range in FY24 and FY25.

In H1 FY26, the adjusted EBITDA margin has inched up to 20% and ROCE has inched up to 8-9%.

Yatra Online Ltd Comparative Analysis

To understand Yatra Online Ltd investment potential, we have conducted a comprehensive analysis. This analysis includes comparing Yatra Online Ltd to its competitors (peer comparison) on various fundamental parameters and Yatra Online Ltd share performance relative to relevant benchmark and sector indices.

Yatra Online Ltd Peer Comparison

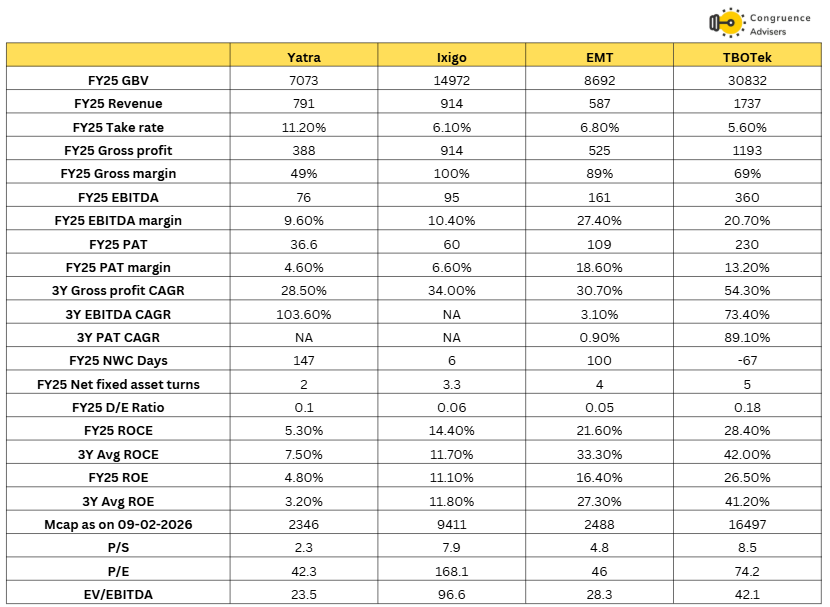

There are several travel companies listed in the Indian stock market. Ixigo and EaseMyTrip are B2C OTAs, TBOTek is a B2B2C company catering to travel agents and Rategain is a supply side SaaS company which helps hotels maximize revenue. The closest peers for Yatra are Ixigo, EaseMyTrip and TBOTek, so let’s do a peer comparison with this set.

All the travel companies have grown topline and gross profits well in a 3Y timeframe because the base year of FY22 was Covid affected. Ixigo and Yatra Online Ltd have turned their PAT around from -ve to +ve in this timeframe while EMT has failed to grow its PAT at all, surprisingly. All the travel companies also have lean balance sheets with very little debt. EMT and TBOTek have the best ROCE and ROE numbers. TBOTek operates on a -ve WC cycle. Ixigo also has very low NWC days whereas Yatra Online Ltd and EMT require significant working capital.

A combination of high NWC days and low net fixed asset turns has kept Yatra Online Ltd’s ROCE metrics depressed and below its peers. With the interventions they are planning to reduce debtor days, one hopes they will be able to massively increase their ROCE over the next 3 years, in line with guidance.

Yatra Online Ltd Index Comparison

Yatra Online Ltd share performance vs S&P BSE Small Cap Index, as the index benchmark comparison is a fundamental tool for understanding the investment potential and making informed decisions in the context of the broader market

Why you should consider investing in Yatra Online Ltd ?

Yatra Online Ltd offers some compelling reasons to track closely and to consider investing in India’s OTA Travel space.

- Leadership in the mid-to-large corporate travel segment – With 1300 mid-to-large corporate customers, Yatra Online Ltd is the largest OTA in this space, comfortably ahead of MMT which has ~600 odd customers.

- Significant operating leverage built into the business model – About 60% of Yatra Online Ltd’s costs are fixed in nature leading to high operating leverage. Yatra Online Ltd already has pan India B2B sales and business development teams, so incremental customer additions have high operating leverage. Most of the technology spends are also behind them with only incremental spends going forward. One can hope that the advent of AI will also reduce resources needed for software development for Yatra Online Ltd. Management has signalled that it is possible for Yatra Online Ltd to start reporting 25% EBITDA margins on gross profit by FY27 end and 30% by FY29.

- ROCE at inflection point – As operating leverage plays out, Yatra Online Ltd’s ROCEs should improve disproportionately. Yatra Online Ltd delivered a ROCE of 5% in FY25 and is on track to deliver a ROCE of 8-9% in FY26 and as per management guidance, should be able to get to a ROCE of 13-14% in FY27.

- Possibility of debtor days reduction via corporate card tie-ups – Yatra Online Ltd is exploring the migration of its customers to Yatra co-branded credit cards. This will help move Yatra Online Ltd’s receivables to the books of the credit card company and also help Yatra Online Ltd earn a share of the MDR (Merchant Discount Rate)

What are the Risks of investing in Yatra Online Ltd ?

Investors need to keep the following risks in mind if they choose to invest into this business. Risks needs to be weighed in combination with the advantages listed above to arrive at a decision that is optimal for your portfolio construct

- Valuations are not cheap – At 40x TTM EPS and 4.7x FY26E Price to Sales (gross profit), Yatra Online Ltd is not trading cheap. While it is not expensive per se, any disappointment in execution can create meaningful downside from these valuations.

- High receivables on the balance sheet – Due to the heavy B2B mix for Yatra Online Ltd and the fact that Yatra Online Ltd extends ~30 days of credit to its corporate customers, Yatra Online Ltd has ~200 days of receivables. This is because Yatra Online Ltd records revenues on a take rate basis but the receivables are on full gross booking value basis for 30 days. This results in high working capital intensity and drains Yatra Online Ltd’s operating cash flows. More importantly it introduces a significant bad debt risk for Yatra Online Ltd, something they’ve suffered from on the supply side during the Kingfisher Airlines bust.

- Competitors in the B2B space are heavyweights – Yatra Online Ltd competes with the likes of MMT, Amex GBT, CFM etc. in the corporate B2B travel solutions space and with the likes of SAP Concur on the expense management software side.

- Chain hotels trying to increase D2C business – While premium hotel chains like Marriott already had significant direct booking share, mid-tier hotel chains like Lemon Tree are also trying to come up with loyalty programs to entice customers to book directly via their websites.

- Leadership transition – Mr. Dhruv Shringi has recently relinquished his CEO role of 2 decades to take the Executive Chairman position and Mr. Siddharth Gupta has been brought in as CEO to drive the B2B business. While Dhruv remains very much involved in overseeing Yatra Online Ltd’s strategic moves, there will be a settling in period for the new CEO. If for some reason, this move does not work out and Dhruv has to step back in the CEO role, this might create a negative perception about Yatra Online Ltd.

Yatra Online Ltd Future Outlook

New initiatives and developments

- Yatra Online Ltd has recently appointed Mr. Siddhartha Gupta as CEO of the company with Mr. Dhruv Shringi moving to the post of Executive Chairman. Siddhartha is the ex-CEO of Mercr Mettl and ex-President of the Mercr Group in India and thus has extensive experience in selling B2B SaaS solutions to corporates. He has been brought in to further penetrate into Corporates and integrate Yatra Online Ltd’s SBT and expense management solutions tightly with Corporate HRMS and ERP systems to enhance customer stickiness.

- Yatra Online Ltd has developed a corporate expense management tool called RECAP. Yatra Online Ltd intends to bundle it along with its Self Booking Tool as part of a wider solution to corporates.

- Yatra Online Ltd is looking at ways to reduce its high debtor days. It is exploring moving corporates to Yatra co-branded corporate credit cards. This can help Yatra Online Ltd in two ways – it will move corporate receivables from Yatra’s books to the books of the issuing bank and Yatra Online Ltd may be able to earn a part of the MDR (Merchant Discount Rate) from the issuing bank as commission. At present, approximately 30% of Yatra Online Ltd’s corporate customers use credit cards, but these are 3rd party credit cards, not Yatra Online Ltd co-branded ones.

Growth outlook

Going forward Yatra Online Ltd expects to grow GBV at 15-20% CAGR. As of H1 FY26, Yatra Online Ltd’s adjusted margins are ~20% of gross profits. Yatra Online Ltd aims to be at 25% margins by the end of FY27 and at 30% margins mid way through FY29. Yatra Online Ltd expects to be clocking 8-9% ROCE in FY26 and 13-14% ROCE in FY27.

Yatra Online Ltd Technical Analysis

We consider technical analysis to be a useful input in taking medium-term investment decisions. Many a time price action tends to lead to fundamental developments; this is too important an aspect to be ignored by retail investors who do not have access to management outside of common forums like investor calls & AGM.

At Congruence Advisers we like to consider both the long-term weekly chart and the daily chart to arrive at a view on price action. Combined with our understanding of fundamentals, we usually end up being better placed to be able to judge both the business cycle and the stock cycle. Playing the stock cycle right is extremely important for investors looking to extract significant alpha over the medium term.

Yatra Online Ltd Price Charts

On the 1 year daily chart, we can see that the Yatra Online Ltd stock weathered the turbulence in markets in the March-May period and then gapped up on high volumes with Q1 results which were a significant beat. Yatra Online Ltd stock went up almost 50% in 3 sessions from 100 to 150 levels. From Q1 results to Q2 results, Yatra Online Ltd stock oscillated between 138 to 170 levels. With Q2 results continuing the Q1 trend, Yatra Online Ltd stock again moved up sharply by 30-35% in the matter of a few sessions. Yatra Online Ltd stock peaked in November and since then has corrected 20%+ along with the broader markets. The critical support level of 138 has held. Yatra Online Ltd stock needs to clear two resistance levels of 155 and 170, before it can create new highs. With most of the acquisition led YoY earnings jump behind us, the earnings growth may revert to a 20-25% kind of a trend. So it should not be surprising if Yatra Online Ltd stock consolidates for a couple of quarters as valuations catch up, before decisively moving up.

The weekly chart captures Yatra Online Ltd stock’s journey since listing in Sep, 2023. Since listing, Yatra Online Ltd stock has consistently delivered solid results. The first 3Qs since listing saw flat operating profits, but from Q2 FY25 it has consistently delivered QoQ operating profit growth. However, Yatra Online Ltd stock price has not mirrored this consistency in execution, with periods of excessive bearishness and excessive bullishness.

After making an intermediate top in Sep 2024, Yatra Online Ltd stock had a terrible next 6-8 months along with the broader Indian market. Yatra Online Ltd stock started coming off lows in March 2025 and then caught on fire after blockbuster Q1 FY26 results, followed by a solid Q2 FY26. From bottom to top, Yatra Online Ltd stock went up 170% between March 2025 and Nov 2025. Since then, Yatra Online Ltd stock has corrected 30-35%, again in line with the broader markets.

Unless results surprise on the downside or there is further market level volatility from current levels, we expect the 138 support level to hold. Q3 FY26 will be the first full quarter with the Globe Travels acquisition in the base (Q2 had 20 days only), so the YoY growth in operating profit in Q3FY26 will be a strong indicator of organic growth at Yatra Online Ltd. If that’s a healthy print (20-25% growth), then Yatra Online Ltd stock should move up gradually as valuations catch up. Better than expected growth, announcement of new acquisition deals or significant reduction in debtors via corporate credit card deals, can make Yatra Online Ltd stock move fast on the upside.

Yatra Online Ltd Latest Latest Result, News and Updates

Yatra Online Ltd Quarterly Results

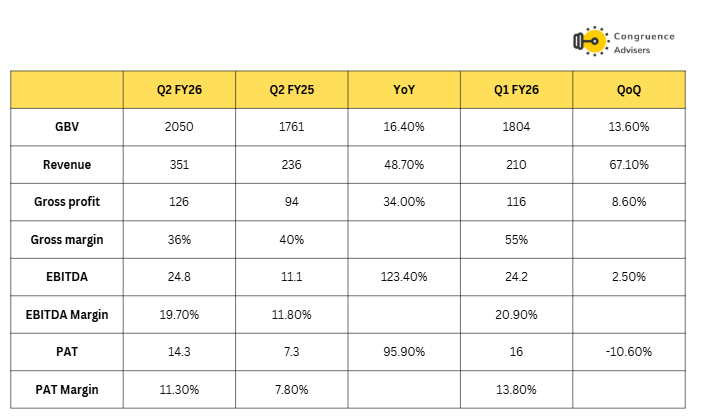

Yatra Online Ltd reported very strong Q2 FY26 numbers with GBV growing 16% YoY, revenue growing 49% YoY and gross profit growing 34% YoY. EBITDA grew 123% and PAT grew 96% demonstrating huge operating leverage.

Gross margins were down QoQ because Q2 was a MICE heavy quarter (MICE involves significant pass through costs).

Final thoughts Yatra Online Ltd

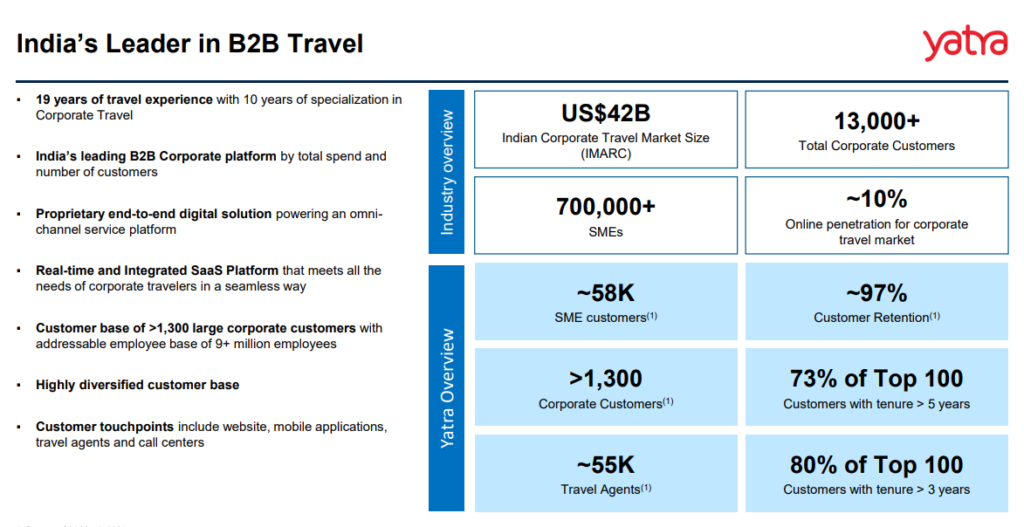

Yatra Online Ltd has created a strong market position for itself in the B2B corporate travel segment in India. It caters to 1300 mid and large scale corporate customers and 58000 SME customers with a claimed retention rate of 97%. The managed corporate travel market in India seems to be ~USD 3.5bn in size, growing at 10%+ per annum. Yatra Online Ltd is one of the largest corporate TMCs in the country along with MakeMyTrip and Amex GBT. In the large and mid corporate segment, Yatra appears to be the comfortable market leader whereas MakeMyTrip Ltd seems to be the market leader in the SME segment.

The mid-to-large corporate travel management system seems to be reasonably sticky with switching costs involved as the service provider’s software is integrated with the customer’s HRMS, ERP and accounts payable software stacks. These integrations are non trivial and time taking and CFO offices aren’t overly keen to switch and repeat the integration process unless significant benefits are available. Thus, having built a lead in this space vs MakeMyTrip Ltd, we believe Yatra Online Ltd is in a position to defend its leadership.

The mid-to-large corporate travel space so far attracts less competition than the cut-throat B2C space and it is likely to remain that way given the entry barriers. The SME travel space is much closer to the B2C space and the service provider with the largest distribution and the smoothest tech-stack and UI/UX is expected to win here. So we expect MakeMyTrip Ltd to always have a lead vs Yatra Online Ltd in the SME travel management space.

Yatra Online Ltd is trying to increase switching costs for its customers by integrating an expense management software called Recap into its travel software stack. This won’t be very easy as there are competent expense management solutions available from global companies, but a bundling with its travel software stack may compel some corporates to switch over. Yatra Online Ltd is also trying to reduce its debtor days significantly by making its customers opt for corporate credit cards which would transfer Yatra Online Ltd’s receivables to the books of the credit card issuing lending company. If successful, this will significantly bump up Yatra Online Ltd’s return on capital ratios. The transition will not be easy as opting for corporate credit cards involves operational efforts on part of Yatra Online Ltd’s customers, something they may not be willing to undertake.

Overall, at ~40x TTM EPS and 4.7x FY26 Price to Sales (We have considered Sales = Gross profits), Yatra Online Ltd. seems to be priced more or less in the fair zone. A B2B focused OTA may not get the same multiples as a B2C OTA, but if Yatra Online Ltd is able to prove over the next few quarters that it has a defensible moat in the B2B segment and if its able to reduce its debtor days via corporate credit cards, then the business may command valuations on par with B2C OTAs because competition is less in the B2B space compared to the B2C space. Peers like Ixigo (B2C) and TBOTek (B2B) trade at 8-9x P/S, Rategain (B2B on the supply side) at 6.5x P/S and EaseMyTrip (B2C) at 4.7x P/S.

Disclaimer – This note is part of a business research & analysis series on small companies, there is no BUY/SELL recommendation or target price issued as part of this to a general audience. There is no assurance that this stock makes for a good investment, there is no guarantee that this stock will continue/be included in the coverage universe of Congruence Advisers. The note contains some forward-looking statements and insights drawn from the historical results, annual reports and investor presentations; they are to be viewed only within this context and not as a prediction of future performance of the business or the stock covered.

While due care has been taken to ensure that the information here is as accurate as possible, Congruence Advisers disclaims any liability in case of any unintentional inaccuracies.

The content does not constitute investment advice.