International Gemological Institute Ltd is world’s largest independent certification and accreditation services provider in the fields of diamond, gemstone and jewellery

We believe International Gemological Institute Ltd presents a rare combination of market leadership, structural growth tailwinds, and exceptional unit economics that is difficult to find in a single company. With a near-irreplaceable position in a trust driven, high-barrier industry, a net cash balance sheet, and margins that are among one of the highest in the Indian listed universe. Management’s guidance of 15-20% CAGR over the next five years supported by LGD volume tailwinds, ARP stabilisation, and global consolidation lends further credence to the thesis.

International Gemmological Institute Ltd – Company Summary

The International Gemological Institute was founded in 1975 in Antwerp, Belgium, by the Lorie family, i.e Marcel Lorie (who passed away prior to the Blackstone acquisition). Roland Lorie, a member of the founding family, served as CEO before the Blackstone acquisition and was involved in its early development.

International Gemological Institute Ltd started as a gemological organization focused on certifying diamonds, colored stones, and jewelry and establishing one of the first independent labs for gem testing and grading. It expanded globally over the decades emphasizing certification for natural diamonds, lab-grown diamonds, and gemstones to build trust among manufacturers, retailers, and consumers.

The Indian arm, International Gemmological Institute (India) was incorporated in February 1999 as a subsidiary to tap into India’s dominant role in diamond processing and jewelry manufacturing.

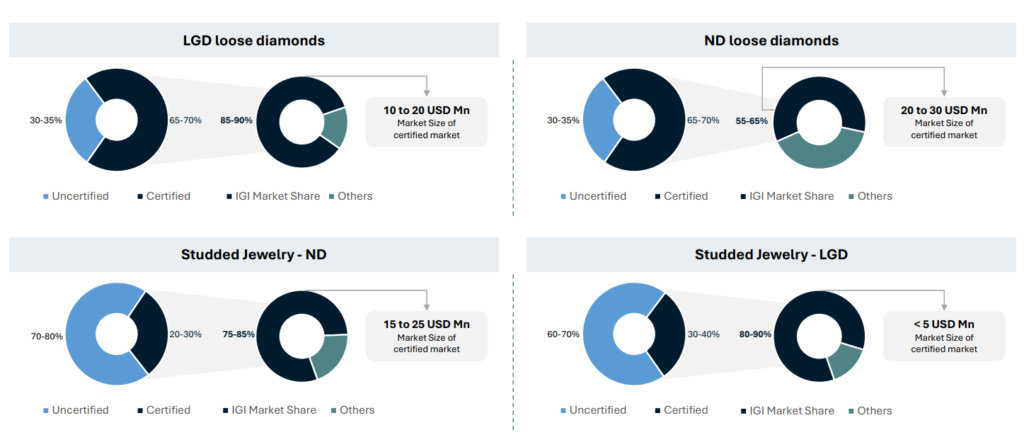

International Gemological Institute Ltd had become the largest independent certification provider with 55-90% market share across key categories, International Gemological Institute Ltd captures a disproportionate share of industry certification volumes

International Gemological Institute Ltd’s dominant market share across segments translates into predictable volumes, operating leverage and sustained pricing power

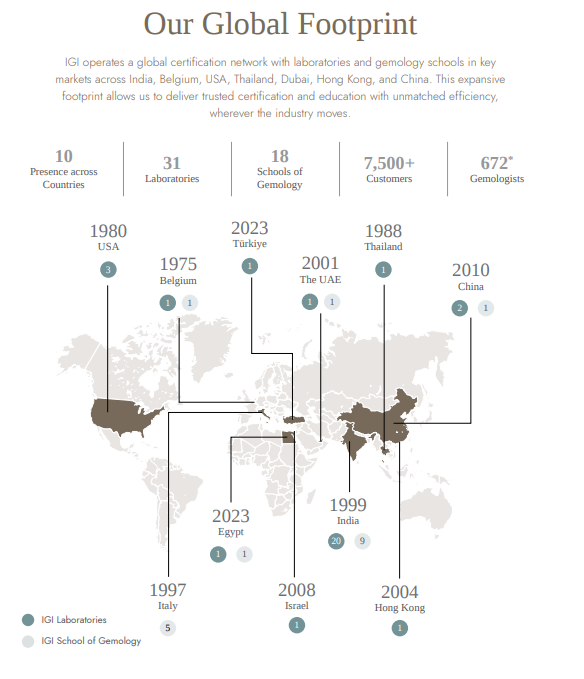

Globally International Gemological Institute Ltd operated 31 laboratories across 10 countries and 18 schools of gemology across 6 countries, with over 7,500 customers.

International Gemmological Institute Ltd – Ownership History & Capital Events

Pre-2018 – Bootstrapped Under the Lorie Family

International Gemological Institute Ltd was primarily self-funded under the founding Lorie family through its early decades of expansion. Entry into India in 1999 and subsequent geographic diversification were financed organically. The establishment of the Surat laboratory in 2010 i.e strategically co-located with India’s largest diamond cutting and polishing hub was funded internally, supported in part through institutional relationships with the Gem and Jewellery Export Promotion Council (GJEPC).

2018 – Fosun Acquisition

In 2018, Fosun International a Chinese conglomerate with diversified interests spanning tourism, pharmaceuticals, and consumer goods, including jewelry through its subsidiary Shanghai Yuyuan Tourist Mart acquired an 80% stake in the global International Gemological Institute group for approximately $101.8 million, implying a total group valuation of ~$127 million at the time.

The acquisition marked International Gemological Institute Ltd’s transition from a family-owned institution to a globally backed certification brand, with Roland Lorie retaining the remaining 20% stake. Fosun’s strategic rationale centred on expanding its footprint in gemological certification, riding the growth of the global diamond and jewelry industry.

2023 – The Blackstone Acquisition

Blackstone, through its private equity funds (BCP Asia II TopCo Pte. Ltd) acquired 100% of the global International Gemological Institute group in May 2023 for an enterprise value of approximately $570 million. This included operations in India, Belgium, the Netherlands, and other regions.

The sellers were:

- Shanghai Yuyuan Tourist Mart (Fosun) received ~$455 million for its 80% stake (a ~4.5x return on its 2018 investment of $101.8 million in ~5 years)

- Roland Lorie received ~$114 million for the remaining 20% stake

The acquisition covered International Gemological Institute Ltd’s operations across India, Belgium, the Netherlands, and other international markets.

Blackstone’s Strategic Thesis:

- Capitalize on structural tailwinds in lab-grown diamond (LGD) certification, where International Gemological Institute Ltd holds a market leadership position

- Accelerate global lab expansion and operational modernization

- Position International Gemological Institute Ltd India as the crown jewel asset for a future public listing

International Gemological Institute Ltd IPO Details

International Gemological Institute Ltd India’s IPO opened from December 13-17, 2024, with an issue price of ₹417 per share. implying an implied market capitalisation of approximately ₹18,020 crore at the issue price. The IPO was oversubscribed 33.79x overall. The stock was listed on December 20, 2024 at ₹510 per share, delivering a 22.3% gain on listing day.

The total issue size stood at ₹4,225 crore, comprising a fresh issue of ₹1,475 crore increased from an initially planned ₹1,250 crore and an OFS of ₹2,750 crore entirely by the promoter, Blackstone, via BCP Asia II TopCo Pte. Ltd. The anchor book of ₹1,900 crore was placed on December 12, 2024, drawing participation from marquee global institutional investors including Norway’s Government Pension Fund Global (Norges Bank), GIC (Singapore), and the Abu Dhabi Investment Authority (ADIA), with sovereign funds collectively contributing approximately ₹430 crore of the anchor allocation.

The proceeds from the fresh issue were earmarked primarily for the acquisition of IGI Belgium and IGI Netherlands from Blackstone approx ₹1,300 crore, consolidating the global IGI group under the listed Indian entity, with the remainder allocated toward general corporate purposes including potential expansions.

It is worth noting that Blackstone had acquired the entire global IGI group for approximately $570 million just 18 months prior to the listing (with IGI India valued at ~$393 million within that transaction), and additionally received $22 million in dividends in 2024 ahead of the IPO.

Technically, the entire IPO was effectively an OFS. While the ₹1,475 crore fresh issue nominally brought in new capital, the bulk of those proceeds were deployed to acquire IGI Belgium and IGI Netherlands assets that were already owned by Blackstone. In essence, fresh issue capital flowed straight back to the promoter, making the economic substance of the transaction an OFS in its entirety.

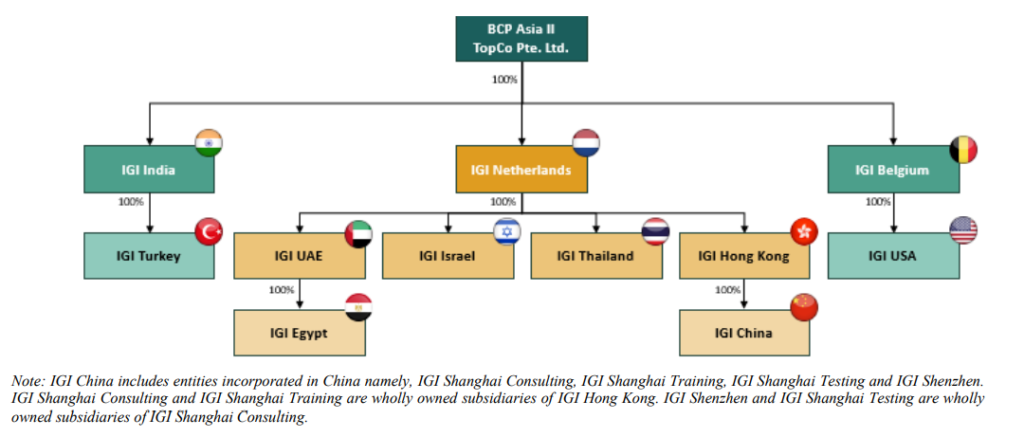

International Gemological Institute Ltd Company Structure Pre Acquisition

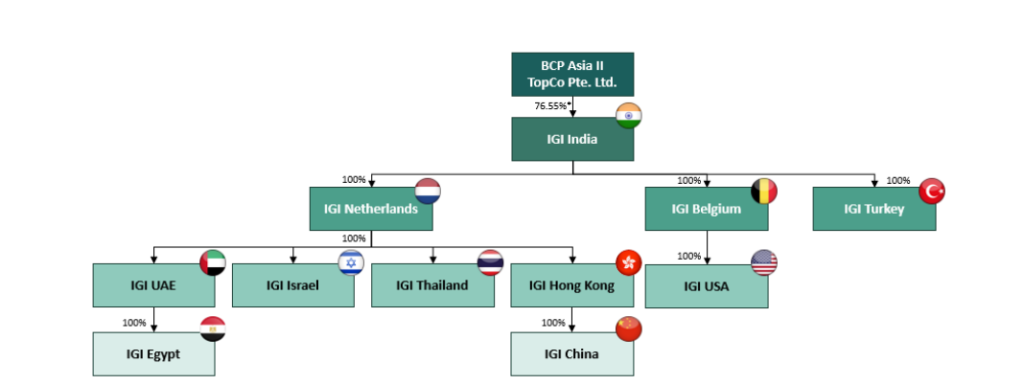

International Gemological Institute Ltd Company Structure Post Acquisition

IGI Belgium Group –

- IGI Belgium was incorporated on June 30, 1975

- IGI USA was incorporated as a domestic business corporation on March 26, 1979

IGI Netherlands Group –

- IGI Netherlands was incorporated on 22 October 2018

- IGI UAE was incorporated on May 21, 2012

- IGI Israel was incorporated on May 28, 1995

- IGI Thailand was incorporated on June 5, 1997

- IGI Hong Kong was incorporated on July 13, 2004

- IGI Egypt was incorporated on November 20, 2022

- IGI Shanghai Consulting was incorporated on October 11, 2013

- IGI Shenzhen was incorporated as a limited liability on November 5, 2019

- IGI Shanghai Testing was incorporated as a limited liability on March 13, 2020

- IGI Gemological Training was incorporated on January 29, 2021

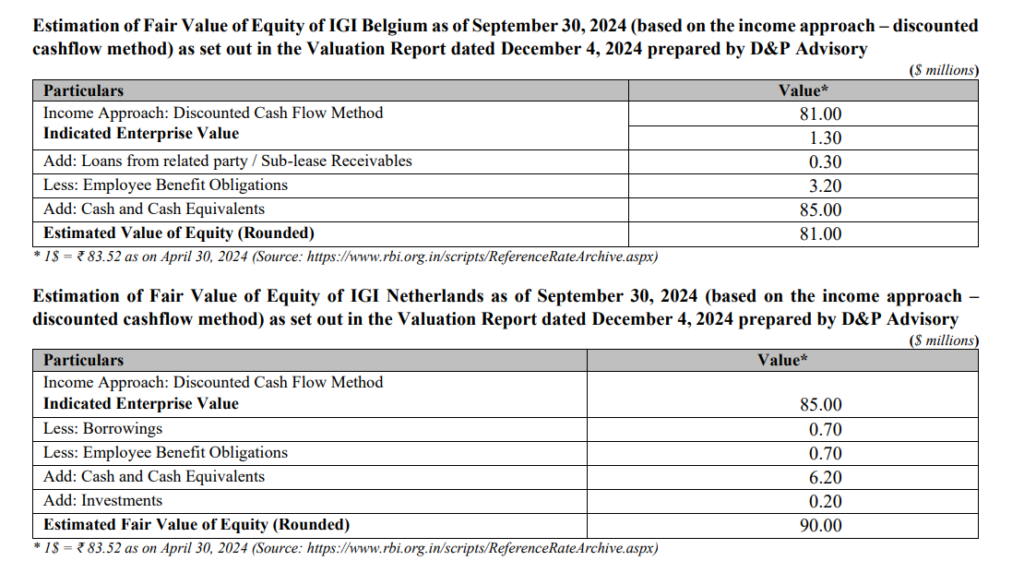

Valuation

The total cost was adjusted for net working capital, debt, and surplus cash at closing are –

Total Enterprise Value – $158.20 mn (₹1,315 cr at ~₹83/USD).

IGI Netherlands B.V – $88.4 min (₹734 cr).

IGI Belgium Group – $69.8 mn (₹579cr).

Blackstone allocated ~$176 million to European arms in its 2023 acquisition of the global group. The sale to IGIL was at a ~10% discount.

International Gemological Institute Ltd Management details

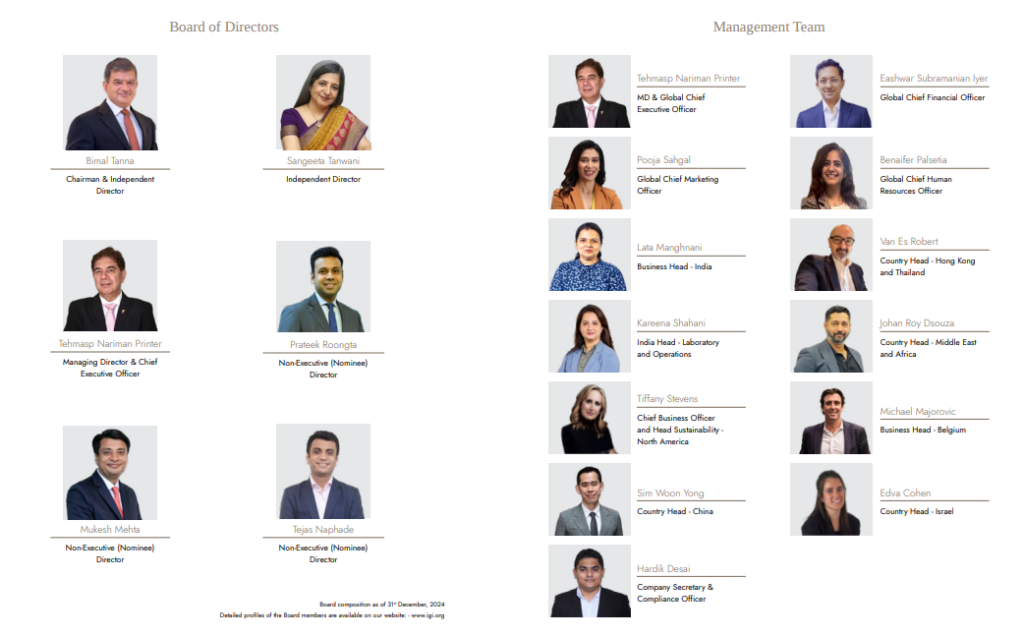

International Gemological Institute Ltd’s board comprises six directors. Bimal Tanna serves as Chairman & Independent Director, Sangeeta Tanwani serves as an additional Independent Director, Tehmasp Printer, as MD & CEO, is the sole executive director on the board. The remaining three seats are held by Prateek Roongta, Mukesh Mehta, and Tejas Naphade, all Non-Executive Nominee Directors representing promoter Blackstone’s interests via BCP Asia II TopCo.

International Gemological Institute Ltd’s operational leadership is helmed by Tehmasp Printer (MD & CEO), who has 25+ year tenure in International Gemological Institute Ltd; he is effectively synonymous with IGI’s growth from a regional certification body to a global listed leader. Eashwar Iyer (CFO) anchors the financial and investor relations function, bringing listed company credibility from his prior role as CFO of Akzo Nobel India.

The two most strategically significant recent appointments are Pooja Sahgal (Global CMO) and Benaifer Palsetia (Global CHRO), Sahgal was hired from the FMCG world with stints at Godrej, Raymond, and L’Oréal.

On the operational side, Lata Manghnani (Business Head – India) and Kareena Shahani (India Head – Laboratory & Operations). Both are long-tenured insiders with 15 and 23 years at International Gemological Institute Ltd respectively.

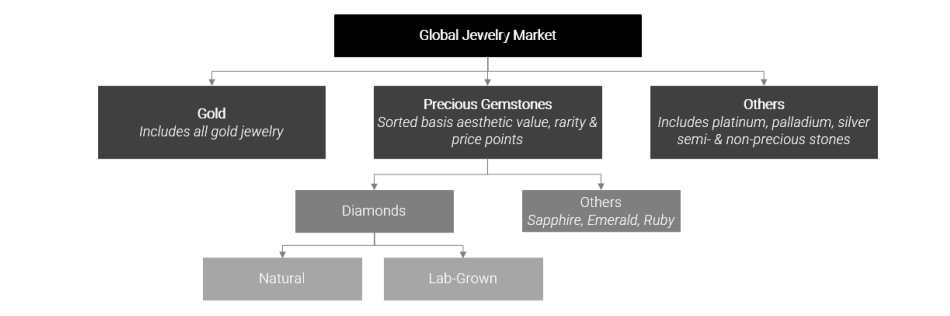

International Gemological Institute Ltd – Industry Overview

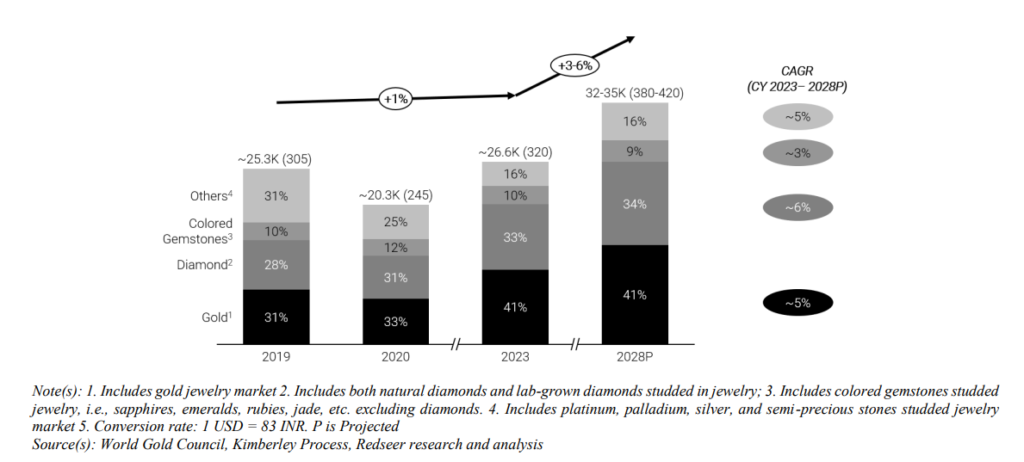

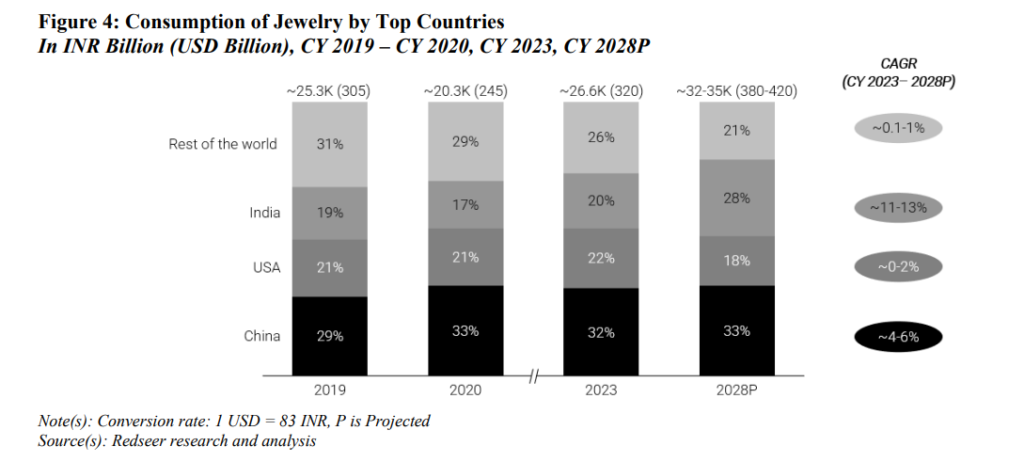

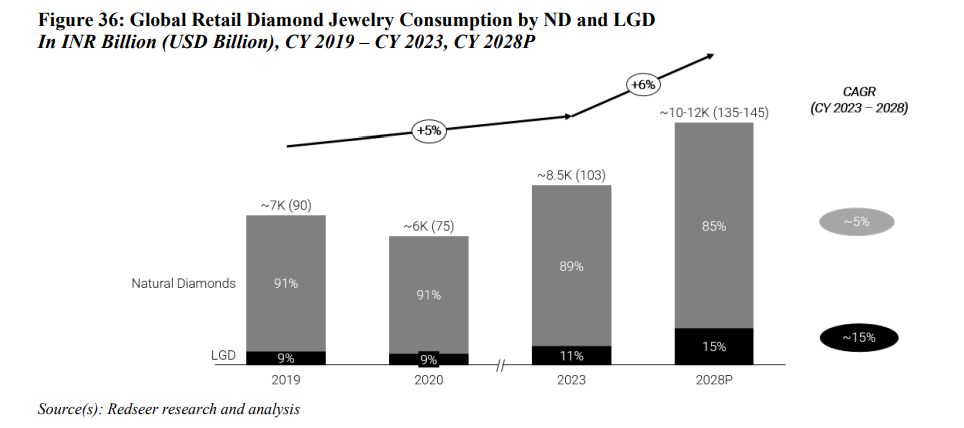

The global jewelry market stood at ~INR 26,600 billion (~USD 320 billion) in CY 2023. Since CY20, the market has rebounded, achieving a CAGR of ~9%. Over the longer term, from CY 2019 onwards, it has experienced a CAGR of 1%. Post-COVID-19, gold and diamond studded jewelry markets grew at a CAGR of 18% and 12%, respectively, from CY20 till CY23; they are currently the two largest contributors, constituting a 74% market share. The global jewelry market is expected to grow at a CAGR of 3-6% in value terms from CY23 till CY28, with the gold and diamond-studded jewelry market expected to grow at a CAGR of 5% and 6%, in value terms, respectively, over the same period.

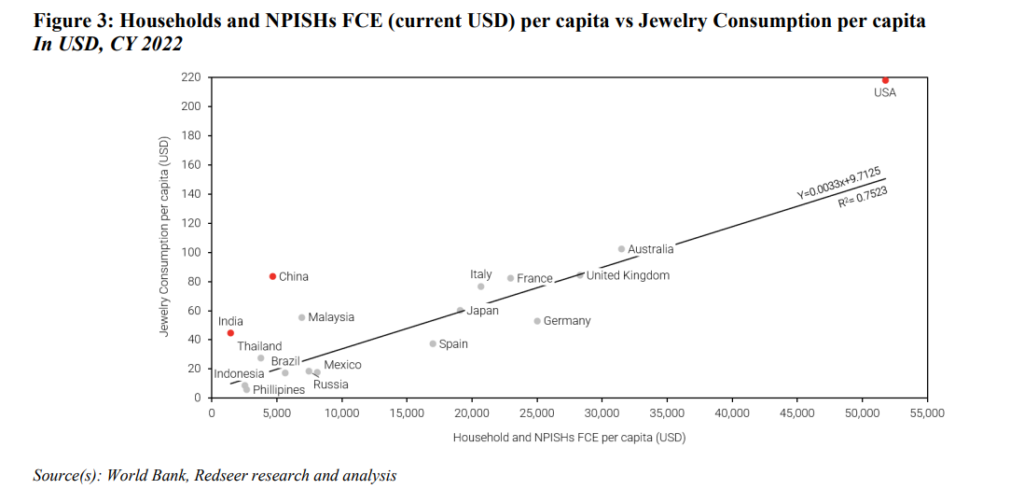

China, India, and the USA observe high spending on jewelry as a proportion of total spending compared to other economies.

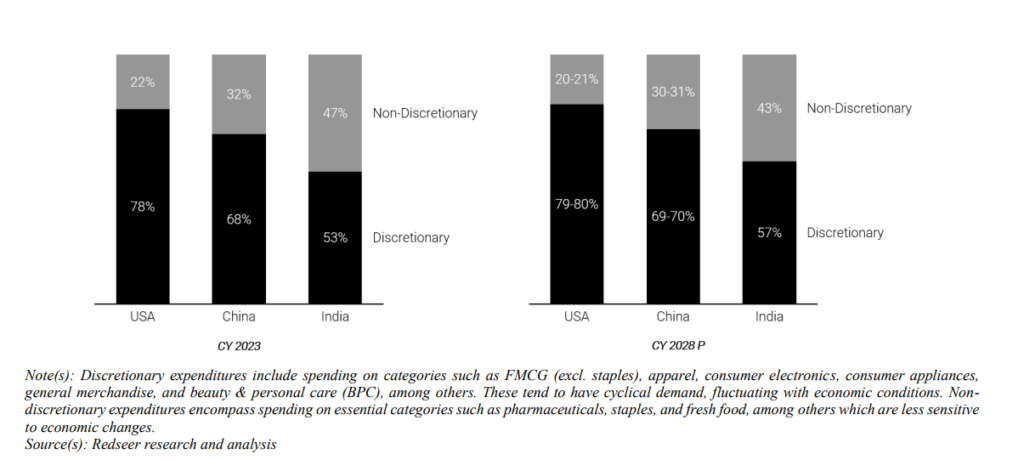

Retail Market by Discretionary and Non-Discretionary Expenditures – the USA, China and India In %, CY 2023, CY 2028P

Indian Jewelry Market Size – by Value

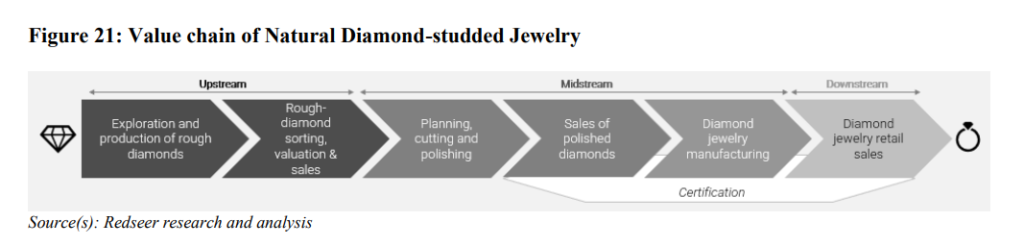

Value Chain

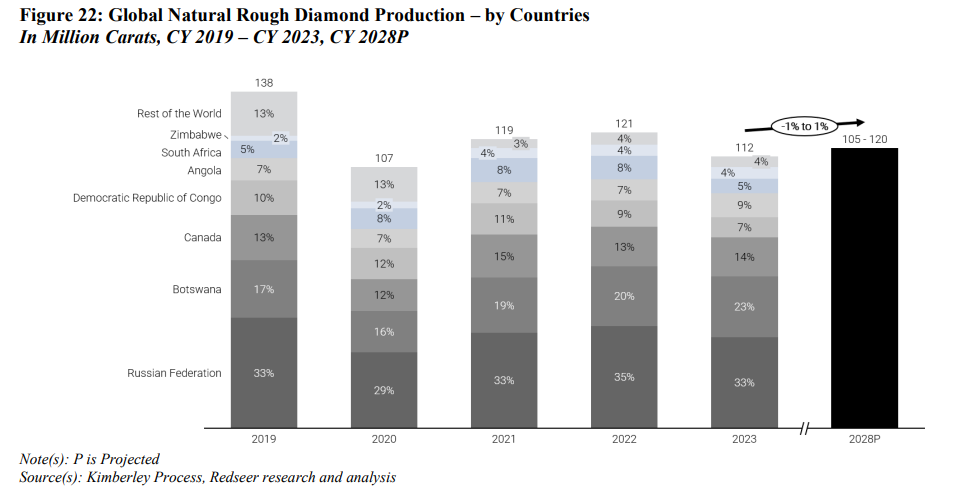

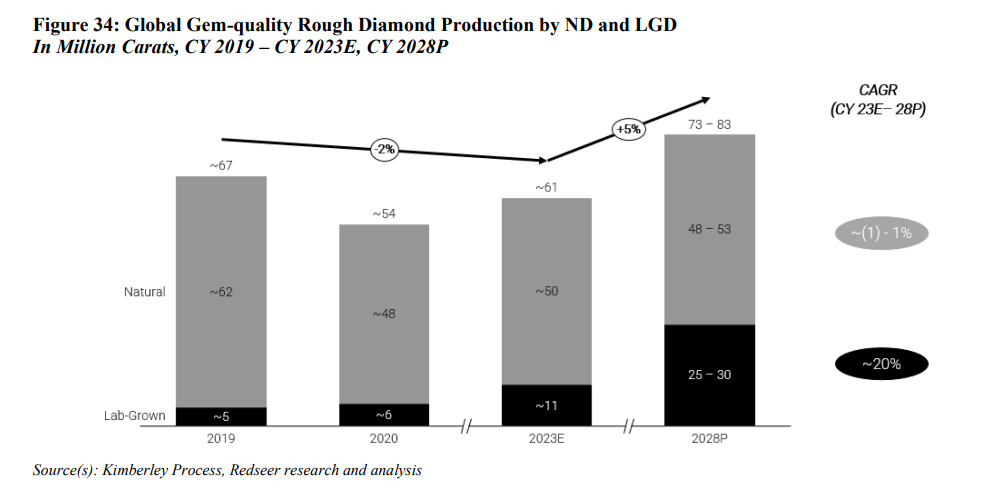

Upstream: This stage starts with exploration, where producers engage in the search for commercially viable diamond resources. Once a promising site is identified, producers proceed to develop and construct new mines. The exploration phase involves extensive geological surveys, exploration drilling, and feasibility studies to evaluate the economic viability of mining operations. Upon confirming the potential of a site, producers invest in infrastructure, equipment, and personnel to establish and operate the new mine. This stage is critical for securing a sustainable supply of diamonds and involves significant investment, planning, and risk assessment to ensure successful mine development and production. In CY 2023, there were ~1,700 million carats of industrial diamond reserves, as per the US Geological Survey. The next phase involves producers extracting diamondiferous ore (diamond-bearing location or materials) mined out of the ground. Once mined, the diamond ore passes through various processing stages to extract rough diamonds from it. Because these diamonds are in their natural state, they are called rough diamonds. Mining of rough diamonds is highly dependent on reserves, and the growth of rough diamond production has been at ~1% from CY 2010 to CY 2019. The annual production has grown by ~1% from CY 2020 to CY 2023 and is expected to be in the range of 105-120 million carats by CY 2028. Russia, Botswana, and Canada account for ~68% of total natural diamond mining in CY 2022. Furthermore, in the same year, ~35% of the world’s rough diamonds are of Russian origin. International sanctions due to the Russia-Ukraine war limiting or prohibiting the importation of these diamonds could negatively affect the worldwide supply of natural diamonds.

In the last phase of upstream processes, after extracting rough diamonds, the producers inspect, classify, and prepare them for sale. An initial sorting of rough diamonds is done for their valuation.

Rough diamonds are sold through 3 main channels –

• Tenders and auctions: Rough diamonds are offered for sale through competitive bidding processes.

• Long-term contracts: Diamond producers and major buyers negotiate long-term supply contracts, where predetermined quantities of rough diamonds are sold at regular intervals.

• Spot market sales: Buyers purchase diamonds at prevailing market prices without long-term commitments.

The authorized bulk purchasers of rough diamonds are called sight holders who can buy them via any of the above sales channels.

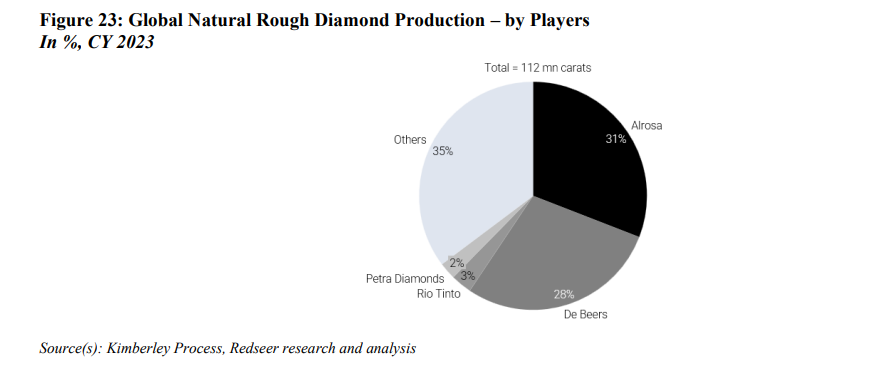

Another feature of the upstream stage of diamond production is that the market is highly concentrated in terms of market participants. The two largest players in the industry, Alrosa and De Beers, together accounted for ~60% of the world’s annual production of rough diamonds in CY 2023.

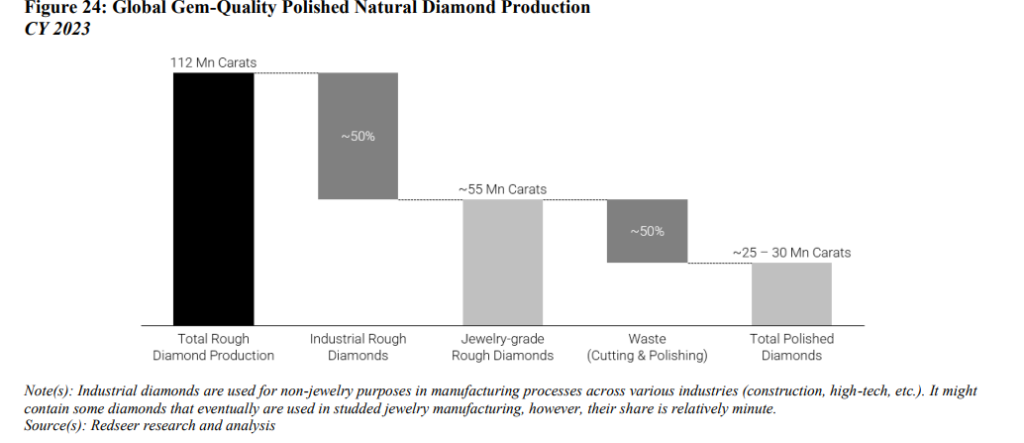

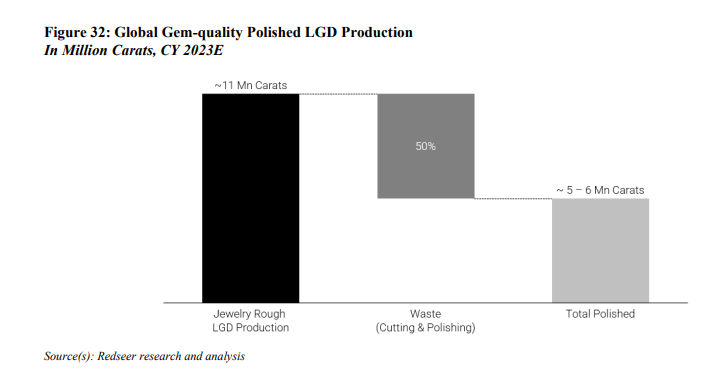

Midstream: This stage begins with careful examination and analysis of the rough diamond’s characteristics, such as its size, shape, color, clarity, and potential internal flaws or inclusion. This is done to maximize each rough diamond’s beauty, brilliance, and value while cutting and polishing. Diamond cutters use advanced technology like 3D scanning and modeling to create precise digital blueprints for each diamond. These blueprints determine the optimal shape and proportions for cutting the diamond to maximize its brilliance and fire while minimizing weight loss. The planning stage also involves making decisions about the number and placement of facets, which significantly influence the diamond’s sparkle and overall appearance. Skilled artisans called “lapidaries” then use their expertise to ensure that each diamond is cut to achieve the best possible combination of beauty and value. They transform the rough diamonds into finished stones to create the largest gem possible, given the physical properties of the stone. From the total rough diamond production, ~50% of diamonds are used for industrial purposes, and the rest, ~50%, are jewelrygrade rough diamonds. These rough diamonds lose ~50% of their weight in the cutting and polishing process.

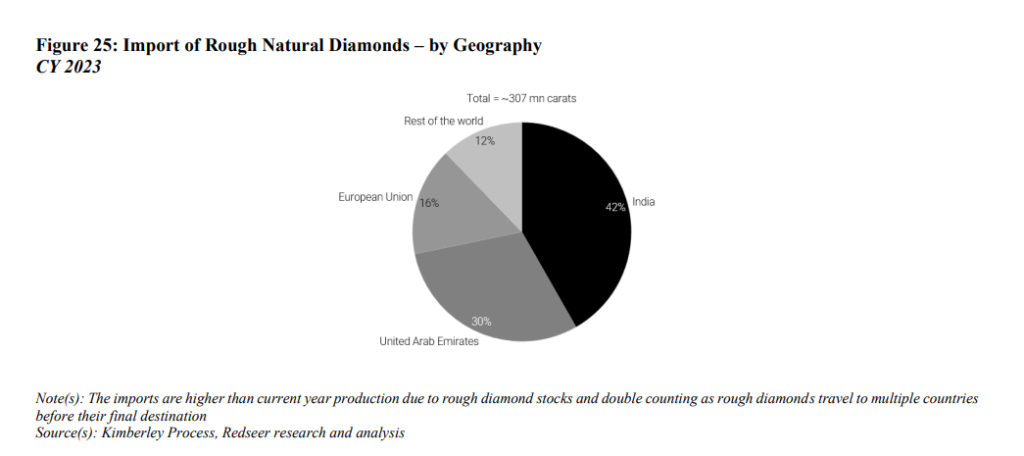

India is the leading importer of rough diamonds, contributing to ~42% of overall rough diamond imports in CY 2023. UAE and EU are the next leading importer of rough diamonds.

Cut and Polished diamonds (CPD) are then sold at wholesale prices to jewelry manufacturers. India is the world’s largest center for cutting and polishing diamonds, accounting for ~95% of the world’s total polished diamonds in volume terms in CY 2023.

This is primarily due to the low labor costs and an abundance of skilled artisans – talent accumulated with Surat, which has been a diamond trading center for several decades. In India, Surat is the primary hub of cutting and polishing diamonds, contributing to more than 90% of India’s total volume of CPD in CY 2023.

Polished diamonds undergo thorough grading and certification by independent gemological laboratories. These laboratories assess various factors, including color, clarity, cut, carat weight, and testing for natural or lab-grown origin to determine the quality and value of the diamonds. Certification of diamonds is done across the last two stages of the value chain for loose gemstones as well as studded jewelry.

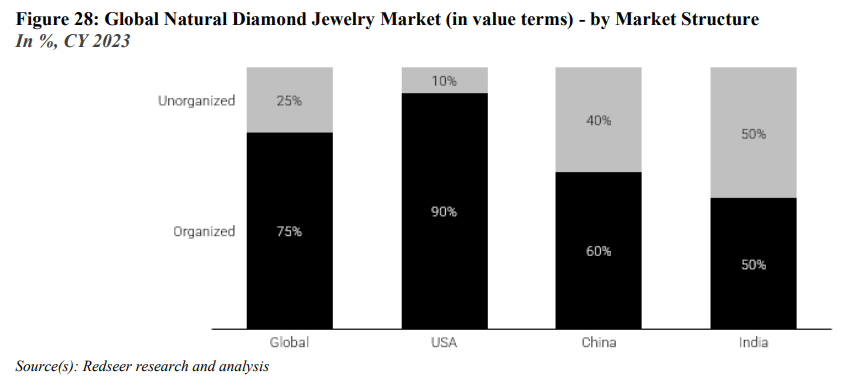

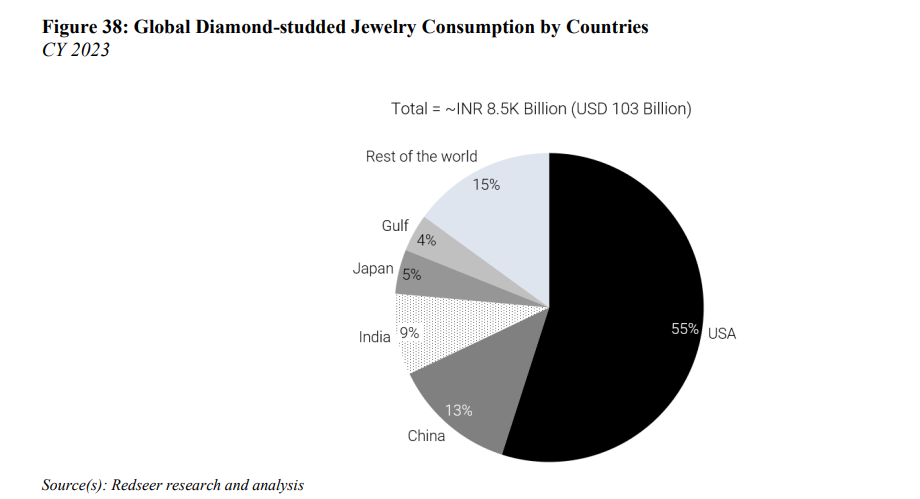

Downstream: Retail sales are the next stage of the value chain, which consists of multiple jewelry retailers selling to consumers around the world. The market is very fragmented, with multiple retail formats. After the pandemic, online retail is increasingly becoming a preferred channel for diamond purchases due to its diverse selection and increased options for consumers. While the USA is the largest consumer of diamonds, demand in Asia is increasing at a faster rate. The retail global diamond market is categorized into organized and unorganized, where organized refers to studded jewelry being sold through established retail chains, branded stores, and online platforms, whereas the unorganized includes sales through local jewelers, family-owned businesses, and informal traders. The global diamond market is primarily organized, with only 20-30% coming from unorganized channels in CY 2023. The USA is the top consumer of natural diamonds, with a 55% market share, followed by China and India, both contributing ~22% combined in CY 2023. The USA diamond market is highly organized, with ~90% contribution due to major established brands, retail chains, and stringent regulations governing the industry. Chinese and Indian diamond markets are relatively more unorganized, with ~60% and ~50% contribution from organized channels, respectively in CY 2023.

Lab-grown diamonds (LGDs): a classic case of innovation-led disruption

The development of LGDs began in the 1950s. Initially, LGDs were manufactured almost exclusively for industrial applications. However, with advancements in technology, they gradually came to meet the demand for jewelry-grade diamonds, which led to the production of jewelry-grade LGDs in the 2000s.

Traditional diamond mining involves several intricate steps, including exploration, extraction, cutting, and distribution. In contrast, LGDs revolutionize the supply chain by bypassing mining and related processes and producing diamonds with the same composition in a faster and more sustainable manner. Technological developments have further streamlined LGD production, reducing both costs and production time. The demand for LGDs is largely driven by changing consumer preferences towards more affordable, sustainable, and ethical options. While natural diamonds still dominate the big engagement markets, LGDs offer a compelling value proposition. Consumers increasingly prioritize larger LGDs with color and higher clarity with the same budget, which would have gotten them a smaller and less quality natural diamond.

Lab-grown diamond (LGD) prices are generally 70-80% lower than those of natural diamonds on a per-carat basis in CY 2023. LGD prices have declined by 37% from CY 2020 to CY 2023. Such a decrease is primarily contributed by the declining wholesale prices. The rising consumer interest and improved technology have pushed multiple players in the production chain of lab-grown diamonds, causing an oversupply in the market.

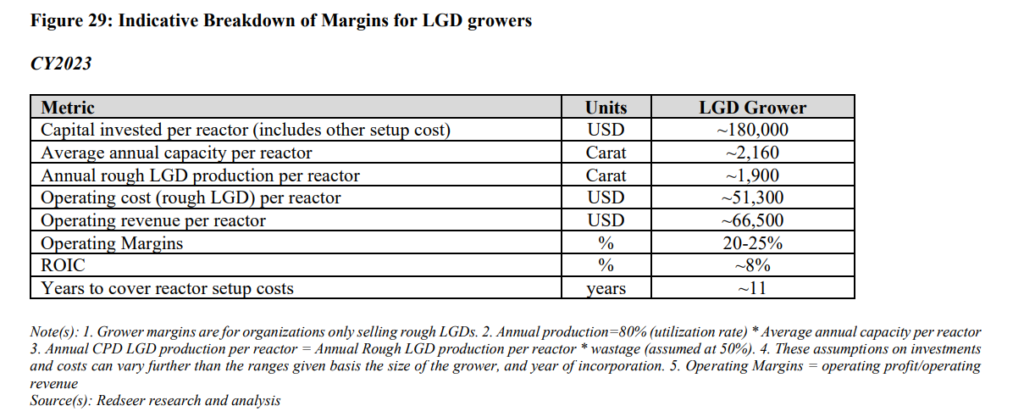

However, prices of LGDs are expected to stabilize shortly due to a theoretical minimum cost of production. In CY 2023, LGD growers are estimated to incur an initial capital investment of USD 180,000 for rough lab-grown diamonds produced per reactor. These expenses include the cost of CVD reactor machines, generators, cooling systems, gas supply systems, and other setup costs. This investment cost can vary depending on the number of reactors a grower operates. These reactors have an estimated average monthly capacity of ~180 carats. Assuming ~85% utilization, they are projected to produce ~1,900 carats of rough LGD annually. An additional estimated operating cost of ~USD 51,300 is incurred for producing rough LGD per reactor, which is then sold to polishers at ~USD 66,500, yielding an estimated margin of ~20-25% over the revenue in CY 2023. The projected operating profit per reactor is around USD 15,200 in CY 2023. Dividing this by the estimated capital investment per reactor of ~USD 180,000 results in an estimated 8% RoIC. Polishers then sell this to jewelry manufacturers with an estimated operating margin of 30-35%, at a wholesale value of USD 200-250 for a 1-carat polished LGD in CY 2023.

After manufacturing diamond studded jewelry, it is sold to retailers at USD 650-700 per carat with an estimated 20-25% operating margin in CY 2023. Jewelry manufacturers bear multiple costs like the High-Pressure High-Temperature (“HPHT”) color treatments, grading and certification, laser inscription, annealing, shipping and handling of the diamonds between different facilities, and insurance . Margins largely depend on the scale of the retailer. Retailer’s prices to the end consumer are often varied with high operating margins of ~30-35%, thus bringing the price of the loose stone up to ~USD 1,100 for a 1-carat loose stone in CY 2023.

Given the capital-intensive nature of LGD production, LGD growers are unlikely to be able to reduce the selling price of rough LGDs much further. Other players in the value chain are also unlikely to shrink their margins significantly. Thus, LGD prices will likely stabilize. Also, LGD per carat retail prices have seen a price decline slowdown towards ~37% from CY 2020 to CY 2023, compared to the 65% decline observed from CY 2016 to CY 2020.

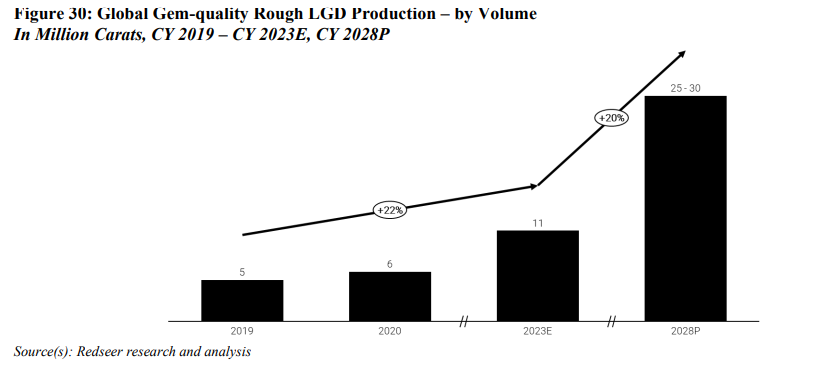

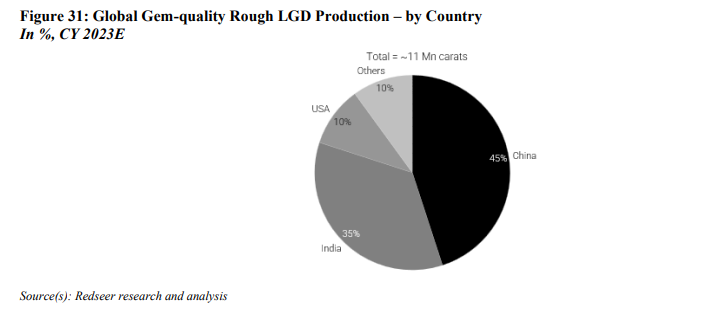

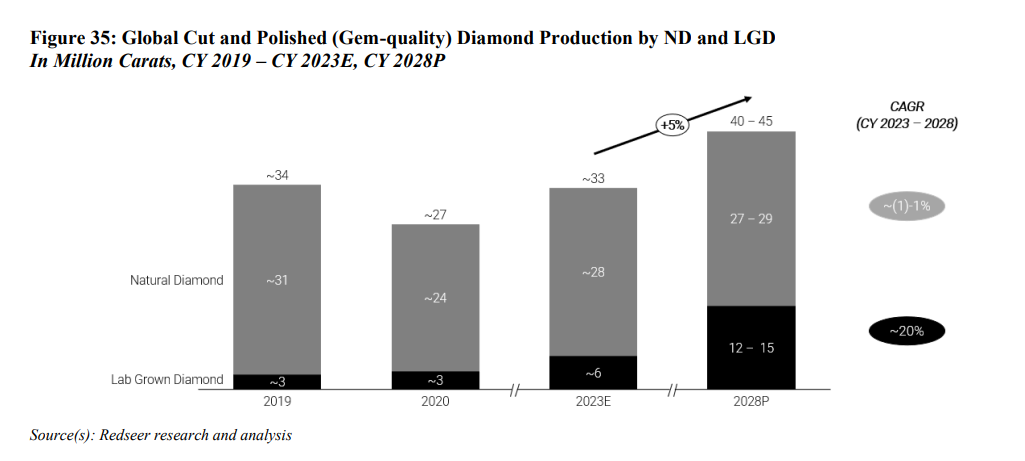

At present, rough gem-quality LGD production for jewelry purposes is estimated at ~11 million carats in CY 2023. The rough gem-quality LGD production is expected to increase at ~20% CAGR to reach a projected ~25-30 million carats by CY 2028.

China and India are the leading producers of LGDs, together contributing to an estimated ~80% of the LGD volume in CY 2023. The USA is the 3rd largest LGD producer with a 10% share.

Amongst the top studded jewelry-consuming nations, the USA leads the consumption of LGD-studded jewelry with more than ~80% of the market demand in terms of estimated volume for CY 2023. The high-income nation is viewing promising growth in non-bridal diamond-studded jewelry owing to the affordability of LGD-studded jewelry. Furthermore, jewelry brands like Pandora, which are leaders in lab-grown diamond sales, have the USA as their largest market. Their expansion into LGD-studded jewelry in North America has captured shoppers’ interest, boosting demand for their entire product range.

Similar to the production process of natural diamonds, lab-grown diamonds undergo sorting for both jewelry and industrial applications before they can be cut and polished to achieve the desired shape. It is estimated that LGDs lose ~50% of their weight during this stage.

Two primary methods are utilized in the production of LGDs: the High-Pressure High-Temperature (HPHT) method and the Chemical Vapour Deposition (CVD) process

HPHT – Emerging in the 1950s, this is the older of the two methods in terms of usage and involves a higher initial investment. Herein, diamonds are produced from carbon material in apparatuses, which create high temperatures and pressures found in natural diamond formation. This method is also used to treat the color of naturally mined or CVD lab-grown diamonds. However, its reliance on graphite input faced supply chain challenges during the pandemic, posing setbacks for the industry, particularly in China, which extensively uses the HPHT technique.

CVD – This method involves the crystallization of a diamond seed through the infusion of a carbon-containing gas in a chamber. However, it was not until the 1980s that this process was refined. Today, it requires smaller machines, works at moderate temperatures and low pressure, and tends to be cheaper and more sustainable than HPHT diamonds, thus opening the possibility for cost-effective mass production of diamonds. Unlike HPHT diamonds, which are contaminated by nitrogen, CVD diamonds are purer as they do not contain nitrogen or boron impurities. India deploys extensive use of the CVD technique.

Diamonds produced through the two methods often differ in shape, clarity, and color. Following production, they require planning, cutting, and polishing before they can become suitable for jewelry. This step is crucial, as it gives the final diamond its shape. About 90-95% of the gem-quality LGDs came to Surat, India, for cutting and polishing in CY 2023.

Currently, the total global gem-quality rough diamond production is estimated at ~61 million carats in CY 2023. LGD production has observed a faster growth than natural diamond production from CY 2020 to CY 2023 and has reached an estimated ~11 million carats. It is further expected to increase at a faster growth rate of 18-22% till CY 2028 and projected to reach 25-30 million carats.

Brief history of Gemstones and Diamond Certification

Diamond certification involves thorough analysis conducted by independent laboratories, blending scientific examination and subjective evaluation. Today, the diamond grading system serves as a crucial communication tool across the industry. Over time, this system has evolved and been influenced by technology, collaboration, and a deeper understanding of diamonds.

In the 1800s, diamond grading faced challenges, especially in determining color consistency. Terms like “Jager” and “Cape” denoted diamond origins (based on their mining locations), and grading metrics were largely inconsistent, complicating the grading system. In 1941, a US-based gemological laboratory became the first firm to introduce a standardized grading system.

The creation of 4Cs (Carat Weight, Color, Clarity, and Cut) in 1953 has since replaced subjective descriptors with objective letter grades, which have emerged as internationally recognized standards

Process of certification for diamonds and colored gemstones

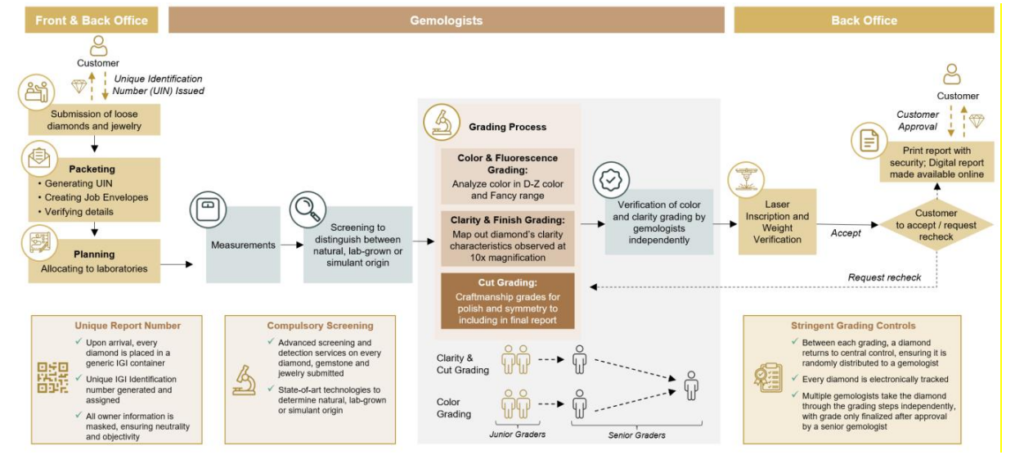

The process of diamond certification involves a series of meticulous steps conducted by independent laboratories to evaluate various aspects of a diamond’s quality –

Weight and measurement: Specialized equipment is employed to accurately weigh and measure the dimensions of the diamond. Typically, the weight of a diamond is measured in “carats” and “cents”, with 1 carat being equal to 200 milligrams and a “cent” denoting 2 milligrams. Precision in these measurements is crucial, forming fundamental aspects of the diamond’s overall evaluation.

Color grading and fluorescence: Color is a significant factor affecting the value of a diamond. The rarity of the color of a diamond, especially a natural diamond, influences its pricing, with exceptional stones fetching premium prices. Each certification agency has its own set of “master stones” consisting of diamonds with known color grades. These stones serve as a reference to determine the color grade of the stone being tested. The diamond is examined under controlled lighting conditions to accurately assess its color, ensuring consistency and reliability. It is done on a D-Z scale where D signifies colorless and Z, light yellow.

Diamonds are also tested on their fluorescence, which is the property of diamonds to emit visible light when exposed to UV rays. The degree of fluorescence impacts a diamond’s brilliance; very strong fluorescence can make it look hazy. The intensity of fluorescence is reported in a range from “none” to “very strong” after optical measurement of the visible spectrum of light generated by passing UV rays through a diamond.

Clarity and finish grading: Highly skilled graders examine the diamond under magnification and standardized lighting conditions. They assess clarity characteristics such as “inclusions” (internal flaws) and “blemishes” (external imperfections). The finish quality, including polish and symmetry, is also thoroughly evaluated against specific standards. Multiple graders may be involved in this step to verify the findings and ensure consistency. The most recognized grading system grades the highest to lowest clarity of diamonds from Flawless (FL) to Included (I). Clarity grades denote the absence or presence of inclusions and are determined under 10x magnification. Gemologists use a step-by-step wedge technique, examining the diamond in segments, to provide a map of the diamond’s internal and external clarity characteristics.

Cut grading: There has been an increased emphasis on and awareness of the fancy-shaped diamonds. Broadly, diamonds are categorized into two primary shapes when considering their cut grades: “round” and “fancy.” For round brilliant diamonds, evaluation is based on a set of guidelines/parameters that directly affect the – brightness (amount of white light that a diamond reflects.), fire (dispersion or colorful flashes of light that a diamond emits when exposed to light), scintillation (shimmer effect that occurs when a diamond is viewed from different angles), weight ratio (weight in relation to a diamond’s average girdle diameter), durability (risk of damage that might result from an extremely thin girdle), polish (quality of the diamond’s surface finish) and symmetry (alignment of diamond’s facets). The first three describe the diamond’s appearance, and the remaining four components describe the design and craftsmanship. Shapes such as “Princess”, “Cushion”, “Heart”, “Radiant”, “Emerald”, “Oval”, “Pear”, etc. fall under the category of “Fancy” shape diamonds. Most laboratories grade these diamonds on select guidelines/parameters (typically only polish and symmetry). The typical grading scale of cut consists of 5 – 6 levels (different for different certification agencies), ranging from poor/fair to excellent/ideal.

Certification report: Finally, a comprehensive certification report is generated detailing the diamond’s characteristics based on the grading system employed by the certification agency. This report includes information and relevant graphical representation of the diamond’s cut, color, clarity, carat weight, finish symmetry, fluorescence, and any inscriptions. It serves as official documentation of the diamond’s quality and attributes, providing valuable information for consumers, retailers, and industry professionals alike.

Other testing parameters (typically provided as optional tests by laboratories)

a. Laser Inscription: A unique identification number can be laser-etched onto the diamond’s girdle. This inscription provides added security and traceability, connecting the report directly to the physical diamond and enhancing confidence for buyers.

b. Origin Identification: Different laboratories have varying methods for certifying the geographical origin of diamonds and colored stones. Some laboratories document a diamond’s unique characteristics from its rough state and examine the finished diamond to certify its origin; others have identified subtle differences in physical traits of diamonds produced from different geographies as markers to create an in-house database.

Diamonds, Studded Jewelry and Colored Stones Certification Market

Diamond grading takes place once the diamonds are cut and polished. They either get certified as loose stones or, after getting studded in the jewelry, for which a certificate is issued detailing the diamond’s various attributes as the studding permits. Since the founding of the business in 1975, IGI has advanced various technical and industry practices in the loose stones and studded jewelry certification segment. In 1980, IGI USA was the first to issue jewelry identification reports among its global peers.

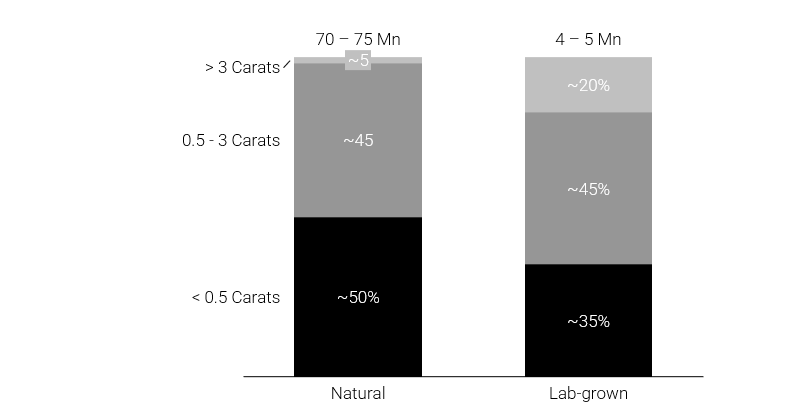

In CY 2023, ~33 million carats of loose-cut and polished diamonds, both natural and LGD, were produced. These 33 million carats of cut and polished diamonds translate to 70-75 million number of diamonds – spread across various carat weights. Natural diamonds exhibit a skewed concentration towards smaller diamond sizes, with ~50% of diamonds measuring less than 0.5 carats. This is mainly due to the conditions needed to form large and rare diamonds. Mining processes often break larger stones, and smaller diamonds are more practical and cost-effective to sell and buy. This is different in the case of lab-grown diamonds, where only ~35% of the loose gemstones measure less than 0.5 carats, as they can be produced in larger sizes more consistently under controlled and optimized growth conditions. Unlike natural diamonds, they aren’t subject to the unpredictable factors of natural formation and mining, allowing for the creation of larger diamonds that meet market demands more effectively.

Global Number of Gem-quality Diamonds Split by Carat Weights Number of Diamonds (Millions), CY 2023E

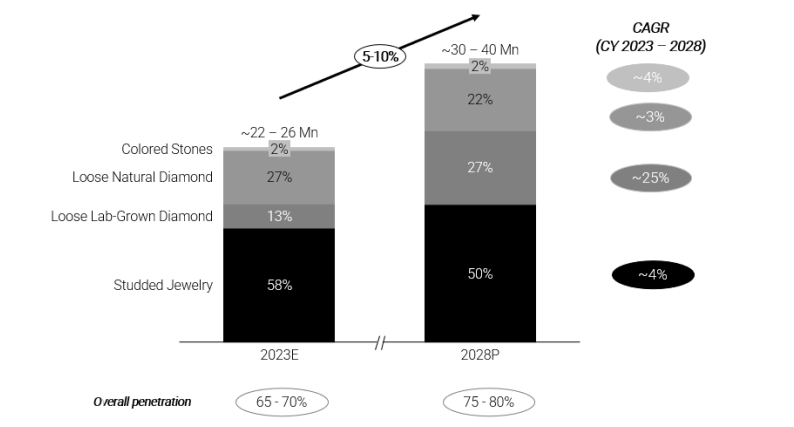

Of the total number of diamonds, the penetration of certification for natural diamonds is ~65% in CY 2023. These can either translate into loose gemstones or studded jewelry certificates. The majority of them are certified as studded jewelry, with IGI having a global market share of ~42% in terms of the number of studded jewelry certifications in CY 2023. IGI commands a global market share of 33% in the number of certifications of diamonds, studded jewelry, and colored stones performed in CY 2023. The certification penetration for LGDs is higher at ~70% in CY 2023. One of the reasons for this is that LGDs are more likely to be produced in larger carat sizes, which are more commonly certified.

The overall natural diamond certificate generation is expected to rise by ~3% till CY 2028. LGD Certification is leading the certification growth by volume expected to rise by ~25 %, leading to a projected total of 8-9 million LGD certificates in CY 2028. Overall, an estimated 22-26 million certifications were issued in CY 2023, which is projected to grow at a CAGR of 5-10% till CY 2028.

Number of Certifications Issued – by Volume Number of Certifications (Millions), CY 2023E, CY 2028P

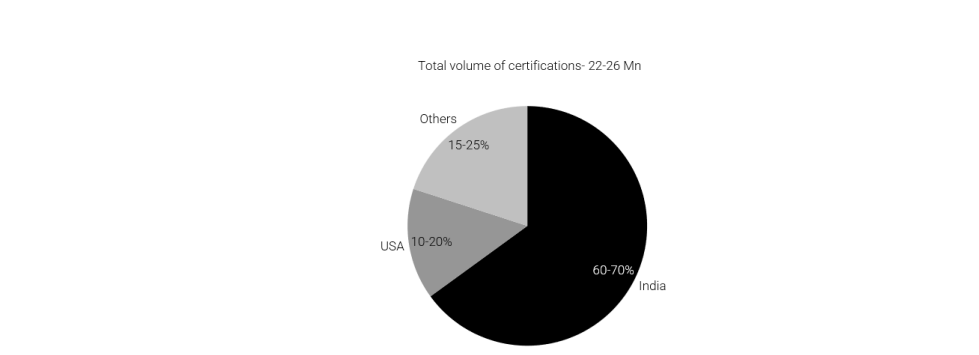

India contributed 60-70% of the overall diamonds, studded jewelry, and colored stones certifications as a key cutting and polishing hub in CY 2023. This is followed by the USA, which contributed to 10-20% of the overall certifications.

Geography wise

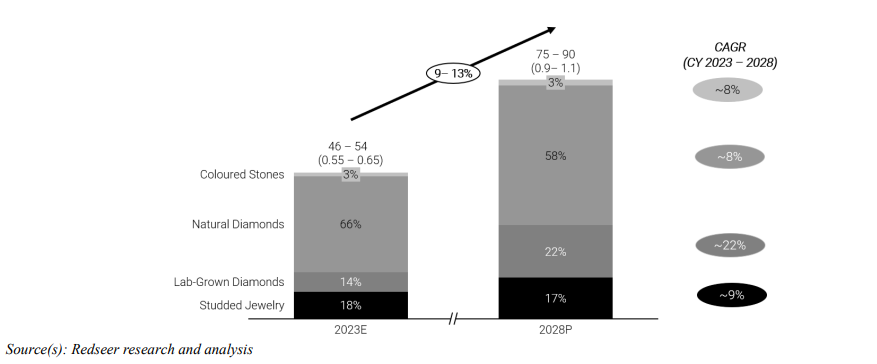

The loose stones and studded jewelry certification market is estimated at INR 46-54 billion (USD 550-650 million) in CY 2023. This is projected to grow by 9-13% from CY 2023 to CY 2028, with LGD being projected as the fastest-growing segment with a CAGR of ~22% in the same period.

Loose Gemstone & Studded Jewelry Certification Market INR Billion (USD Billion), CY 2023E, CY 2028P

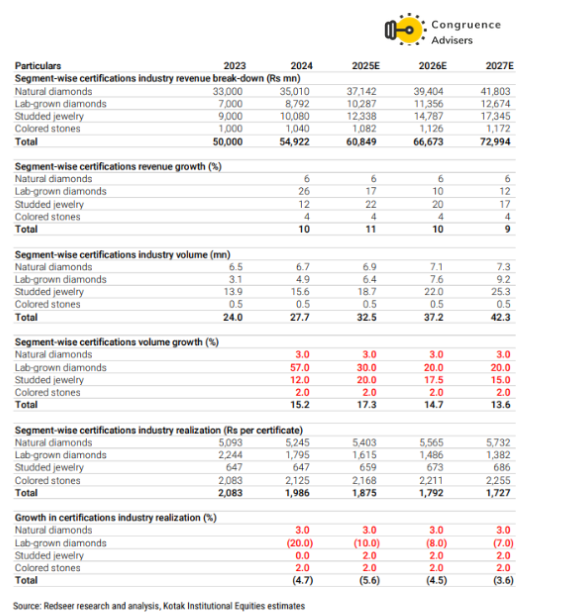

Global Certification Industry Breakdown – Revenue, Volume & Realization (2023-2027E)

The certification industry’s trajectory through 2027 tells a clear story: volume growth will decisively outpace realization growth. Total certification volumes are projected to expand from 27.7 million reports in 2024 to 42.3 million by 2027, a ~53% increase in three years driven by growth in lab grown diamonds (+57% volume growth in 2024 alone) and studded jewellery. The offset is a structural decline in per-certificate realization, with total industry ARP expected to compress from ₹1,986 in 2024 to ₹1,727 by 2027 as LGD pricing normalises. Net-net, total industry revenue is projected to grow from ₹5,492 crore in 2024 to ₹7,299 crore by 2027 at a ~10% CAGR, a healthy, if not spectacular, industry growth rate.

For International Gemological Institute Ltd, this backdrop is structurally favourable. As the dominant player in the fastest-growing segment i.e LGD certification at 65% global market share. International Gemological Institute Ltd is best positioned to capture disproportionate volume growth while its scale and operating leverage insulate margins against realization pressure. The industry is not just growing; it is growing in precisely the segments where International Gemological Institute Ltd leads.

International Gemological Institute Ltd Business Analysis

At its core, International Gemological Institute Ltd operates an independent, third-party certification and accreditation business for natural diamonds, lab grown diamonds, studded jewelry, and colored stones. The business model is highly scalable, asset light, and deeply integrated into the global jewelry supply chain, which allows them to capture value from diamond growers all the way to retail consumers

Certification Services – The core business of International Gemological Institute Ltd is the issuance of detailed grading reports assessing the 4Cs – cut, colour, clarity, and carat weight across natural diamonds, lab-grown diamonds, coloured stones, and fully finished studded jewellery.

The inclusion of finished jewellery certification is a meaningful competitive distinction. International Gemological Institute Ltd is one of very few global certifiers to assess the complete piece, evaluating mounting quality, craftsmanship, and overall value. This capability is particularly valued by jewellery retailers seeking third-party validation at the point of sale, and is a category where GIA does not participate (as noted in the peer comparison). The near-total revenue concentration in certification (~97%) reflects the purity and focus of the business model; there is minimal distraction from ancillary activities.

Co-Branded Reports & Retail Support – International Gemological Institute Ltd collaborates with leading luxury retailers to produce co-branded certification reports, a service that simultaneously functions as a marketing tool for the retailer and a brand-building exercise for International Gemological Institute Ltd at the consumer level.

As International Gemological Institute Ltd executes its “IGI: Trust, Certified” brand campaign globally, co-branded partnerships with luxury retailers represent a powerful B2C distribution channel for building consumer recognition of the International Gemological Institute Ltd hallmark i.e something no amount of trade advertising can replicate at scale.

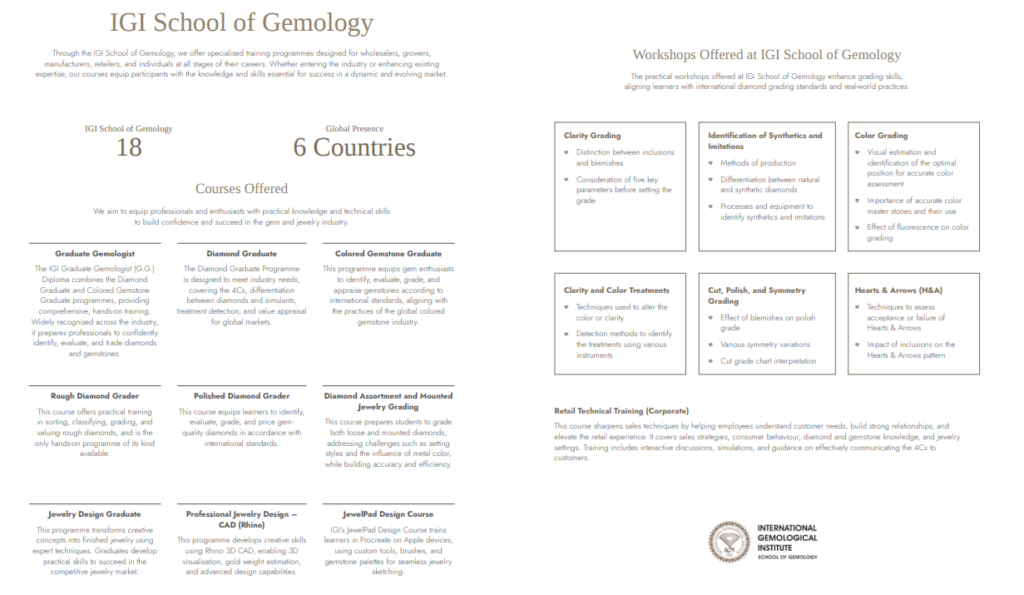

Education – International Gemological Institute Ltd Schools of Gemology operates 18 Schools of Gemology across 6 countries, offering courses in gemology, diamond grading, and jewellery design. This is far more than a revenue line, it is a strategic flywheel.

The schools serve three purposes: they build brand awareness among future industry professionals; they create a captive talent pipeline of trained gemologists for International Gemological Institute Ltd ‘s own laboratories, reducing recruitment costs and ensuring grading quality; and they educate retail sales teams, who in turn drive consumer demand for IGI-certified stones. Among all global certification peers, International Gemological Institute Ltd has the largest educational footprint, a moat that has been built over decades and cannot be quickly replicated.

Technology & Sorting Services – International Gemological Institute Ltd generates supplementary revenue through sorting and screening services, appraisals, and the sale of its proprietary D-Check screening machines to external customers.

The D-Check, which can identify and differentiate natural from lab-grown diamonds even when mounted in jewellery, is not merely an internal tool; its commercialisation as a standalone product creates an additional revenue stream while simultaneously establishing International Gemological Institute Ltd as a technology authority in the industry.

Global Footprint & Operational Model

International Gemological Institute Ltd operates 31 laboratories across 10 countries, including major hubs in India, Belgium, USA, China, UAE, and Israel. i.e the largest operational network among all global certification peers. This geographic breadth allows International Gemological Institute Ltd to serve clients seamlessly across the full diamond supply chain, from rough processing in India to retail certification in the US and Middle East.

In-Factory Laboratories – The LGD Moat Perhaps the single most strategically important operational innovation in International Gemological Institute Ltd’s model is its “in-factory laboratory” concept. International Gemological Institute Ltd currently operates 12 in factory setups embedded directly within the manufacturing facilities of large LGD growers primarily in India and China, where the bulk of global LGD production is concentrated. This model achieves three things simultaneously: it dramatically reduces turnaround times by eliminating stone transportation; it deeply integrates International Gemological Institute Ltd into clients’ production workflows, raising switching costs significantly; and it ensures high-volume retention by making International Gemological Institute Ltd certification the path of least resistance for high-output growers. This structural stickiness is a key reason why International Gemological Institute Ltd’s 65% LGD market share is defensible rather than merely incidental.

Proprietary Technology & Grading Process – International Gemological Institute Ltd maintains a rigorous 14-step grading process supported by advanced R&D capabilities and proprietary technology. The global network is unified under SwiftCert, an in-house developed software platform that tracks every submitted stone globally, standardising workflows and customer interactions across all 31 laboratories.

At the grading level, International Gemological Institute Ltd employs AI, automation, and advanced instruments including Raman Microscopes to enhance accuracy and throughput. This technology stack serves a dual purpose: it improves grading consistency (protecting the brand) and drives operational efficiency (protecting the margins).

International Gemological Institute Ltd Financial Performance

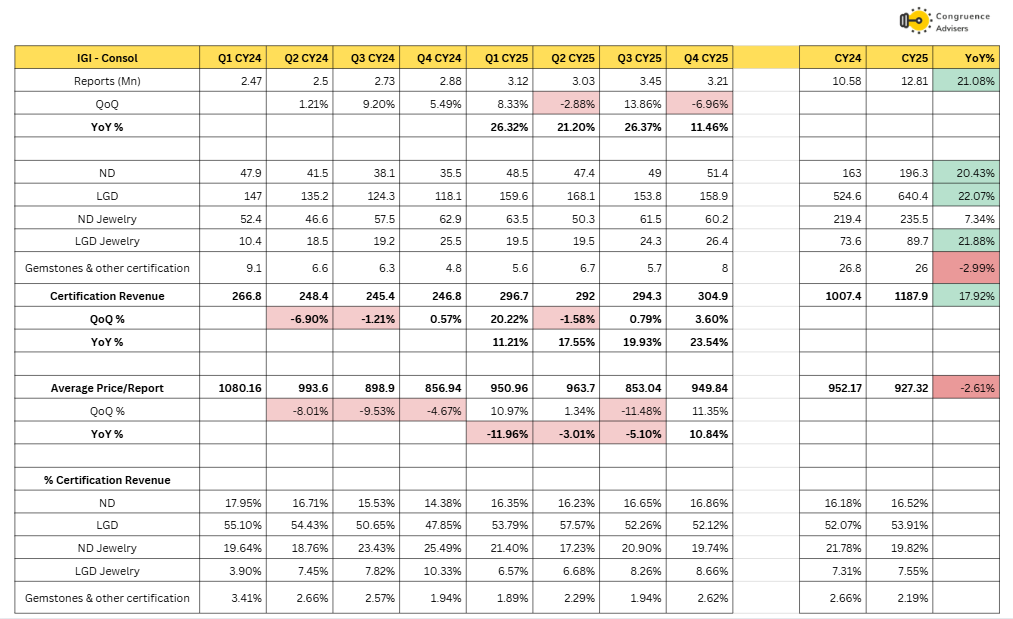

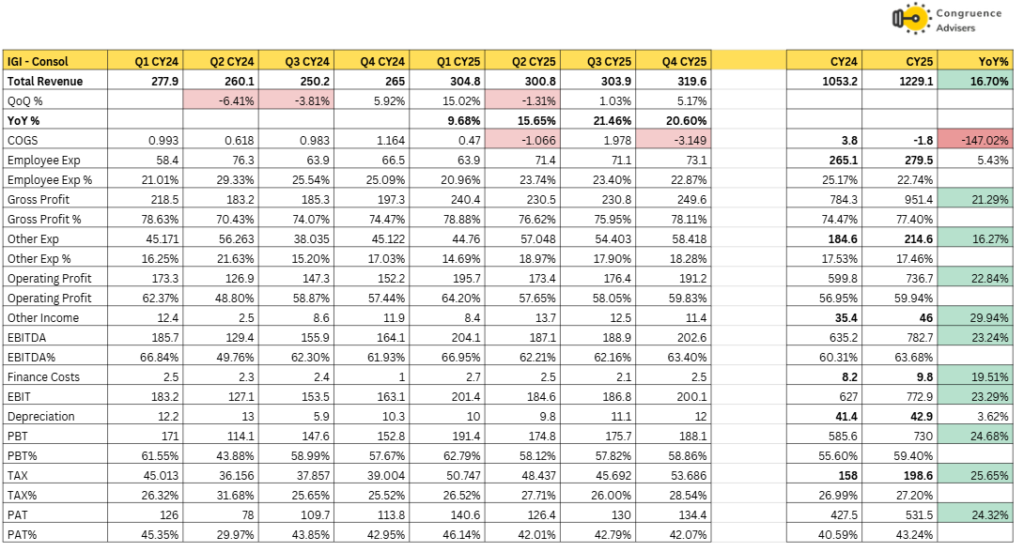

International Gemological Institute Ltd delivered 12.81 million reports in CY25, up 21.08% YoY from 10.58 million in CY24, a strong volume print that reflects broad based demand across certification categories. Quarterly momentum was healthy through most of the year, with YoY growth accelerating from 26.32% in Q1CY25 to a sustained 11-26% range through the full year, though Q4 showed some sequential moderation (-6.96% QoQ), i.e reflecting seasonality rather than any structural slowdown.

On revenue mix, LGD loose stones remain the dominant category at ~54% of certification revenue in CY25 (vs. 52% in CY24), reinforcing International Gemological Institute Ltd’s structural dependence on and leadership in the LGD segment. Natural diamond loose stones contributed ~16.5%, growing a robust 20.43% YoY, a positive signal given the broader pricing headwinds in the natural diamond market. LGD Jewellery, while still a small contributor at ~7.5% of certification revenue, grew 21.88% YoY consistent with management’s thesis of an emerging LGD jewellery retail boom. ND Jewellery at ~20% of mix grew a more modest 7.34% YoY.

Average Realized Price tells a nuanced story. CY25 ARP of ₹927 was 2.61% below CY24’s ₹952, a modest decline reflecting the pricing correction in early 2024 flowing through annual averages. However, the quarterly trajectory is encouraging: ARP recovered from a trough of ₹853 in Q3 CY25 to ₹950 in Q4 CY25 (+10.84% YoY), suggesting stabilisation that management has guided will be maintained in the ₹900-950 range going forward.

Total consolidated revenue grew 16.70% YoY in CY25, with quarterly YoY growth accelerating through the year from 9.68% in Q1 to 20.60% in Q4 a healthy exit rate heading into CY26. also Q4 CY25 EBITDA margin of 63.40% marks a strong exit quarter, consistent with management’s commentary on sustained margin strength.

Employee expenses, the primary cost line remained well-controlled at 22.74% of revenue in CY25, down from 25.17% in CY24, reflecting operating leverage on the human capital base as certification volumes scaled over a largely fixed headcount structure. This ratio is expected to improve further as the global business consolidates the integration of IGI Belgium and IGI Netherlands under the “One IGI” framework. PAT grew 24.32% YoY with PAT margins expanding to 43.24% from 40.59% in CY24, a meaningful improvement. PBT margins similarly expanded to 59.40% in CY25 from 55.60%.

International Gemological Institute Ltd Comparative Analysis

To understand International Gemological Institute Ltd investment potential, we have conducted a comprehensive analysis. This analysis includes comparing International Gemological Institute Ltd to its competitors (peer comparison) on various fundamental parameters and International Gemological Institute Ltd share performance relative to relevant benchmark and sector indices.

International Gemological Institute Ltd Peer Comparison

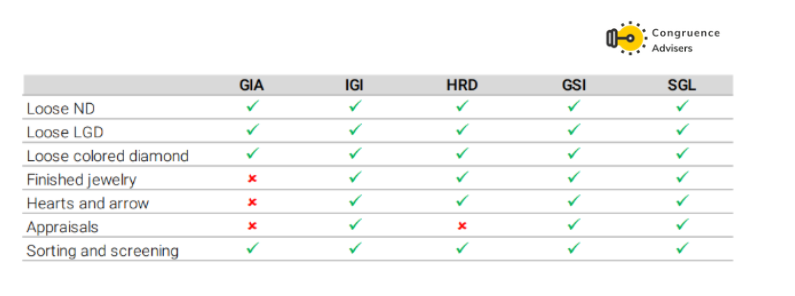

The competitive landscape for gemological certification, as defined by the Redseer Report, comprises players with an Indian presence and global reach across at least 5 countries are GIA (Gemological Institute of America), GSI (Gemological Science International), HRD Antwerp (Hoge Raad Voor Diamant), SGL (Solitaire Gemmological Laboratories).

GIA is a non-profit institution, and no other peer in this universe is publicly listed, making International Gemological Institute Ltd a unique pure-play listed proxy for the gemological certification industry globally.

Across core certification categories, International Gemological Institute Ltd offers the broadest service portfolio among all peers (Exhibit 25). While all 5 players cover the standard categories. International Gemological Institute Ltd is one of only two players (alongside GSI and SGL) to offer finished jewellery certification, a category where GIA is notably absent. The breadth of offerings positions International Gemological Institute Ltd to capture a wider share of wallet across the diamond and jewellery value chain compared to more narrowly and lower scale focused peers.

While GIA remains the undisputed gold standard in natural diamond certification, a position built over nine decades since its founding in 1931. Its approach to the lab grown diamond segment has been hesitant and inconsistent. GIA first began accepting lab grown diamonds for grading only in 2006, a full year after International Gemological Institute Ltd had already pioneered LGD certification in 2005. Even then, GIA’s commitment to the segment remained lukewarm. As recently as 2019, GIA was still only including standard colour, clarity, and cut grading scales on LGD reports for reference purposes only, without grading lab grown diamonds the same way it did natural stones.

In a significant policy reversal, GIA announced it would stop grading lab-grown diamonds using the colour and clarity scale it uses for natural diamonds, replacing detailed grades with just two broad classifications “Premium” and “Standard”.

This created a vacuum that International Gemological Institute Ltd moved decisively to fill. With 65% global LGD market share, International Gemological Institute Ltd is the direct beneficiary of GIA’s reluctance to fully embrace the fastest-growing segment in the diamond industry. GIA’s latest move to further downgrade LGD grading standards effectively cedes this battleground to International Gemological Institute Ltd, which further proves this competitive dynamic that is unlikely to reverse in the near term.

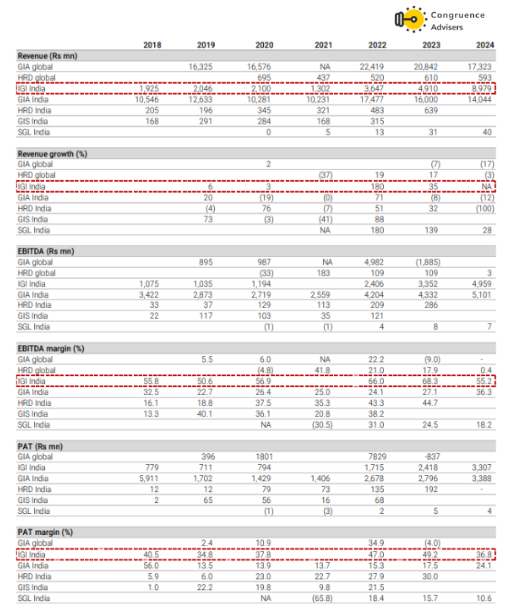

Source – Kotak, Notes: (1) Kindly note that the GIA global, HRD global and IGIL reporting are as of December, hence FY(N)=CY(N-1), (2) IGIL financials prior to FY2024 indicates standalone numbers.

A cross sectional read of the peer financials tells a clear story, International Gemological Institute Ltd is not just growing faster, it is structurally more profitable than every comparable peer. While GIA India leads on absolute revenue scale, its margin profile is significantly weaker. HRD, despite being a globally recognised name, has struggled to generate consistent profitability, with negligible EBITDA and PAT across most years in this period. GSI and SGL remain subscale in comparison.

Among all peers in this universe, International Gemological Institute Ltd is the only player that combines scale, growth, and margin quality simultaneously thus making it the standout player in the global certification industry.

Why You Should Consider Investing in International Gemological Institute Ltd ?

Global & Domestic Market Leadership with High Entry Barriers – International Gemological Institute Ltd is the world’s second largest independent gemological certification body, holding a 33% global market share across diamonds, coloured stones, and studded jewellery. Its domestic positioning is even stronger in India, which cuts and polishes approximately 95% of the world’s diamonds, International Gemological Institute Ltd is the undisputed leader with a 50% market share, with 9 of the top 10 jewellery chains in the country as clients.

The certification industry is structurally protected by high entry barriers, brand trust built over decades, deep specialised expertise, and significant capital investment in advanced grading equipment making it extremely difficult for new entrants to meaningfully challenge incumbents. International Gemological Institute Ltd’s twin moats of global scale and domestic dominance make it a near-irreplaceable node in the diamond supply chain.

Dominant Position in the Fastest Growing Segment Lab Grown Diamonds – The LGD market is the fastest-growing category in the global jewellery industry, expanding at a CAGR of ~19%. International Gemological Institute Ltd has been at the forefront of this shift; it pioneered LGD certification globally in 2005 and today commands a 65% global market share in LGD certification, a dominant position that is significantly ahead of any competitor.

To cement this leadership, International Gemological Institute Ltd has deployed an innovative in-factory laboratory model, embedding grading operations directly within LGD manufacturers facilities. This reduces turnaround times, deepens supply chain integration, and raises switching costs creating structural stickiness with high-volume LGD producers.

Exceptional Unit Economic with Inherent Operating Leverage – International Gemological Institute Ltd operates one of the most profitable business models in the listed Indian market. The business model is inherently asset light and scalable i.e once laboratory infrastructure is in place, incremental certification volumes flow through at minimal marginal cost which leads to strong operating leverage. This is evidenced by the standalone Indian entity achieving EBITDA margins of 75% in CY25 among the highest of any listed company in India. The company is also net cash positive with zero debt.

Education as a Strategic Growth Engine – International Gemological Institute Ltd operates 18 International Gemological Institute Schools of Gemology worldwide, giving it the largest educational footprint among its peers. These schools serve a highly strategic dual purpose: they create a captive talent pipeline of skilled gemologists for International Gemological Institute Ltd ’s own laboratories, and they educate consumers and industry professionals, which builds profound brand trust and acts as a direct precursor to increased demand for International Gemological Institute Ltd’s.

What are the Risks of Investing in International Gemological Institute Ltd?

Investors need to keep the following risks in mind if they choose to invest into this business. Risks needs to be weighed in combination with the advantages listed above to arrive at a decision that is optimal for your portfolio construct

Terminal value risk due to LGD Price Deflation – Lab grown diamond retail prices fell approximately 37% between 2020 and 2023, driven by rapid capacity additions, primarily out of China. While lower prices broaden consumer accessibility and may sustain volume growth, continued price deflation risks commoditising LGDs which potentially compress International Gemological Institute Ltd’s ARP per report as clients push back on certification fees. In an extreme scenario, sustained LGD price erosion could challenge the long-term terminal value of International Gemological Institute Ltd’s dominant LGD certification franchise.

Intense Competition in an Oligopolistic Market – While the certification industry’s oligopolistic structure is broadly a barrier to entry, it also means International Gemological Institute Ltd competes against a small number of well-resourced, globally recognised players like GIA, HRD, GSI, and SGL. Competitive risks manifest in several forms like Price undercutting, Faster turnaround times, Technological disruption, etc.

GIA, in particular, carries unparalleled global brand equity in the natural diamond segment. Any aggressive pricing or market share strategy would warrant close monitoring.

Geopolitical Supply Disruptions – International sanctions restricting the import of Russian rough diamonds, Russia accounts for roughly 30% of global rough diamond supply and have already created supply chain volatility. Any escalation or broadening of such restrictions could dampen rough diamond availability which will lead to reduced cutting and polishing activity in India and can directly compress International Gemological Institute Ltd’s certification volumes.

Absence of Insurance Coverage for Grading Claims – Another risk in International Gemological Institute Ltd’s business model is its lack of insurance coverage against claims arising from certification errors or grading disputes. Unlike many professional services firms that carry errors and omissions (E&O) insurance, International Gemological Institute Ltd bears direct financial exposure if a customer or end consumer successfully pursues legal action over an incorrect or disputed grading outcome.

Given the high unit values involved in diamond and jewellery certification, even a small number of successful claims could result in material financial damages. As IGIL’s certification volumes scale particularly in high-value natural diamond and jewellery segments this uninsured tail risk becomes increasingly significant. The reputational damage from a high-profile grading dispute, irrespective of its financial quantum, could also be disproportionately damaging for a business whose entire franchise is built on trust and accuracy.

Counterfeiting and Forgery – There is a constant threat of third parties forging International Gemological Institute Ltd certificates, tampering with reports, or creating counterfeit laser inscriptions. If the company fails to detect advanced synthetic stones or prevent forgeries, it could devalue the trust associated with genuine International Gemological Institute Ltd certifications

Global Integration Challenges – A major portion of the IPO proceeds is used to fund the acquisition of IGI Belgium and IGI Netherlands to unify the global brand. Meaningful time has already elapsed since the acquisition, yet a visible acceleration in the performance of these subsidiaries is yet to fully materialise

It is also worth recalling that the fresh issue proceeds used for this acquisition flowed directly back to Blackstone as the seller meaning public investors funded the promoter’s exit from these assets.

International Gemological Institute Ltd Future Outlook

International Gemological Institute Ltd management anticipates extremely strong tailwinds over the next few years i.e projecting for 15-20% CAGR over the next 5 years. The primary growth engine is the explosion of LGD jewellery retail i.e showrooms in India alone have crossed 1,000 outlets backed by LGD manufacturers planning to double production capacity over the next three years from Q1CY26 which will directly translate into higher certification volumes. On pricing, following a one-time correction in early 2024, ARP has stabilised in the ₹900-950 range and management does not anticipate structural changes.

Globally, International Gemological Institute Ltd is executing its “One IGI” strategy, with particular focus on rebuilding the US market through a fresh leadership team. On the product side, International Gemological Institute Ltd is deliberately deepening penetration in natural diamonds and coloured stones to broaden its revenue mix beyond LGD. Overarching all of this is a major brand investment cycle, the “IGI: Trust, Certified” campaign launched in January 2025 targeting both trade and consumers through initiatives including co-sponsorship of the Women’s World Cup.

International Gemological Institute Ltd is one of the superior businesses operating at the intersection of two powerful trends i.e the globalisation of diamond certification standards and the rapid mainstreaming of lab-grown diamonds. Its combination of market leadership, asset-light economics, excellent return ratios, and a net cash balance sheet is rare in the Indian listed universe, and management’s 15-20% CAGR guidance appears credible given the volume tailwinds from LGD capacity additions and retail expansion.

That said, investors should be clear-eyed about the risks. International Gemological Institute Ltd’s certification volumes are derived from demand which is entirely contingent on the health of the broader diamond market. Among all the risks we have highlighted are real, even if currently manageable given International Gemological Institute Ltd’s structural advantages. Of these, the most critical risk to monitor in the near term is LGD price commoditisation, as it directly threatens both volume growth and ARP. Investors should track quarterly ARP trends and LGD retail pricing data as leading indicators of this risk crystallising.

On balance, International Gemological Institute Ltd represents a high-quality compounding business but one where valuation discipline and ongoing risk monitoring remain essential.

International Gemological Institute Ltd Technical Analysis

We consider technical analysis to be a useful input in taking medium-term investment decisions. Many a time price action tends to lead to fundamental developments; this is too important an aspect to be ignored by retail investors who do not have access to management outside of common forums like investor calls & AGM.

At Congruence Advisers we like to consider both the long-term weekly chart and the daily chart to arrive at a view on price action. Combined with our understanding of fundamentals, we usually end up being better placed to be able to judge both the business cycle and the stock cycle. Playing the stock cycle right is extremely important for investors looking to extract significant alpha over the medium term.

International Gemological Institute Ltd Price charts

On a Daily Chart, International Gemological Institute Ltd’s performance since its IPO has been characterized by a sharp initial rally to the ₹610-₹650 range followed by a significant, year-long corrective phase. The chart structure has been range bound and choppy for the most part, especially since the July 2025 breakdown. It is interesting to note that the all-time low of ~290 has been tested in February 2026 after the first instance in the tariff shock of April 2025. The price trend over the past 6 months indicates that the tide could slowly turn, now that valuation multiple has turned reasonable in the 25-26x TTM PE range.

The price has been sustaining above the 50DMA for 3 months now with two instances of price rejection from the 200DMA. The price trend is approaching a key pivot level, once the price breaks out above the shaded parallel horizontal range, good numbers might provide the much needed momentum to the price trend.

Revenue growth sustaining above the 20% YoY mark for a couple of more quarters could signify a change in the market view of this business, given the fundamental strengths we have already highlighted.

International Gemmological Institute Ltd Latest Latest Result, News and Updates

International Gemmological Institute Ltd Quarterly Results

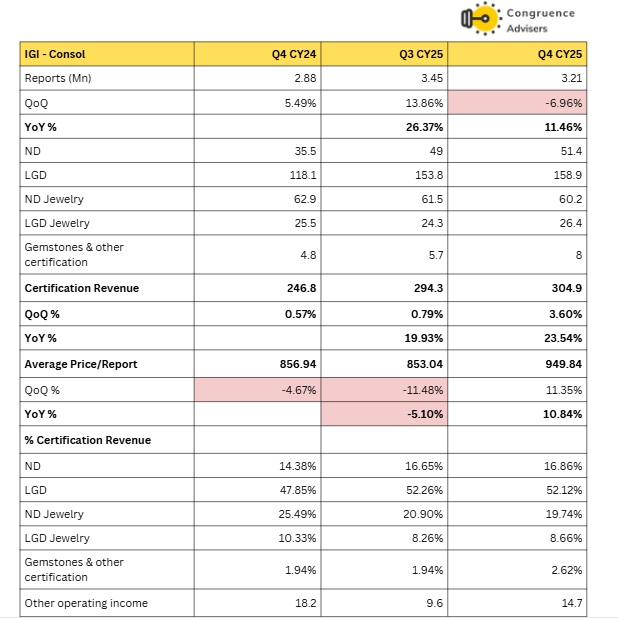

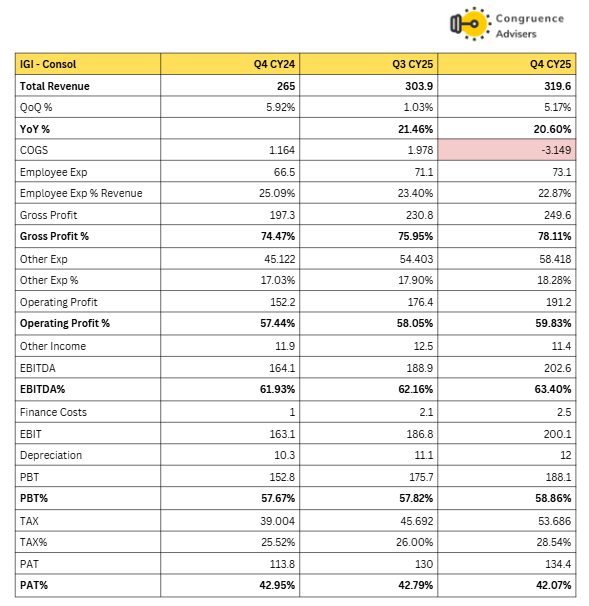

International Gemological Institute Ltd delivered a strong quarter, with total revenue from operations growing 21% YoY to ₹319.7 Cr led by a 23% YoY rise in certification revenues to ₹304.9 Cr. Volume growth remained healthy, with the company issuing 3.21 million reports during the quarter i.e up 11% YoY from 2.88 million in Q4CY24.

The revenue outperformance was primarily driven by a favourable shift in product mix toward premium segments. The ND loose stone segment surged 45% YoY, while the LGD loose stone segment grew 35% YoY, both significantly ahead of overall volume growth, reflecting strong underlying demand and International Gemological Institute Ltd’s pricing power in higher-value certification categories. This mix improvement translated into an 11% YoY expansion in ARP from ₹859 to ₹950.

On profitability, the quarter was exceptional. EBITDA grew 26% YoY to ₹191.3 Cr, with margins expanding to 59.9% due to operating leverage in International Gemological Institute Ltd’s asset-light business model. PAT rose 18% YoY to ₹134.6 Cr, yielding a PAT% of 42.1%.

The Q4CY25 print was strong across all operating metrics i.e volume, realization, and margins with the quarter’s outperformance driven by a combination of premium mix tailwinds, operating leverage, and robust Indian operations.

Importantly, the strong Q4 outturn enabled International Gemological Institute Ltd to exceed its full year 2025 financial guidance issued at the start of the year

Final Thoughts on International Gemmological Institute Ltd

One does not find too many businesses that offer this combination –

- Market leadership in a sunrise sector like LGD

- Oligopoly industry structure across the world

- Revenue growth < 15% p.a. over the medium term

- PAT margin > 40% that appears sustainable

- Asset light business model with with no debt on the balance sheet

The positives are obvious, so is the prospect of a moat that has stood the test of time so far. Given that the LGD store opening pace is picking up in India across so many brands, one can be hopeful of the retail side of the business picking up traction as the newer brands may have the SKU’s but they do not possess the trust that a proven brand like Tanishq has. More the number of LGD players who are fiercely competing in the Indian market, better the prospects for a certification player like International Gemmological Institute Ltd.

The wholesale certification side of the business should continue to do well, in fact this will remain the primary determinant of numbers over the next 2-3 years. While there is an obvious moat here, further fall in LGD prices could impact realization for the International Gemmological Institute.

For the time being we would classify this business into the category of “Interesting & worth tracking till get a clean handle on all factors”. We keenly look forward to the quarterly results over the next 2-3 quarters and watch if the business can continue to deliver 20% YoY revenue growth. The critical thing to assess in such businesses, especially those who are majorly owned by a large PE player is the market view once the remaining large blocks come to the market. We have seen a few instances of PE players consistently selling stakes in their listed businesses depending on when they want to return capital to their shareholders in the fund.

This business has many ingredients that we like to see in our stocks, but it is time to take a nuanced view in the case of businesses where the track record as a listed company is < 2 years.

Disclaimer – This note is part of a business research & analysis series on small companies, there is no BUY/SELL recommendation or target price issued as part of this to a general audience. There is no assurance that this stock makes for a good investment, there is no guarantee that this stock will continue/be included in the coverage universe of Congruence Advisers. The note contains some forward-looking statements and insights drawn from the historical results, annual reports and investor presentations; they are to be viewed only within this context and not as a prediction of future performance of the business or the stock covered.

While due care has been taken to ensure that the information here is as accurate as possible, Congruence Advisers disclaims any liability in case of any unintentional inaccuracies.

The content does not constitute investment advice.