We want consistency and we love predictability.

The world however does not care about our preferences, our need for linearity is rarely satisfied. What appears to be more common is the step function.

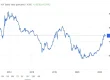

Financial markets work this way. If you had missed 2014, 2017 and 2020 in the Indian equity market, your return through the decade of 2010-2020 would have been miniscule. This trend works over longer horizons too. If you had missed the best 25 days in the US stock market since 1990, your return wouldn’t have beaten fixed income returns.

The expectation of linear progression and predictability is what hurts most investors in the market. You can go 3-4 years with very average returns, then comes along one good year that changes the numbers for the better. If you aren’t patient enough to hold out till that good year comes along, equity markets won’t do much for you.

Investing can sometimes feel like…

Consistency in the intensity and the quality of the effort we put into anything is important. The rewards however are rarely linear, they accrue over time but come in bunches. Systematic investments don’t necessarily result in systematic returns.

This can be the case across other aspects of life too

- Entrepreneurs slog it out for years of minimal payoff until they hit pay dirt. Suddenly their net worth is north of a million dollars, all it takes is one investor to see the potential in the business

- As an employee you turn up every day for work and give it your best shot, you consistently meet your numbers too. But until you get beyond a threshold career level, your personal P&L does not see too much of an improvement

- You’ve dated someone for 5 years and then tie the knot. You get to know more about the person over the next 3 months than you have over the past 5 years

Even your lifestyle changes are a step function, assuming you are disciplined enough to stay within your means. Once you cross beyond the next threshold, it is a different ballgame.

How people internally react to their affluent status is something I have always found fascinating. My observation as a wealth manager has been that the ranges of net worth form a step function that impacts your spending pattern and your satisfaction level. This is backed by my personal experience of having interacted with people across these categories and analyzing how they go about viewing life and taking decisions. Nothing very scientific about this, though this is observably true often.

Here is how I would broadly slot these ranges

2 Cr to 5 Cr

5 Cr to 10 Cr

10 Cr to 25 Cr

25 Cr to 50 Cr

50 Cr to 100 Cr

100 Cr to 500 Cr

500 Cr to 5000 Cr

5000 Cr and beyond

What do I mean by this?

When you move within the bounds of any specific range, not much about your lifestyle or your satisfaction level will change. For e.g. 2 Cr to 4 Cr is a 100% increase in net worth, but it will not give you any great incremental sense of accomplishment or satisfaction. Similarly, when one moves from 25 Cr to 40 Cr, the absolute jump in net worth is a whopping 15 Cr, but life does not feel very different.

However, when one makes the jump to the next category you can see a spike in the lifestyle decisions one takes. You can see people making higher discretionary spends when they move from 5 Cr to 6 Cr, you don’t see them changing their discretionary spends too much when they move from 2 Cr to 3 Cr.

Once one gets past a net worth of 50 Cr, the complexity involved in managing one’s assets sees a spike. From this point on there are multiple properties, multiple businesses, and cross border aspects to be managed. Complexity follows an exponential curve beyond this point.

Beyond a net worth of 500 Cr the challenges are mostly on the personal front, not so much on the financial front. Imagine having a son who at 18 knows he makes more from the annual return on the portfolio he will eventually inherit than the does the average Indian CEO from salary. How do you motivate him to pursue excellence at anything when the incentives just aren’t enticing enough? This is where one starts to worry about the value system of the family breaking down. This is the segment that is most interested in estate planning mechanisms like family governance structure, trust formation and putting in qualification conditions for the next generation to fulfil if they are to enjoy their inheritance.

There is every possibility that a person who starts from the scratch and builds up to a net worth of 20 Cr will have a higher satisfaction level than someone who was born with 500 Cr and works up to 1000 Cr. Absolute level of net worth does matter to the world, but internal satisfaction levels depend on the delta that one is able to experience.

The trajectory and direction matter a lot. When do you think you will feel happier? When you start with zilch and end at 15 Cr, or when you start with 60 Cr and end at 50 Cr? In the second situation your house might be bigger and your car maybe swankier, but you will never wake up feeling good about yourself.

More the number of step functions you can experience in life and higher the frequency of these step functions, the higher your satisfaction level is likely to be. No wonder organizations have a long tail of designations and career levels. This is an artificial way of creating step jumps that employees can regularly experience and feel better about themselves. They game their employees into experiencing periodic progress while keeping them hooked to the necessity of a regular salary.

Investing can provide the much-needed step jump to your net worth over a decade or so when done right, assuming you have your career progression and lifestyle already optimized. That it is also a passive way of doing so is the icing on the cake.