Goodluck India Ltd (formerly, Goodluck Steel Tubes Ltd) manufactures sheets, pipes, engineering structures, fabricated structures, forgings, and automobile tubes. Goodluck India Ltd, incorporated in 1986, has 5 manufacturing facilities in Sikanderabad (Uttar Pradesh) and 1 in Kutch (Gujarat), with a total installed capacity of more than 450,000 tonnes per annum.

We believe Goodluck India Ltd. presents an interesting investment opportunity. Goodluck India Ltd. is expected to deliver 15-20% volume growth with improving EBITDA margins over the next 2-3 years. Goodluck India Ltd has grown its volume by over 20% in the last 3 years, driven by a shift towards value-added products. The recent foray into the defense and aerospace sector, along with the ramp-up of its new hydraulic tube plant, offers significant growth potential.

Goodluck India Ltd Company Summary

Goodluck India Ltd was incorporated in 1986 by Mr. Mahesh Chandra Garg, IIT Alumni & who has worked overseas with MNC and came back to India and started business in 1987 as there was an opportunity for making pipes and got publicly listed on the stock exchanges in 1995. At the time, there was a huge demand for irrigation pipes due to a shortage of water supply. Goodluck India Ltd was initially started as a manufacturer of ERW tubes, which were at that time a value-added product and in demand. Gradually, over a period of time, ERW tubes became commoditized products and soon the management realized this was not a business with technical barriers. Hence Goodluck India Ltd, owing to its engineering background, started entering into other business segments and extended into value-added segments. The business now has offerings across CR sheet and pipes, Precision pipes and auto tubes, Forging, and Engineering structure & fabrication. Originally named Goodluck Steel Tubes to capture a diversified product profile, it changed its name to Goodluck India Ltd in 2016.

Goodluck India Ltd has a total capacity of 450,000 MTPA as of 30 September 2024, out of which 235,000 MTPA capacity is for high-margin value-added products and 215,000 MTPA for high-volume products spread across plants in 2 states (Uttar Pradesh & Gujarat). Goodluck India Ltd caters to 600+ customers (100+ Countries of exports) and has an employee base of 4000+ employees.

Goodluck India Ltd Journey

Goodluck India Ltd has 37+ years of industry presence with a demonstrated track record of innovation & engineering.

Goodluck India Ltd Management Details

Goodluck India Ltd. is led by first-generation entrepreneur Mr. Mahesh Chandra Garg (an alumnus of IIT Roorkee) and supported by three generations of family members, all professionally qualified. Other family members involved include Ramesh Chandra Garg, his brother, who serves as the Whole-Time Director and is an engineer from ISM Dhanbad; his son Manish Garg, Chief Operating Officer and IIT engineer; and Umesh Garg, his nephew, the senior management executive with a B.Tech from IIT Delhi and an MS from London. Mr. Nitin Garg, another family member, holds the position of Executive Director and an MBA from Narsee Monjee Institute of Management. The Garg family plays a significant role in Goodluck India Ltd’s operations. The remaining departments are managed by a team of qualified professionals.

Goodluck India Ltd – Industry Overview

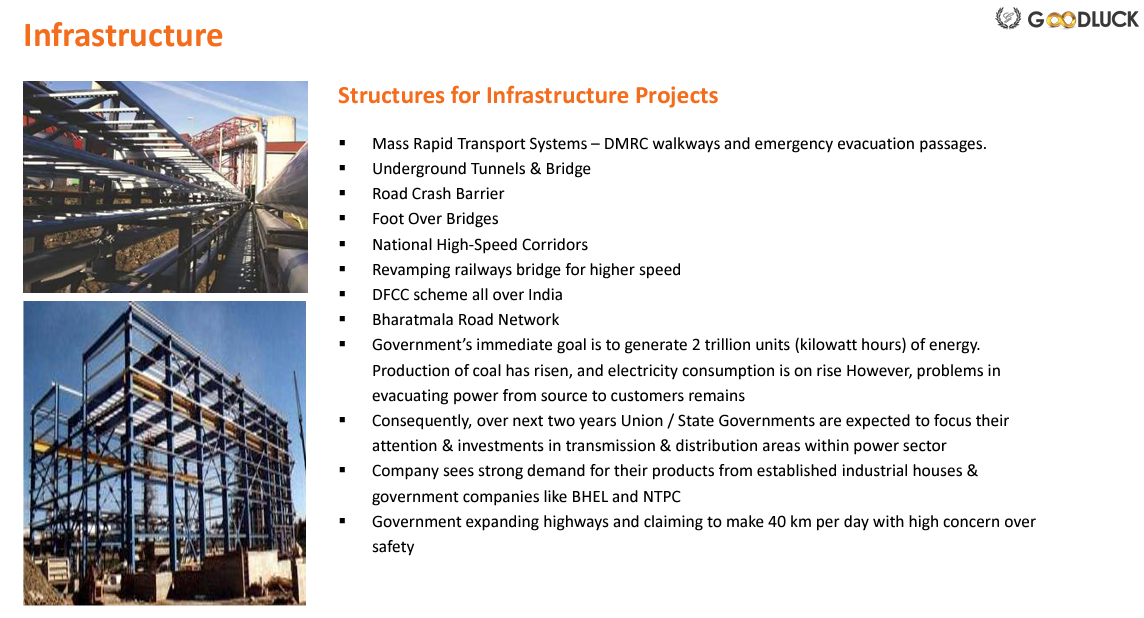

The Indian government is significantly increasing infrastructure spending, with a 10% hike to Rs. 12.21 lakh crore, led by strong tax collections. This supports initiatives like Gati Shakti, Jal Jeevan Mission and ambitious projects such as providing 2 crore houses, installing rooftop solar panels on 1 crore homes, and allocating Rs. 2.6 lakh crore for railway development, including four high-speed corridors. Defense expenditure is on the rise, including a boost in defense exports. Upcoming projects like three new bullet trains, the remodeling of 100 railway stations, and the Amrit Bharat Scheme are creating a wave of development across sectors like auto, defense, and infrastructure, positioning Goodluck India well for substantial growth within the thriving Indian economy.

Goodluck India Ltd Business Segments

Goodluck India Ltd business is divided into 4 main segments :

- CR sheet and Pipes

- Precision Pipes and Auto tubes

- Forging

- Engineering structure and Precision Fabrication

Engineering structures and Precision Fabrication – Goodluck India Ltd designs and constructs critical components and fabricates structures like Railway, road, Bridges and Girders, Structures for Roads & Highways, Primary & Secondary Structures for Boilers & Turbine Generators, Launching Girders for Steel & Concrete Girders Building Structures, Technology Structures, Solar Structures.

Goodluck India Ltd designs, manufactures, and fabricates the structure and provides it to the EPC client. Erection work is done by the EPC player, or in some cases Goodluck India Ltd also does the erection work. Goodluck India Ltd is a category 1 supplier for large EPC players. Margins in this division vary depending on the subsector. Transmission line structures have lower margins, while solar structures and bridge structures have higher margins. Blended EBITDA margins in this division range from 9-10%, and the Current capacity of this division is 85000 MT as of H1FY25. Normally, Goodluck India Ltd does not take working capital risk because 70% of the bridge parties give the material, and the raw material is basically a special grade of plates that are purchased from the Steel Authority, JSPL, and JSW, and those plates are fabricated and painted, and supplied to the site.

Goodluck India Ltd has been making fabricated structures for the bullet train project under a joint workshop of L&T, IHI Japan, and Goodluck at Bhuj. In this contract, L&T is giving the raw material and working capital risk and Goodluck India Ltd is only fabricating and supplying, While erection has been done by some other agency, Goodluck India Ltd has an order for 22,000 MT of fabricated structures for the bullet train project. As of November 2024, 65% of this order has been produced with the remaining portion expected to be completed within the next 8 to 12 months.

Goodluck India Ltd is also producing structures for bus bodies. This is a growing area of focus due to the Indian government’s urban renewal program, which mandates the replacement of hard diesel buses with electric vehicles. Goodluck India Ltd has established relationships with major bus manufacturers, such as Ashok Leyland, SMN, and others, who will be key consumers of these structures.

Some marquee clients that Goodluck India Ltd caters in Engineering structures and Precision Fabrication division are Indian Railways, ABB, L&T, Reliance Industries, GMR, ISGEC, Sterling & Wilson, Alstom, NTPC, Power Grid, Toshiba, TRF, EIL, NPCIL, MHSR.

End User Industries – Roads & Highways, Railways, Boiler and Turbine Generators, Telecom, Steel & Concrete Girders, Building Structure, Solar Energy

New Areas of Growth and Drivers for Engineering Structures and Precision Fabrication Division

Special Formwork for Elevated corridors

Special Formwork for Tunnel Boring Machine for High-Speed Rail

Station Buildings for High-Speed Bullet Train

Super Critical Bridges for High-Speed Bullet Train

Smart City Structures

Car Port and Solar Parks — Design Engineering & Supply.

Architectural Structures in Wire-drawn Bridges

Forging – Goodluck India Ltd started this segment in 2006 by commissioning its first forging plant at Dadri (Uttar Pradesh). Forging served as an essential component for a wide range of industries, including oil & gas, automotive, general industrial equipment, marine, aerospace, and defense sectors. Goodluck India Ltd’s specialization lies in manufacturing steel, duplex, carbon, alloy steel forgings, and flanges across over 100 grades. Moreover, Goodluck India Ltd is a trusted supplier to esteemed programs of DRDO, contributing materials to prestigious initiatives like BrahMos.

Products – Forged flanges, Gear rings, Gear shanks, Forged shafts, Blind & tube sheets, Socket welding flanges, Slip on flanges and Defence products & Aerospace parts.

Open and Close Die machines – forgings ranging from 300 kgs to 7000 kgs. Current Capacity of forging one single piece -14,000 Kgs with total capacity of 30,000 MT per annum

End User Industries are Aerospace, Defence, Automobile Construction & Earth Moving Equipment Nuclear Power Oil & Gas Petrochemical Fertiliser General Engineering

Marquee Clients in Forging division are DRDO, SRO, HAL, GE Oil & Gas Allied Group, Saint-Gobain, BPCL, Indian Oil, BHEL, RIL, L&T

EBITDA margins in Forging division range from 13-15%

Goodluck India Ltd is focusing on the production of stainless steel, duplex, carbon and alloy steel forgings and flanges. This strategic direction aims to enhance its manufacturing capabilities and provide comprehensive end to end solutions to its clients.

Precision pipes and Auto tubes – Goodluck India Ltd started this segment in 2007 by commissioning the first plant for ERW/CDW Precision Tubes at Sikandrabad, UP

Goodluck India Ltd manufactures CDW Tubes, ERW Tubes, Engineering Tubes, and Boiler Tubes for Aerospace, Defence, Automobile & Railways, Construction & Earth Moving Equipment Fertilisers, General Engineering, Heat Exchanger Nuclear Power Oil & Gas and Petrochemical, Pressure Vessels, Thermal Power Valves and Wind Energy.

Goodluck India Ltd is the preferred category II vendor, and they supply to OEMs like Volkswagen, Audi, BMW, Mercedes, Skoda, and Renault. In India, they are supplying Honda, Maruti, Tata, and M&M.

60% of revenue from Precision pipes and Auto tubes is from exports, and this segment generates around EBIDTA% of 12-14% and capacity as of H1FY25 at 120000/MT p.a. Goodluck India Ltd manufactures a proprietary product and holds an approved supplier status with its buyers. This ensures that customers must source directly from Goodluck India Ltd, providing a strong competitive edge and protecting its margins. Goodluck India Ltd has recently commissioned a plant to manufacture large-diameter heavy walls and thicker pipe for making hydraulic tubes (to be used in the construction industry) in the month of September which is one of the very few plants in the world and commercial production has started on 1 Jan 2025. The facility has been installed with an investment of 200 crore in the capacity of 15,000 MT.

The decision to expand into hydraulic tubes is led by strong global demand and consistent inquiries; with applications in the construction industry, the hydraulic tube market faces a global shortage and in India too. Goodluck India Ltd’s hydraulic tube plant is among the first of its kind in India within this product range and will primarily focus on exports. Goodluck India Ltd has already secured a marketing agreement with a reputed firm covering Europe, Canada, and Mexico. 1st year capacity utilization will be less, around 50%, and is expected to increase to 70-80%. At peak, this new plant is expected to generate 500-600 Cr revenue, and EBITDA% will be in the ranges of 12-13%

Goodluck India Ltd caters to a diverse range of industries, including aerospace, automobile, construction equipment, defence, earth-moving equipment, fertilizers, general engineering, heat exchangers, nuclear power, oil and gas, petrochemical, pressure vessels, railways, thermal power, valves, and wind energy.

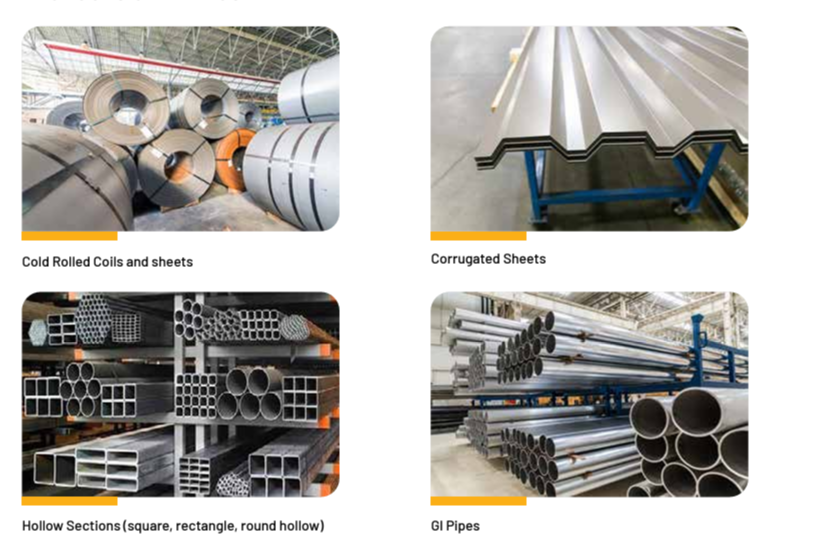

CR coils, pipes and tubes – Goodluck India Ltd manufactures a wide range of commodity products like Cold Rolled Coils and Sheets, Corrugated Sheets, Hollow Sections (square, rectangle, round hollow) and Galvanized Pipes. These products are used in railways, road bridges, and other support structures. Clients in this segment are Public & Private sector OEMs, Central Govt & State Govt. This is the high volume and lowest margin segment for Goodluck India Ltd., Generating EBITDA% of around 2.5-3% and Rs 2,500-3,000/MT.

The business has been operating for the past 30 years, producing a low-margin, consistent-volume product. This line is maintained primarily to serve long-standing, committed customers who continue to rely on the company for their requirements.

Management is focusing on increasing the margin by converting GI lines to produce Solar tracker tubes where margins are 7500-8000/MT vs GI segment at 2500/MT, which is expected to drive EBITDA per ton of this segment from 2,500-3,000/MT to over Rs 5,000/MT. Solar is expanding everywhere, and Goodluck India Ltd is supplying hardware steel products and steel boundary structures and also exporting them. The demand in these transmission tubes was earlier 50 tons per megawatt, but now it has reduced to almost 14 to 17 tons per megawatt.

Goodluck India Ltd is also actively pursuing opportunities in the road safety sector, focusing on the production of cost-effective crash barriers based on European designs. The company has secured partnerships, and is aligning with government initiatives to ensure substantial demand and growth in this sector. The total capacity for this segment is 215,000 MT p.a. As of H1FY25, this segment accounted for 37% of revenue in FY24.

Goodluck India Ltd’s clientele includes a mix of public sector and private sector OEMs, along with various central and state government entities at both national and international levels.

Goodluck Defense and Aerospace Limited

Goodluck India Ltd has established a subsidiary, Goodluck Defense and Aerospace Limited, to manufacture specialized parts for the artillery and aerospace sectors. Goodluck Defense it’s a dedicated project for ammunition and for the shells of ammunition.

Initially, the plant was scheduled for commissioning in Q4 2026. Due to excellent progress the timeline has been advanced, the plant is now expected to be operational by the end of FY25. Goodluck India Ltd plans to manufacture 155 mm gun shells, a product with robust demand and high inquiries. Goodluck India Ltd believes the commissioning of this plant will be a game-changer.

The global defense landscape has recently undergone significant standardization, with the 155 mm shell emerging as the primary size used worldwide. Over the last two, then geopolitical tensions, including conflicts like the Ukraine war, the Israel-Hamas crisis, and concerns over China-Taiwan relations. Countries that previously lacked sufficient ammunition stocks or defense capabilities are now actively increasing their purchases. The Indian government has significantly increased its defense procurement. For instance, this year alone, the government has ordered 2.5 lakh shells from an Indian company. This demand surge is expected to further bolster the prospects for Goodluck India’s new venture.

The defense sector is known for its long gestation periods, and it takes time to establish relationships and secure contracts. Goodluck India Ltd is focusing on limited products initially. While these are restricted and licensed products, Goodluck India Ltd is also exploring opportunities in defense exports, although these are restricted items and require government assistance.

Goodluck India Ltd has invested 200 Cr capex, and this can generate 300 Cr revenue at peak utilization with 20%+ EBITDA

Defence Business

Currently, the defence business contributes a small percentage (around 2-3%) to Goodluck India Ltd revenue, In next 3-4 years management is aiming for 10%

Right now, From current setup Goodluck India Ltd is working with DRDO, HAL Projects, like Brahmos missile by making small forging parts for these projects catering through Forging division. While new setup Goodluck Defense and Aerospace Limited is for a particular product, which will be ammunition part

Regular & value added product mix

Goodluck India Ltd defines value-added products as those with an EBITDA margin of 10% or more. Goodluck India Ltd has strategically shifted its focus from high-volume commodity-type products with lower margins towards these value-added higher-margin products over the last several years. Going forward, management intends to increase the proportion of value-added products to 75%.

Exports

Goodluck India Ltd exports its products to 100 countries. While 85% of exports are from the developed markets of Europe, America, and Australia. Goodluck India Ltd wants to growth exports higher than domestic

Goodluck India Ltd faced some disruptions in exports during FY23 & FY24 due to geopolitical tensions and issues with sea routes. However, Goodluck India Ltd’s primary offerings cater to the automotive sector and general engineering projects, which are essential products. Despite muted economic conditions, the management sees no decline in demand and remains confident about continued growth and new products primarily targeted for the export market.

As per management, no new geographies are required right now for expansion as Goodluck India Ltd is already supplying to 100 countries, and Goodluck India Ltd focuses on reshuffling markets based on demand.

Good Luck India Ltd Orderbook

For the infrastructure business, Good Luck India Ltd holds an order book covering nearly 9 to 10 months. In the forging segment, the order book is for 3 to 4 months. In the auto tubes segment, orders are received on a weekly program basis, providing consistent visibility into demand. While the exact monthly order book cannot always be defined

Industry Served

Goodluck India Ltd offers a versatile range of products and services tailored for multiple industries which includes Infrastructure, High Speed Railways, Aerospace, Defense, Automotive, Oil & Gas, and Renewables.

Goodluck India Ltd Manufacturing Plants

Goodluck India Ltd has 6 state-of-the-art manufacturing facilities, of which 4 are located at Sikandrabad and 1 is in Dadri in Uttar Pradesh, and 1 in Kutch, Gujarat. The structures for special steel bridges for the Bullet Train project are being supplied from the Kutch plant.

Goodluck India Ltd Current Capacity

Goodluck India Ltd’s current capacity utilization is around 89% as of H1FY25 vs. 93% in FY24 & 87% in FY23.

Going by the management guidance of 15-20% volume growth on FY24 volume of 3,83,795 MT, the volume would be reaching around 4,40,000 MT by the end of FY25. Further capex will be required for the next phase of growth. As per management, plans are ready and will be announced shortly. Management has said capex will be a brownfield project and no acquisitions are on the radar.

Goodluck India Ltd Financial Performance

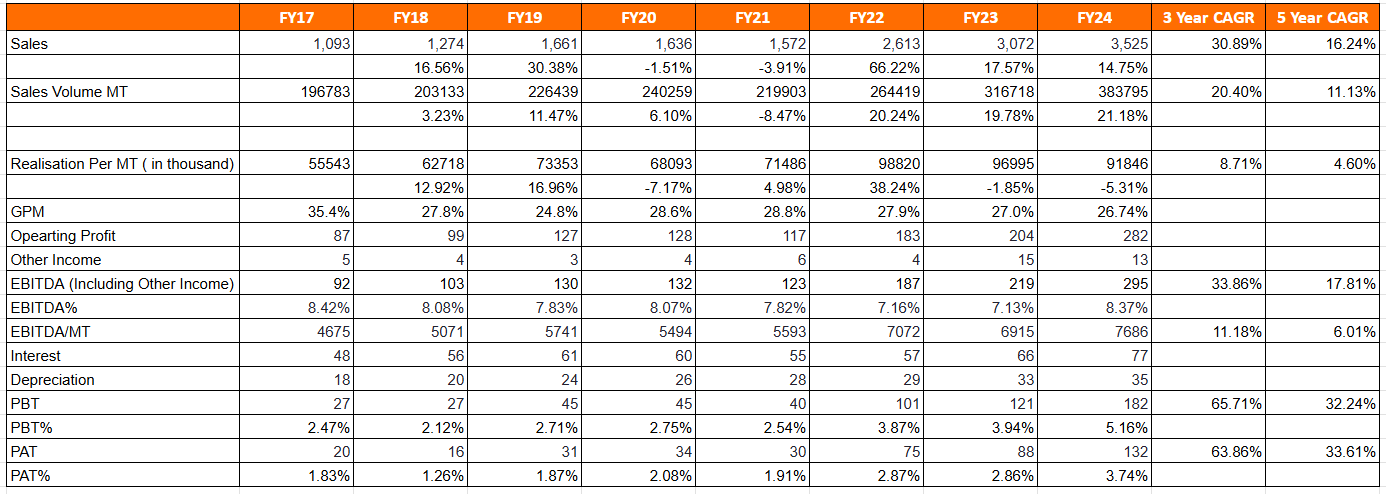

Goodluck India Ltd has posted 3-year & 5-year sales CAGR of 30% & 16%; Growth is mostly driven by volume growth of 20% and 11%. Both Realisation per MT and EBITDA per MT have increased from 55543/MT & 4675/MT in FY17 to 91846/MT & 7700/MT in FY24. The proportion of value-added products has increased over time. Goodluck India Ltd has posted the highest PBT% & PAT% in FY24.

Goodluck India Ltd Debt & Cashflow

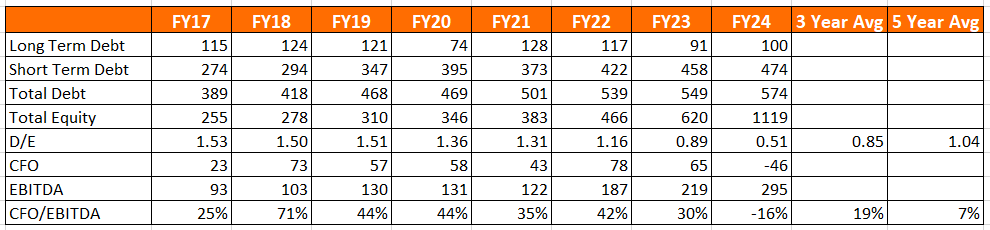

Out of the total debt of 574 Cr in FY24, 474 Cr is short-term debt, which is mainly for working capital. Debt/Equity has decreased to 0.51x in FY24 from 0.89x in FY23, mainly due to higher equity as Goodluck India Ltd has raised 200 Cr QIP in Jan24. CFO/EBITDA has been lower due to high working capital requirements.

In our assessment, high working capital intensity is keeping operating cash flow generation limited which forces the business to borrow funds to meet working capital requirements. At a working capital cycle of more than 100 days, ~30% of incremental revenue gets added to the gross debt every year. Debt to Equity ratio has trended above 1x for this reason until FY23. While the QIP of 2024 has helped bring down the Debt to Equity ratio to ~0.6x, it would be more preferable for the business to reduce debt by organic means over the medium term.

The business may have challenges in funding both capex and working capital needs through internal accruals, necessitating more equity dilution in the future unless the margin profile or the working capital profile improves. With the business model skewed in favor of large B2B customers, improvement in working capital will not be easy to come by.

Goodluck India Ltd Asset turn, Working capital & Return ratio

Working capital days are around 95 days in FY24 and Gross assets turns are lower at 4.8 vs 5.3 in FY23 lower due to ongoing capex. (Already started commercial production on Jan 25). FY24 ROE is lower due to a recent fund raised of 200 Cr by QIP & FY24 ROCE is at 15.46%.

Goodluck India Ltd Comparative Analysis

To understand Goodluck India Ltd investment potential, we have conducted a comprehensive analysis. This analysis includes comparing Goodluck India Ltd to its competitors (peer comparison) on various fundamental parameters and Goodluck India Ltd share performance relative to relevant benchmark and sector indices.

Goodluck India Ltd Peer Comparison

Goodluck India Ltd operates in multiple segments, and the competitive landscape varies significantly across each one.

In the Engineering structure and Precision Fabrication segment closest listed peer for Goodluck India Ltd is Salasar Techno Engineering Ltd, which has a manufacturing capacity of 211,000 MTPA, While Goodluck India Ltd has a manufacturing capacity of 85,000 MTPA, and the margin profiles are similar for both companies, around 9-10%.

In the Precision Pipes and Auto tubes segment, the closest listed peer for Goodluck India Ltd is Tube Investments of India Ltd. Goodluck India Ltd margins are slightly higher as Tube Investments has a broader range of products that impacts their average margins.

In the Forging segment, the closest listed peer for Goodluck India Ltd is Bharat Forge Ltd, with a capacity of 773,910 MTPA. Goodluck India Ltd has a manufacturing capacity of 30000 MTPA, and Bharat Forge Ltd has a superior profitability profile due to its scale of operations.

While CR sheet and Pipes is a commodity product and has a fragmented market

Tube Investments of India Ltd and Bharat Forge Ltd have much higher scale than other players. All the players have posted 27%+ 3 Years Sales CAGR, EBITDA & PAT CAGR have been higher than Sales CAGR. Goodluck India Ltd and Salasar Techno Engineering Ltd have poor CFO/EBITDA conversion. Tube Investments of India Ltd has the highest return ratios.

Goodluck India Ltd Index Comparison

Goodluck India Ltd share performance vs S&P BSE Small cap Index as the index benchmark comparison is a fundamental tool for understanding the investment potential and making informed decisions in the context of the broader market

Goodluck India Ltd Corporate Governance

Board Composition – The Board consists of 8 Directors, 4 of whom are Non-Executive Independent Directors. 2 of whom are Woman Directors. The Board comprises renowned professionals drawn from diverse fields.

Audit & Remuneration Committee – Although an independent director chairs both the audit committee and remuneration committee, it also includes Promoter Mr. Mahesh Chandra Garg as a member; in general, having a fully independent audit & remuneration committee is seen as a better corporate governance practice.

KMP Remuneration – Remuneration paid to KMP & Relatives of KMP for FY24 is around ₹10 Cr, i.e. increase of 45% over FY23 & is 7.6% of FY24 Net Profit.

Related party – Advance Given to promoter entity Excellent Fincap Pvt. Ltd. is 39.55 Cr and trade receivables are at 13.45 Cr as of 31 March 2024

Contingent Liabilities – Contingent Liabilities related to Central Excise & Commercial Tax U.P and disputed demand under the Income Tax Act is at 1.20 Cr, which is minimal.

Dividend Payout – Goodluck India Ltd has been paying dividends for the last 3 years, and Dividend Payout for FY24 is 14% net profit

Why You Should Consider Investing in Goodluck India Ltd?

Goodluck India Ltd offers some compelling reasons to track closely and consider investing.

Consistent Growth – Goodluck India Ltd has delivered volume growth of 20% CAGR and sales growth of 30% CAGR in the last 3 years. Management is guiding for 15-20% volume growth along with EBITDA% improvement for the next few years. This guidance does not factor in the revenue potential from the new defense and aerospace plant.

Focusing on Value-Added Products – Goodluck India Ltd has, over the years, successfully diversified from high-volume products to value-added products; all the incremental capex has been towards value-added products. Going forward, Goodluck India Ltd plans to increase the contribution from value-added products.

Experienced Management: Goodluck India Ltd is led by first-generation Mr. Mahesh Chandra Garg (an IIT Roorkee alumni) & supported by three generations of family members – all professionally qualified with a long history in the industry.

Defense and Aerospace foray – Goodluck India Ltd has Incorporated a wholly-owned subsidiary, Goodluck Defence and Aerospace Limited, to strengthen its presence in the defence sector exclusively. The new plant is expected to be commissioned by March 2025. At peak utilization, Goodluck Defence and Aerospace Limited can generate revenue of 300-350 Cr with EBITDA% of 20%

New capex utilization – Goodluck India Ltd has recently started commercial production from its newly commissioned plant of hydraulic tubes (300 Cr capex), and this is expected to generate peak revenue of 500-600 Cr at peak utilization with EBITDA% of 12-13%.

New Product launches & Exports – Goodluck India Ltd is focusing on exports, particularly to developed countries, as exports have a higher realization also. Goodluck India Ltd is focusing on newer products like solar tubes, road safety etc, for these products have higher realization than commodity products.

What are the Risks of Investing in Goodluck India Ltd ?

Investors need to keep the following risks in mind if they choose to invest into this business. Risks need to be weighed in combination with the advantages listed above to arrive at a decision that is optimal for your portfolio construct.

Volatility in RM prices – Prices of raw materials such as steel are linked to commodity markets and thus subject to fluctuation. Goodluck India Ltd has passed the increase in the cost of raw materials with a lag to domestic customers except to those companies that bid through tenders such as railways, government, and the public sector. So, any volatility in raw material prices can impact profitability and cashflows.

Higher Competition – Goodluck India Ltd’s high volume business, i.e., CR sheet and pipes (accounting for 40% in H1FY25), is a commodity product and has a fragmented market, which causes margin pressure due to pricing fluctuations and higher competition.

Expansion Risks – Goodluck India Ltd is expanding into defense and aerospace, Which offer huge growth potential but can also pose risks if not executed effectively, as manufacturing defense-related products requires several licenses and approvals.

Geopolitical & Exports Risk – Exports account for around 30% of Goodluck India Ltd sales, and in the past, Global geopolitical tensions have disrupted exports; global geopolitical tensions and headwinds can disrupt export activities and slow down demand. Changes in trade policies can also impact export growth.

Slowdown in economic & infrastructure spending – A general downturn in global economic conditions, a decrease in Indian demand, and a Slowdown in government infrastructure spending (infra accounts for 60% of revenue) can affect the performance of Goodluck India Ltd.

Currency Volatility: Fluctuations in currency exchange rates can significantly impact export margins of Goodluck India Ltd

Insufficient cash flow generation: In our assessment, the business will need substantial investments in both fixed assets and working capital to keep up an aggressive growth rate of 20% p.a. Given the track record of operating cash flow generation, it is unlikely that all of these growth needs can be met through internal accruals. While the current environment is conducive for QIP, the market may see equity dilution in an unfavorable manner in other market conditions.

Goodluck India Ltd Future Outlook

Goodluck India Ltd Aiming for the product portfolio mix to have more Value Added Engineered Products by upgrading regular products/product expansion with domestic/international tie-ups/know-how/agreements.

Management is guiding for 15-20% growth for the next 2-3 years. FY25 growth will be impacted by slower H1FY25 due to heavy monsoons & elections while exports are being impacted by geopolitics and the US election. Management is expecting stronger H2FY25 with 15-20% growth, but FY25 Blended growth may end at a lower band. i.e., 4000 Cr revenue by FY25 and 4600 Cr by FY26 without the new Aerospace and Defence plant.

Aerospace and Defence capex is expected to generate revenue by next FY, and at the peak, they can contribute around 300 Cr with 20%+ EBITDA%. Execution needs to be tracked closely. If executed properly can lead to further improvement in consolidated margins to 10%+. One will need to watch the working capital cycle of this new vertical; though margins are likely to be higher than other lines, a longer working capital cycle may not move the needle on capital efficiency.

Management is aiming to become a billion-dollar company in the next 3-4 years which we view as a very optimistic situation.

Goodluck India Ltd Technical Analysis

We consider technical analysis to be a useful input in taking medium-term investment decisions. Many a time price action tends to lead to fundamental developments; this is too important an aspect to be ignored by retail investors who do not have access to management outside of common forums like investor calls & AGM.

At Congruence Advisers we like to consider both the long-term weekly chart and the daily chart to arrive at a view on price action. Combined with our understanding of fundamentals, we usually end up being better placed to be able to judge both the business cycle and the stock cycle. Playing the stock cycle right is extremely important for investors looking to extract significant alpha over the medium term.

Goodluck India Ltd Price charts

The day chart is largely inconclusive in our opinion and indicates a meandering trend that is looking out for fresh triggers. Special attention needs to be paid to the large volume support breakout of August 2024 that doesn’t show any major changes in the shareholding pattern nor is backed by any substantial corporate announcement. The price trend has been listless since then with a lack of buying force as the broader market conditions have taken a turn for the worse.

Defending the trend line in the short term will be crucial as the 50 DMA is on the verge of breaking below the 200 DMA from above.

On the weekly chart, the pattern suggests a gently sloping uptrend at play since July 2021 which started with the biggest volume spike we have seen in 5 years. The current level is testing the lower bound of the parallel channel and presents an interesting juncture in our opinion. The management has recently announced the commencement of manufacturing of hydraulic tubes at the UP plant, Q4 results should indicate the initial views of the management on the new growth initiatives.

Both the daily and the weekly chart indicate a key support level getting tested right now. A conclusive break below this may indicate some more downside before stability resumes. If the support level holds through this correction, it can give more conviction to investors about the fruits of the new growth engines.

Goodluck India Ltd Latest Latest Result, News and Updates

Goodluck India Ltd Quarterly Results

Q2FY25 has been impacted by heavy monsoon all over the country, Indian elections, Exports has been also impacted by geopolitics and US election but still Goodluck India Ltd posted a decent revenue growth for both QoQ & YoY, The growth was driven by operational efficiency, EBITDA growth is driven by cost optimization measures and increased operational efficiencies.

Volume for H1FY25 at 200489/MT vs 183256/MT in H1FY24

H1FY25 Business mix at Engineering structure and fabrication at 21%, CR sheet and pipes at 40%, Precision pipes and auto tubes at 24% and Forging 15%

Final thoughts on Goodluck India Ltd

The steel converter and processing industry is a tough one to operate in. Rarely will one see a player who is able to grow at a healthy rate at good unit economics and ROCE > 25%. In this regard, APL Apollo Tubes continues to be an exception where healthy growth at high ROCE appears possible for some more years. For all the other businesses, they have to grapple with volatile margins and below average ROCE during most years.

While the product portfolio is good and differentiated compared to commodity steel processors, this hasn’t yet resulted in any increase in gross margins for the business. The bulk of the bottom line improvement appears to be emerging from better absorption of depreciation and interest cost. Gross margin and operating margin have been steady, though realization and EBITDA per MT have shown a marked improvement over the past few years. Better margin over the next 2-3 years is an important trigger to watch for as this can change the capital efficiency of the business for better. We believe that it will not be easy for a B2B business model that sells to large EPC players and automotive players to substantially improve the working capital cycle. Hence better cash flow and capital efficiency is more likely to result from improvement in the margin profile of the business.

While the newer business lines are expected to deliver higher margin, it remains to be seen if the aerospace & defence vertical will operate at a more elongated working capital cycle compared to the current level of ~100 days. One of the big doubts we have is on the ability of the business to invest both into fixed assets and working capital to be able to deliver 15%+ growth. If the operating cash flow generation doesn’t improve, the business might have to keep raising equity capital to keep the growth engine going. At a capacity utilization of more than 85%, operating leverage is unlikely to lend a helping hand any more.

The best businesses are those who can deliver above average growth over a long period of time without needing additional capital. While we do like the product portfolio of Goodluck India Ltd, we need more evidence that the business can fund growth without increasing debt perennially or having to resort to further equity dilution. QIP’s may happen easily in the current environment but the institutional investor community doesn’t like frequent equity dilution unless the stock in trade itself is money, like a lending business.

A few things will need to fall into place for this business to get into a self reinforcing virtuous cycle where better margins and capital efficiency can reduce dent and improve unit economics further, all the while growing at a healthy rate.

Definitely a business worth keeping an eye on in the meanwhile.

Disclaimer – This note is part of a business research & analysis series on small companies, there is no BUY/SELL recommendation or target price issued as part of this. There is no assurance that this stock makes for a good investment, there is no guarantee that this stock will be included in the coverage universe of Congruence Advisers. The note contains some forward-looking statements and insights drawn from the historical results, annual reports and investor presentations; they are to be viewed only within this context and not as a prediction of future performance of the business or the stock covered.

While due care has been taken to ensure that the information here is as accurate as possible, Congruence Advisers disclaims any liability in case of any unintentional inaccuracies.

The content does not constitute investment advice.

Disclosure (Updated as of Dec 31, 2024) – No position in the stock in personal portfolio