MPS Ltd is a premium B2B learning and platform solutions company that powers the education, research, and corporate markets in its quest to engage with its learners more meaningfully. MPS Ltd’s purpose is “to help make learning accessible to ALL,” which unifies their diverse talent pool of over 3,000 professionals spread across 10 countries.

High margin, high cash flow business set to become a high growth business too?

MPS Ltd presents an interesting investment opportunity as it transitions from a margin-focused consolidator to a scalable growth platform. With a good track record of acquisitions, efficient integration capabilities and a clean balance sheet, MPS Ltd is well-positioned to ride the next leg of growth. Its ability to generate consistent free cash flow, coupled with disciplined capital allocation, provides financial flexibility for further expansion. With management targeting 1,500 Cr sales by FY28, MPS Ltd is quietly building into a differentiated digital-led publishing solutions platform with potential valuation re-rating ahead.

MPS Ltd Company Summary

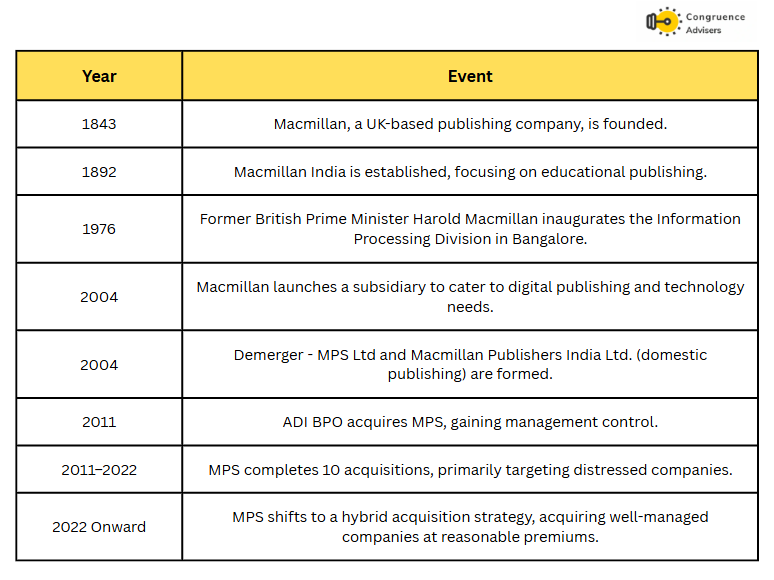

MPS Ltd is a leading global provider of platforms, content, and learning solutions for the digital world. It was established as an Indian subsidiary of Macmillan (Holdings) Limited in 1970. The long service history as a captive business allowed MPS to build unique capabilities and talents through strategic partner programs.

MPS Ltd is now a global partner to the world’s leading enterprises, learning companies, publishers, libraries, and content aggregators. After a change of majority stake in 2011-12 and with an entrepreneurial mindset, MPS Ltd developed significant momentum as a result of consistent reinvestment in the business and seven successful acquisitions in the same number of years.

MPS Ltd History

Since its acquisition by the ADI Group, MPS Ltd has demonstrated a strong ability to execute successful and meaningful acquisitions. MPS Ltd has completed 10 acquisitions at favorable valuations, not only revitalizing struggling entities but also seamlessly integrating them into its broader operations.

Until 2022, MPS Ltd primarily focused on acquiring distressed companies at discounted valuations. However, there has been a notable strategic shift. MPS Ltd is now open to acquiring well-managed businesses, even if it means paying a reasonable premium. This transition reflects a thoughtful move toward a hybrid acquisition strategy, which we expect MPS Ltd to continue pursuing in the future.

MPS Ltd Management Details

Rahul Arora is the Chairman and CEO of MPS Limited. Under his leadership, MPS Ltd has significantly diversified its business interests, transitioning from an India-based content services provider to a Global market leader in learning and platform solutions.

Rahul joined MPS Ltd in Noida, India, in August 2012 as Chief Marketing Officer to lead and develop the growth of MPS Ltd. Rahul relocated to the U.S. in early 2013 to jumpstart the first wave of US-based acquisitions (2013–15) via a newly established subsidiary, MPS North America LLC. After the successful integration and growth of these assets, Rahul was promoted by the Board of Directors to lead the diversification agenda as CEO and Managing Director of MPS Ltd. Rahul powered the diversification phase between 2015 and 2020 with the acquisitions of marquis market players, including HighWire Press (founded at Stanford University), and the purchase of TIS (a division, founded in 1990, as part of one of the largest Indian conglomerates), which propelled MPS Ltd further into an accelerated trajectory. Much of MPS Ltd’s story during this period was inorganic. Each acquisition was unlocked for tremendous synergies, enhancing MPS Ltd long-term competitive advantage.

MPS Ltd – Industry Overview

Expected growth rate across various Publishing and eLearning subsegments

source: keynote, MPS ltd

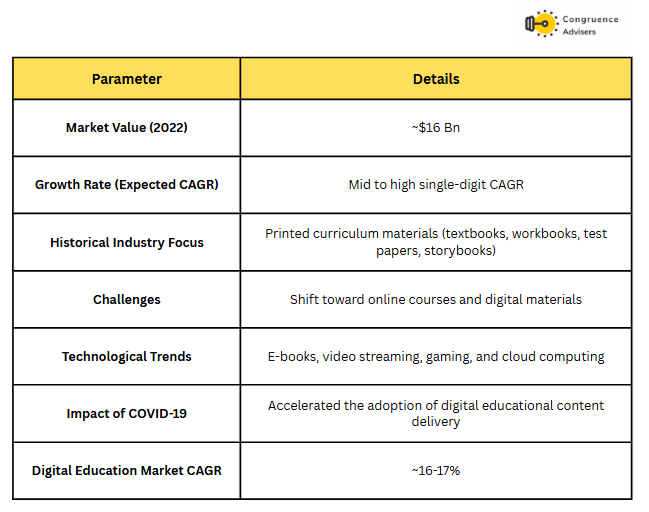

Global Education Publishing Industry

Major Publishers Globally

Source: keynote, MPS ltd

Global E-Learning Industry

In 2020, the global e-learning industry was valued at $250 Bn and was projected to grow at a CAGR of ~21% until 2027, surpassing the $1 Tn mark in opportunity. The COVID pandemic resulted in a paradigm shift, and the industry saw drastic digitalization of operating models, which also included training and development programs. Advanced technologies like AI, VR, and cloud-based Learning Management Systems (LMS) are driving growth in the e-learning sector. The rise of AI-enabled e-learning solutions is enabling the creation of intelligent content, digital study aids, and live interactive assessments.

Both schools and businesses are embracing interactive tools to boost student engagement and enhance the overall learning journey. As a result, Edtech providers are expanding their offerings to meet this growing demand for innovative educational products and services.

MPS Ltd Business Details

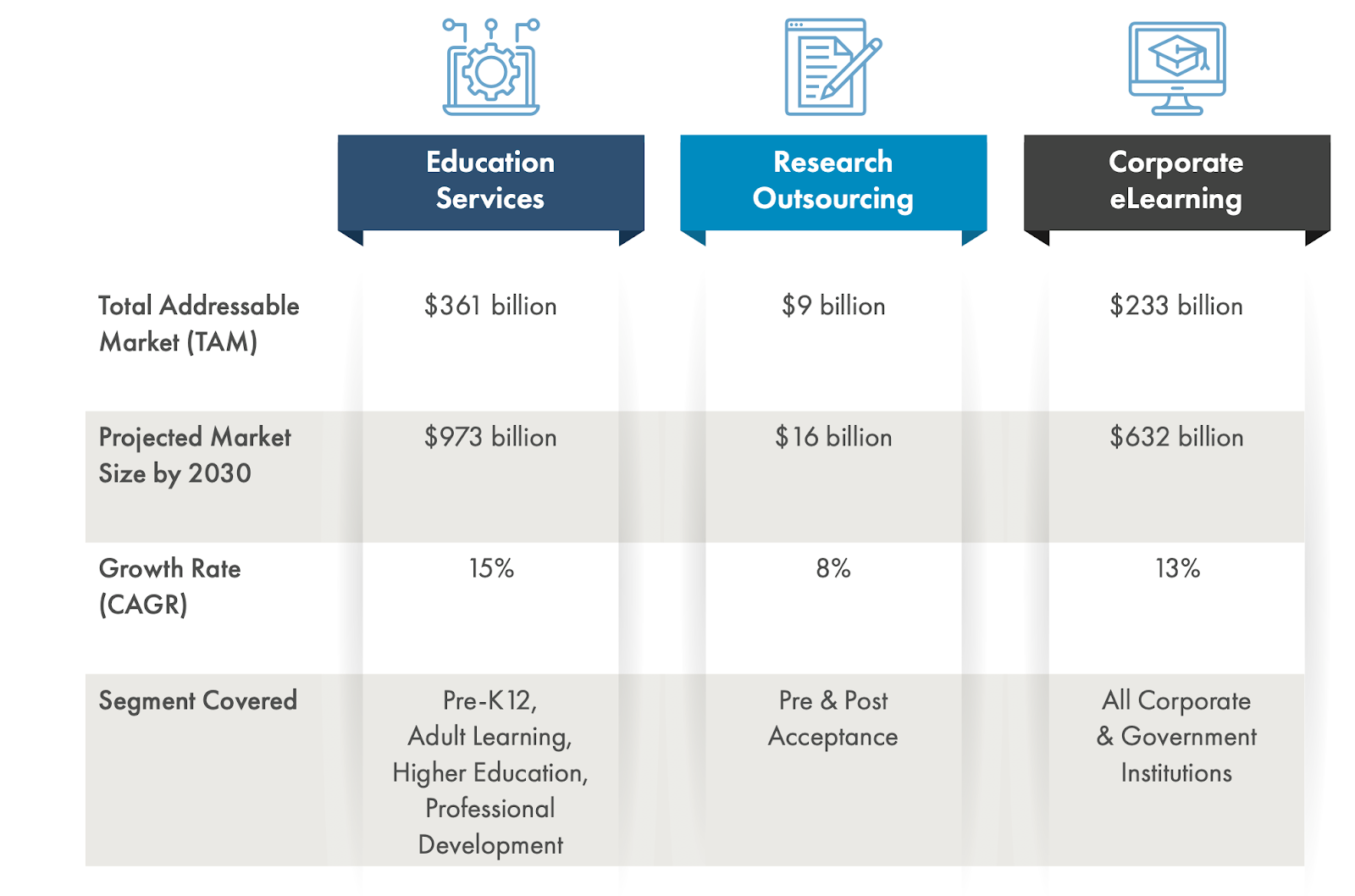

MPS ltd’s business journey from 2012 to 2020 marked a profound transformation. Initially focused solely on content solutions, MPS Ltd successfully diversified its offerings to include Platform and eLearning Solutions, leading to a substantial increase in revenue contribution from these areas. This diversification was achieved through a series of acquisitions over the years. As a result, MPS Ltd’s Total Addressable Market (TAM) expanded dramatically from $2 billion to $365 billion. The strategic shift also led to a healthier revenue distribution, with the proportion of revenue from the top 10 customers decreasing from 78% in FY15 to 52% in FY23.

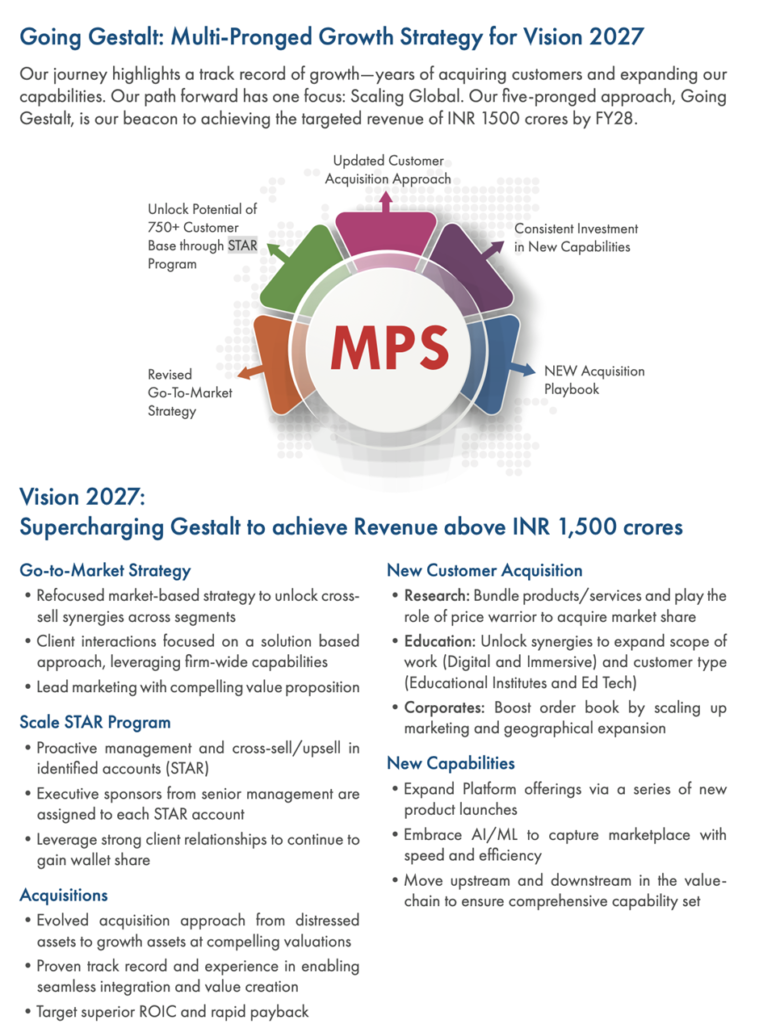

MPS Ltd plans to drive growth through a dual-engine strategy, leveraging both organic and inorganic expansion. MPS Ltd has set a target to achieve a guided scale of 1500 Cr by FY28.

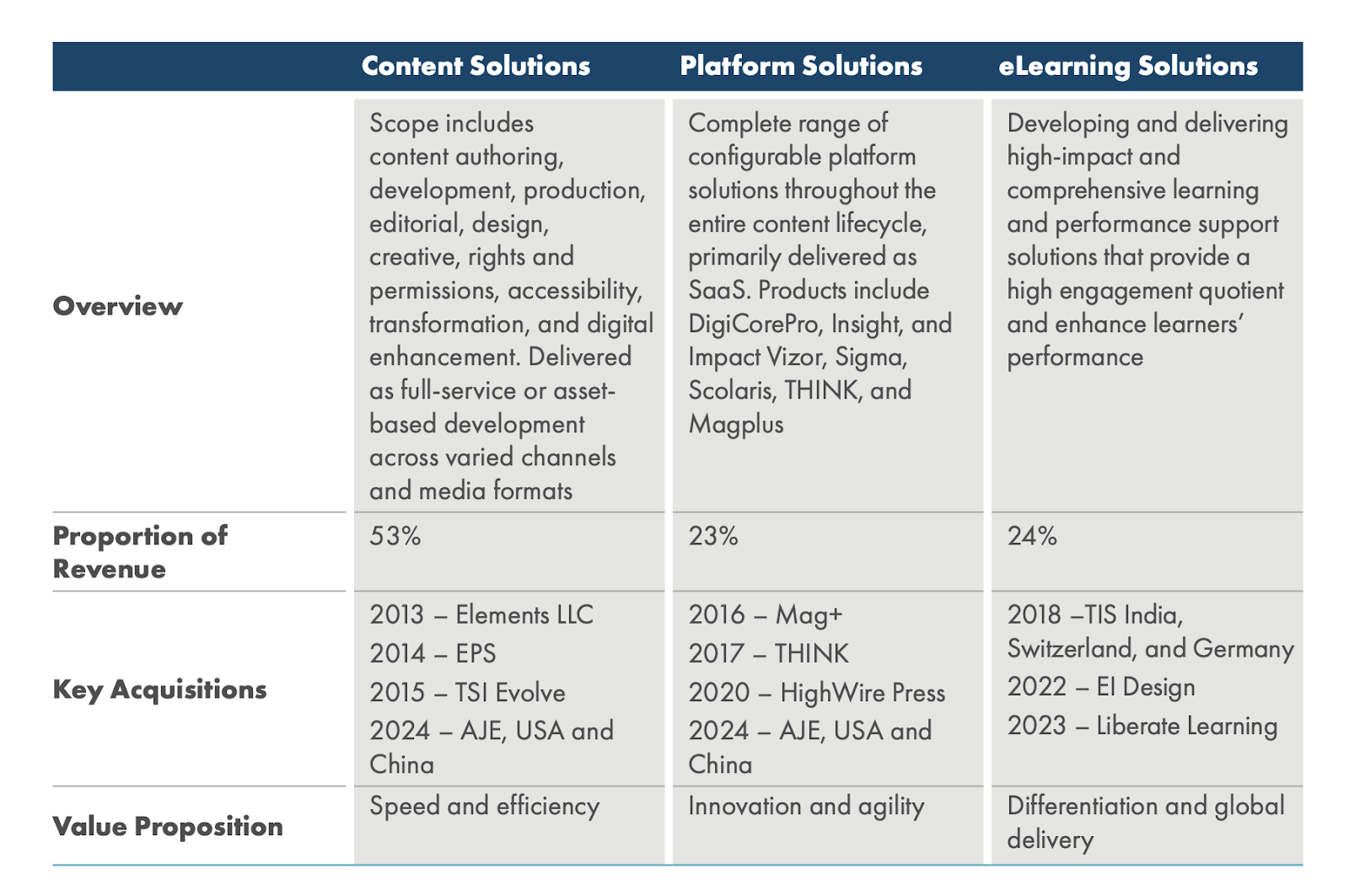

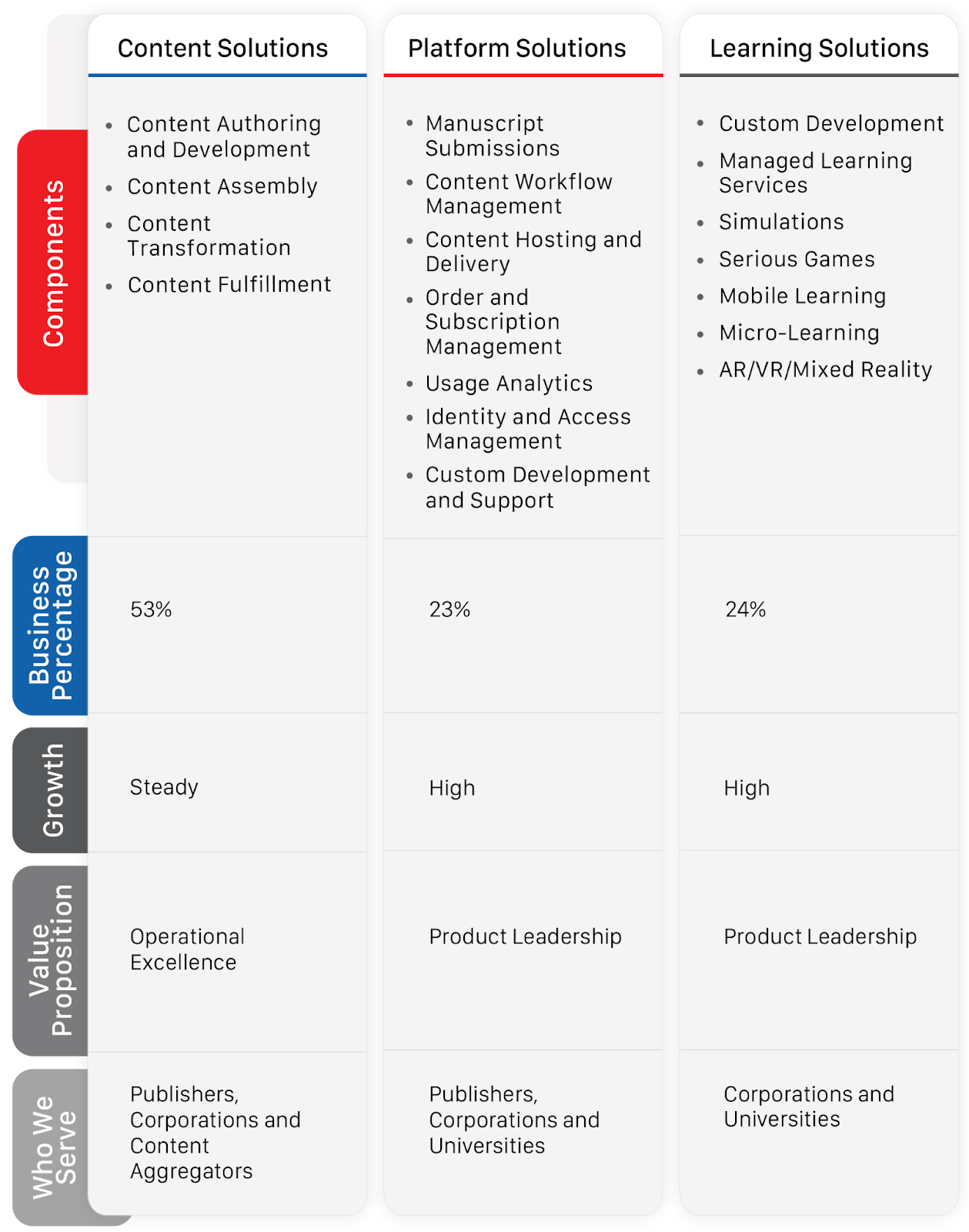

MPS Ltd currently operates across three key segments: Content Solutions, Platform Solutions, and eLearning. Geographically, MPS Ltd derives most of its business from North America and Europe.

MPS Ltd Segmental Mix

MPS Ltd has strategically diversified its revenue mix over the years, reducing dependence on Content Solutions (from 86% in FY17 to 52% in 9MFY25) while significantly scaling Platform and eLearning Solutions.This shift underscores MPS Ltd’s transformation into a balanced, full-stack learning and platform solutions provider.

Content Solutions

MPS Ltd primarily operated as a provider of content solutions, serving publishers on a global scale. Over time, MPS Ltd expanded its capabilities to encompass end-to-end content services. Up until 2015, content solutions remained the sole focus of MPS Ltd’s business operations and continued to contribute substantially to its revenue.

Though the content solution segment’s overall contribution has come down significantly, it still forms a material part of MPS Ltd’s overall revenue, contributing to the tune of 52% of MPS Ltd’s overall revenue for FY24.

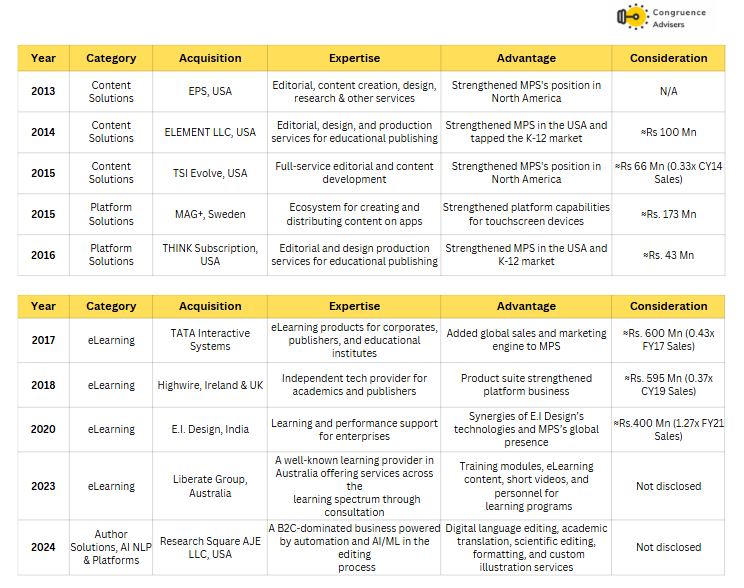

Key Acquisitions in the Content Solutions segment

2013 – Elements LLC

2014 – EPS

2015 – TSI Evolve

2024 – AJE, USA and China

Platform Solutions

MPS Ltd forayed into the platform solutions business in 2015. This segment enjoys the highest operating leverage and has shown acquisition-led growth.

Over the years, MPS Ltd has taken strides to strengthen its platform solutions business by adding new features that can help users navigate through their content creation journey quicker and more efficiently.

The platform solution segment’s overall contribution has moved up significantly. The segment contribution has moved up from 16% in FY20 to 22% of MPS Ltd’s overall revenue and 23% for FY24.

Key Acquisitions in the Platform Solutions segment

2016 – Mag

2017 – THINK

2020 – HighWire Press

2024 – AJE, USA and China

E-Learning Solutions

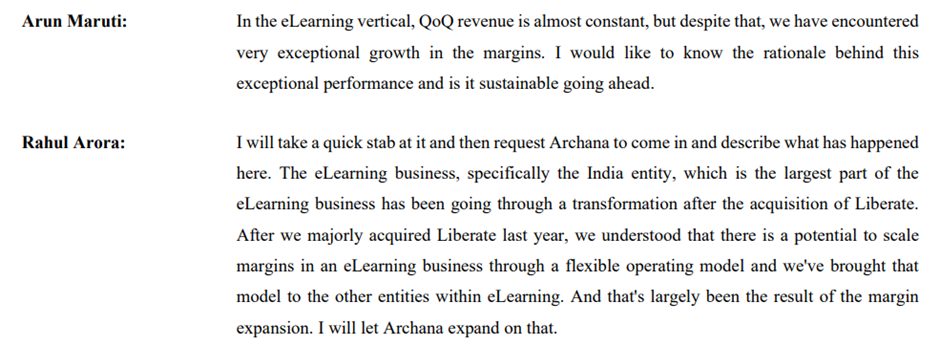

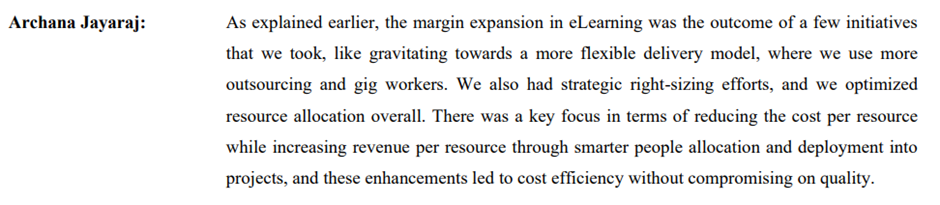

This segment is the latest addition to MPS Ltd’s business. MPS Ltd forayed into the eLearning business in the year 2018, and since then the segment has shown remarkable progress both in terms of growth and profitability. Currently, the eLearning solution segment contributes materially to the tune of 25% of MPS Ltd’s overall revenue for FY24.

Key Acquisitions in the E-learning Solutions segment

2018 – TIS India, Switzerland, and Germany

2022 – El Design 2023 – Liberate Learning

Other Important Metrics

Acquisition History

Recent Acquisitions

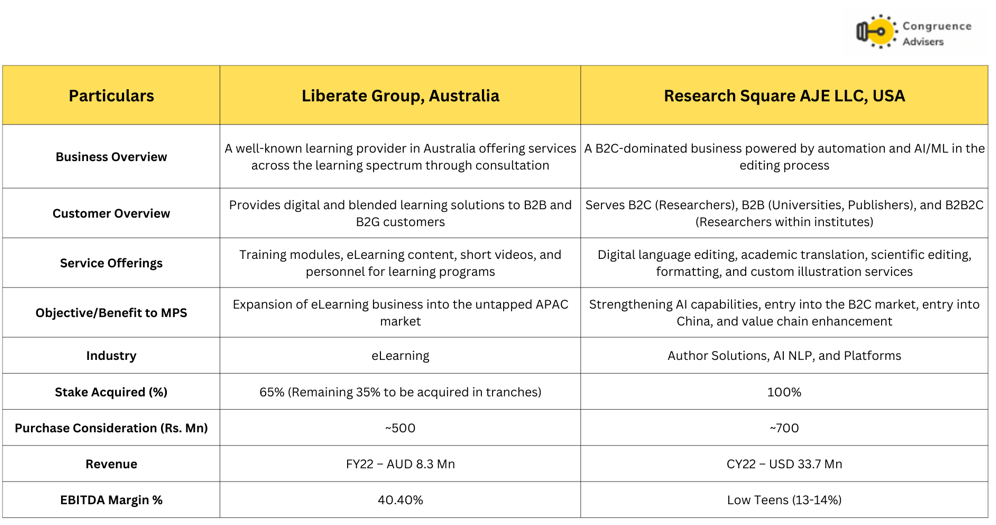

In FY24, MPS Ltd executed a partial acquisition of Liberate Group in August 2023, followed by a full acquisition of Research Square AJE LLC in February 2024.

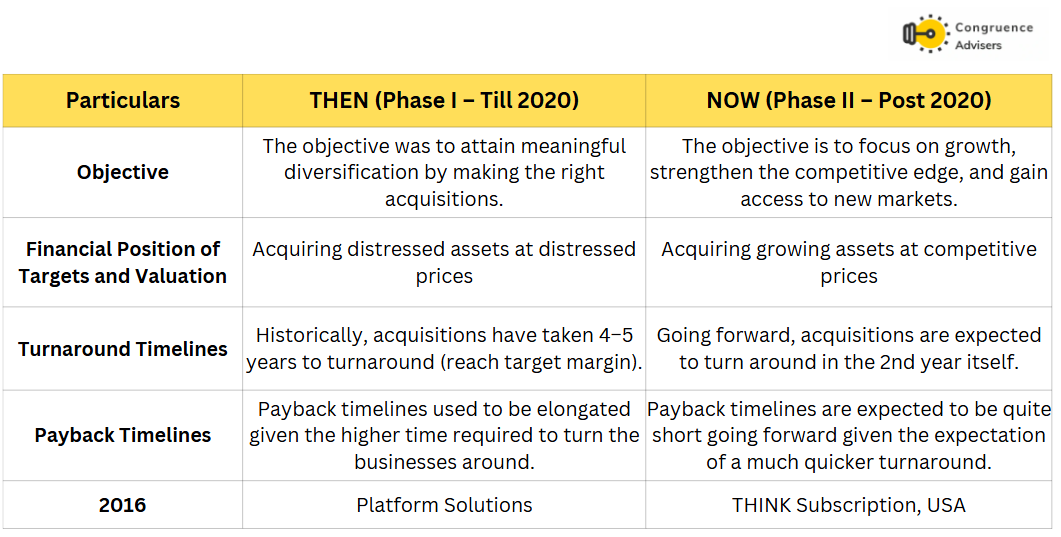

MPS Ltd Acquisition Strategy

Until 2021, it was all about putting in the right blocks to build a diversified business and combating pandemic-related challenges. From 2022 onwards, MPS Ltd shifted its focus back to business growth. To attain this goal, MPS Ltd believes that it will have to make some significant changes in its acquisition strategy and expectations from the target companies.

Below is a comparison indicating the key changes in the MPS Ltd’s acquisition strategy.

Liberate Group – Profitable Company Acquired at Reasonable Valuations:

MPS Ltd acquired a 65% stake in Liberate Group in August 2023 for ~Rs. 50 Cr, valuing the entire entity at ~Rs. 77 Cr. Liberate Group reported revenue of ~Rs. 45 Cr in FY22 with an EBITDA margin exceeding 40%. MPSL paid ~2 times Liberate Group’s FY22 revenue for this acquisition, indicating a reasonable Valuation.

AJE LLC – Distressed Company Acquired at Low Valuations:

In February 2024, MPS Ltd acquired a 100% stake in AJE LLC from Springer Nature for ~Rs. 70 Cr. AJE LLC reported revenue in the range of Rs. 200-250 Cr in CY22 with an EBITDA margin of ~13%, considerably lower than MPS Ltd’s existing overall EBITDA margins.

This acquisition falls into MPS Ltd’s traditional value category, which focuses on acquiring distressed companies at attractive valuations. MPS Ltd plans to improve AJE LLC’s EBITDA margins and bring them closer to its own levels of 28-30%. Unlike in the past, MPS Ltd aims to complete these turnarounds within a couple of years rather than the longer time frames seen historically. This reflects the MPS Ltd’s shift towards a hybrid acquisition strategy where the turnaround is expected to be attained relatively quickly compared to history.

Our Assessment of execution on M&A

9MFY25 results already indicate that the turnaround of AJE financials is well underway. In FY25, the management has not only improved operating margin through cost efficiencies and offshoring but has also figured out the right model to deliver platform services going forward.

The Q2 and Q3FY25 results have demonstrated very good execution on optimizing the acquisitions for better margins, Further quarters should see better revenue growth at good margins (32% operating margin), thereby setting the base for very good earnings growth YoY till H1FY26

Other focus areas of management to improve revenue growth

The STAR Account Strategy

STAR accounts are the customers who provide significant business to MPS Ltd.. These accounts are identified based on their growth potential, scale, and strategic positioning. Initially, MPS Ltd implemented this strategy in its content solutions business, which yielded extremely positive results.

In FY23, MPS Ltd focused on 30 STAR accounts and broadened the number to 60 accounts in FY24. Going forward, MPS Ltd plans to scale the STAR strategy to all the business segments and achieve a significant scale by FY28.

What is a STAR account? A STAR account is a customer who qualifies for two out of the following three conditions:

- Current business is above a certain size

- Potential business can be above a certain size

- The business has some strategic element that improves the total business for MPS Ltd

Forging better relationships

MPS Ltd has identified STAR accounts across all three business segments and has started to deepen ties with customers. MPS Ltd Ltd makes sure that a STAR account has the following :

- Dedicated delivery team

- Dedicated account manager

- Executive sponsor from the senior management team of MPSL who corresponds with the executive sponsor from the client’s senior management team

MPS Ltd, along with its customers, work on figuring out ways to unlock the value of the partnership.

Expected outcome

As a result of the implementation of the STAR strategy, MPS Ltd expects to have 7-8 lines of business with each of its STAR customers, which is 4-5 currently. Additionally, as the strategy is now being implemented across business segments, it is expected to contribute even more as MPS Ltd scales its business going forward.

Long Term Vision

MPS Ltd Capital Allocation

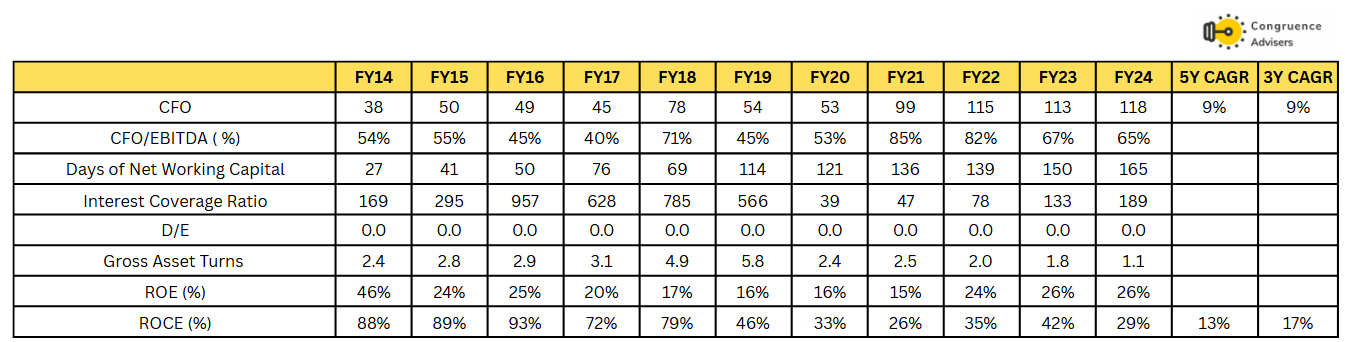

It becomes crucial to evaluate the capital allocation strategy of companies that generate strong cash flows. MPS Ltd generated ~Rs. 800 crores plus worth of cash flow from its operations (CFO) in the last 12 years. Out of this, ~20% of the cash was utilized for business expansion (Organic + Inorganic), and ~60% of the cash was given back to shareholders either in the form of dividends or buybacks.

Going forward, MPS Ltd plans to continue with this capital allocation strategy. Management indicated that the next phase of the acquisition will target a significant expansion of scale, which will enable MPS Ltd to approach its Vision CY27. Additionally, MPS Ltd also highlighted that based on the current management bandwidth, MPS Ltd will optimally only be able to execute 1-2 acquisitions per year.

Given MPS Ltd’s strong cash generation ability, there will be instances where MPS Ltd will be sitting on surplus cash, which it might not require in the coming 6-12 months. In such instances, the management finds it apt to distribute such funds in the form of dividends rather than sitting on excess cash. According to the management, this is a sign of good corporate governance, and they would want to continue doing the same.

Other Important Growth Initiatives

MPS Ltd does not see AI/ML as a threat but as an opportunity to differentiate itself in the fragmented market. To carry out this transformation, the Company launched a new initiative, headquartered in Bengaluru, called MPS Labs. MPS Labs is an R&D center that uses cutting-edge technology around AI/ML/NLP and cloud for a scalable architecture.

Under this initiative, MPS Ltd is investing heavily in incubating new products and innovations that can help MPS Ltd with future-proofing by staying ahead of the competition in a market that is enjoying secular tailwinds.

MPS Ltd Recent Developments to Note

The Board has recently approved the raising of funds through the QIP route to the extent of INR 300 Cr in as many tranches as needed. The last time MPS Ltd did a fundraiser was in 2015; after that, we have only seen buybacks and dividend distribution rather than any equity raising. The Board has also approved changing the salary structure of Rahul Arora to a non-INR payment since he has relocated to Singapore to drive business growth in the APAC region (primarily China & Australia following the Liberate & AJE acquisitions).

Given that MPS Ltd has been on the prowl for larger acquisitions (growth at reasonable price philosophy rather than distressed asset purchasing), the board approval for QIP needs to be seen in this context. The sooner the business can close the next acquisition, the higher the growth rate over FY26 and FY27 since the organic growth rate is likely to be between 12-15% p.a. If MPS Ltd can execute the next 2-3 acquisitions as well as they did with Liberate and AJE, this business can become a high growth, high margin & high cash flow generating business with minimal balance sheet risk.

MPS Ltd Corporate Governance

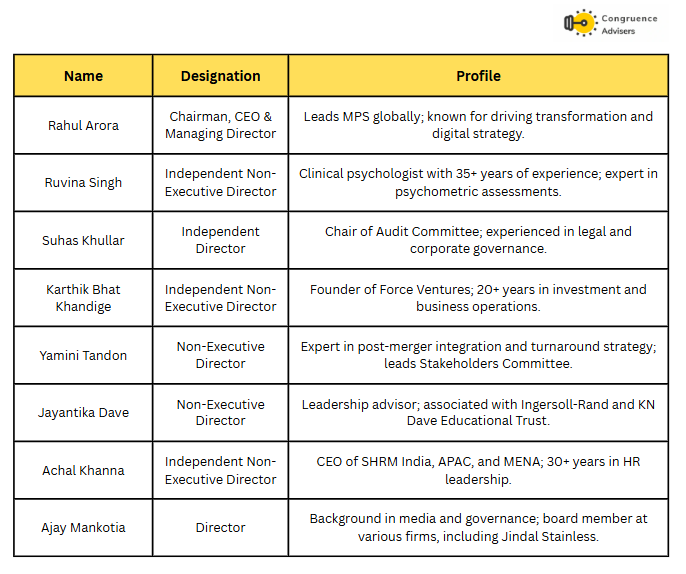

Board Composition – The Board of Directors for MPS Ltd comprises 7 directors, of whom 4 are Independent and 6 are non-independent. Mr. Rahual Arora is the Chairman, CEO & Managing Director. The non-executive/independent Directors on the board bring diverse and relevant experience to the company across the domains of consumer tech startups, private equity, HR, Publishing, and consulting.

Promoter Remuneration – The total remuneration to KMP for FY24 amounted to INR 5.35 Cr. Total KMP remuneration as % of PAT amounted to ~5% in FY24.

Related Party Transactions – MPS Ltd had no significant related party transactions in FY24. Some transactions have been done for subsidiaries, which have no impact.

Contingent Liabilities – According to the annual report for FY24, the total amount of contingent liabilities amounts to ~INR 3.4 Cr, only related to income and service tax.

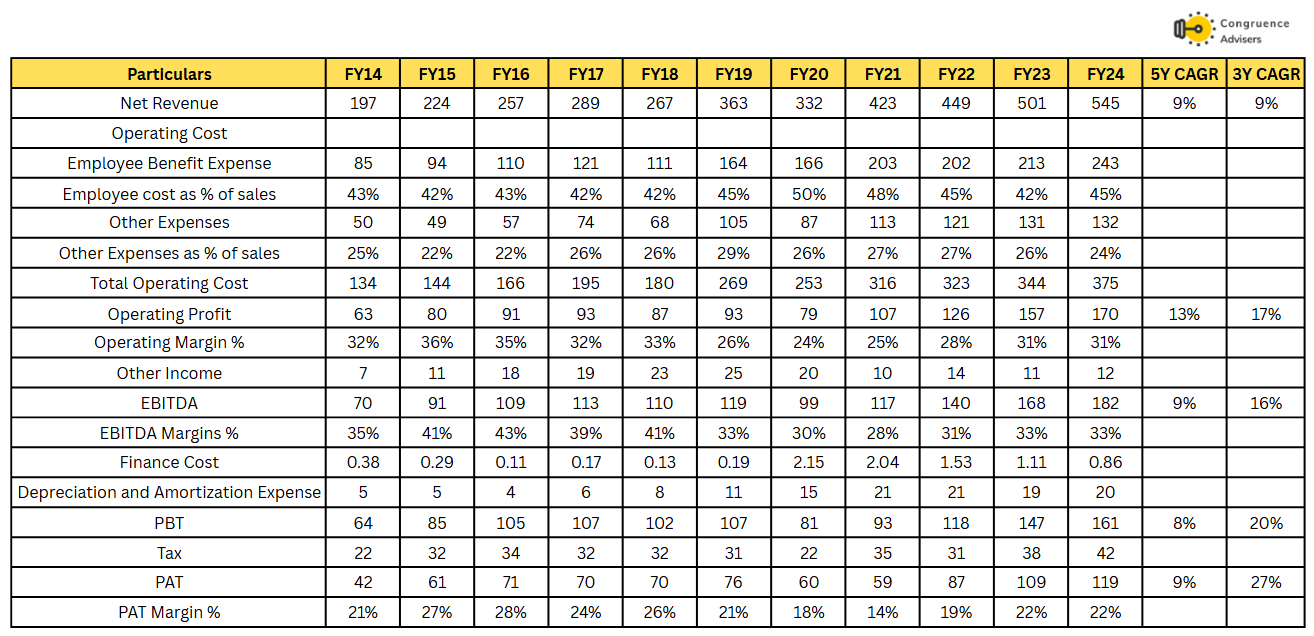

MPS Ltd Financial Performance

Over the last 5 years, MPS Ltd. has grown revenues at a CAGR of 9%, EBITDA at a CAGR of 9%, and PAT at a CAGR of 9%, demonstrating a steady growth trajectory. During this period, EBITDA and PAT margins have remained steady, staying between 28%-36% and 14-22%, respectively. Over the 3 years, MPS Ltd has grown revenues at a CAGR of 9%, EBITDA at a CAGR of 16%, and PAT at a CAGR of 27%.

MPS Ltd Return Ratios, Working capital, Debt, and cash flow analysis

MPS Ltd generated good cash flow over the years, good margins, and an excellent balance sheet quality with no debt are good qualities of a good business. It becomes crucial to evaluate the capital allocation strategy of companies that generate strong cash flows. MPS Ltd generated Rs. 800 Cr plus worth of CFO in the last 12 years. Out of this, ~20% of the cash was utilized for business expansion (Organic + Inorganic), and ~60% of the cash was given back to shareholders either in the form of dividends or buybacks.

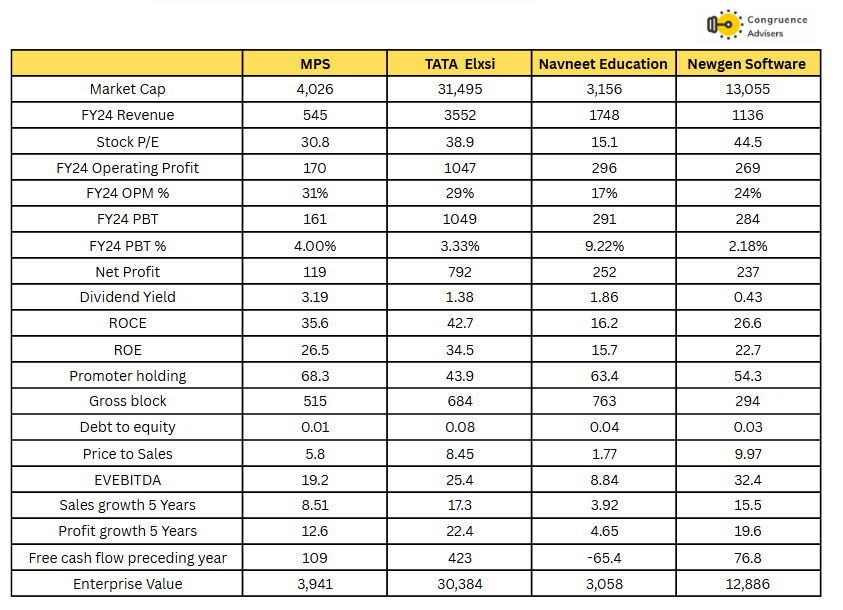

MPS Ltd Comparative Analysis

To understand MPS Ltd’s investment potential, we have conducted a comprehensive analysis. This analysis includes comparing MPS Ltd to its competitors (peer comparison) on various fundamental parameters and MPS Ltd’s share performance relative to the relevant benchmark and sector indices.

MPS Ltd Peer Comparison

There are no like-for-like peer companies of MPS Ltd listed in India. Hence, we chose a couple of mid & low-tier IT companies as peers to benchmark MPS Ltd against business performance metrics.

MPS Ltd Index Comparison

MPS Ltd share performance vs S&P BSE Small cap Index as the index benchmark comparison is a fundamental tool for understanding the investment potential and making informed decisions in the context of the broader market

Why You Should Consider Investing in MPS Ltd

MPS Ltd offers some compelling reasons to track closely and to consider investing if one is looking to invest in the education publishing Industry.

Inorganic Growth Strategy – MPS Ltd has a proven track record of inorganic growth in the consolidation-driven publishing services industry. They are among the larger players in this industry with excellent domain knowledge of how to use technology to optimize costs and reduce time to market for the largest publishing players across the world. It is very likely that they will continue to acquire the right businesses at the right price, thereby keeping the growth trajectory high for the next 3-5 years.

Efficient Integration & Cost Optimization – MPS Ltd can now integrate acquired businesses faster (12-18 months vs. 3-5 years), using low-cost centers in Dehradun & Noida to offshore operations and improve margins even if acquisitions initially have lower profitability.

Organic Growth Outlook from FY26 – Starting FY26, MPS Ltd expects organic revenue growth of 12–15% per annum, shifting focus from margin optimization and new client acquisition (in FY25) to deeper growth in existing businesses. Leadership changes support this direction.

Strong Cash Flow & Balance Sheet Flexibility – MPS Ltd generates strong free cash flow (~₹15 Cr/month), with the ability to raise funds via QIP or bank loans without pressuring the balance sheet, thanks to its simple and clean financial structure.

Valuation Upside with Execution – If MPS Ltd executes acquisitions in FY26 and shows a clear path to hitting its FY28 revenue target of ₹1500 Cr, the market could reward it with higher valuation multiples than its historical average.

Premium Potential vs. Peers – MPS Ltd, with its high growth, margins, and ROCE, could command premium valuations compared to IT services firms, especially as smaller players like All E Technologies are already trading at higher multiples than industry giants.

Earnings Growth Visibility – MPS Ltd has clear visibility of year-on-year earnings growth up to Q2 FY26 due to a low base, offering steady performance even in a market where predictable growth is rare across traditional defensive sectors.

What are the Risks of Investing in MPS Ltd

Investors need to keep the following risks in mind if they choose to invest into this business. Risks need to be weighed in combination with the advantages listed above to arrive at a decision that is optimal for your portfolio construct.

M&A Risk & Industry Dynamics – The failure rate of M&A is high if one sees the base rate across market cycles. The biggest risk is that MPS Ltd becomes too ambitious and tries to acquire a much larger business than they have experience with. This possibility is hedged to some extent since the publishing services industry is seeing a good range of consolidation, where good business capabilities can be acquired at reasonable prices. Hopefully, the management will continue to be judicious in M&A.

QIP & Acquisition Delays – Completion of QIP was followed by challenges in the acquisition completion. Sometimes, acquisitions can run into unforeseen challenges due to cross-border legal aspects & employee-related issues. Since the business is cash-generating, further cash on the balance sheet due to QIP can turn out to be ROCE dilutive for a few quarters.

Valuation Concerns – Elevated valuation multiple compared to the historical average. Our assessment is that the business today is trading at ~25x forward 12M earnings; this is the highest multiple the business has ever traded at since the high of 2015.

Stock Liquidity & Investor Exit Risk – A closely held counter where 1-2 large investors are exiting (for their own reasons) can induce significant volatility in the stock price. The average daily volume of the stock over the past 45 days is in the range of 25-30k shares per trading session.

MPS Ltd Future Outlook

We expect Q4 FY25 earnings to show strong momentum on the lines of Q3FY25 since the cost optimization initiatives are already showing up in the P&L. Q3 and Q4 are traditionally the best quarters for the business, and there is a high probability of the business meeting the management guidance of 750 Cr revenue at 25%+ Earnings growth YoY for FY25.

We expect the management to focus on these for FY26.

- Sustain operating margin at ~32% for the organic part of the business (as current)

- Focus on driving 15% growth in the organic business over FY26 and FY27.

- Close at least one acquisition that can add > 150 Cr of annual revenue each in FY26 and FY27

- All acquisitions will come at healthy unit economics (even if operating margins will need to be optimized over 12+ months) or with a clear path to good unit economics within 1 year.

MPS Ltd trades at ~25x FY26 organic earnings. While this appears a tad expensive, we suspect that the market is already pricing in a new acquisition that can move the needle on revenue and earnings in FY26 itself. The Board approval for QIP and the relative strength of the stock price all point towards this possibility.

MPS Ltd Technical Analysis

We consider technical analysis to be a useful input in taking medium-term investment decisions. Many a time, price action tends to lead to fundamental developments; this is too important an aspect to be ignored by retail investors who do not have access to management outside of common forums like investor calls & AGM.

At Congruence Advisers, we like to consider both the long-term weekly chart and the daily chart to arrive at a view on price action. Combined with our understanding of fundamentals, we usually end up being better placed to be able to judge both the business cycle and the stock cycle. Playing the stock cycle right is extremely important for investors looking to extract significant alpha over the medium term.

MPS Ltd Price charts

Starting with the weekly chart, the trend line is very easily noticeable. MPS Ltd overall structure tells us that the business can go quite some distance to go if the numbers support it over the next few quarters. The stock price bounced off the long term trend line, even in the face of a collective market shock that materialized post the Tariff announcements.

On the Daily Chart, the recent price behaviour was interesting. For further strength, the price will need to hold above the upper trend line. There is a good chance that the support on both the day & weekly charts have been established in the market correction of April 5 – 11

MPS Ltd Latest Result, News and Updates

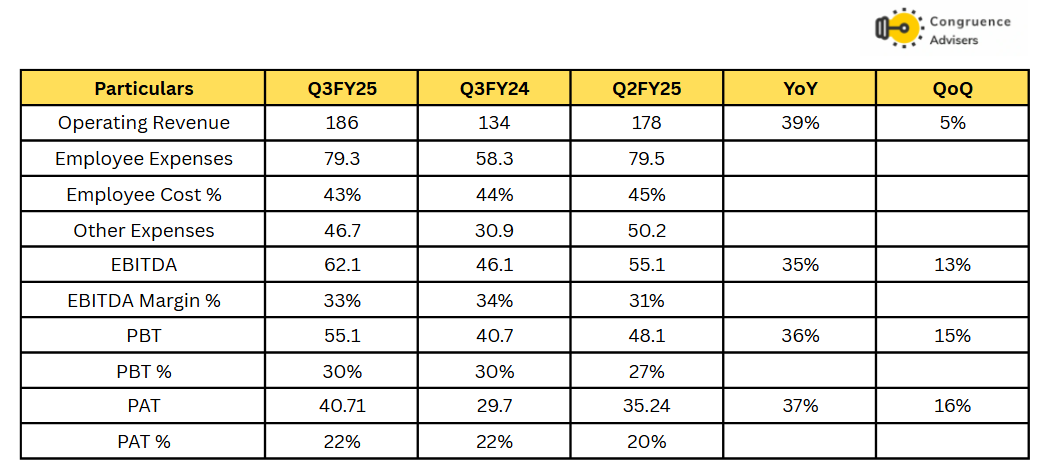

MPS Ltd Quarterly Results

MPS Ltd Q3 FY25 revenues reached INR 186 Cr, representing a 39% YoY and 5% QOQ. EBITDA margins improved to 33% in Q3 FY25, with overall EBITDA growing by 36% compared to the same period last year.

The Content Solutions segment drove topline growth, aided by the acquisition of AJE and strong momentum in the education vertical. A notable development was the signing of a 3-year minimum volume agreement with a long-standing client, which management sees as a potential model for future long-term partnerships.

While FY25 saw a record number of deals evaluated, no acquisitions were finalized as the company maintained strict valuation discipline. MPS Ltd remains focused on acquiring education-sector companies with revenues of USD 15–30 million and EBITDA margins of ~15%. Technological innovation continues to be a core strength, with MPS Labs implementing AI/ML across various processes such as content structuring, editing, and chatbot automation. This tech-first approach has enabled the company to scale revenues 6–7x since its acquisition by

MPS Ltd, in partnership with HighWire, also launched an end-to-end publishing workflow platform. Meanwhile, the eLearning segment has turned profitable ahead of schedule, driven by resource optimization and a more flexible delivery model. The near-term focus is on consolidating profitability, with FY26 targeted for scaling the business. Internationally, MPS Ltd is prioritizing the high-potential APAC region, especially China and Australia, with CEO Rahul Arora relocating to Singapore to lead regional initiatives.

Disclaimer – This note is part of a business research & analysis series on small companies, there is no BUY/SELL recommendation or target price issued as part of this to a general audience. There is no assurance that this stock makes for a good investment, there is no guarantee that this stock will continue/be included in the coverage universe of Congruence Advisers. The note contains some forward-looking statements and insights drawn from the historical results, annual reports and investor presentations; they are to be viewed only within this context and not as a prediction of future performance of the business or the stock covered.

While due care has been taken to ensure that the information here is as accurate as possible, Congruence Advisers disclaims any liability in case of any unintentional inaccuracies.

The content does not constitute investment advice.

Disclosure – The stock is currently (April 2025) part of one of our research offerings, our view may be biased for this reason. Please do an independent evaluation of the business and do not depend only on this note for initiating/closing out positions.