Sky Gold Ltd designs, manufactures, and markets gold jewelry. It follows a B2B model. Its in-house and freelance designers, who are skilled in Computer-Aided Design (CAD), develop designs for the purpose of manufacturing. Sky Gold Ltd caters to the unique preferences of its customers given its strong understanding of the local and regional market.

Sky Gold Ltd presents the interesting possibility of a proxy play on the long term theme of the Indian Jewellery sector getting organized with the leading players. While traditional heavy gold jewellery will always need a specialized set of skilled workers, the more contemporary segments of jewellery are ripe for an outsourced manufacturing model. While the growth prospects are obvious, it remains to be seen if Sky Gold can pivot to a model where operating cash flows improve to a level that can make future growth self funded rather than relying on high external debt.

Sky Gold Ltd Company Summary

Sky Gold Ltd designs, manufactures, and markets gold jewelry. It follows a B2B model. Its in-house and freelance designers, who are skilled in Computer-Aided Design (CAD), develop designs for the purpose of manufacturing. Sky Gold Ltd caters to the unique preferences of its customers, given its strong understanding of the local and regional markets.

Sky Gold Ltd offers an extensive range of designs and uses studded American diamonds and colored stones in many jewelry pieces. Its product range includes necklaces, rings, pendants, bracelets, earrings, bangles, and customized jewelry based on customer demand. Besides clients in Mumbai and nearby areas, it caters to various jewelry brands. It has set up sales offices in Kerala and Telangana to offer better service in South India.

Sky Gold Ltd Management Details

Sky Gold Ltd promoters have over two decades of experience in the gold manufacturing/processing business. Sky Gold Ltd is a family-owned listed entity, and Mangesh Chauhan, Mahendra Chauhan, and Darshan Chauhan are its directors and promoters.

Sky Gold Ltd – Industry Overview

Gold and Jewellery Industry Overview

Measures that could lead to a shift to organized trade

- Better Enforcement – Widespread presence across cities and locations, & Price transparency and product quality.

- Better Compliance – Compulsory hallmarking of Gold Jewellery, Mandatory PAN Card for jewellery purchases over INR 200,000.

- Rising ticket prices, improved buying experiences, wider availability of choices through a variety of SKUs, etc, are driving this significant trend.

- In July 2024, the Indian government reduced the import duty on gold from 15% to 6% to curb smuggling and boost the domestic jewelry industry.

- Mandatory Hallmarking: The implementation of the Bureau of Indian Standards (BIS) hallmarking rule ensures quality assurance, which benefits organised players.

- The availability of gold loans, buyback options, and easy installment plans attracts buyers to organised channels.

- Digital wallets, UPI, and credit card transactions make purchases easier in the organized sector.

Gold Value Chain In India

Reduction in import duties lowers the overall cost of raw materials, making it more affordable for manufacturers to procure gold and have a positive impact on the market by making gold jewellery more accessible to a broader range of customers. Lower prices lead to a surge in demand, causing manufacturers to increase production.

Duty cuts also let companies to invest more in innovation, design, and advanced manufacturing techniques. This enhances the quality of jewellery and improves production efficiency.

Managing Impact on Margins – Sky Gold Ltd uses hedging and pricing teams to manage the impact of duty cuts. When orders come in, rates are not fixed with consumers. Bullion is purchased from banks or licensed importers and sold in the market to hedge against price variations. The company claims to hedge via MCX contracts as well, but we haven’t see any declared impacts on P&L from hedging, which seems a little unusual to us.

Potential Margin Pressure for Retailers – Some jewelry retailers indicate that margins will be under pressure because of changes in import duties.

Sky Gold Ltd purchases bullion from banks or licensed importers when they receive orders from clients. Additionally, Sky Gold Ltd purchases gold from nominated agencies prescribed by banks and other customers.

In India, the Reserve Bank of India (RBI) nominates specific banks and agencies to import gold bullion under strict guidelines, primarily to meet domestic demand from jewelers, traders, and investors. These “nominated agencies” include public sector banks like the State Bank of India (SBI), private banks like ICICI Bank, and government entities like the Minerals and Metals Trading Corporation (MMTC) and PEC Limited. The RBI authorizes these entities to import gold, often in forms like 1 kg bars or 100-gram bars, from international suppliers accredited by bodies like the London Bullion Market Association (LBMA).

Gold metal loan (GML) is a mechanism under which a jewelry manufacturer borrows gold instead of cash and settles the loan in terms of equivalent gold quantity (or INR equivalent of the gold quantity calculated based on gold prices on day of loan maturity) and an interest cost ranging from 3-5% per annum. GML can be availed for 180/270 days in the case of domestic sales/exports.

As Sky Gold Ltd holds 30 days of inventory to fulfill its orders, it has one of the lowest lead times in the industry. It avails working capital loans to service its clients faster. Its cost of debt stands at 9.5%. However, it is planning to tap the government’s gold metal loan scheme. For SkyGold under this scheme, the interest cost will be 4.5%. The management aims to gradually raise the contribution of GML to 60%/80% by FY25/FY26. This will result in lower interest costs for the company.

Outsourcing trends

Why does Indian Retail Jewelry Outsource its products instead of in-house manufacturing?

Focus on Sales and Retail Stores: Retailers prioritize sales and store operations, so they outsource manufacturing to concentrate on their core business. Over 80-90% of retail players outsource, and 10-20% manufacture in-house

Access to Diverse Designs: Outsourcing allows retailers and jewelry players to offer a wider variety of designs developed by specialized manufacturers from different regions and concepts. Manufacturers develop special designs from Kolkata designers and from worldwide.

Avoid Manufacturing Investments: Retailers avoid investing in manufacturing facilities for the same products they display.

Design Specialization: Manufacturers develop special designs and maintain good inventory and pricing.

Economies of Scale: Sky Gold Ltd benefits from the increasing scale, which reduces costs by spreading overhead.

Expertise and Craftsmanship: Manufacturers provide expertise, craftsmanship, and specialized machinery. Sky Gold Ltd employs designers trained in Kolkata and uses computer-aided design technologies to manufacture lightweight jewelry.

Design Innovation: Manufacturers focus on design innovation and creation, which is essential for attracting customers. Sky Gold Ltd has a design team that focuses on developing new products and designs to meet customer requirements.

Inventory Management: Sky Gold Ltd solves the important pain point of inventory management. Retailers are able to liquidate sales of designs quickly, Sky Gold is in a position to generate more sales or orders.

Lower Overhead Costs: Online retailers often have lower overhead costs compared to physical stores, which translates to more competitive pricing for consumers.

A wide array of options: Large corporate retailers prefer to outsource diamond jewelry because they get creations from different factories. They get numerous creations of future plans.

New Trends: Large corporate retailers are positive and looking to outsource diamond jewelry because of new designs and creations

State-wise Organized Store Network vs. Population Mix and GDP Mix

Source: MOFSL, Company

The Indian gems and jewellery sector contributes 7% to India’s GDP. The domestic gems and jewellery market was valued at ~USD58bn, with gold jewellery being the leading segment in FY23. From USD38bn in FY23, India’s gems and jewellery exports are expected to touch USD145bn by 2028.

Top-10 organised players command more than 30% of the total jewellery demand:

A substantial portion of the industry is unorganised, particularly in rural and semi-urban areas. Around 36% of companies are branded national chains, while others are small regional players or independent retailers.

We expect the share of organised players to rise further to 44% by FY26 which should support the volume growth for Sky Gold Ltd. The total jewellery market reported ~8% revenue CAGR during FY19-24, reaching a market value of INR 6,40,000. The organised market clocked ~18-19% revenue CAGR while Titan, Kalyan, and Senco combined recorded ~20% revenue CAGR during FY19-24.

The total gold consumption in India was attributed to 66% of jewellery and the remaining 34% of bars & coins.

Source: MOFSL, Company

The jewelry market was close to USD 48-50 billion within the organized market in FY18, accounting for a share of 20-22%. The total market reported a CAGR of 9-10% during FY18- 24, while the organized market registered a CAGR of more than 17%. The last three years were golden years for the industry, which clocked a 20%/30% value growth for total/organized market segments.

First, the COVID-19 pandemic disrupted the unorganized sector more severely than organized players. Lockdowns and restrictions hit small, independent jewelers—often cash-based and lacking digital infrastructure—harder, as physical stores closed and consumer footfall plummeted. Organized retailers like Tanishq, Kalyan Jewellers, and Senco had the resources to pivot quickly to e-commerce and omnichannel strategies. For instance, Tanishq rolled out virtual try-on features and online booking systems across 200 stores by July 2020, capitalizing on a shift to online shopping when consumers couldn’t visit local goldsmiths. This adaptability allowed organized players to capture demands that unorganized jewelers couldn’t fulfill.

Second, consumer behavior shifted toward trust and transparency—areas where branded retailers excel. With economic uncertainty in FY21, buyers favored established chains offering certified products, transparent pricing, and buyback guarantees over informal sellers. Industry reports from later years note a growing preference for branded jewelry, a trend accelerated by the pandemic as people sought reliability amid chaos. Organized retailers’ use of karatometers, authenticity certificates, and exchange schemes further eroded the unorganized sector’s edge.

Industry revenue and profit pool

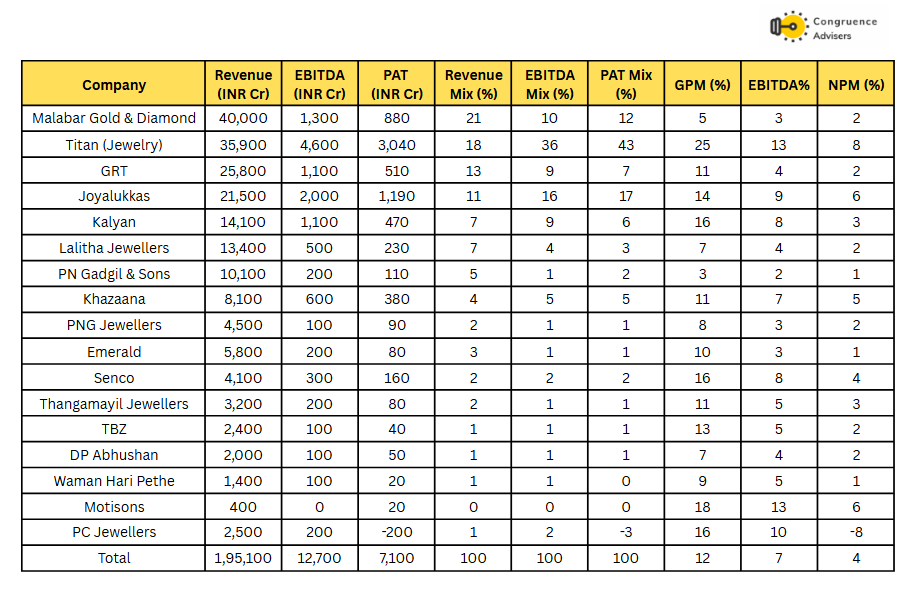

Industry revenue and profit pool. Although organized players have benefited from the change in consumer preferences, each player has a different business model within the industry. Jewellery is a highly localized market, and demand patterns vary significantly among regions. Therefore, the operating profit margin varies significantly among players despite using the same metal. The mix of bullion sales, stud ratio, and consumer preferences varies based on the financial profiles of the players. At the aggregate level, gross margins are close to 12%, with an EBITDA margin of 7% and PAT of 4%. Titan is a clear outlier with almost double the industry average gross margin (25%), EBITDA margin (13%) and PAT margin (8%). Titan is a clear outlier with almost double the industry average gross margin (25%), EBITDA margin (13%) and PAT margin (8%).

Source: MOFSL, Company

Inventory Turns (x) – As of FY23

Inventory turns are a very key metric for jewellery retailers. Unlike other retail formats such as apparel and QSR, inventory forms a bulk of the investment required for a jewellery retail store. In fact the amount spent towards capex and debtors are both negligible compared to the amount spent towards inventory for a jewellery retailer. The jewellery retailers who sell a higher proportion of bullion tend to have higher inventory turns (but lower gross margins). A retailer who can sell higher proportion of value added jewellery at higher than industry average inventory turns, can truly hope to earn supernormal return on capital.

Top Players – ROE (%)

Top players – Background and key business Overview

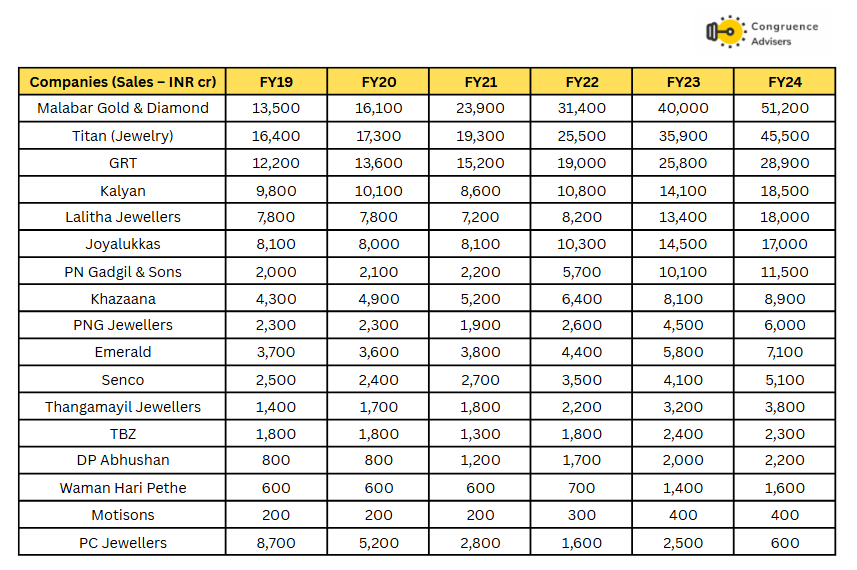

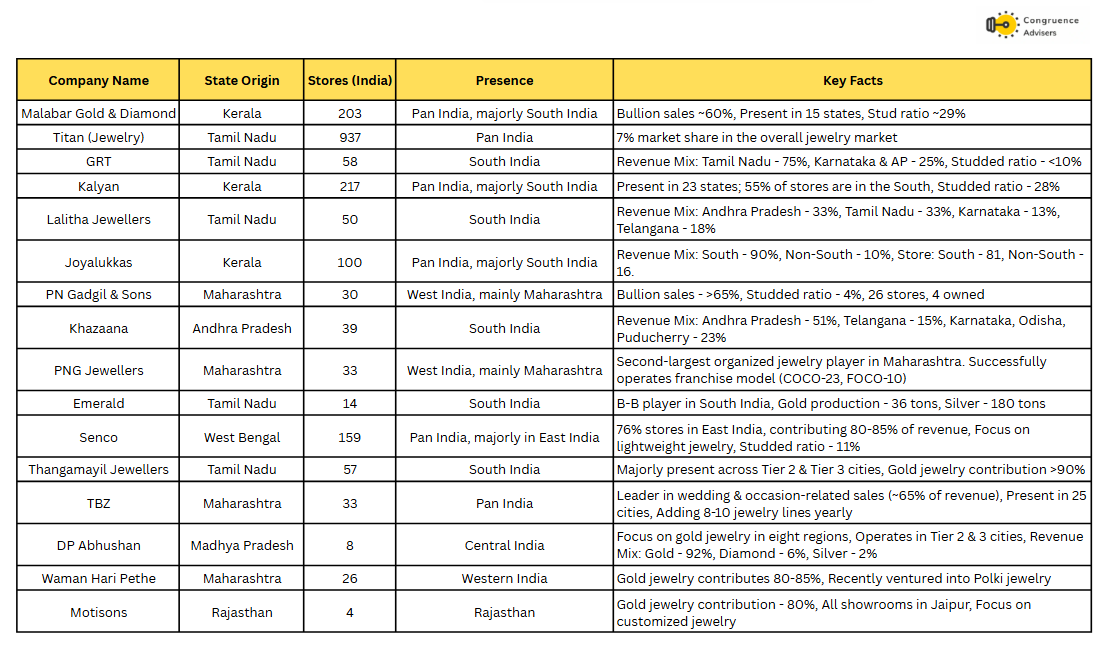

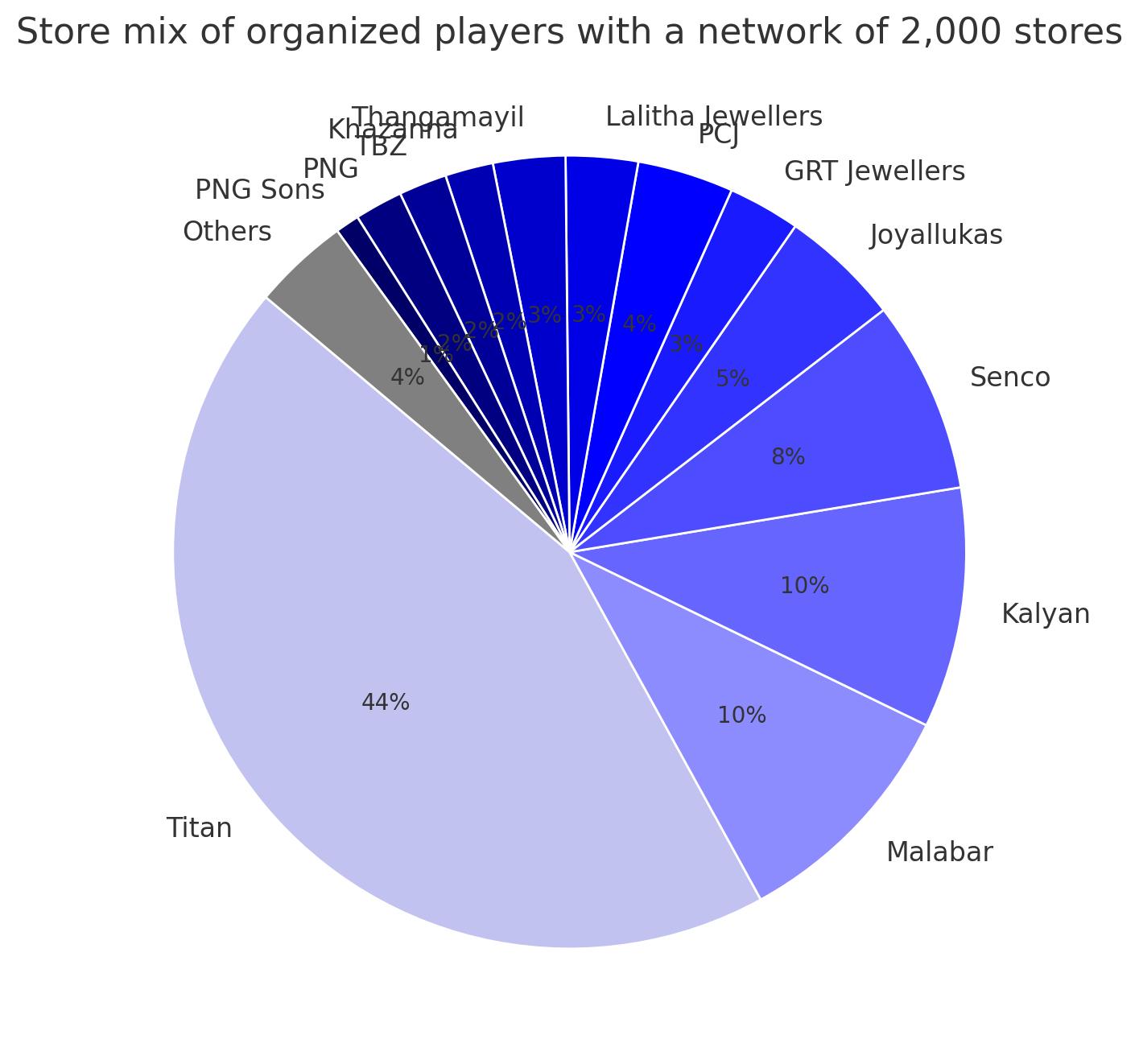

Top players’ store mix: Organized retail store network at over 2,000 stores. Titan holds the lion’s share in the organized retail sector with ~45% share in a network of over 900 stores spanning Tanishq, Caratlane, Mia, and Zoya. Other major retail players include Malabar, Kalyan, and Senco. Several players, after experiencing success in their own region, have gradually become pan-India players.

Source: MOFSL, Company

Gold Consumption Patterns in India

Jewelry consumption in India can be categorized into three segments: Bridal, Everyday wear, and Fashion jewelry. These segments have their unique attributes, offering various products, sizes, and designs. While companies like PC Jeweller and Kalyan Jewellers India are national chains catering mainly to the bridal segment, CaratLane and Tanishq cater to the daily wear segment, especially working women. Smaller independent retailers cater to their trusted client segment by focusing on specialization and customization.

Jewelry for occasions, weddings, and festivals is the primary reason for the purchase of jewelry in India. Bridal jewelry still accounts for a significant portion of demand, contributing 55% to the total jewelry demand. Daily wear jewelry accounts for 30-35% of the Indian jewelry market. Players are strategically focusing on manufacturing lightweight pieces to cater to the preferences of younger consumers, especially those who desire daily wear gold jewelry that complements Western-style attire.

Fashion jewelry, on the other hand, contributes nearly 10% to the Indian jewelry market Expectations indicate continued growth, especially among the youth seeking diverse and affordable products. Fashion jewelry, available across various value segments, materials, craftsmanship, and designs, caters to different preferences and purposes.

Source: MOFSL

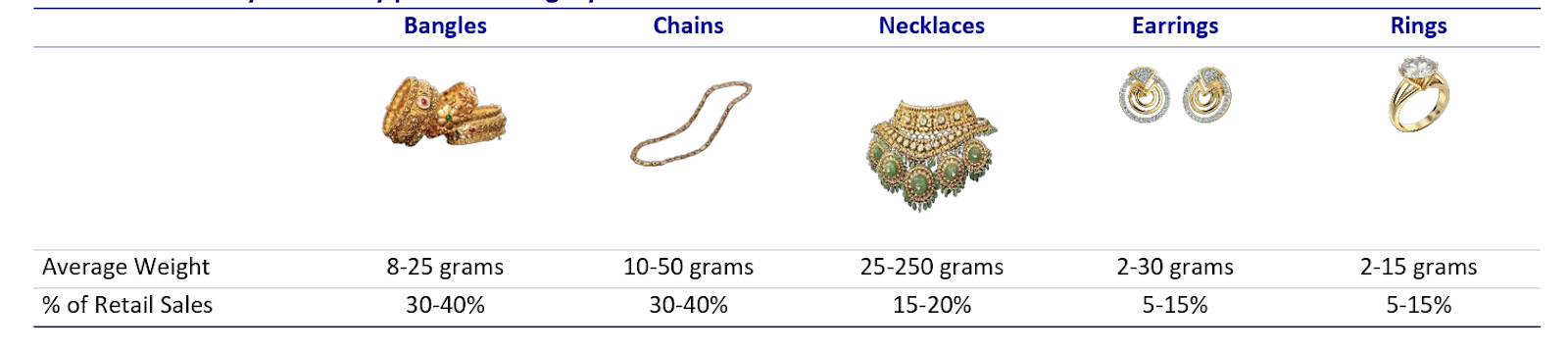

Jewelry by product category

Bangles and chains are the primary contributors to domestic jewelry consumption, accounting for 60-70% of total sales. These are preferred as daily wear by women.

Necklaces contribute around 15-20% to the sales volume, with their sales surging during special occasions, such as festivals and weddings. The remaining 5-15% of sales is attributed to rings and earrings.

Jewelry Demand Pattern

Global gold production is ~3,600 tonnes, while India imports ~900 tonnes, of which ~60-65% is consumed for jewelry. As per the industry, recycled gold contributes ~20% of India’s gold consumption for jewelry.

The last three years were golden years for the industry, which clocked a 20%/30% value growth for total/organized market segments.

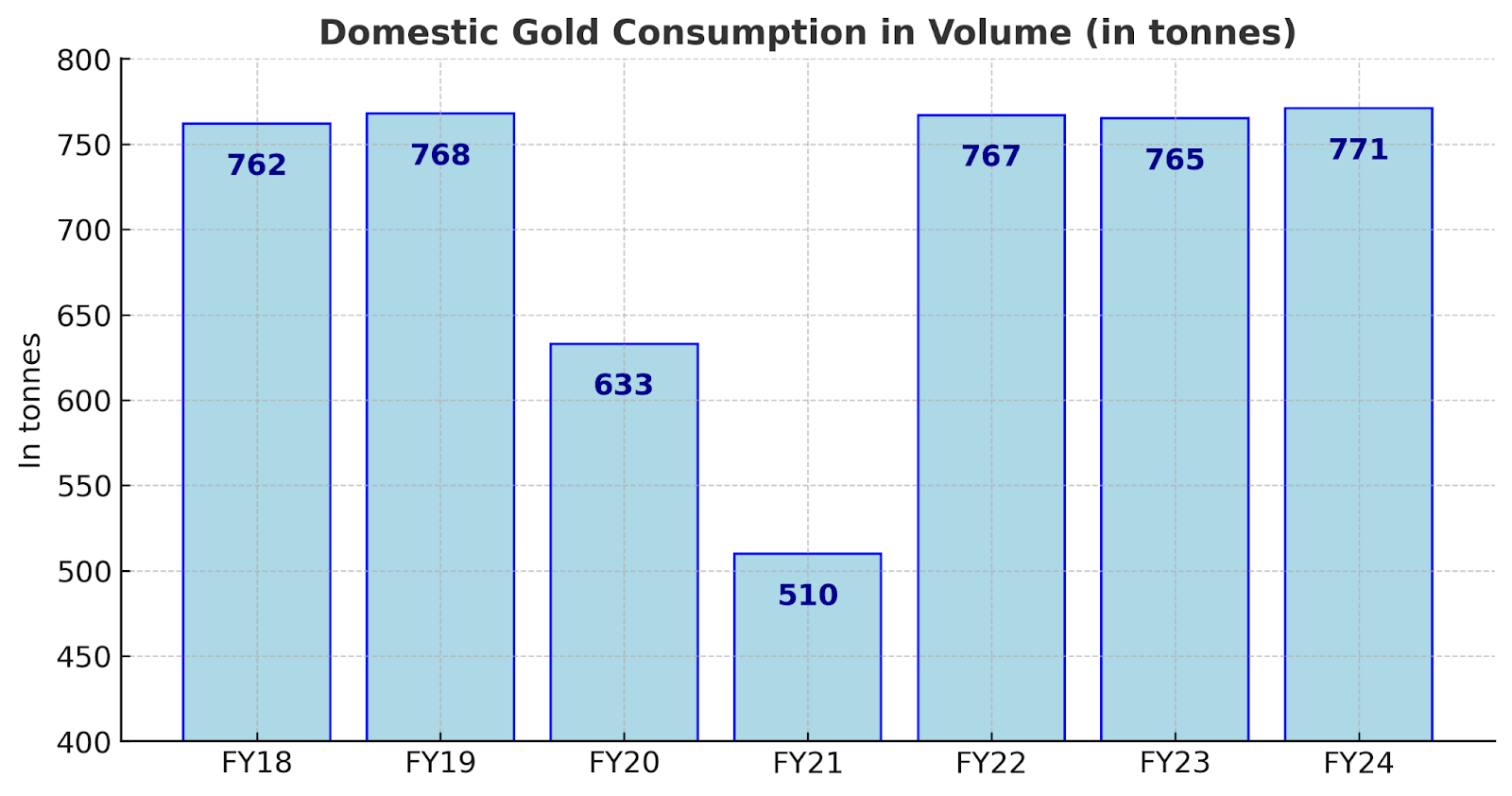

The closure of stores for a significant period and intermittent lockdowns in select states during that time further exacerbated the decline. Post-COVID, the revival trend persisted due to increased wedding-related purchases and an improvement in overall consumer sentiment.

In FY22, there was a notable improvement in the volume of gold to reach 767 tonnes from 510 tonnes in FY21. This surge was propelled by heightened discretionary spending and the gradual easing of the pandemic’s impact. The deferral of weddings due to the pandemic led to pent-up demand during FY22, contributing to a 50% surge in overall demand.

However, FY23 witnessed a marginal decline in domestic gold demand, attributed to the escalation of import duty from 7.5% to 12.5% starting 30th Jun. The first quarter of FY23 saw an improvement in gold demand, attributed to a low baseline and increased purchases for festivities and weddings. Nevertheless, the higher import duty prompted retailers to transfer the additional costs to customers, adversely impacting discretionary purchases.

Domestic gold consumption (in tonnes) and Price (in INR/10 grams) correlation

Source: MOFSL

Regional Insights

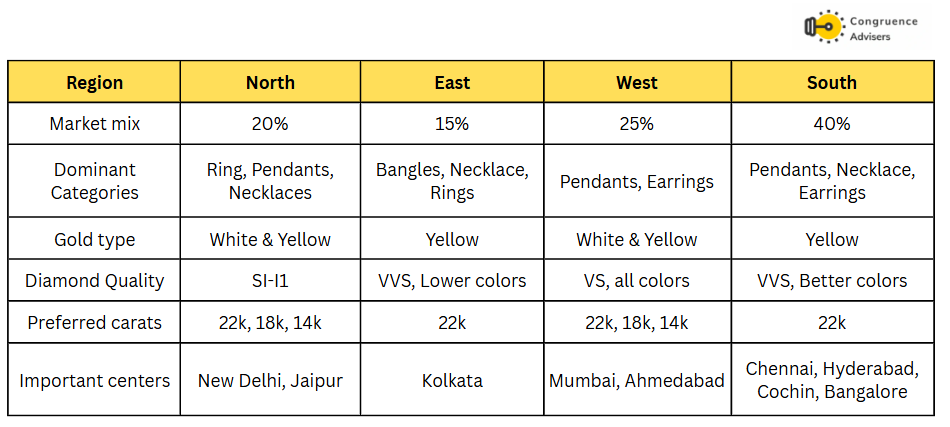

Regional variations in jewelry demand and their impact on profitability In the southern states of India, consumer purchasing behavior tends to favor traditional plain gold jewelry, which usually has lower margins.

Consumers in the northern and western regions of India are more receptive to studded jewelry and impulse-led, lighter-weight jewelry purchases (14k, 18k jewelry) vis-à-vis their southern counterparts.

Plain gold jewelry typically has a gross margin ranging from 10% to 14%, while diamond-studded jewelry has a gross margin ranging from 30% to 35%.

Consequently, as the studded ratio (studded jewelry/total revenue) goes up, profitability improves, thereby incentivizing South-focused retailers to expand towards the North, West, and East.

Regional jewelry demand and preferences

Seasonality in Gold Purchases

Seasonal and regional factors to drive Jewelry demand are also very seasonal in nature, with different seasonal patterns across regions in India. Jewelry demand peaks during the months leading up to popular wedding seasons, such as May-June, September-November, and January. Agricultural output and monsoon patterns influence gold demand in Tier II and Tier III towns. Rural households invest their proceeds from harvests in gold jewelry during the months of November and December.

Demand for gold and silver jewelry improves during auspicious religious events such as Diwali/Dhanteras in October and November and Akshaya Trithiya in April and May.

Source: MOFSL

India’s gold supply is dominated by imports

The gold market experienced notable fluctuations in imports from FY18 to FY20, reaching 980 tonnes in FY19 before declining to 720 tonnes in FY20.

Source: MOFSL

This volatility was led by various factors, including declines in global gold prices, buoyant economic conditions leading to heightened disposable incomes, and substantial demand for gold due to traditional celebrations and weddings. However, in FY20, a significant drop occurred due to escalating import duties and the initial stages of an economic slowdown.

Recovery signs emerged in FY22, marked by an increase in imports to 879 tonnes. Factors contributing to this rebound included gold’s appeal as an inflation hedge and the release of pent-up demand following the easing of pandemic restrictions.

However, in FY23, imports experienced a slight reduction to 678 tonnes, possibly influenced by government measures aimed at managing the current account deficit and promoting domestic gold recycling.

Procurement value chain for organized Jewelers in India

Source: MOFSL

Retail business comparison

The jewellery wholesale sector in India has traditionally been highly fragmented and dominated by unorganized firms. The unorganized sector dominates the wholesale industry, and organized wholesale penetration in India is comparatively lower than in developed countries. In the Indian wholesale jewellery sector, the unorganized segment accounts for the lion’s share with about 85% plus share.

Sky Gold Ltd Business Overview

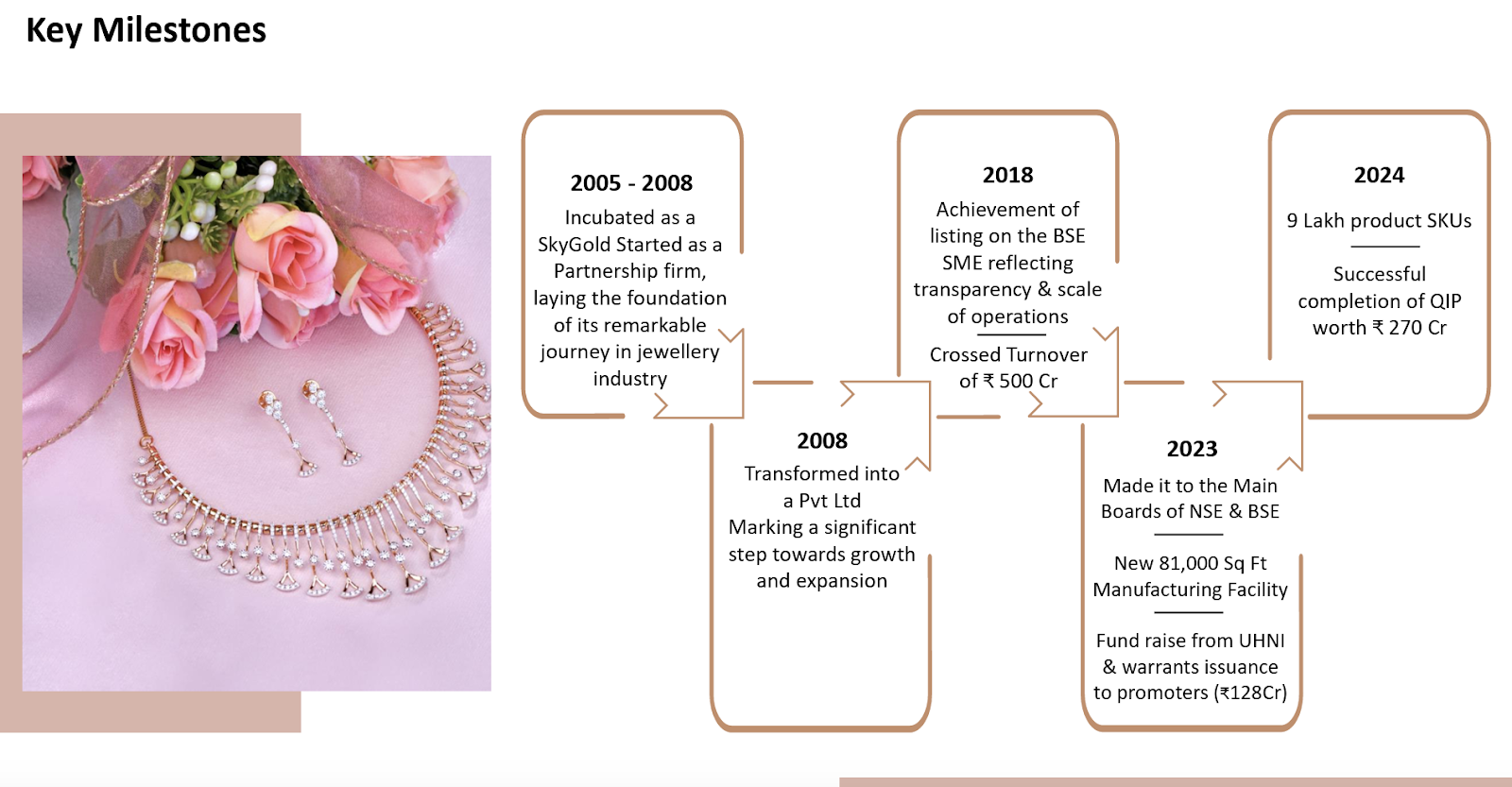

Sky Gold Ltd was incubated as a Partnership Firm in the year 2005, laying the foundation for its remarkable journey in the jewelry industry. Later on, it was incorporated as a private limited Company with the name Sky Gold Private Ltd on May 7, 2008, marking a significant step towards growth and expansion. After working as a Private Limited Company, the status of the Company was changed to a public limited Company, and the name of the Company was changed to Sky Gold Ltd on June 26, 2018. The Company decided to be listed on the SME Platform of BSE, and the Company was first listed on the BSE SME Platform on October 03, 2018, as “Sky Gold Ltd.” Sky Gold Ltd spent more than 4 years in BSE’s SME platform and then successfully migrated to the Main Board of BSE & listed its securities on NSE Limited on January 06, 2023. Now, Sky Gold Ltd’s securities are available for trading on BSE and NSE Limited.

Sky Gold Ltd manufactures its Jewelry in its 81,000 Square Feet manufacturing facility in Navi Mumbai, India, with the help of German & Italian Equipment. The Company has having capacity of processing 750 Kg to 800 Gold per month. In Q3FY25, capacity increased to 1050 kg per month due to the acquisition of promoter-owned companies. Sky Gold Ltd has a design library of more than 5,00,000 designs of rings, bracelets, bangles, fancy pendants, earrings, etc.

Product offerings:

Sky Gold Ltd offers gold jewellery in the affordable range, starting from Rs 5,000 to ~Rs 1 lac. It specializes in lightweight jewelry of 18 and 22-carat gold; further, Sky Gold Ltd makes plain, studded, and Turkish jewelry.

They cater to a variety of customers across mid-market and value-market segments, and products are designed by our in-house team of creative designers, allowing them to manage a large and diverse portfolio of designs.

Their product range includes necklaces, rings, pendants, bracelets, earrings, bangles, and customized jewelry based on customer demand. They have incorporated the latest technology for our manufacturing facility, which reduces our turnover time from order receipt to delivery to just 72 hours. Its products are available in over 2,000 showrooms across India. With a vast design library of over 9 lakh designs, Sky Gold Ltd produces approximately 3,000 pieces daily.

Product Categories:

- Plain gold jewelry

- Studded gold jewelry

- Diamond-studded jewelry

- Turkish Jewelry

Sky Gold Ltd continues to expand into new jewelry segments, including:

- 18K gold

- Natural diamond jewelry

- Lab-grown diamond jewelry

Offering exclusive designs across 14 product categories, Sky Gold Ltd provides customized designs for corporate jewelers, with an active portfolio of approximately 3 lakh SKUs.

Sky Gold Owned Sub-Brands:

- Tazim – Celebrating Turkish and Kuwaiti traditions

- Rangi – Specializing in color stone designs

- Sky9 – Representing elegant bonds

The top 5 customers contribute more than 55% to the gross revenue, while the top 10 customers contribute more than 72%. The top 10 players are the reputed brands in the gold retail industry, namely Malabar Gold, Kalyan Jewellers India, Joyalukkas India Pvt Ltd. SGL also caters to GRT Jewellers India Pvt Ltd, Senco Gold Limited, and Khazana Jewellers Pvt Ltd.

Order patterns of various clients

Malabar Gold & Diamonds operates on a replenishment system. It acquires designs from Sky Gold Ltd, which doesn’t offer these designs to any of its other customers. Showrooms place their orders after these designs go live on Malabar’s internal system. The stores can order multiple times based on how a design is performing. Skygold gets a high volume of orders from this replenishment system. Malabar Gold also keeps buffer stock at the regional level.

Joyalukkas India operates on a multiple-order system. Each showroom in a particular region places its own orders. The company also places orders on weight terms (such as 20kg of rings). Sky Gold Ltd sends a set of 20kg rings based on different designs.

Kalyan Jewellers operates on an open purchase (designs sent by Skygold) as well as a design locking system. Senco Gold operates on a design locking system.

Smaller players attend exhibitions and select their designs.

Receivables: Malabar Gold pays three days after delivery, Joyalukkas India after a week, and Kalyan Jewellers within 25 days.

Recent acquisitions to provide entry into new segments of chains and mangal sutra

Sky Gold Ltd has acquired 2 promoter-owned companies in FY25. Acquisition of group companies with a combined turnover of 370Cr was done for 50Cr via share swap and took over 38Cr promoter debt in Jun CY24, implying an EV of 88Cr. The companies together reported 7.5Cr PAT in FY24, implying a 2% PAT margin and potentially a 3.5% EBITDA margin, implying acquisition valuations of < 7x EVEBITDA and < 7x PE.

The rationale for acquisition – Has expanded share of wallet for Sky Gold Ltd

- Sky Gold Ltd standalone was is doing casting jewellery, which accounts for 40% of consumption in a retail store

- Starmangalsutra is doing mangalsutras, which is 15% consumption in a store

- Sparkling chains are 80% machine-led process for making chains; 25% is consumed in a store

Export

It has launched products in the UAE, Malaysian, and Singaporean markets. Exports contributed 6% to overall revenue in FY24. Sky Gold Ltd is planning to grow its export revenue multi-fold and take it to 20-30% of overall revenue. Do note that the margin in the export business is better, and payments are made on the spot.

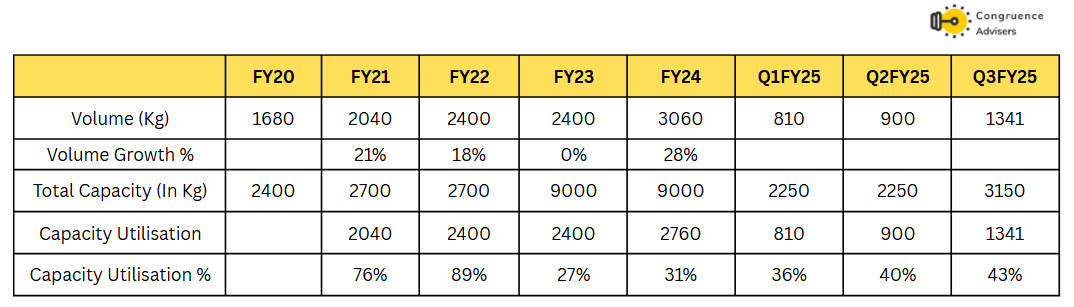

Manufacturing Facilities and Capacity

Sky Gold Ltd has transitioned from its older manufacturing facility in Mulund (West), Mumbai, which had an area ranging from 2,740 sq. ft. to 18,000-20,000 sq. ft. and then 25,000 sq. ft. This older facility had a production capacity of approximately 300 kgs per month.

Sky Gold Ltd now operates from a significantly larger 81,000 sq ft manufacturing facility located in Navi Mumbai, which became operational in August 2023.

The current production capacity of the Navi Mumbai facility is between 750 kg to 800 kg per month. The volume turnover in Q3 FY25 was 449 kgs per month. In Q3 FY25, capacity utilization was reported at 43%.

Sky Gold Ltd has also acquired subsidiaries, such as Star Mangalsutra Private Limited and Sparkling Chains Private Limited. These subsidiaries together contribute an additional manufacturing capacity of 300 kg per month. The current capacity utilization of the subsidiary companies is approximately 30%-33% and overall at 40% in the last few quarters. Therefore, the total current manufacturing capacity of Sky Gold Ltd, including its subsidiaries, is around 1050 kgs per month.

Sky Gold Ltd manufacturing style seems like it is made using German and Italian casting machines.

Sky Gold Ltd’s position as a B2B manufacturer allows it to have a better understanding of jewellery trends and choices, as compared to jewellery retailers.

Granular Understanding of End Consumers: Sky Gold Ltd has gained a deep understanding of end consumers by working with many large Indian retailers. This helps them understand that jewellery preferences vary from region to region.

Close Relationships with Retailers: Sky Gold Ltd solves the inventory management challenges of jewellery retailers, fostering close, sticky relationships. If retailers can quickly sell Sky Gold’s designs, it leads to more sales and orders for Sky Gold Ltd.

Extensive Design Team and Library: Sky Gold Ltd has a design team that helps them maintain a design library. They are constantly refreshing their designs to ensure they are current and appealing to consumers. Sky Gold Ltd has a design library of more than 500,000 designs. Sky Gold Ltd has a design library of 900,000 designs, with 200,000 to 250,000 designs being live. Sky Gold Ltd floats 2,000-2,500 designs every month.

Ability to Design Demographic Preferences: Sky Gold Ltd can design jewellery products based on the latest trends, fashion, and demographic preferences of end-users.

Responsiveness to Customer Needs: Sky Gold Ltd has increased responsiveness to end-customer requirements.

Market Research: Sky Gold Ltd conducts continuous market research to understand the latest trends and end-customer tastes and preferences

Customization and Exclusivity: Sky Gold offers exclusive, customized design catalogs and consistently provides quality products. They create separate designs for every corporate jeweller.

Emphasis on Lightweight Jewelry: Sky Gold specializes in lightweight jewellery.

Diverse Product Portfolio: Sky Gold has a diversified product portfolio and is well-positioned to leverage growth opportunities in both Indian and international markets.

Gold metal loans lead to lower interest costs – The transition to Gold Metal Loans (GML) is projected to significantly impact Sky Gold’s profitability through reduced interest costs, though it will require collateral.

Impact on Profitability

Sky Gold Ltd anticipates a substantial decrease in interest costs by transitioning to GML. Sky Gold Ltd has expressed that interest costs, which are currently at 9.5%, would be reduced to 4.5% with gold metal loans.

Sky Gold Ltd will need to provide collateral, typically in the form of fixed deposits (FDs), to secure the GML. The collateral required might range from 30% to 40% of the loan amount. The implementation of GMLs will help to reduce hedging costs for Sky Gold Ltd. By reducing finance costs, GML is expected to increase the company’s PAT margins. Sky Gold Ltd is targeting a PAT% of 3% to 4% in the next three years, with the initial target being 3%.

GML Strategy and Implementation

Sky Gold Ltd plans to transition to GML in phases. Initially, they aim to utilize 70% to 80% of the GML facility and then move towards 100% as the bank permits. Sky Gold Ltd expects to convert 50% to 55% of its debt to GML by the end of a given period and aims to reach 75% to 80%. Sky Gold Ltd plans to increase its debt from INR 240 crores to INR 250 crores, with 70% to 80% of it being GML. The inventory will be funded by GML. Banks are renewing and changing Sky Gold Ltd’s facilities to GML. ICICI Bank has already granted Sky Gold Ltd INR 100 crores of GML. Collateral Transition: Sky Gold Ltd plans to replace existing equity share collateral with fixed deposits. Sky Gold Ltd will receive back INR 70 Cr shares and give INR 40 Cr to INR 45 Cr in FD.

Sky Gold Ltd Corporate governance

Board Composition – The Board of Directors for Six Gold Ltd comprises 6 directors, of whom 3 are Independent and 5 are non-independent. Mangesh Chauhan acts as the Managing Director & CFO. Darshan Chauhan & Mahendra Chauhan act as Whole-time Directors.

Promoter Remuneration – The total remuneration to promoters for FY24 amounted to INR 2.36 Cr. All three promoters take 78.75 lakhs each. Total promoter remuneration as % of PAT amounted to ~5% in FY24.

Related Party Transactions – The transactions involving share warrants, the rent paid to them, and the acquisition of Sparkling Chains LLP and Starmangalsutra LLP represent the high-value related party transactions in FY24.

Contingent Liabilities – According to the annual report for FY24, the total amount of contingent liabilities amounts to ~INR 21.30 lakhs only, which is related to the GST Issue.

Sky Gold Ltd Financial Performance

Over the last 5 years, Sky Gold Ltd. has grown revenues at a CAGR of 17%, EBITDA at a CAGR of 49%, and PAT at a CAGR of 68%, demonstrating a steady growth trajectory. During this period, EBITDA and PAT margins have outperformed the revenue growth; EBITDA margins increased from 1% in FY20 to 5% in FY24, and PAT margins around 1-2%, respectively. Over the 3 years, Sky Gold Ltd has grown revenues at a CAGR of 30%, EBITDA at a CAGR of 85%, and PAT at a CAGR of 104%.

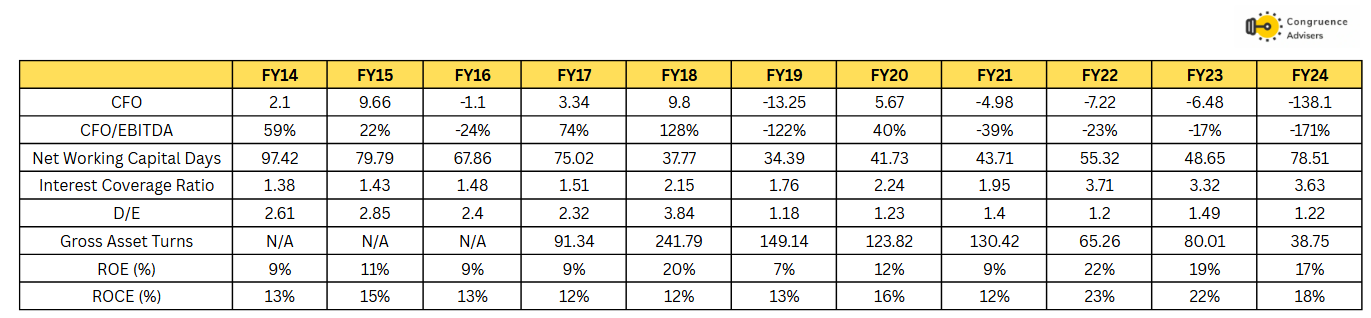

Sky Gold Ltd Return Ratios, Working capital, Debt, and cash flow analysis

Although Sky Gold Ltd has shown remarkable growth in its P&L over the years, one thing that bothers us quite a bit is the lack of cash flow generation since inception. Between FY14-FY23, the net CFO generated by the company was almost zero and in FY24 the CFO was INR -138 Cr. Therefore the 17% CAGR revenue growth through its history, has been funded by external cash flows in terms of debt and equity dilution.

Sky Gold Ltd Comparative Analysis

To understand Sky Gold Ltd investment potential, We have conducted a comprehensive analysis. This analysis includes comparing Sky Gold Ltd to its competitors (peer comparison) on various fundamental parameters and Sky Gold Ltd share performance relative to relevant benchmark and sector indices.

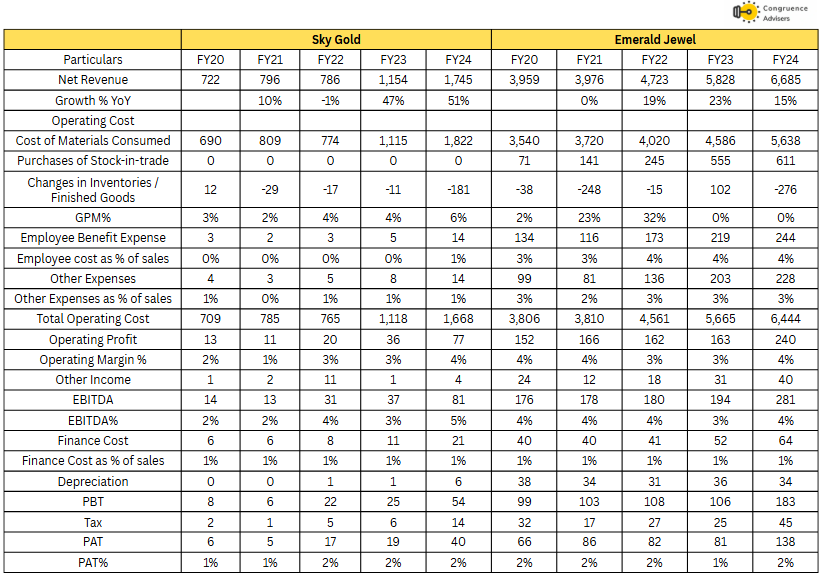

There are no like-for-like strong peer companies of Sky Gold Ltd listed in India. Emerald Jewel Industries Ltd is a private company that is currently the leading player in casting jewellery in India, with Sky Gold Ltd being the second largest in this segment.

Emerald Jewel is one of the leading jewellery manufacturers with an established presence both in the manufacturing and the retail segments. Its flagship brand, Jewelone, enjoys strong recall, and its performance over the years has been supported by its diversified business profile and established network across the value chain. Emerald Jewel is one of the largest organised jewellery manufacturers with a production capacity of 36 tonnes of gold jewellery and 180 tonnes of silver jewellery per annum & 4 plants in Coimbatore.

Both Sky Gold Ltd and Emerald have shown impressive growth in revenues between FY20 and FY24 suggesting strong momentum in the organised jewellery manufacturing space. While Emerald has superior gross margins (double digit), the EBITDA and PAT margins for both companies are at similar levels.

Sky Gold Ltd Index Comparison

Sky Gold Ltd share performance vs S&P BSE Small cap Index as the index benchmark comparison is a fundamental tool for understanding the investment potential and making informed decisions in the context of the broader market

Why You Should Consider Investing in Sky Gold Ltd

Sky Gold Ltd offers some compelling reasons to track closely and to consider investing if one is looking to invest in the Indian jewellery market.

Shift towards larger organized gold manufacturers – Large retailers are eating the share of unorganized/single-store players. A similar trend is being witnessed in the B2B gold manufacturing outsourcing space as well, with large retailers opting to source more from large suppliers, which makes operations more efficient. Large jewellery retailers outsource almost 75-80% of their requirements from numerous small manufacturers. Currently, organized gold manufacturers share 10-15%, which is expected to increase going forward.

Acquisitions to provide an entry in new segments of chains and mangalsutra – Sky Gold Ltd’s acquisition of promoter-owned entities Star Mangalsutra and Sparkling Chains significantly enhances its product portfolio, expanding its presence from casting jewellery (40% of a typical retail store’s consumption) to include mangalsutras (15%) and machine-made chains (25%). This strategic move increases its share of wallet to nearly 80% per store, strengthens its position in the B2B segment, and was executed at compelling valuations of under 7x EV/EBITDA and PE, making it both a synergistic and value-accretive transaction.

Capacity Expansion – Sky Gold Ltd undertook a significant capacity expansion in FY24, shifting to a new 80,000 sq. ft. facility in Navi Mumbai from its earlier 25,000 sq. ft. setup at a cost of ₹20 crore. This upgrade, along with advanced machinery, increased its monthly production capacity from 300 kgs to 750 kgs. Additionally, the acquisitions of Star Mangalsutra and Sparkling Chains added another 300 kgs of monthly capacity, taking the total to 1,050 kgs in FY25—a 3.5x rise from FY23 levels—to support growing demand and scale operations.

New Client Onboarding & Asset Light Model – Sky Gold Ltd has onboarded several prominent clients in FY25, including CaratLane, PN Gadgil, and Aditya Birla, significantly strengthening its customer base. This development has led the management to revise its long-term revenue guidance for FY27 upwards—from ₹6,200 Cr to ₹7,200 Cr. Sky Gold Ltd is strategically targeting and onboarding new clients who provide their own raw materials (gold), such as Aditya Birla Novel Jewels and CaratLane. For these clients, Sky Gold Ltd primarily charges a making charge and does not need to fund the gold inventory. Sky Gold Ltd expects that in the next two years, 30% to 40% of its raw material could be provided by such clients.

Shift to Gold Metal Loans to Improve Profitability – Sky Gold Ltd is transitioning to gold metal loans (GML) to meet its working capital needs, which is expected to significantly reduce interest costs. While traditional working capital loans carry an interest rate of around 9.5%, GMLs are available at a lower rate of 4–7%. With the GML share in total debt rising from 0% in FY24 to 20% in Q3FY25—and projected to reach 70–80% by FY27—this shift is expected to boost PAT margins by 30–40 basis points.

What are the Risks of Investing in Sky Gold Ltd

Investors need to keep the following risks in mind if they choose to invest into this business. Risks needs to be weighed in combination with the advantages listed above to arrive at a decision that is optimal for your portfolio construct.

Lack of operating cash flows – In our view, the biggest weakness in Sky Gold Ltd’s business metrics, lies in its chronic inability to generate cash flows through its history. Sky Gold Ltd aims to grow revenues rapidly over the next 2 years at a CAGR > 40%. This will mean a lot of incremental working capital will need to get funded (in spite of significant scale up in the asset light model). This working capital will likely be funded via debt or additional equity dilution. These approaches put pressure on the balance sheet and reduce EPS growth vs PAT growth. The Sky Gold Ltd management has said that it expects to start generating positive CFO from FY27. This remains a key monitorable for us to gauge sustainability of the business model at high rates of growth.

Competition – Sky Gold Ltd operates in a highly competitive market that includes both organized and unorganized players. The presence of smaller, unorganized entities can pressure pricing and margins, while established competitors, particularly in the casting jewellery segment, pose significant challenges. Unorganized players have an 80-85% market share in the gold manufacturing segment.

Gold Price Volatility – As a jewellery manufacturer, Sky Gold Ltd is inherently exposed to fluctuations in gold prices. Although Sky Gold Ltd employs strategies like gold metal loans and hedging to manage this risk, price volatility can still impact consumer demand and inventory valuation.

Regulatory Environment – The jewellery industry is subject to frequent changes in government policies, including import duties and compliance regulations. While some recent changes have been favorable, any adverse shifts could impact the profitability and operational efficiency of Sky Gold Ltd

Operational Risks – Manufacturing disruptions, supply chain inefficiencies, and the potential for gold loss during production are inherent risks. Additionally, the high value and portable nature of jewellery inventory necessitate strong safeguards to prevent theft or fraud.

Sky Gold Ltd Future Outlook

Sky Gold Ltd is shaping up to be a strong growth story, a smart strategic pivot, and rising operational efficiency. We believe Sky Gold Ltd is expected to more than double its revenue from ₹3,400 Cr in FY25 to ₹7,048 Cr by FY27. A key driver behind this growth is Sky Gold Ltd’s shift toward an asset-light model, where gold is processed for clients instead of being owned and held as inventory. While this model currently represents a small share of operations, it’s expected to contribute around 25% of total volumes by FY27, significantly improving margins.

Net Profits are also set to grow strongly, with PAT rising from ₹119 crore in FY25 to ₹249 crore by FY27 while maintaining a healthy 3.5% PAT margin. This profitability, along with Sky Gold Ltd’s guidance to become cash flow positive by FY27, reflects a strengthening financial profile. On the cost front, Sky Gold Ltd is keeping things tight—employee and other operational expenses are expected to stay under 2% of revenue, allowing for stronger operating leverage as the business scales.

On the flip side, debt levels are projected to increase from ₹458 Cr in 9M FY25 to ₹1,375 Cr by FY27, mainly to fund working capital needs, especially through gold metal loans (GML), which will make up 30% of total borrowings. While this leverage is notable, finance costs are expected to remain under control, and all working capital needs are assumed to be debt-funded without further equity dilution.

Sky Gold Ltd Technical Analysis

We consider technical analysis to be a useful input in taking medium-term investment decisions. Many a time, price action tends to lead to fundamental developments; this is too important an aspect to be ignored by retail investors who do not have access to management outside of common forums like investor calls & AGM.

At Congruence Advisers, we like to consider both the long-term weekly chart and the daily chart to arrive at a view on price action. Combined with our understanding of fundamentals, we usually end up being better placed to be able to judge both the business cycle and the stock cycle. Playing the stock cycle right is extremely important for investors looking to extract significant alpha over the medium term.

Sky Gold Ltd Price charts

On a Daily Chart, Sky Gold Ltd has been going through a consolidation phase since October 2024. Once the NIFTY 50 and the broader markets peaked out, investors have been circumspect in looking at many stocks like Sky Gold that show strong earnings growth but have limited cash flow generation. The RSI has cooled down significantly to a range of 40-50 which is a healthy indicator for potential medium term investors. The stock price has been closely tracking the 50DMA that has been acting as a resistance level since January 2025.

The stock has been moving in circuits after the management announced a large export deal with incremental volume that can be 50% of the current monthly volume.

Sky Gold Ltd Latest Result, News and Updates

Sky Gold Ltd Quarterly Results

Sky Gold Ltd delivered a strong Q3 performance, with consolidated revenue surging 116.7% YoY to ₹998 Cr and EBITDA growing 217.6% to ₹57.3 Cr. PAT rose to ₹36.5 Cr, improving margins to 3.7% from 1.9% last year. For 9MFY25, revenue stood at ₹2,489.8 crore, up 102% YoY.

Sky Gold Ltd has onboarded key clients like Aditya Birla’s Indriya and deepened ties with CaratLane and P.N.Gadgil, driven by strong wedding jewellery demand and industry expansion. It diversified into 18-carat and lab-grown diamond jewellery, prompting a rebrand to Sky Gold and Diamonds.

Production rose 66% YoY to 447 kg/month, with exports touching ₹71 crore. A credit upgrade to IND A-/Stable is expected to lower borrowing costs, with gross debt projected at ₹550–600 crore next year, primarily for gold metal loans (GML).

FY27 revenue guidance has been raised to ₹7,200 crore, with expected PAT margins of 3.5–4% and positive cash flow by 2027. Capacity stands at 1 ton/month, with plans to scale to 4 tons post-FY27. While high gold prices pose near-term demand challenges and GML conversion is slower than expected, management remains confident of reaching 60–70% GML mix by March 2025 and sustaining long-term growth.

Our view is that this will continue to be a high beta stock with excellent earnings growth potential but with the fragility of high working capital and debt. The fundamental view will change for the better once the business starts generating positive operating cash flows (likely by FY27 going by the management guidance). On a market cap to cash flow basis, the valuation looks extremely stretched. Conservative investors are unlikely to get too enthused with the business model until the unit economics change in favour of healthier cash flows. Unless an investor is willing to take this forward looking call on cash flows, it will be difficult to justify the current valuation on a conventional basis (which sees cash flows as the most important variable in business valuation).

For margins to improve, the customer profile will need to pivot in favour of more customers from the current top heavy profile. Large Jewellery chains are unlikely to permit considerable margin improvements since the balance of power will always be skewed in favour of large, institutional customers.

Disclaimer – This note is part of a business research & analysis series on small companies, there is no BUY/SELL recommendation or target price issued as part of this. There is no assurance that this stock makes for a good investment, there is no guarantee that this stock will be included in the coverage universe of Congruence Advisers. The note contains some forward-looking statements and insights drawn from the historical results, annual reports and investor presentations; they are to be viewed only within this context and not as a prediction of future performance of the business or the stock covered.

While due care has been taken to ensure that the information here is as accurate as possible, Congruence Advisers disclaims any liability in case of any unintentional inaccuracies.

The content does not constitute investment advice.

Disclosure – No position (April 2025)