Faze Three Ltd is a manufacturer and exporter of home furnishing textile products, mainly floor coverings, bathmats, rugs, towels, blankets, throws, and cushions. They have diversified their product mix and have included chair pads, floor covering, curtains, and kitchen textiles in the past few years.

Faze Three Ltd offers the prospect of a business that is set to complete an aggressive capacity expansion in FY27 at a time when the operating margin has fallen significantly over FY25 and FY26. In the face of the current macroeconomic cloud of tariffs, unclear policy and geopolitical shocks, a mean reversion to good operating performance can surprise investors, if it happens. But can we build conviction early enough to take a meaningful position in a business like Faze Three Ltd where quarterly investor updates aren’t easy to come by? What will it take for this stock to see a significant re-rating from here given that the textile sector has been going through a challenging period of price performance? We will try to explore these perspectives in this note.

Faze Three Ltd – Company Summary

Faze Three Ltd, founded by Mr Ajay Anand in 1985, is primarily engaged in manufacturing and exporting end home textile products like bathmats, rugs, blankets, throws, cushions, etc.

Faze Three Ltd has diversified its product mix across categories in the Home Textile segment and is also a direct exporter to top retail store chains in the USA, UK, and Europe (Over 90% Revenue is Exports).

8 Factory Locations – Factory Locations Silvassa (2) (UT of DN&DD) and Vapi (1) (Guj.) for Home & Technical Textiles. Panipat (4) (Haryana) for Handloom Home Textiles. (1) In Aurangabad, Maharashtra.

During the year, Faze Three Ltd added an office cum Showroom location in New York, USA, to accelerate reach and efforts towards growing the business and new product categories.

Technical & Home Textiles Products: Floor coverings (Bathmats / Rugs – Rubber backed), Performance & Outdoor Home Textiles made of micro polyester, Cushions, Top of the Bed Products, Blankets, Curtains, Accessories, etc.

Handloom Home Textiles Products like Bathmats, Accent Rugs, Throws, Cushions, Powerloom rugs, Accessories, etc.

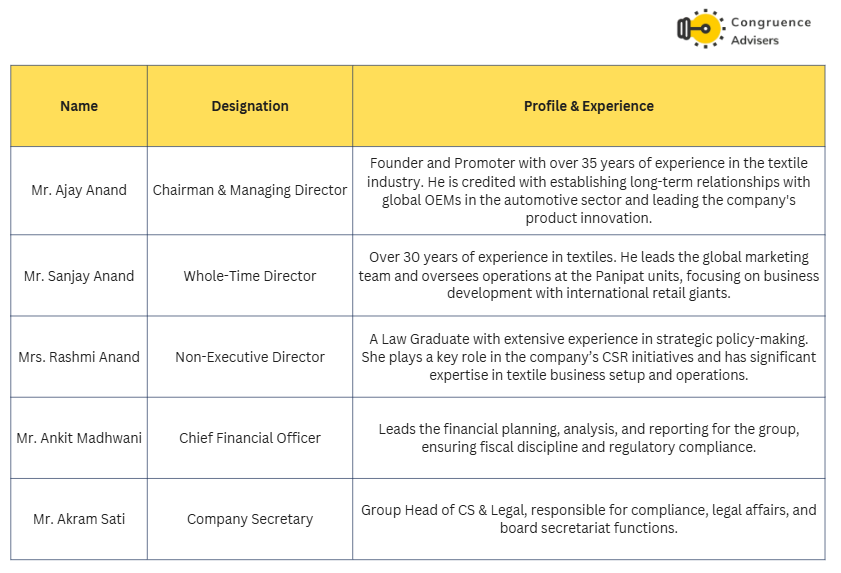

Faze Three Ltd Management Details

In 1985, Ajay Anand, a graduate and first-generation entrepreneur, founded Faze Three Ltd amid India’s vibrant textile landscape, fueled by an unyielding passion for home and technical textiles. Over three decades, he honed expertise in international marketing of home interiors, furnishing fabrics, and automotive textiles, transforming Faze Three Ltd into a trusted supplier for major US and UK retailers.

As Chairman & Managing Director, Ajay drove day-to-day management, administration, and bold strategic decisions, championing product innovation and craftsmanship that elevated Faze Three Ltd to global prominence. He also leads Faze Three Autofab Ltd, extending his vision into automotive fabrics.

Faze Three Ltd – Industry Overview

Indian Textile Industry

The textiles and apparel industry contributes approximately 2% of India’s GDP and about 11% of manufacturing GVA (Gross Value Added) as of August 2025. The textile industry in India is predicted to double its contribution to the GDP to approximately 5% by the end of this decade.

The domestic market is valued at US$ 225 billion in 2025 and is growing at a brisk pace of 10–12% CAGR. Rising incomes, e-commerce penetration, and evolving consumer preferences are expected to push the market size to US$ 350 billion by 2030. On the export front, India’s textile shipments currently stand at US$ 35.14 billion, with the target of reaching US$ 100 billion by 2030.

The India Textile Manufacturing market size reached USD 133.6 billion in 2025, and is projected to grow at a CAGR of 3.99% during 2026–2034, reaching USD 192.0 billion by 2034. This growth is driven by government incentives such as the PLI scheme, rising exports, increased domestic demand, technological advancement, synthetic fibre adoption, and sustainability-focused manufacturing.

Home Textile Segment – Where Faze Three Ltd Earns Most of Its Revenue

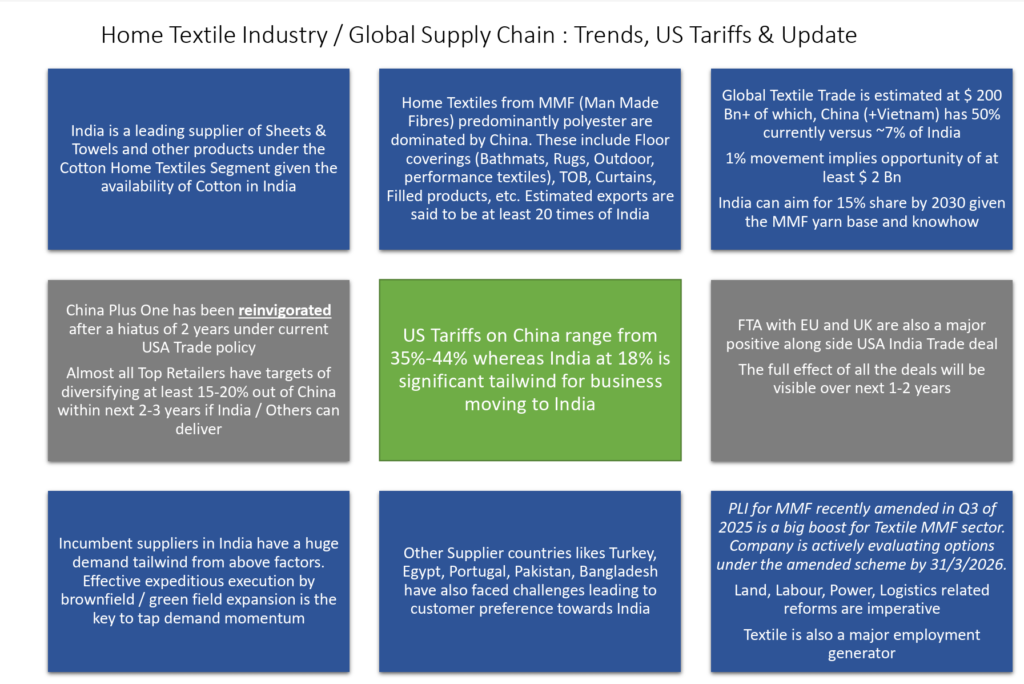

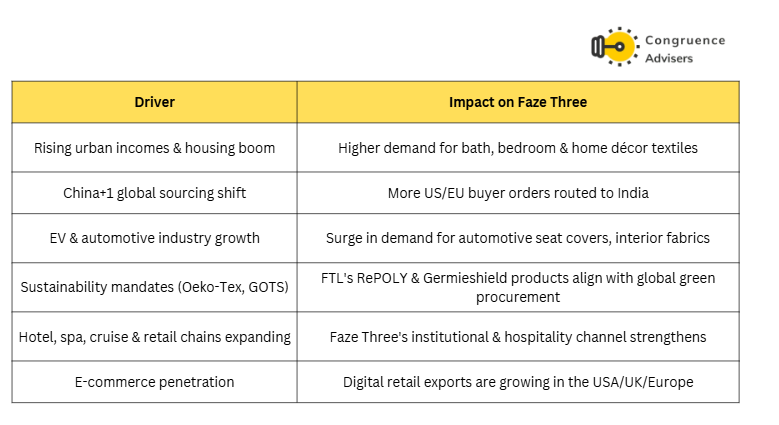

The Indian home textile market size reached USD 10.38 billion in 2025 and is projected to advance to USD 15.47 billion by 2030, reflecting an 8.32% CAGR over the forecast period. Growth is supported by the Production Linked Incentive scheme, steady gains in disposable income, and rapid urban migration that concentrates purchasing power in large cities. Digital commerce adoption widens market access for smaller manufacturers, while export momentum created by the “China+1” sourcing shift improves capacity utilisation at large integrated mills.

The global home textile market stood at USD 143.09 billion in 2025 and will reach USD 209.53 billion by 2032, growing at a CAGR of 5.6%. India and China together contribute more than 70% of the world’s production. While Asia-Pacific dominates production, North America and Europe remain the primary consumption markets — the very geographies where Faze Three exports its products.

Key product categories within the home textile space where Faze Three is active include bathmats (cotton, rubber-backed and tufted), rugs, blankets, cushions, curtains, throws, baby blankets, outdoor furniture covers, awning fabrics, canopies, lounge cushions, durries, bedspreads, and throws.

Panipat, where Faze Three operates one of its key manufacturing units, is a recognised national hub for home textiles and recycled products, with a capacity of 2,000 tonnes/day of recycled material and strong global export credentials.

The Indian Technical Textiles market is the fifth largest in the world. The technical textiles industry was valued at US$ 29 billion in 2024 and is projected to grow to US$ 45 billion by 2026, US$ 123 billion by 2035, and US$ 309 billion by 2047. The Indian mobiltech textile market (a division of technical textiles for automotive use) is projected to grow from US$ 2.32 billion in FY25 to US$ 4.57 billion by FY33, at a CAGR of 8.84%.

India is rapidly emerging as a strong contender in the global technical textile market, supported by government policies like the National Technical Textiles Mission (NTTM). India’s expanding infrastructure, booming automotive sector, and rising awareness about protective clothing and sustainable textiles are key demand drivers. With rising exports and investment in research centres, India is positioned to become a global hub for affordable and innovative technical textile solutions.

Industry Growth Drivers

Non-essential consumption reached 54.7% of urban household spending in July 2025, confirming a structural shift toward discretionary categories such as branded bedding, coordinated furnishing sets, and designer curtains. Demand gains extend into Tier-2 metros in Gujarat, Tamil Nadu, and Karnataka, where wage growth outpaces national averages.

Sustainability is emerging as a key driver of growth for the industry, as more and more companies adopt green practices. India is among the world’s largest producers of organic cotton, with over 300 Global Organic Textile Standard (GOTS)-certified textile units. Recycled fibres, water-saving dyeing, and solar-powered textile mills are finding favour as the market for eco-fashion grows.

The major demand drivers for Faze Three Ltd’s specific segments are:

Government Policy Support

The Union Budget 2025–26 allocated ₹52.7 billion for the Ministry of Textiles, representing a 19% increase over the previous year. The PLI scheme reopened in 2025 with applications accepted until September 30, 2025, offering incentives for achieving threshold investment and turnover. The technical textiles market is expanding rapidly, with the government’s target of ₹870 billion in exports by 2025–26.

Government schemes like the PM Mega Integrated Textile Region and Apparel (PM MITRA) program, which aims to set up over seven integrated textile parks across the nation, are enhancing the Indian textile outlook. With ₹4,445 Cr sanctioned under the scheme, the government plans to create an integrated value chain in textiles, enhancing competitiveness and lowering logistics costs. The Production Linked Incentive (PLI) Scheme, with an outlay of ₹10,683 Cr, is encouraging large-volume production of man-made fibres and technical textiles.

In 2026, the Indian textile and apparel industry is entering a “defining decade,” evolving from a cost-focused producer into a high-value, strategic cornerstone of global supply chains. Seven PM MITRA Parks are now operational catalysts for integrated manufacturing, aiming to attract ₹70,000 crore in total investment. The PLI scheme has been expanded with lower investment thresholds, specifically targeting man-made fibres (MMF) and technical textiles.

Key Challenges & Risks – Cotton price swings, compliance costs linked to new BIS norms, and supply base fragmentation temper margin expansion for firms that rely on volatile raw material markets. Spot cotton prices swung more than 20% during 2024 due to weather events and policy-linked export caps that created supply tightness.

In 2025, the United States (India’s largest export market) imposed reciprocal and punitive tariffs, bringing total duties on some Indian textiles to a staggering 50%, making Indian goods 30–35% more expensive than those from competitors like Bangladesh or Vietnam, leading to a potential 70% contraction in US-bound orders for certain segments. This directly affects Faze Three, whose exports are concentrated in the USA. In February 2026, India and US announced a broad framework for a bilateral trade deal to be concluded and inked in the coming months. Following this announcement, the US Supreme Court passed a landmark judgement declaring the 2025 US tariffs imposed by the new regime illegal. While there is a lot of uncertainty on the tariff front even today, the situation is far better than what was seen through H2 CY25 when the US hiked tariffs on India to ~50%.

PLI scheme

The recent amendments to India’s PLI scheme for MMF (Man-Made Fibre) apparel, fabrics, and technical textiles, notified in Q3 2025 (around July-October), lower barriers for participation and expand opportunities in the sector. These changes provide a significant boost by making incentives more accessible amid global demand for synthetics.

Key Amendments

- Expanded product coverage with 8 new HSN codes for MMF apparel and 9 for MMF fabrics.

- Reduced minimum investment thresholds effective August 1, 2025: ₹300 Cr to ₹150 Cr (Part 1) and ₹100 Cr to ₹50 Cr (Part 2).

- Relaxed incremental sales criteria from 25% to 10% starting FY 2025-26, allowing easier incentive claims.

- Flexibility to set up units within existing companies, no new entity required.

Application Timeline

The portal reopened in August 2025 post-amendments, initially until December 31, 2025, but was extended to March 31, 2026, due to strong industry response.

Faze Three Ltd Business Overview

Business Model

Faze Three Ltd has a diversified product basket that includes cotton and rubber-backed bathmats, blankets, durries, throws, hand-tufted carpets and rugs made of cotton and wool, cushion covers, curtains, as well as poly-cotton and cotton masks, table covers, patio mats, and seat covers.

Own Brands

Geographic Distribution & Clients

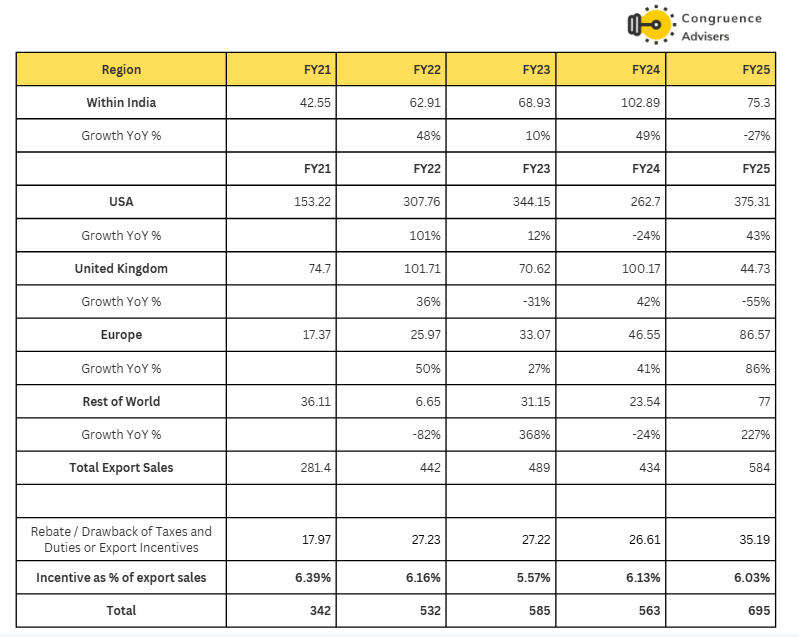

The majority (~90%) of Revenue is derived from direct exports to organised retail in the USA, UK, and the European region.

Export incentive

RoDTEP incentive cut by 50% on Feb 24th

Implementation and Coverage

- Introduction: The RoDTEP scheme was introduced effective January 01, 2021, replacing the MEIS (Merchandise Exports from India Scheme).

- Product Scope: At the time of introduction, Faze Three Ltd management stated that the majority of the products were expected to be covered under the RoDTEP scheme.

- Differentiation: This is distinct from the RoSCTL (Rebate of State and Central Taxes and Levies) scheme, which covers “Apparel/Garments and Made-ups.” Faze Three Ltd noted that only approximately 11% of its total income (as of mid-2021) came from products covered under RoSCTL, implying the bulk of the remaining portfolio would fall under RoDTEP.

Financial Impact and Rates

- Incentive Rates: Faze Three Ltd estimated the RoDTEP rates for its products to range between 2% to 4%.

- Arrears Recognition: Due to delays in the notification of rates by the government, FTL did not initially accrue this income in early 2021. It later recognised ₹1.55 Crores in the quarter ended September 2021, which specifically pertained to exports made between January 2021 and March 2021.

- Projected Income: Based on the estimated rates, Faze Three Ltd projected an additional annual income of approximately ₹4 Crores to ₹7 Crores from this scheme for FY22.

New Incentive cut Impact will be 2.5-3% to the revenue

Customers

Faze Three Ltd primarily caters to Global Big-Box Retailers and large retail chains. Faze Three Ltd does not sell directly to consumers (B2C) but operates on a B2B model where it designs and manufactures products for these brands to sell.

- Strong relationship with Top 15 customers over the last 2 decades. Consistent business across product lines

- In FY25, the Top 12 customers contribute around 80% of Revenue.

- Any single Customer revenue < 16% of the revenue of Faze Three Ltd’s revenue.

- Most customers procure multiple products across Faze Three Ltd’s factories.

Key Clients by Region:

USA – Key customers include Walmart, Target, Costco, Macy’s, Williams Sonoma, Pottery Barn, TJ Maxx, Marshalls, Ross, Burlington, Dollar General, Lands’ End, Frontgate, and Restoration Hardware.

UK & Europe – Major clients include Sainsbury’s, ASDA, Marks & Spencer (M&S), LIDL, Dunelm, Next, Zara Home, and Action.

Other Markets – They also supply retailers like Myer (Australia) and KAS.

- Co-Creation and R&D – Faze Three Ltd leverages customer feedback and market insights to design collections tailored to international trends. It has a design studio in New York to facilitate this close collaboration.

- Dedicated Service: Faze Three Ltd assigns a Dedicated Key Account Manager for each customer at each location to ensure “360-degree communication” and rapid feedback resolution

Faze Three Ltd’s customers are actively shifting sourcing away from China due to tariffs and supply chain diversification. Management notes a “tangible move” of volume to India from Chinese suppliers, particularly for floor coverings, where China historically held a massive market share advantage.

In FY23 and FY24, major US retailers (Faze Three Ltd’s primary clients) faced high inventory levels, leading to a temporary slowdown in orders and destocking. However, Faze Three Ltd managed to navigate this better than many peers due to its diversified product mix.

Inhouse Capability

1. Vertical Integration

- Faze Three Ltd operates on a vertically integrated model described as “Design to Delivery” or “Yarn to Finished Product”.

- Unlike players who outsource key steps, Faze Three Ltd controls the entire production lifecycle. This includes captive process houses for dyeing and processing, ensuring they are not dependent on external vendors for critical finishing stages.

- Raw Material Sourcing: Faze Three Ltd procures approximately 95% of its raw materials (Cotton and Man-Made Fibers) domestically, reducing reliance on volatile international supply chains.

- Dual Expertise: Faze Three Ltd claims equal capabilities and expertise in both Cotton and Polyester/Man-Made Fiber (MMF) products, positioning it to capture the growing global shift toward polyester-based technical textiles.

2. Design and R&D Capabilities

- A core pillar of Faze Three Ltd’s strategy is its transition from a contract manufacturer to a “solutions provider” through strong design capabilities.

- In-House Design Teams: Faze Three Ltd maintains dedicated in-house design, R&D, and development teams at each factory location.

- Global Presence: To stay aligned with Western trends, Faze Three Ltd has established a design office and showroom in New York, USA. This allows them to co-create collections with retailers like Walmart and Target rather than just accepting standard orders.

- Innovation: The R&D team works on product innovations such as “High-Performance Outdoor/Indoor rugs” and specialised micro-polyester textiles. Faze Three Ltd views innovation as a continuous process essential for staying ahead of the curve.

3. Technological and Operational Standards

- The factories are built and operated according to globally mandated infrastructure standards to meet the stringent compliance requirements of US and UK retailers (e.g., Walmart, Sainsbury’s).

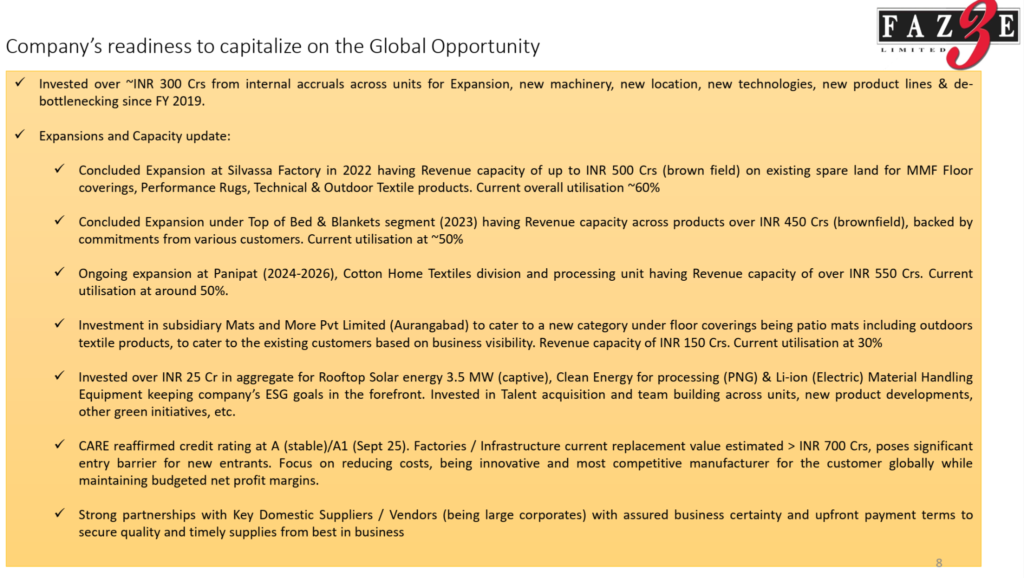

- Between 2017 and 2025, Faze Three Ltd invested more than ₹60 Crores from internal accruals into new machinery, technology absorption, and de-bottlenecking to improve throughput and cost leadership.

- Faze Three Ltd has implemented Zero Liquid Discharge (ZLD) systems at multiple sites to treat and reuse wastewater. They have also invested in solar power plants (1.70 MW and 1 MW) at Silvassa and Panipat, covering ~30% of their power requirements.

4. Execution Speed

Faze Three Ltd’s integrated model allows for faster turnaround times compared to fragmented competitors.

- Turnaround Time: Faze Three Ltd reports an order turnaround cycle of 60 to 120 days, which is critical for meeting the “fast fashion” cycles of global retail chains.

- Flexibility: Their setup allows for moderate Minimum Order Quantities (MOQs) and flexibility across colours and designs, enabling them to service campaign-based and promotional orders effectively

Business Potential

- Customer appetite is at least 10x across all product lines, given their global sourcing, including in India

- Tangible move for sourcing to India from China across tFaze Three Ltd’s products amongst the Faze Three Ltd’s Customers

- Huge unfulfilled demand within the existing customer base/product mix offered by the Faze Three Ltd

The total cumulative capex reported has crossed ₹300 Crores from FY19-Q3FY26

Plants Commissioned (Concluded Expansions)

A. Silvassa Factory (Floor Coverings, Performance Rugs, Technical & Outdoor Textiles)

- Project Timeline: Commenced in December 2020 / April 2021 and concluded in June 2022.

- Capacity Potential: Built to support a revenue capacity of up to ₹500 Cr.

- Current Status: Commissioned. As of the most recent updates, overall utilisation stands at around 60%.

B. Top of Bed & Blankets Segment

- Project Timeline: Commenced in November 2021 and concluded between November 2022 and 2023.

- Details: Brownfield expansion on existing land to scale capacity to 3x of existing levels, backed by commitments from various customers.

- Capacity Potential: Built to support a revenue capacity of over ₹450 Crores.

- Current Status: Commissioned. Current utilisation is at approximately 50%.

C. Aurangabad Plant (Mats and More Pvt Limited)

- Project Timeline: Investment phase spanned from July 2022 to December 2023.

- Details: A subsidiary investment aimed at capturing a new category of floor coverings: patio mats and outdoor textile products.

- Capacity Potential: Built to generate a revenue potential of at least $10 Million (Phase 1) over 3-4 years, translating to a revenue capacity of ₹150 Crores.

- Current Status: Commissioned. Current utilisation is hovering around 30% to 31%.

D. ESG and “Green” Capex Initiatives

- Faze Three Ltd has invested in sustainable energy and operational equipment, including a 3.5 MW Rooftop Solar energy plant (captive), transitioning to Clean Energy (PNG) for processing, and acquiring Lithium-ion (Electric) Material Handling Equipment.

- Investment: The aggregate investment for these green initiatives is over ₹25 Crores.

Plants Yet to be Commissioned / Ongoing

Panipat Factory (Cotton Home Textiles & Processing Unit)

- Details: A major ongoing brownfield expansion to increase output by 3x in the Handloom and Cotton Home Textiles division.

- Project Timeline & Delays: The timeline for this project has been extended several times. Initially slated for completion in April/May 2023, the target was subsequently moved to October 2023, January 2024, and December 2024. The latest PPT cite the ongoing expansion timeline as 2024 – 2026.

- Capacity Potential: Once fully operational and ramped up, this unit is projected to have a revenue capacity of over ₹550 Cr.

- Current Status: Ongoing/Partially Operational. Current utilisation is reported at around 50%, indicating that while parts of the expansion are functional, the full scale of the project is still ramping up.

Faze Three Ltd has stated that its current planned capex cycle is expected to be fully concluded in FY27.

Historically, Faze Three Ltd has reinvested a significant portion (often over 70%) of its CFO into expansions. Once the current capex plan concludes in FY27, management expects that at least 40% to 45% of its CFO will become available for alternative uses in the years ahead.

Care rating credit report – Sep 2025

Raw Material and Pricing

1. Key Raw Materials and Composition

- Faze Three Ltd’s major raw materials are Cotton, Polyester Yarn, and Latex.

- Polyester yarn and synthetic latex are crude oil derivatives. Consequently, their pricing is directly linked to international factors such as OPEC output, US-Iran sanctions, and global crude oil prices.

- Faze Three Ltd claims to have equal capabilities and expertise in both Cotton and Man-Made Fibre (MMF)/Polyester products. Management expects the share of MMF/Polyester to rise in the future, aligning with global trends.

2. Sourcing Strategy: Domestic Dominance

- Faze Three Ltd procures approximately 95% of its raw materials from domestic sources within India.

- This high level of domestic sourcing minimises exposure to international supply chain disruptions and fluctuations in global commodity pricing.

- Manufacturing units are strategically located in districts where major raw materials are locally available, allowing the Faze Three Ltd to prioritise suppliers in the local community.

3. Cost Structure and Margin Impact

- Faze Three Ltd’s operating margins remain susceptible to adverse movements in raw material prices (cotton and crude oil).

- While peers faced margin hits due to rising cotton prices in recent years, Faze Three Ltd was able to sustain margins better than many competitors. This is attributed to its business model of focusing on promotional/ campaign-based orders (which allow for fresh price negotiation) rather than fixed long-term replenishment programs.

4. Risk Management and Hedging

- Faze Three Ltd explicitly states that it does not deal in commodity price hedging activities. Therefore, it bears the risk related to commodity price fluctuations.

- Order-Backed Procurement – To mitigate this risk, sourcing is planned in advance. Depending on the order size, material is acquired either individually at each plant or in bulk. The Faze Three Ltd typically follows an order-backed raw material stocking model, securing supplies upfront to lock in costs.

- Inventory Cycle: Since the business is made-to-order, the entire inventory (raw material + WIP + finished goods) is geared toward specific order deliveries, typically within a 75-120 day cycle.

Working Capital days

Faze Three Ltd has an elongated working capital cycle owing to large inventory holding requirements, given the cotton stocking requirements due to its seasonal availability and credit offered to customers. Faze Three Ltd maintains an average inventory of 90-100 days towards raw material to meet the delivery timelines.

The average collection period from customers has remained at 50-60 days over the last three years.

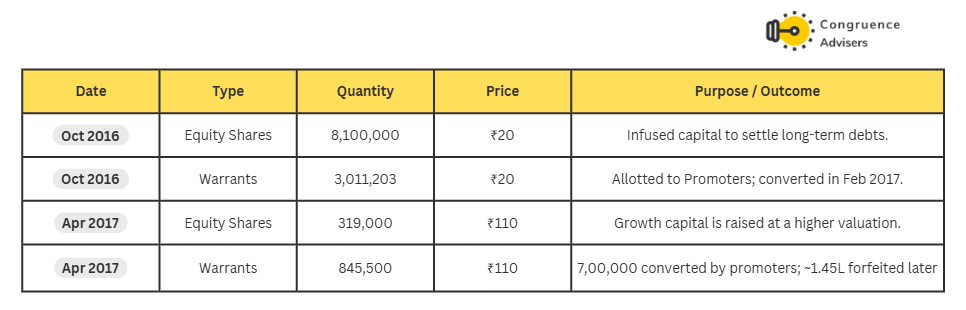

Preferential Issues played a pivotal role in the history of Faze Three Ltd (FTL), specifically serving as the primary vehicle for the financial turnaround of Faze Three Ltd between 2016 and 2018.

The Turnaround Phase (FY 2016-17)

Faze Three Ltd made a Preferential Issue and Allotment of 81,00,000 Equity Shares and 30,11,203 Convertible Equity Warrants (Rs. 20/share)on October 16, and the total amount raised was 22.22crs (Promoters infused – 6crs)

On February 15, 2017, Faze Three Ltd converted the 30,11,203 warrants held by promoters (Mr Ajay Anand and Mr Sanjay Anand) into equity shares.

Growth Capital Phase (FY 2017-18)

Following the initial stabilisation, Faze Three Ltd raised further capital at a significantly higher valuation to support growth.

- April 2017 Issue – Faze Three Ltd allotted 3,19,000 Equity Shares and 8,45,500 Convertible Equity Warrants on a preferential basis.

- These were issued at ₹110 per share/warrant (Face Value ₹10 + Premium ₹100), reflecting a substantial increase in valuation compared to the previous year.

- Promoter Conversion: On December 26, 2017, the promoters converted 7,00,000 warrants into equity shares.

Summary Table of Key Preferential Issues

Faze Three Ltd Corporate Governance

Board Composition – As of FY25, Faze three Ltd Board of Directors comprised 8 members, of whom 5 were Independent Directors. Mr Ajay Anand serves as Chairman & Managing Director, Mr Sanjay Anand as Whole-time Director (Promoter, Executive), and Mrs Rashmi Anand as Non-Executive Director (Promoter).

Promoter remuneration – The total remuneration paid to promoters by virtue of remuneration was INR 1.78Cr in FY25, amounting to ~15% of Faze Three Ltd’s PAT.

Related Party Transactions – There are no related party transactions worth flagging.

Contingent liabilities – INR 18 Cr as of FY25 outstanding for Faze Three Ltd. Of this amount, INR 15 Cr are by Corporate Guarantees, and the remaining INR 3 Cr is by bank guarantees. The total contingent liabilities amount to 4.5% of Faze Three Ltd’s consolidated net worth as of Sep 2025.

Faze Three Ltd Financial Performance

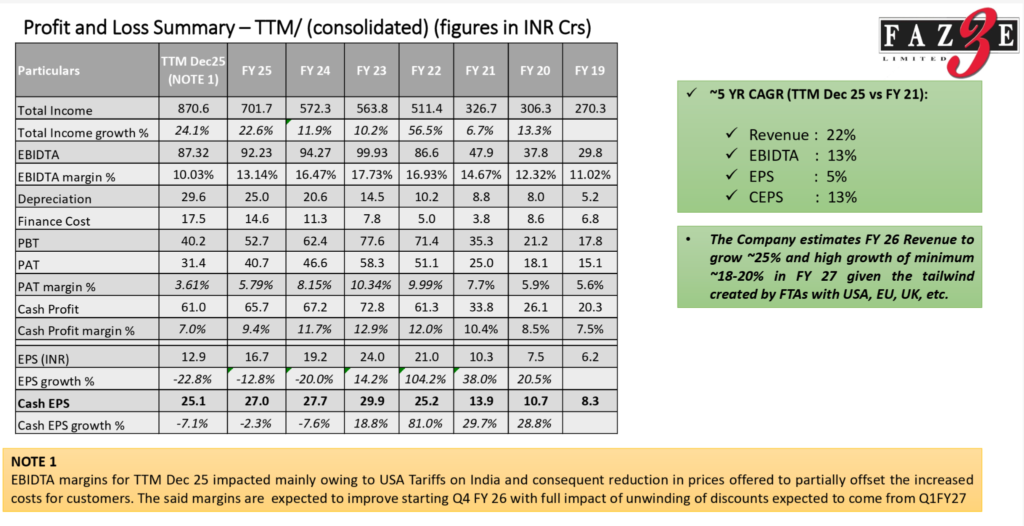

Faze Three Ltd has clearly seen strong top-line growth and its revenue has jumped from ₹326.7 Cr in FY21 all the way to ₹871 Cr over the last 4 years, that’s a remarkable 22% compounded annual growth rate. But profitability hasn’t kept pace: EBITDA margins have dropped from 17-18% to a mere 10% in just the past year because of all the downward pressure on prices and due to tariffs. Even so, absolute EBITDA has stayed pretty steady, showing that Faze three Ltd’s operations are actually pretty resilient.

Faze Three Ltd net profit margins have taken a real hit, with PAT margins plummeting to 3.6%. It looks like depreciation charges, finance costs & margin squeeze are all taking an impact on earnings. Cash flows have held up quite well (cash profit margins are about 7%), which is some reassurance that Faze three Ltd is still generating a decent amount of cash. With management saying they’re expecting 25% revenue growth in FY26 and margins starting to recover after the discounts are all cleared out, the key things to watch for now are whether margins get back on track.

Faze Three Ltd Return Ratios, Working capital, Debt, and cash flow analysis

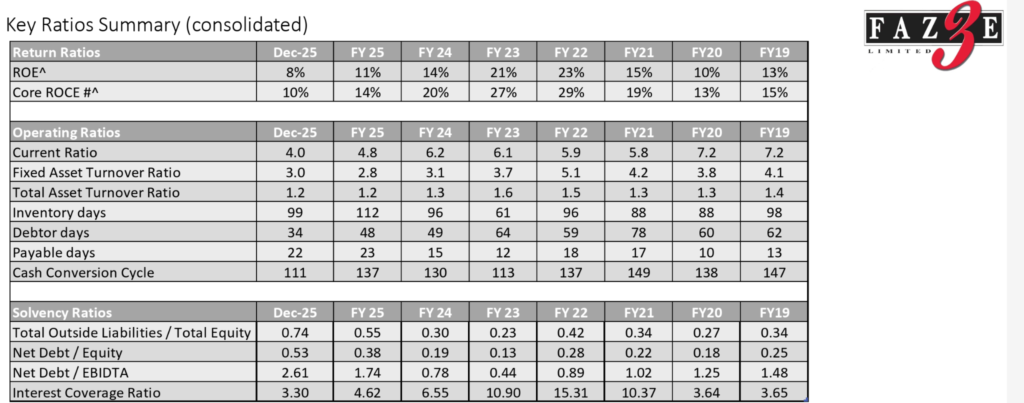

Faze Three Ltd indicates a period of significant operational strain and deteriorating capital efficiency. Since peaking in FY22, Faze Three Ltd’s Core ROCE has plummeted from 29% to 10% (as of Dec-25), while ROE has followed a similar downward trajectory to 8%, suggesting that the business is currently struggling to generate meaningful returns on its incremental investments. This decline is exacerbated by a weakening solvency profile; the Net Debt/EBIDTA ratio has spiked from a healthy 0.44 in FY23 to 2.61, and the Interest Coverage Ratio has eroded from 10.90 to 3.30, indicating reduced headroom to service debt amid falling profitability. While there is a slight improvement in the Cash Conversion Cycle (dropping to 111 days), it appears driven more by an unsustainable reduction in Debtor days rather than structural efficiency, as the overall asset turnover remains stagnant and the leverage profile continues to expand.

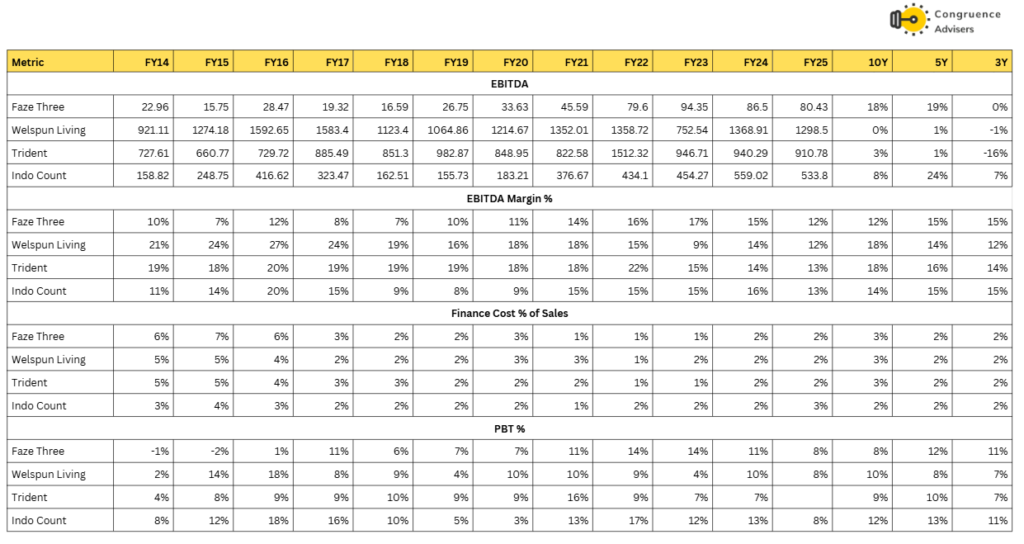

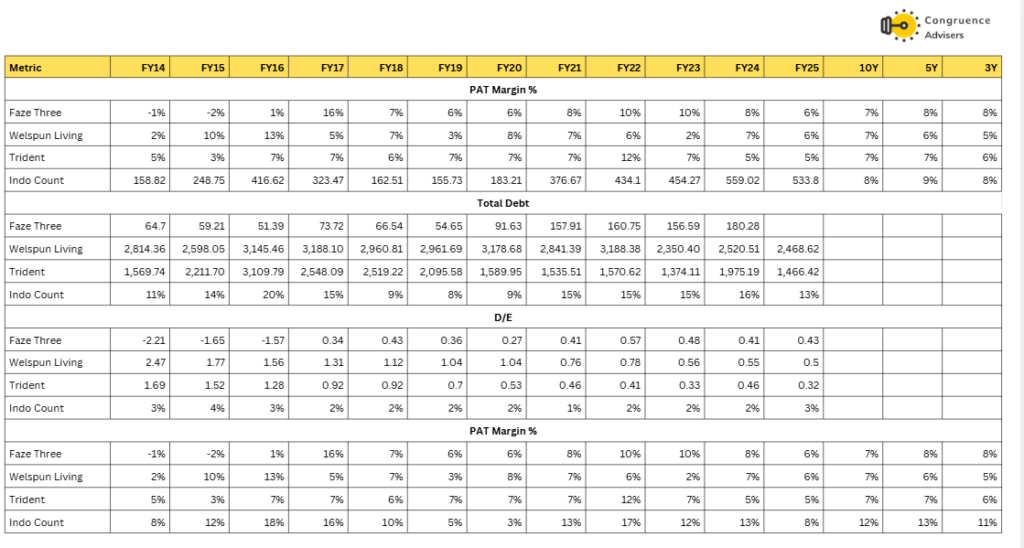

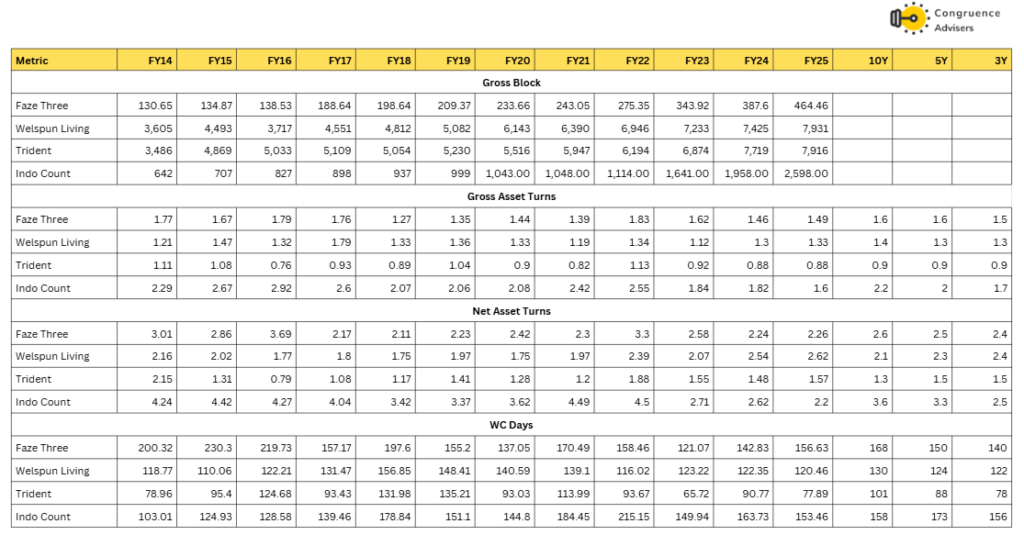

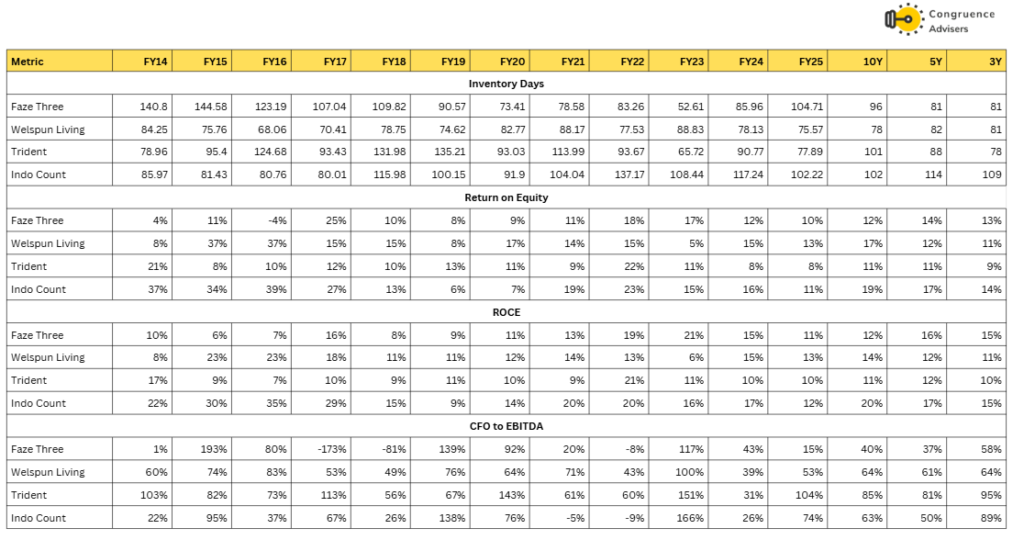

Faze Three Ltd Comparative Analysis

Faze Three Ltd Peer Comparison

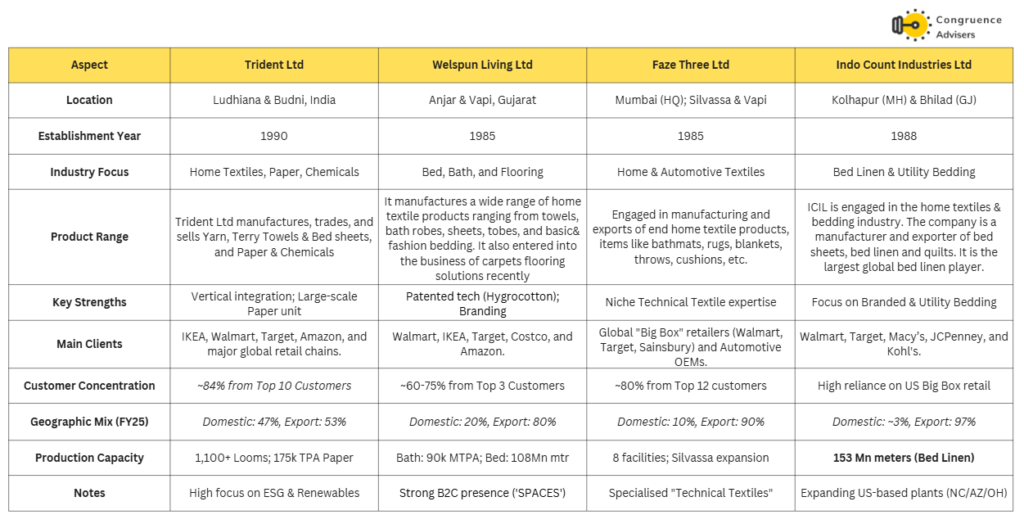

Faze Three Ltd distinguishes itself from Indian textile giants like Welspun and Trident primarily through its specific product niche, competitive landscape, and integrated manufacturing capabilities.

Product Focus:

- Welspun & Trident – These companies primarily specialise in high-volume commodity products like Bed Sheets and Terry Towels.

- While Faze Three Ltd focuses on Floor Coverings (Bathmats, Rugs) and “Top of the Bed” items (Blankets, Throws).

- Faze Three Ltd claims a specific manufacturing advantage that differentiates it from other exporters.

- Faze Three Ltd is “uniquely placed” to offer in-house handloom, Technical, and Rubber-backed floor coverings under a single corporate umbrella.

- Unlike the consolidated sheet/towel market, the competition for Bathmats in India is described as “fragmented” and dominated by unlisted, privately owned entities rather than large, listed conglomerates.

- Currently, Faze Three Ltd positions itself to capture a different wave of the “China Plus One” shift.

- Faze Three Ltd is now targeting this specific “unfulfilled demand” in Man-Made Fibre (MMF) and polyester textiles, where China is losing competitiveness due to tariffs and costs.

Why You Should Consider Investing in Faze Three Ltd

A Unique, Uncrowded Product Niche – Unlike large Indian textile giants (like Welspun or Trident) that focus heavily on mass-market commodity products like cotton bed sheets and terry towels, Faze Three Ltd specialises in floor coverings (bathmats, rugs), “top of the bed” items (blankets, throws), and technical/outdoor textiles. Faze Three Ltd is uniquely positioned by housing handloom, technical, and rubber-backed manufacturing under one umbrella. This integrated model gives Faze Three Ltd a distinct competitive advantage, serving as a comprehensive “one-stop shop” for global retailers.

Aggressive Capacity Expansion – To capture this incoming demand, Faze Three Ltd is executing a major capital expenditure plan to increase its capacity by 2 to 3 times, aiming to reach an annual revenue run rate of ₹1,500 Crores over the next five to six years. Crucially, Faze Three Ltd is funding this entire expansion with zero long-term debt since FY18. The capex is highly capital-efficient, with new investments projected to generate asset turnovers of 8x to 10x.

Sticky Blue-Chip Clientele & Recession Resistance – With over 90% of its revenue derived from exports, Faze Three Ltd supplies to some of the world’s largest retail giants, including Walmart, Target, Costco, Marks & Spencer, and TJ Maxx. These relationships are highly sticky, with top clients providing consistent business for over two decades. Furthermore, Faze Three Ltd ‘s products are generally positioned in the 10–25 retail price band, a “home improvement” segment that historically remains highly resilient even during economic slowdowns or recessions in the US and Europe.

Strong Promoter – Faze Three Ltd is anchored by a deep-rooted, second-generation promoter leadership with over 35 years of specialised expertise in home and technical textiles. Founded in 1985 by Ajay Anand (CMD), the leadership has successfully navigated complex international markets, establishing a robust global footprint in high-value home furnishings and technical fabrics. The strategic induction of Vishnu Ajay Anand in 2017 signals a disciplined approach to succession planning. This seasoned promoter group is complemented by a professionalised senior management tier, blending entrepreneurial agility with institutional oversight, a critical framework for scaling operations in the competitive textile export segment.

Favourable Government Policies – Faze Three Ltd operates in a highly supported sector, benefiting from government schemes like the Remission of Duties and Taxes on Exported Products (RoDTEP) and the Production Linked Incentive (PLI) scheme for Man-Made Fibres (MMF), which further optimise the supply chain and boost export competitiveness.

What are the Risks of Investing in Faze Three Ltd

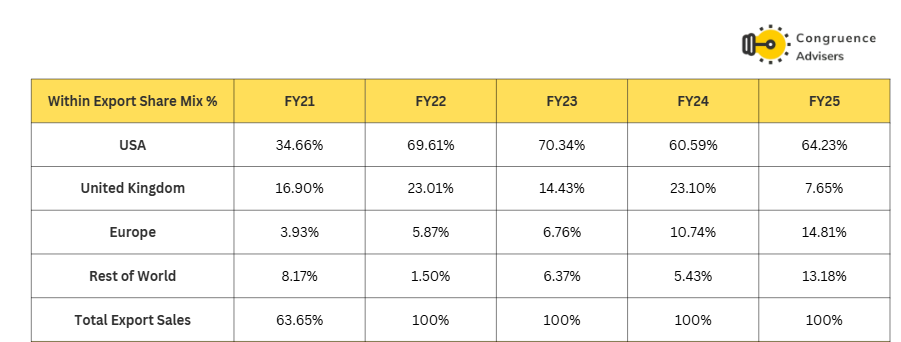

Highly export dependent model – Faze Three Ltd is predominantly an export-driven Faze Three Ltd, deriving roughly 90% of its total revenue from overseas markets. The United States is its largest market, historically accounting for 50% to over 65% of revenue, with the UK and Europe contributing another 25% to 35%. This heavy reliance makes Faze Three Ltd highly vulnerable to economic slowdowns, recessions, or shifts in consumer spending in these specific Western markets.

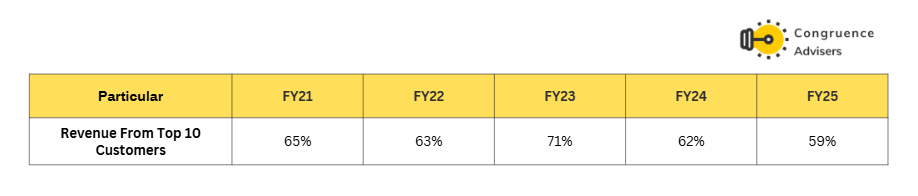

Client Concentration – Faze Three Ltd relies heavily on a small pool of massive global retailers. The top 12 to 15 customers consistently contribute approximately 80% of total revenue. While these relationships are long-standing, the loss of even one major retail client would have a significant negative impact on earnings

.

Forex Fluctuations – Because 90% of Faze Three Ltd sales are realised in US Dollars, its profitability is highly exposed to currency volatility. While the Faze Three Ltd utilises forward contracts to hedge its exposures, it does not follow a strict hedge accounting policy, meaning mark-to-market (MTM) fluctuations are routed directly through its Profit & Loss account. This can cause massive swings in reported profitability; for example, in Q2 FY26, Faze Three Ltd recorded a ₹16.92 Crore MTM loss on USD/INR forwards, which significantly depressed its operating margins for that quarter.

Raw Material Price Volatility & Climate Risks – Raw material costs, primarily cotton and crude-linked polyester/latex, consume 42%–50% of revenue, leaving margins highly sensitive to volatile oil prices and OPEC-driven shocks. Furthermore, climate change poses a systemic risk to cotton yields; unpredictable weather and water scarcity threaten long-term supply stability and fibre quality.

Highly Working-Capital Intensive Operations – The nature of Faze Three Ltd made to order business requires deliveries to be made in single large shipments, leading to an elongated working capital cycle historically hovering around 130 days. To meet delivery timelines, Faze Three Ltd is forced to maintain high average inventory levels of 90 to 100 days just for raw material stocking. This ties up significant cash and relies heavily on smooth supply chain functioning.

Intense Global Competition – While Faze Three Ltd is taking market share from China, it operates in a highly competitive global landscape. It faces constant pricing pressure not only from China but also from other low-cost manufacturing hubs in South Asia, including Vietnam, Bangladesh, and Pakistan. Furthermore, Faze Three Ltd faces the continuous risk that Chinese competitors might receive unfair subsidies from their government, distorting market prices

Changing world order & US policies – It has been a tumultuous period for US export oriented players since April 2025 due to the change in the tariff structure and the unreliability of the terms proposed by the new US regime. In the face of such volatility in policy that has translated into volatility across energy prices, capital flows & currency markets, one has to wary of possibilities that can significantly dent the business prospects of businesses like Faze Three Ltd.

Faze Three Ltd Future Outlook

Management Guided for FY26 and FY27 as “high growth years ahead”. They project a revenue growth of at least 22% to 25% for FY26 and FY27. Management notes that Faze Three Ltd successfully doubled its revenue and EBITDA in the four years from FY21 to FY25, and expects to exceed its 5-year historical CAGR in the next 5-year period.

Source: Annual Report

While recent EBITDA and net profit margins in FY25 were suppressed by one-time product development costs, initial operating costs of new product lines, and raw material fluctuations, Faze Three Ltd expects a turnaround.

Management guides for improvement in margins over the next 12-15 months. With high growth expected in FY26 and FY27, Faze Three Ltd anticipates significant operating leverage on its fixed costs across new product lines and functions.

Faze Three Ltd Technical Analysis

We consider technical analysis to be a useful input in taking medium-term investment decisions. Many a time, price action tends to lead to fundamental developments; this is too important an aspect to be ignored by retail investors who do not have access to management outside of common forums like investor calls & AGM.

At Congruence Advisers, we like to consider both the long-term weekly chart and the daily chart to arrive at a view on price action. Combined with our understanding of fundamentals, we usually end up being better placed to be able to judge both the business cycle and the stock cycle. Playing the stock cycle right is extremely important for investors looking to extract significant alpha over the medium term.

Faze Three Ltd Price charts

On a daily timeframe, Faze Three Ltd Chart is currently in a recovery phase after hitting a major support floor near ₹352 in early 2026. Following a sharp correction from the July highs, the price has stabilised and is attempting to form a series of higher lows, currently trading around ₹451.70. While the recent bounce shows some bullish intent, the volume bars at the bottom suggest that buying conviction is still inconsistent compared to the high-volume selling seen in February. A key overhead resistance remains at the ₹577 level (the blue horizontal line), and until Faze Three Ltd stock can decisively clear the ₹470–₹500 zone.

On the weekly chart, the price action indicates a listless stock with a lot of choppiness in the structure. By the looks of it, the market has no clear view on the business and investor positioning is unclear. Our experience with such charts indicates that it takes a significant positive narrative followed by 2-3 Q’s of good numbers for the price to show a strong uptrend. For the time being, the chart shows no such possibilities. The only tangible takeaway from the price chart is that the level of ~320 has been defended multiple times and may indicate the point of peak pessimism.

Faze Three Ltd Latest Result, News and Updates

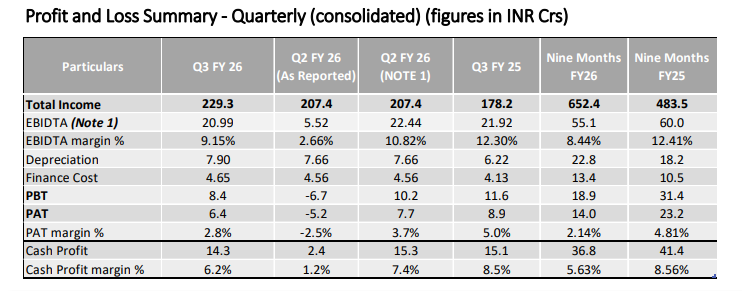

Faze Three Ltd Quarterly Results

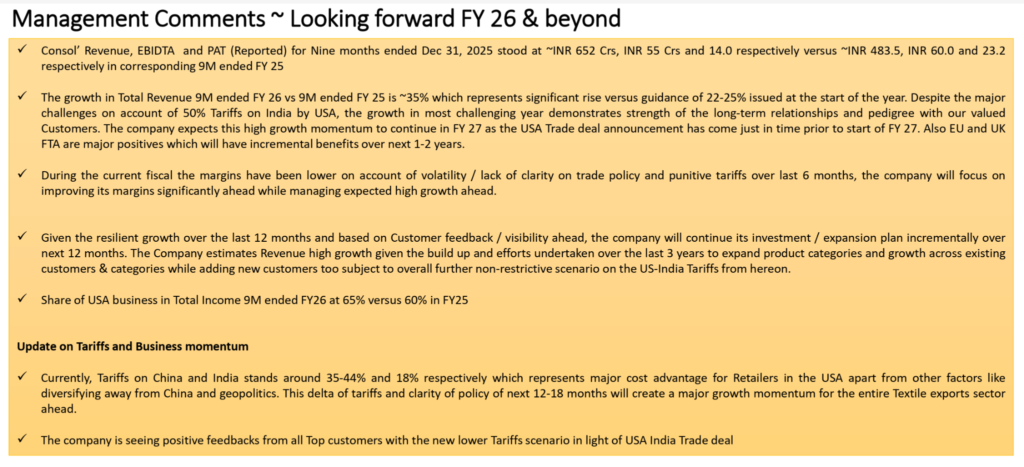

Faze Three Ltd achieved its highest-ever quarterly net sales of ₹229 Cr, representing a 27.5% YoY increase, driven by strong export demand and a recovery from a challenging Q2. However, profitability remained under pressure due to punitive US tariffs on Indian home textiles (currently at 18%) and rising operational costs, resulting in a 27.9% YoY decline in Net Profit to ₹6.40 Cr.

While Faze Three Ltd demonstrated improved operational efficiency with a high debtors turnover ratio, EBITDA margins contracted by 306 basis points to 9.2%, and the debt-to-equity ratio rose to a recent high of 0.55x. Despite these bottom-line headwinds, the nine-month revenue for FY26 reached ₹652 Cr (up 35% YoY), surpassing management’s initial guidance and reflecting the Faze Three Ltd’s successful scale-up in its technical and home textile segments.

Final thoughts on Faze Three Ltd

We found ourselves evaluating a few textile businesses over the past 15 months to see if there are any structural indicators of better times for the sector. In addition to Faze Three Ltd, we have also researched PDS Ltd, Welspun Living, Gokaldas Exports & Pearl Global Industries to explore if there is any tangible thesis here one can build for the next few years. Our efforts so far haven’t been decisive enough to offer a tangible view on this sector.

While India has signed an FTA with the UK, a trade deal with the EU and has outlined the broad contours of a trade deal with the US, the positive effects of these deals are expected to take a couple of years to show up in the P&L of the individual businesses. Specific to Faze Three Ltd, while we appreciate that the aggressive capex is coming to a logical conclusion in FY27 and that the management is guiding for a very healthy 20%+ revenue growth; the operating environment at the global level still has a lot of uncertainty.

Operating leverage as a theme can be reliably played only if unit economics is very likely to be stable over the next few years, we still do not have that level of confidence in Faze Three Ltd. All the more so given that operating margin has significantly dipped through FY25 and FY26. We will look for tangible indicators that capex commissioning is on track and that revenue growth is coming in as projected at more than 20% YoY. This business will need better utilization, mean reversion of operating margin, better cash flows and debt repayment to all fall into place if a significant rerating has to take place.

Wait and watch will be our motto on Faze Three Ltd for the time being, especially because the management team does not do investor calls. The business can make for a tactical trade upon the first quarter of good results, but until we have the macro clouds clearing up we are unlikely to put this business into the category of a medium term investment.

Disclaimer – This note is part of a business research & analysis series on small companies, there is no BUY/SELL recommendation or target price issued as part of this to a general audience. There is no assurance that this stock makes for a good investment, there is no guarantee that this stock will continue/be included in the coverage universe of Congruence Advisers. The note contains some forward-looking statements and insights drawn from the historical results, annual reports and investor presentations; they are to be viewed only within this context and not as a prediction of future performance of the business or the stock covered.

While due care has been taken to ensure that the information here is as accurate as possible, Congruence Advisers disclaims any liability in case of any unintentional inaccuracies.

The content does not constitute investment advice.