Shaily Engineering Plastics Limited is engaged in manufacturing of high precision injection moulded plastic components and sub-assemblies for various requirements of Original Equipment Manufacturers (OEM). It also offers secondary operations in plastics like vacuum metalizing, hot stamping and ultrasonic welding. Shaily Engineering Plastics Limited caters to a wide range of industries including home furnishing, FMCG, pharmaceuticals, switchgear components, auto components, electronics and electrical appliances

We find Shaily Engineering Plastics Ltd. interesting at this point because we consider it to be a global picks-and-shovel play on the theme of GLP-1 medication in the healthcare industry. Shaily Engineering Plastics Ltd. seems to have achieved enough technical competence in precision engineered plastics moulding to embed itself into the global GLP-1 supply chain on the medical devices side. Since the turn of the decade, GLP-1 medications have been touted to be the next big thing in the treatment of widespread chronic diseases such as diabetes and obesity. These medications appear to represent a significant novel breakthrough in treating these prevalent chronic diseases and are thus expected to have blockbuster sales for several years to come.

For an Indian manufacturing company to get plugged into this supply chain at a device level is unique. We believe the market is also viewing Shaily Engineering Plastics Ltd. with the same lens. In addition to the healthcare segment, Shaily Engineering Plastics Ltd. is also targeting interesting optionalities in the industrial and consumer segments, which by themselves can become large business lines.

Shaily Engineering Plastics Ltd Company Summary

Shaily Engineering Plastics Ltd is a small-cap company headquartered in Baroda, Gujarat. Shaily Engineering Plastics Ltd. is one of the world’s largest manufacturers of high-precision injection moulded plastic components. Shaily Engineering Plastics Ltd. manufactures products and components across three key segments – 1. Consumer segment 2. Industrial segment, and 3. Healthcare segment. A bulk of the revenues come from exports (~75%)

Shaily Engineering Plastics Ltd. was founded in 1987 by Mr. Mahendra (Mike) Sanghvi. In 1987, Shaily Engineering Plastics Ltd started as a supplier of precision clock gear components for a Japanese corporation. Over the last 4 decades, Shaily Engineering Plastics Ltd has established itself as a leading global manufacturer of precision-moulded plastic components. Shaily Engineering Plastics Ltd now has globally reputed clients such as IKEA, Gillette, P&G, GE Appliances, Schaeffler, Sanofi, Dr. Reddy’s Labs, Sun Pharma, etc. Shaily Engineering Plastics Ltd. has the ability to manufacture plastic components weighing as low as 0.03 grams and with tolerances of 5 microns.

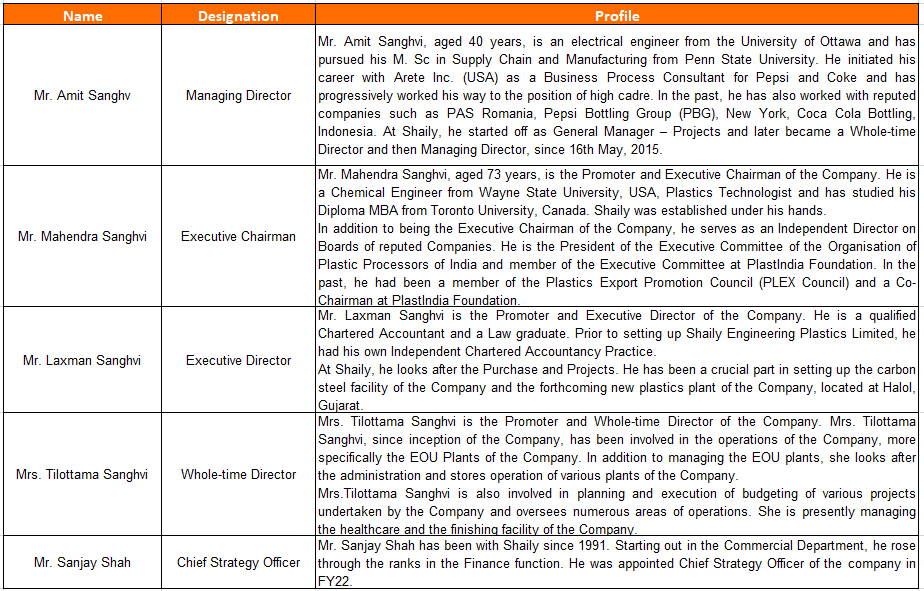

Shaily Engineering Plastics Ltd Management Details

Shaily Engineering Plastics Ltd. was founded in 1987 by Mr. Mahendra (Mike) Sanghvi. His brother, Mr. Laxman Sanghvi, and his wife, Ms. Tilottama Sanghvi, have been part of the executive team for a long time. His son, Mr. Amit Sanghvi, took over as Managing Director in FY15. At present, Mr. Mahendra Sanghvi is the Executive Chairman, while Mr. Amit Sanghvi is the Managing Director.

Shaily Engineering Plastics Ltd – Industry Overview

Engineered plastics

Engineered plastics are a set of specially designed high-performance polymers that are designed to have better thermal, mechanical, electrical, and chemical properties compared to commodity plastic polymers like polyethylene and polypropylene. They have better strength, durability, chemical resistance, and dimensional stability compared to commodity polymers and hence find usage in industrial sectors such as automotive, aerospace, consumer electronics, healthcare, and consumer and industrial goods.

Let’s take a brief look at some of the engineered plastics that Shaily Engineered Plastics Ltd. uses to manufacture its products.

- Polyamides (PA6/PA66/PA12) – Good mechanical strength, dimensional stability and low moisture absorption. Used across industries.

- PES (Polyethersulfone) – High temperature resistance and chemical resistance and flame retardant. Used in medical devices that need repeated usage and autoclaving.

- PPS (Polyphenylene sulfide) – Excellent chemical resistance and high-temperature stability

- PBT (Polybutylene Terephthalate) – Excellent electrical insulation, chemical resistance, and low moisture absorption. Ideal for electrical and automotive use cases

- LCP (Liquid Crystal Polymers) – Extremely high mechanical strength even in thin-walled applications. Used extensively in miniature electronic components.

- PC (Polycarbonate) – High impact resistance and optical clarity. Suitable for transparent applications

- Torlon – Very high thermal and dimensional stability. Considered to be one of the highest-performing thermoplastics in extreme environments.

- PEEK (Polyether-ether-ketone) – Very high thermal stability, good biocompatibility and wear resistance. Often used as a metal replacement due to its high strength.

Most of these engineered plastics are not manufactured in India and have to be imported from countries such as Germany, the USA, Japan, China, and South Korea.

Precision moulded plastic products and components.

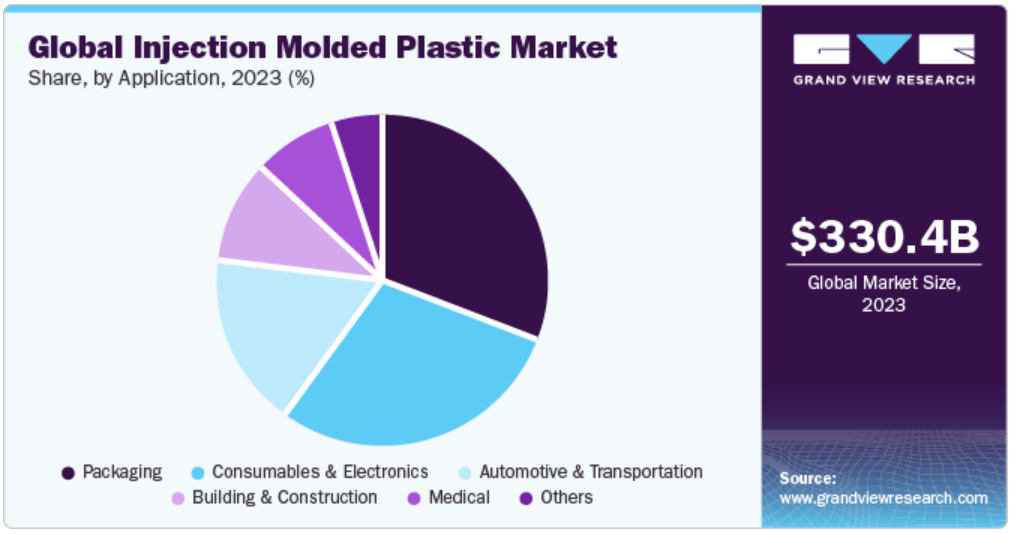

The overall injection moulded plastic industry is estimated to be ~$ 330 bn in size currently and is projected to grow at a 3-4% CAGR over the next decade.

A bulk of the demand (~40%) comes from the Asia-Pacific region.

Packaging, consumer electronics, and automotive are the highest-consuming industries for injection moulded plastic products.

The high-precision injection moulded plastic industry is a subset of the more generic injection moulded plastic industry, where components and products are used for critical and high-performance applications in healthcare, consumer electronics, automotive, industrial, and consumer products. The key differences between the high-precision injection moulded plastics and normal injection moulded plastics are as follows:

- Low tolerances – High precision injection moulded plastics require tolerances as low as 5-25 microns, whereas normal injection moulded plastics can operate at tolerances of 100 microns

- Requires high-performance materials – High-precision injection moulded plastics require engineered plastics that have more consistent properties and higher dimensional stability

- Requires advanced machinery – High-precision injection moulded plastics require advanced machinery to have precise control over temperature, moisture, and speed of injection during the molding process to ensure correct dimensions and precise finishing

- Requires strict quality control – High precision injection moulded plastics require very strict automated and manual quality control and testing procedures

- Requires advanced design and engineering capabilities – High-precision injection moulded plastics require advanced design and engineering capabilities to decide the correct design, choose the right materials for the right use cases, etc.

Some of the global leaders in the high-precision injection moulded plastics industry are companies such as Jabil, Molex, Celanese Corp, Rochling Group, BASF Engineering Plastics, Berry Global Group, Plastikon Industries, B Braun Medical Inc., etc.

The high-precision injection moulded plastic components and products industry is growing much faster than the general plastic industry due to increased adoption in critical use cases across industries such as healthcare, automotive, aerospace, consumer electronics, etc. Competition is limited here compared to the general plastics industry due to the high technical and R&D hurdles.

The GLP-1 and biologics landscape in healthcare

GLP-1 medications are the hottest drugs in the pharmaceutical industry by some distance at the moment. Global GLP-1 medication sales have increased from $0 in 2017 to ~$30-40 bn in 2024. The market is expected to reach $100 bn in the not-so-distant future.

GLP-1 stands for Glucagon-Like-Peptide-1, a naturally occurring hormone that is produced by the intestines of humans in response to food intake. The GLP-1 hormone performs the following functions in the body.

- Increase insulin secretion in the body, which helps to remove sugar from the bloodstream and put it into the cells of the body.

- Inhibit the secretion of glucagon, a hormone that raises blood sugar by releasing stored glucose from the liver into the bloodstream.

- Slow down gastric emptying, i.e.; it increases the time taken to process the food in the stomach before it is passed on to the intestines for absorption in the body. Through this process, it results in a longer-lasting feeling of satiety, thus reducing food intake.

GLP-1 medications aim to mimic the role played by the naturally occurring GLP-1 hormone. By mimicking the actions of the GLP-1 hormone, these medications have opened up a completely new pathway for treating chronic metabolic diseases such as diabetes and obesity. Clinical studies have shown that GLP-1 medications can result in as much as 15-20% weight loss in adults compared to placebo drugs and as much as 1.5-2% reduction in HbA1C (blood sugar) compared to placebo drugs. These results are quite remarkable and have proven to be a completely new breakthrough in the treatment of chronic metabolic diseases such as diabetes and obesity.

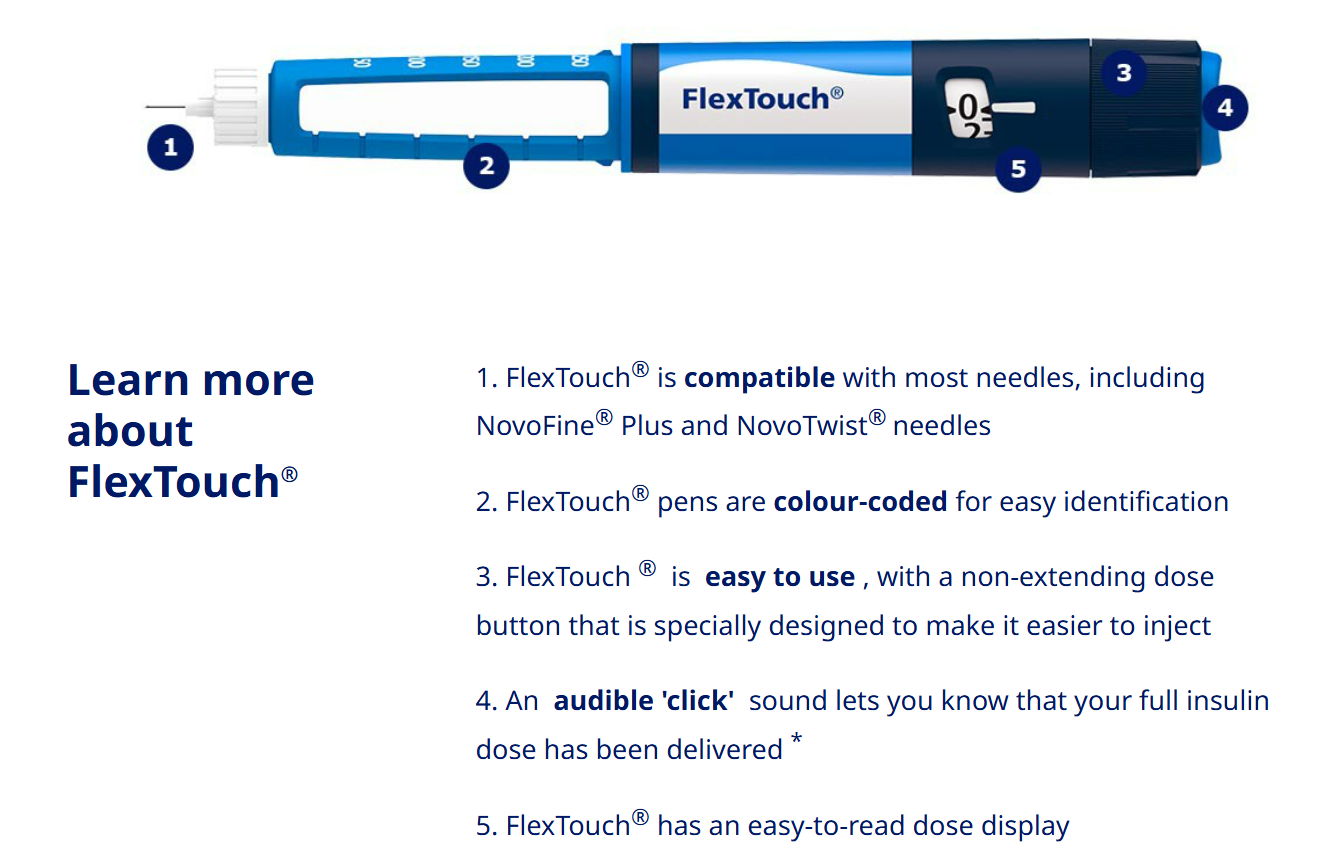

GLP-1 medications are biological drugs as opposed to chemical drugs and hence have a large molecule size. Larger molecules cannot be absorbed by our body effectively via our mouth and stomach and hence need to be directly injected into the bloodstream. Thus, most GLP-1 medications are self-administered by patients using devices called pens and auto-injectors, which inject the medicine directly into the patient’s bloodstream. Medications are usually taken once a week and for patients to see sustained benefit, the medications need to be taken regularly without break. Thus, each patient would be taking 52 doses of GLP-1 injections each year. At present, these medicines are selling at ~$ 300/dose in the USA, so the annual bill per patient could be as high as $15000.

One of Novo Nordisk’s GLP-1 pens called Flextouch

At present almost all GLP-1 drugs are under patent in all geographies. Patents start to lapse in various countries such as Canada, Brazil, Saudi Arabia, China, and India starting in 2026. US patents start lapsing around 2030. There are several generic pharma companies in the world that have filed for generic versions of these medications with the US FDA. Once patents lapse and generic medications are introduced, the price per dose of GLP-1 medications is expected to come down to $100-150 levels per dose. With this price decrease, the no. of patients under coverage is expected to explode. It is expected that the number of patients under GLP-1 coverage will increase from ~2 million at present to ~15 million after the launch of generic versions. It is estimated that approximately 1bn people worldwide are suffering from obesity.

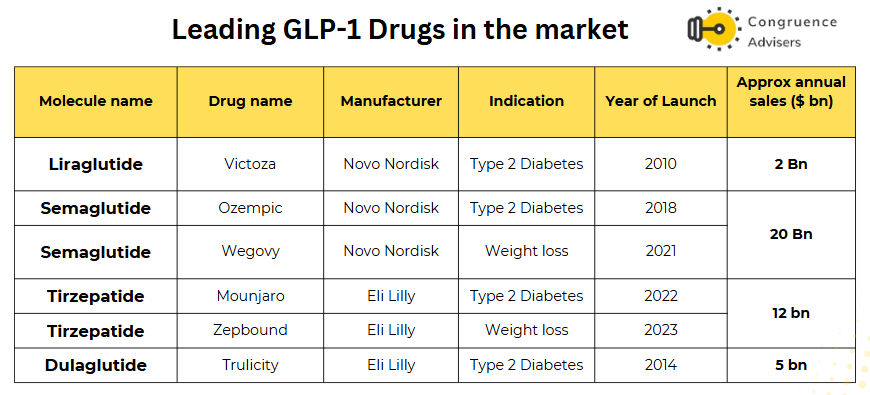

Below is a list of the most popular GLP-1 medications in the market as of today, along with certain additional information about each drug. The list below is not exhaustive but covers the major drugs that have significant market share.

Global GLP-1 Device Manufacturers

As discussed above, GLP-1 drugs are administered using injectable devices such as pens and auto-injectors. Insulin is also administered using similar pens. These pens and auto-injectors are manufactured by a handful of highly precision-engineered plastics companies globally, with Shaily Engineering Plastics Ltd. being one of them. The other leading pen and auto-injector manufacturers globally are

- Ypsomed AG: A Swiss company with a turnover of ~$600 mn

- Becton Dickinson: A US medical devices giant with a turnover of ~$20 bn (Only a fraction of overall revenues pertain to insulin and GLP-1 delivery devices)

- SHL Medical: A Taiwanese company with a turnover of ~$110 mn

Ypsomed seems to be the clear leader in working with innovator GLP-1 companies. For example, Novo Nordisk’s GLP-1 devices are manufactured by Ypsomed. It is estimated that Becton Dickinson is going to be one of the major competitors for Shaily Engineering Plastics Ltd. in winning business from generic GLP-1 manufacturing pharma companies. Not much is known about SHL Medical at this point in time as it is a privately held company, but it also has significant capacities in the pen/auto-injector space.

Shaily Engineering Plastics Ltd Business Segments

Shaily Engineering Plastics Ltd.’s business is organized into 3 segments.

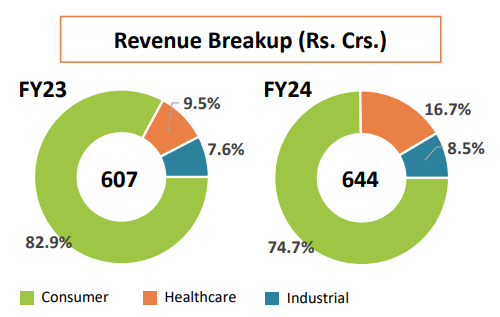

- Consumer segment: This segment contributed ~75% of Shaily Engineering Plastics Ltd.’s total revenues in FY24. A bulk of revenues in this segment come from IKEA. The consumer segment de-grew by ~4.5% YoY in FY24

- Industrial segment: This segment contributed ~8% of Shaily Engineering Plastics Ltd.’s total revenues in FY24. The industrial segment grew by ~19% YoY in FY24.

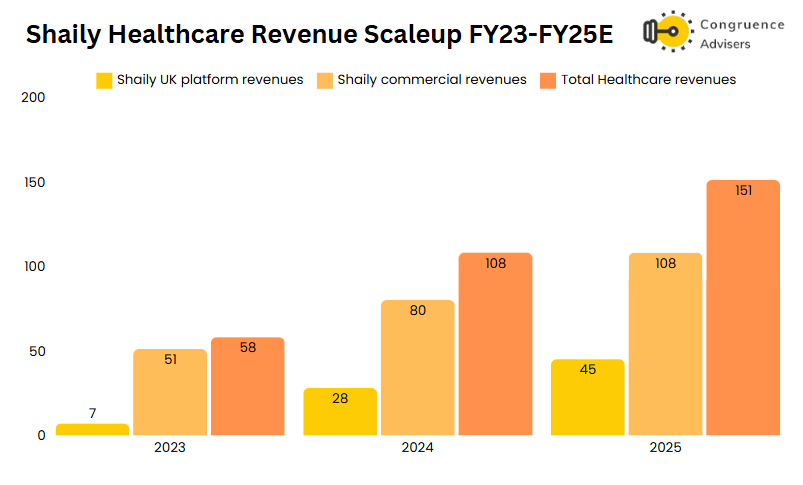

- Healthcare segment: This segment contributed ~17% of Shaily Engineering Plastics Ltd.’s total revenues in FY24. The healthcare segment grew by ~87% YoY in FY24 thanks to a gradual scale-up in its own IP development and commercial revenues across GLP-1 and insulin.

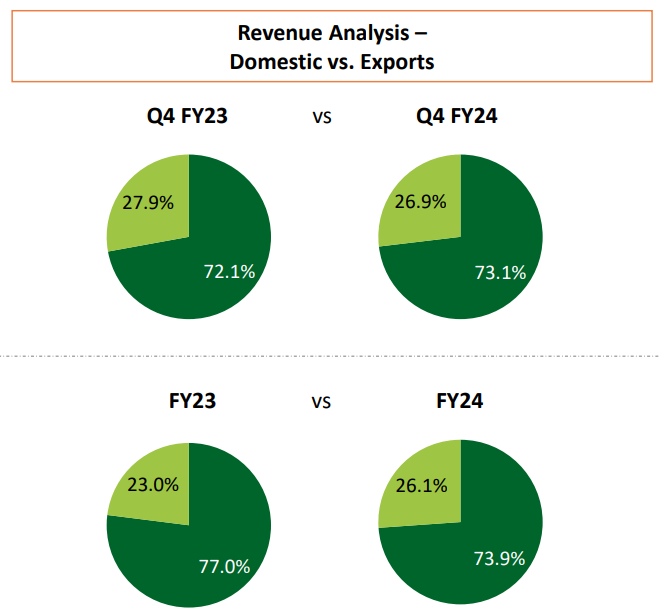

A bulk of Shaily Engineering Plastics Ltd.’s revenues have come from exports over the years. In FY24, ~74% of Shaily Engineering Plastics Ltd.’s revenues came from exports.

Shaily Engineering Plastics Ltd. justifies its high precision tag and differentiates itself from other injection moulded plastic companies due to the following capabilities.

- Ability to work with engineered polymers such as polyamides, polycarbonate, Torlon, PEEK, PES, PBT, Liquid crystal polymers etc. These require special machinery and a differentiated understanding of materials and design.

- Ability to manufacture plastic components weighing as low as 0.03 grams and ability to deliver precision tolerances as low as 5 microns

- Having certifications such as MDSAP (Medical Devices Single Audit Program), ISO 13485:2016 (globally recognized QMS certification for medical devices), and US FDA 21 CFR:820 (set of US FDA guidelines for medical device manufacturers wanting to sell in the USA ) for its healthcare segment

- Having secondary operations capabilities post moulding for a variety of products such as pad printing, hot stamping, painting, screen printing, ultrasonic welding, laser marking, and vacuum metallising.

- Having its own state-of-the-art tool room with advanced CNC machines for manufacturing its own molds for high-precision components

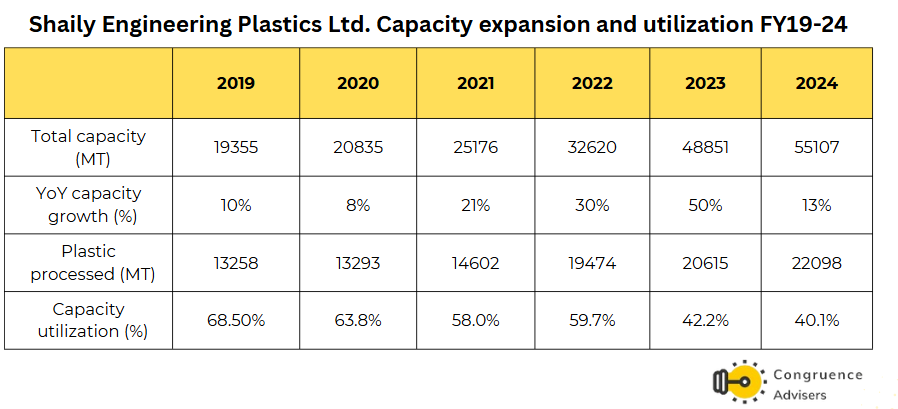

Over the last 6 years, Shaily Engineering Plastics Ltd. has scaled up its plastic processing capacity significantly. However, capacity utilization has slipped significantly as sales volumes haven’t yet caught up with the expanded capacity. It is expected that utilization numbers will improve significantly starting from FY26 as the healthcare segment starts scaling up and the other segments also pick up after a few years of post Covid slowdown. If a swift capacity utilization uptick does not happen in the next 2-3 years, then serious questions would need to be asked about the rationale behind expanding processing capacity by 3x in 6 years.

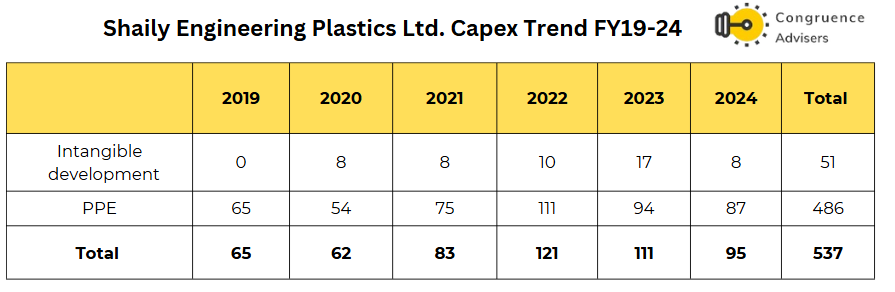

Over the last six years, Shaily Engineering Plastics Ltd. has spent ~INR 540 Cr in capital expenditure. Of this, ~INR 50 Cr has been towards the development of IP and patents for the healthcare business, and the rest has been towards plant property and equipment

Let’s take a quick look at Shaily Engineering Plastics Ltd consumer and industrial segments before taking a deeper look at the healthcare segment

Consumer segment

Shaily Engineering Plastics Ltd. makes plastic products for various consumer products under this segment, such as home furnishings, carbon steel furniture, FMCG packaging, etc. Some of their largest clients in this segment are IKEA, Gillette, HUL, P&G, and Corvi. IKEA and P&G have been multi-decade clients for Shaily.

IKEA is by far the largest client for Shaily in this segment. By virtue of the consumer segment being the largest for Shaily Engineering Plastics Ltd., IKEA is a very critical client for Shaily Engineering Plastics Ltd. Shaily Engineering Plastics Ltd supplies a range of plastic home furnishing products to IKEA globally and claims to have between 30-90% global market share in each of the products it supplies to IKEA.

In FY20, Shaily Engineering Plastics Ltd also ventured into carbon steel furnishing products by setting up an exclusive plant at the behest of IKEA. However, the plant couldn’t scale up as envisaged due to Covid-related delays and the resultant slowdown in customer order offtake. In fact the carbon steel plant has still not broken even in FY24 at the EBITDA level. It is finally expected to do so in FY25. At maximum utilization, the plant can do a revenue of ~INR 120 Cr.

Shaily Engineering Plastics Ltd. also ventured into the toys segment in FY20 and signed on a couple of large global clients. However, the management realized thereafter that the toys segment had little customer stickiness or loyalty and was prone to undercutting from China, leading to sub-par margins. Recognizing this foray as a strategic misstep, Shaily Engineering Plastics Ltd decided to pause fresh investments into the toys business in FY23 and decided to stop the toys business altogether in FY24. An amount of ~INR 25-30 Cr had been invested in creating capacity for the toys segment, which lay unutilized. Shaily Engineering Plastics Ltd has said that it is repurposing the toys’ capacity for use towards other products in the consumer and industrial segments.

Shaily Engineering Plastics Ltd management has hinted in recent calls that they are exploring opportunities in the consumer electronics space. Consumer electronics is a rapidly growing industry and it is a space where many precision injection-moulding companies have a large presence. So, an entry in this segment could lead to exciting possibilities for Shaily Engineering Plastic Ltd

Overall, the consumer segment is a steady growth business with low double-digit growth rates and low double-digit EBITDA margins. It contributed about ~75% of Shaily Engineering Plastic Ltd.’s topline in FY24.

Industrial segment

The industrial segment is the smallest segment for Shaily Engineering Plastics Ltd. It contributed ~8% to Shaily’s FY24 topline. This segment comprises automotive components, appliance components, and high-performance engineering components. Some of the key clients in this segment are GE Appliances, Garrett Advancing Motion (previously part of Honeywell), Schaeffler, MABE, Amvian, etc.

Over the last 4 quarters, Shaily Engineering Plastics Ltd. has received several orders in this segment from automotive and appliance customers. In Q4 FY24, it received an order from a major US appliances manufacturer for global supplies of knobs for its appliances.

The industrial segment is expected to grow in the high teens to early twenties year on year due to the low base.

Healthcare segment

Healthcare is by far the most important and exciting segment for Shaily Engineering Plastics Ltd. from a future growth and margin expansion point of view. This segment contributed ~17% to Shaily’s topline in FY24 and showed a YoY growth of ~87%. Growth in this segment is expected to be very strong for the next few years as generic markets open up for GLP-1 drugs and insulin manufacturing also scales up for Shaily Engineering Plastics Ltd.

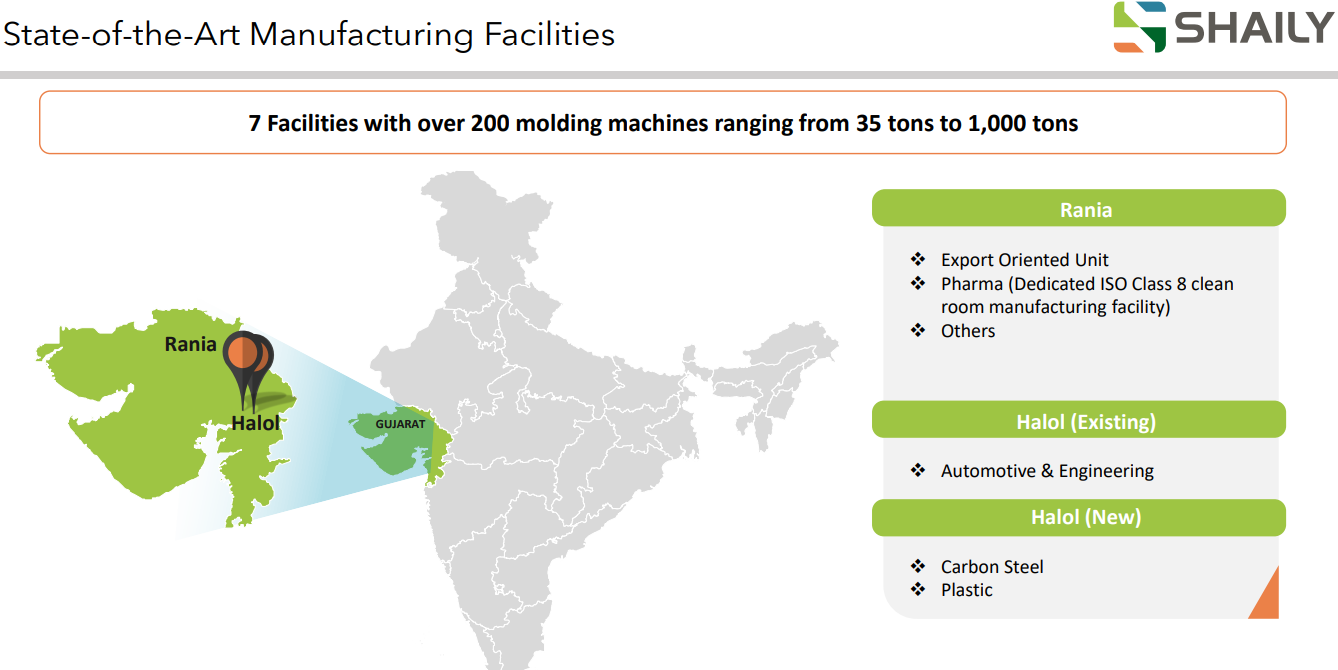

Shaily Engineering Plastics Ltd. started its journey in drug delivery devices way back in 2000. In 2005-06, Shaily Engineering Plastics Ltd successfully designed and developed insulin pens made of 100% plastic for Wockhardt with the help of the famous UK-based product design and development consultancy firm IDC (Industrial Design Consultancy). The IP for this pen was transferred to Wockhardt as per the agreement. Post the success with Wockhardt, they received a contract manufacturing deal from global insulin leader, Sanofi for their Allstar pens. Based on these orders from Wockhardt and Sanofi, Shaily Engineering Plastics Ltd. set up a dedicated unit with an ISO Class 8 clean room in Rania, Gujarat, for manufacturing these devices. However, the IP for these two devices was not with Shaily Engineering Plastics Ltd, and they were pure contract manufacturers.

Over the last few years, Shaily Engineering Plastics Ltd has been working with partners such as IDC and others to develop their own IP pens and auto-injectors for insulin, GLP-1, and other biological drugs such as human growth hormones, peptides, monoclonal antibodies, etc. Shaily Engineering Plastics Ltd efforts bore fruit as it was able to register 7 patents through its UK subsidiary, Shaily UK Ltd.

At present, Shaily Engineering Plastics Ltd has 7 platform devices

- Protean : 0-60 IU insulin reusable/disposable, settable for alternate therapies – triple-dose, and single dose for Peptides

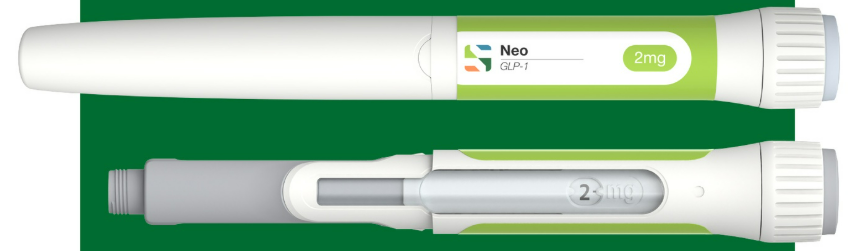

- Neo : Automatic spring driven variable dose and fixed dose pen-injector developed for the delivery of GLP-1

- Toby : A two-step auto-injector for the delivery of Semaglutide (Wegovy)

- Tristan : A three-step auto-injector with an automatic needle insertion for the delivery of Dulaglutide and Terzipetide

- Axiom : HGH (human growth hormone), FSH (follicle stimulating hormone), PTH (parathyroid hormone) and GLP-1 therapies

- Maxim : 0-80 IU insulin reusable/disposable, single dose and multidose alternate therapies

- Mira : Wearable two-step auto injector for subcutaneous or intramuscular injections

With the development of these multiple own-IP pen platforms, the sales of contract manufactured vs. own-IP pens, which used to be 90%:10% a few years back, has already shifted to 70%:30% and is expected to shift to a 50%:50% ratio soon. Eventually, with the scale-up of GLP-1 molecules and own-IP insulin devices, own-IP sales are expected to dwarf contract manufacturing.

Let’s understand the steps involved in commercializing a pen or auto-injector for a pharmaceutical company that is interested in partnering with Shaily Engineering Plastics Ltd for its drug.

- Registration on Shaily’s platform – Once a company is interested in partnering with Shaily Engineering Plastics Ltd for a device for its drug, it has to register as a program partner with Shaily UK Ltd. by paying a platform development fee. This fee goes towards compensating Shaily UK Ltd. towards development, validation and testing of the device for the client’s drugs. The platform development fee is amortized over a period of 12-15 months.

- Supply of exhibit batches by Shaily India – Once validation and testing are completed by Shaily UK, the process flow transfers over to India operations. Shaily India starts supplying exhibit batches to the client which are required for completing filing formalities for the drug. Each exhibit batch consists of ~30000 pen supplies for each strength of the drug. If a drug has 3-4 different strengths, then between 90000-120000 pens are supplied by Shaily Engineering Plastics Ltd to the client as exhibit batches.

- Commercialization – Using the exhibit batches, the client files for approval with the concerned regulatory. The filing contains the name of the device manufacturer, i.e., Shaily Engineering Plastics Ltd. Once the drug-device combination is approved by the regulator, it is very difficult and resource-intensive for the client to change the device supplier. Hence there is huge customer stickiness for Shaily Engineering Plastics Ltd post filing. Once the client receives the regulator’s approval for launching the molecule, Shaily Engineering Plastics Ltd starts supplying commercial batches for end market sales.

At present Shaily Engineering Plastics Ltd. has ~20 different programs ongoing with 20 different pharmaceutical clients for several molecules such as semaglutide (Ozempic), semaglutide (Wegovy), liraglutide (GLP-1), teriparatide (parathyroid hormone used to treat osteoporosis), tirzepatide (GLP-1) and lanreotide (somatostatin analog).

The commercial launch pipeline for Shaily Engineering Plastics Ltd. looks as follows:

- Commercial launch of teriparatide in UK and USA between H2 2024 and early 2025

- Commercial launch of liraglutide in USA and Europe in H2 2025

- Commercial launch of semaglutide (Ozempic) in Canada, Brazil, India and China in late 2025-early 2026

- Exhibit batch supplies ongoing for semaglutide (Wegovy) and tirzepatide NCE-1 filing

In addition to the exciting developments on the GLP-1 front, Shaily Engineering Plastics Ltd. is also expected to experience a significant uptick in demand in its insulin pen sales. Leading global drug delivery device manufacturer and Shaily Engineering Plastics Ltd competitor, Ypsomed AG, has recently said that it intends to focus on developing devices for GLP-1 and other novel biologics and hence plans to vacate the contract manufacturing business for insulin pens. This is expected to bring more global insulin business Shaily Engineering Plastics Ltd way. In Q1 FY25, Shaily Engineering Plastics Ltd. received a 10mn insulin pens order from a global pharmaceutical company which is to be fulfilled within a year.

While Shaily Engineering Plastics Ltd. management is focusing on capturing the generic GLP-1 market initially, they have said in investor conference calls that once their products are visible in regulated markets like USA and Europe, they are confident of getting enquiries from innovator companies and getting a breakthrough there as well.

So, overall, as must be evident from this section, healthcare is a very exciting segment for Shaily Engineering Plastics Ltd at the moment. Margins in this segment will be significantly higher than the margins in the other two segments; hence, as healthcare revenues scale up, the overall Shaily Engineering Plastics Ltd margin and return on capital ratios are both expected to improve significantly.

Shaily UK Ltd

Shaily UK Ltd. is the R&D and innovation arm of Shaily Engineering Plastics Ltd. Established in September 2021, Shaily UK was created to focus on the development of successful products for drug delivery. With four dedicated mechanical and industrial design engineers working alongside Shaily’s Operations Director and Head of Quality Assurance, the team is based in the UK with close affiliation to Shaily Engineering Plastics Ltd in India. All stages of product development, prior to design and manufacturing validation take place in Shaily UK and then the process is transferred to India. Shaily UK also works closely with international design consultancy, IDC, which supports the design process for electronic developments.

In FY24, Shaily UK Ltd. reported a turnover of ~INR 28 Cr, and a PAT of ~INR 21 Cr. Shaily UK Ltd. gets tax credits from the UK Government due to the R&D and innovation it does in the UK, which leads to a lower tax rate for Shaily UK Ltd.

Shaily Engineering Plastics Ltd Manufacturing Facilities

Shaily Engineering Plastics Ltd. has 7 manufacturing facilities located in Gujarat across two locations – Rania and Halol. Of the 7 plants, 6 are for plastic products and 1 is for steel furniture. Shaily Engineering Plastics Ltd. has 200 moulding machines across the 7 facilities with the capacity of each machine ranging from 35 MT to 1000 MT.

Shaily Engineering Plastics Ltd Corporate governance

- Board Composition – The Shaily Engineering Plastics Ltd. board of Directors has nine members in total, with 5 independent Directors. The independent directors have relevant experience across domains such as healthcare, finance, business management, M&A, and HR. The 4 non independent members of the Board are all members of the promoter family.

- Promoter Remuneration – The total remuneration drawn by promoters and their related parties (relatives and enterprises over which promoters exercise control) in the form of salaries and rent amounted to ~INR 9.7Cr in FY24. This amounted to ~17% of the PAT of the company for FY24. For FY23, the corresponding figures were INR 8.2 Cr and ~23% of PAT. As % of PAT, these numbers are quite high. We hope management will bring down their share of remuneration as % of PAT close to 10% levels in the future.

- Related Party Transactions – There were no significant related party transactions for Shaily Engineering Plastics Ltd. in FY24.

- Contingent Liabilities – The total contingent liabilities for Shaily Engineering Plastics Ltd on account of service tax and custom duty claims amount to ~INR 3 Cr, which is less than 1% of Shaily Engineering Plastics Ltd consolidated net worth and hence immaterial.

Shaily Engineering Plastics Ltd Financial Performance

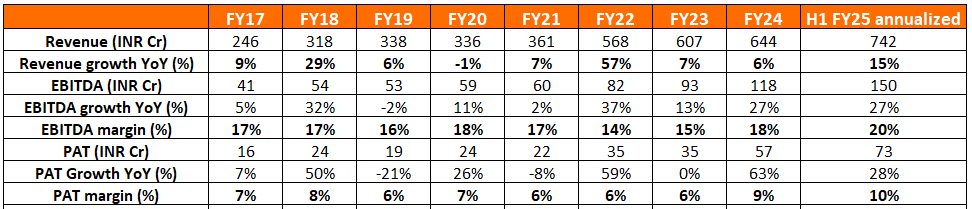

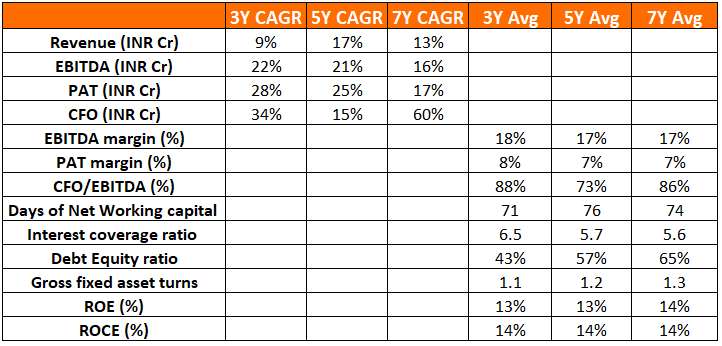

Over the last 7 years, Shaily Engineering Plastics Ltd. has grown revenues at a CAGR of 13%, EBITDA at a CAGR of 16% and PAT at a CAGR of 17%, demonstrating a steady growth trajectory. During this period, EBITDA and PAT margins have also remained quite steady, staying between 15-18% and 6-8% respectively.

*Standalone nos from FY17-FY21 and consolidated nos from FY22 onwards

Shaily Engineering Plastics Ltd Ltd Working capital, Debt and cash flow Analysis

Net working capital days have also been quite steady around the 70-80 day mark. The capital structure has also remained quite steady with interest coverage ratio and debt equity ratio being in comfortable zones throughout.

The one noticeable change over the years has been in the decrease in gross fixed asset turns, which has more than halved from 2.3x in FY17 to 1.1x in FY25. Between FY17-H1 FY25, Shaily Engineering Plastics Ltd. has invested ~INR 600 Cr in tangible and intangible fixed assets. Investments have been made mostly towards the consumer and healthcare segments. Revenues are yet to catch up with the level of assets created, as reflected in the current machine utilization levels of 40%.

*Standalone nos from FY17-FY21 and consolidated nos from FY22 onwards

Shaily Engineering Plastics Ltd Ltd Return Ratios

Decrease in gross fixed asset turns has caused Shaily Engineering Plastics Ltd.’s return ratios to suffer over the years. From an ROCE of 16.5% and an ROE of 19% in FY17, the company had dropped to ROCE and ROE levels of 9.1% and 11.3% respectively in FY23. Over the last 1.5 years however, the return ratios have bounced back strongly as the healthcare division has started scaling up.

*Standalone nos from FY17-FY21 and consolidated nos from FY22 onwards

Shaily Engineering Plastics Ltd. Key metrics CAGR & Averages FY17- H1 FY25 Annualized

Shaily Engineering Plastics Ltd Comparative Analysis

To understand Shaily Engineering Plastics Ltd investment potential, we have conducted a comprehensive analysis. This analysis includes comparing Shaily Engineering Plastics Ltd to its competitors (peer comparison) on various fundamental parameters and Shaily Engineering Plastics Ltd share performance relative to relevant benchmark and sector indices.

Shaily Engineering Plastics Ltd Peer Comparison

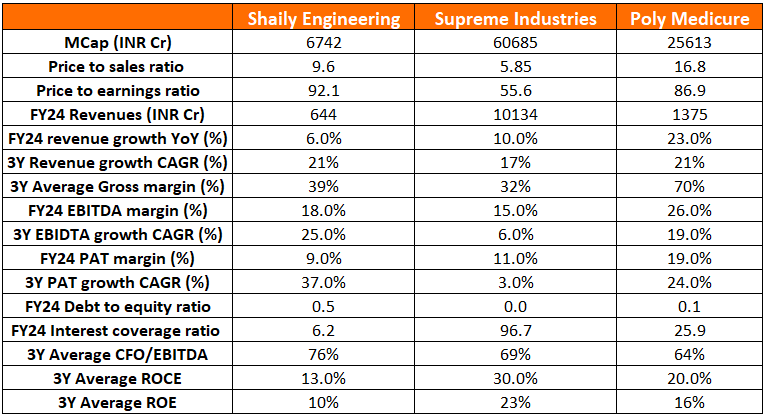

There are no like-for-like companies which can be considered to be an exact peer of Shaily Engineering Plastics Ltd. Since Shaily Engineering Plastics Ltd. is a precision moulded plastics product manufacturer and has a large medical devices business segment, we feel Supreme Industries Ltd. and Poly Medicure Ltd. can be considered as peers for comparison.

As is evident from the table below, Poly Medicure Ltd has the most superior unit economics among the 3 businesses with gross margins in the range of 70% and EBITDA margins in the mid-to-high 20%s.

However, on a capital efficiency basis,Supreme Industries Ltd is head and shoulders above the other two companies, with a 3Y average ROCE and ROE of 30% and 23% respectively. This is due to Supreme Industries’s high net fixed asset turns and extremely low net working capital days.

In comparison to the other two companies, Shaily Engineering Plastics Ltd. lags behind in return on capital metrics. But as we have discussed above, Shaily Engineering Plastics Ltd was going through an investment phase for the last few years. The next few years are expected to see the benefits of those investments in tangible and intangible assets playing out. As that happens, the return on capital metrics for Shaily Engineering Plastics Ltd also should inch up towards 20% levels. In terms of growth and margin expansion, Shaily Engineering Plastics Ltd already seems to be on track.

Shaily Engineering Plastics Ltd Index Comparison

Shaily Engineering Plastics Ltd share performance vs S&P BSE Small cap Index as the index benchmark comparison is a fundamental tool for understanding the investment potential and making informed decisions in the context of the broader market

Why You Should Consider Investing in Shaily Engineering Plastics Ltd

Shaily Engineering Plastics Ltd offers some compelling reasons to track closely and to consider investing if one is looking to play on high-precision injection moulded plastic components and GLP-1 opportunity

Direct play on the booming theme of GLP-1 medications – As discussed earlier, GLP-1 medications are the hottest theme in pharma right now due to their potential for treating chronic epidemics like obesity and diabetes. GLP-1 sales globally have increased from ~$20 bn in 2023 to ~30bn run-rate in 2024. With this kind of growth, the market for GLP-1 is expected to reach $100 bn by 2030. Rapid growth is anticipated as innovators scale up manufacturing, patents expire in various markets, generic supplies increase, and GLP-1 medications get US FDA approvals for other chronic indications such as cardiovascular disease.

Shaily Engineering Plastics Ltd, by virtue of its patented pen platforms, is directly plugged into the global GLP-1 supply chain. While right now it is gearing up to supply generic GLP-1 manufacturers, in the future it may also be able to crack innovator business from the likes of Novo Nordisk or Eli Lilly.

Less competition in insulin pen devices – Due to the booming market of GLP-1 devices, some device makers, such as Ypsomed, have decided to move away from the insulin device business and put their complete focus on the GLP-1 device business. This is opening up new opportunities for Shaily Engineering Plastics Ltd. to take over more market share in the insulin devices space.

Increasing proliferation of biologics in the pharmaceutical industry – Biologic drugs today account for ~30% of global pharma sales, and they are taking up an increasing proportion of new drug approvals given by the US FDA each year. Most biologic drugs are injected into the human body directly into the bloodstream for better absorption, as the digestive tract is not suitable for large molecules that make up biologic drugs. Therefore, as more and more biologics take up global pharma market share, the business visibility for injectable device manufacturers like Shaily Engineering Plastics Ltd. improves in the long term.

Possibility of significant operating leverage as revenues scale up – As discussed earlier, Shaily Engineering Plastics Ltd.’s current machine utilization levels are at ~40%. Therefore, there is significant scope for operating leverage to play out as the various segments scale up to fill the capacity.

Significant optionalities in other areas, such as consumer electronics – The Shaily Engineering Plastics Ltd. management has hinted at the possibility of entering into precision plastics manufacturing for the consumer electronics segment. Consumer electronics components such as mobile phones, wearable devices, etc., are a huge segment for precision plastics manufacturers, and several of Shaily Engineering Plastics Ltd’s largest global peers have a significant presence in this segment. With the boom in electronics manufacturing and assembly in India, if Shaily Engineering Plastics Ltd. can crack a few global electronics companies as clients, then this segment has huge potential for scale-up.

What are the Risks of Investing in Shaily Engineering Plastics Ltd

Investors need to keep the following risks in mind if they choose to invest into this business. Risks needs to be weighed in combination with the advantages listed above to arrive at a decision that is optimal for your portfolio construct

Valuations are not cheap, and there is execution risk – At 90x trailing earnings, Shaily Engineering Plastics Ltd. is certainly not cheap by any standards. Any slip in execution at these valuations can cause significant drawdowns in the stock price. While Shaily Engineering Plastics Ltd. has a healthy pipeline of signups on its pen platforms, only time will tell how well the platform subscriptions will convert to actual commercial revenues. There are two risks here – one that a generic company that has signed on to Shaily’s platform now may eventually choose to go with another device manufacturer, and two, the generic companies that proceed with Shaily’s platforms for commercial launches are unable to garner significant GLP-1 market share eventually.

High margin development revenues in Shaily UK will ramp down eventually – As Shaily Engineering Plastics Ltd. finishes the development of platforms for various pharma companies who are keen to partner with Shaily for their GLP-1 launches, the high margin platform development fees will eventually start ramping down. This is likely to start happening in late FY27 or FY28. Hopefully, by then, commercial GLP-1 revenues will be large enough to more than make up for the drop in revenues and margins from the platform revenue ramp-down. Even if commercial revenues take slightly longer to make up the deficit, a drop in revenues or profits is only going to be a temporary phenomenon lasting a few quarters. Irrespective, this remains a factor worth keeping an eye out for, especially as valuations are baking in flawless execution.

Potential US FDA inspection pending – Shaily Engineering Plastics Ltd. is MDSAP (Medical Device Single Audit Program), ISO 13485:2016, and US FDA 21 CFR:820 certified and, therefore, has all the necessary certifications for supplying medical devices to regulated markets such as the USA. However, if Shaily Engineering Plastics Ltd. does become a key supplier of pens and auto-injectors in the US market, a USFDA inspection of their facilities at a future date cannot be ruled out. As an example, India’s premier medical devices manufacturer, Polymedicure, has had USFDA inspections of its plants in the past. Shaily Engineering Plastics Ltd. hasn’t gone through a US FDA inspection before. As pharma investors would know, US FDA inspections are key risk events for pharma and medical device companies.

Management bandwidth – Scaling up GLP-1 devices to service global generic pharmaceutical clients is going to be a mammoth task. With such a task at hand and two other segments that are also growing, it remains a question whether Shaily Engineering Plastics Ltd. has enough top-quality management bandwidth beyond the promoter level. Shaily Engineering Plastics Ltd has been without a CEO since 2021, and recently, the promoters have said that they have abandoned the search for a CEO and instead plan to promote internal employees to segment head positions for the 3 key segments. Without sufficient high quality management bandwidth, Shaily Engineering Plastics Ltd may face issues in quality and compliance or in ramping up execution at the required pace for GLP-1 and insulin, so this remains an area we continue to monitor closely.

Significant under-utilization of capacity – Shaily Engineering Plastics Ltd. has invested significant amounts of capital into asset expansion over the last 5-6 years. However, its machine utilization levels have fallen from 60%+ in FY22 to 40% over the last two and a half years. Most of the under-utilization seems to be in the consumer and industrial segments as healthcare volumes are ramping up. Sustained underutilization over 2.5 years does prompt questions regarding the timing of capital deployment by management.

Entry and exit from the toys business within a span of a few years – Shaily Engineering Plastics Ltd. ventured into the toys segment in FY20 with global toy major Spin Master with a capex spend of ~INR 30 Cr. However, as early as FY23,Shaily Engineering Plastics Ltd realized that the toy business had a lower margin due to China dumping, and customer stickiness in this segment wasn’t high. In FY24, they admitted that entering the toys business was strategically not the right move and hence decided to shut down the segment. The capacity for toys is fungible with other consumer products. While such miscalculations are part of any business, this misadventure coupled with the generally low machine utilization levels, does cause us to ask some questions on whether management was too overenthusiastic in creating assets, especially in the consumer segment.

Shaily Engineering Plastics Ltd Future Outlook

The current capacity for pens and auto-injectors for Shaily Engineering Plastics Ltd. is between 30-40mn pens a year. Of this, about 12mn pen capacity is available for insulin, and about 10mn pen capacity is available for semaglutide. In the Q2 FY25 conference call, Shaily Engineering Plastics Ltd’s management indicated that they are about to embark on a significant expansion of healthcare capacities.

- Insulin capacity will go up from the existing 12mn pens to ~30-35mn pens within the next 14-16 months.

- Semaglutide capacity will go up from the existing 10mn pens to ~35mn pens by H1 CY26 i.e. in another 12-18 months

- Therefore, overall capacity will go up from the existing 30-40mn pens per year to 80-90mn pens per year. The expected capex for this expansion will be in the range of INR 150-200 Cr.

If the expanded capacities of insulin and semaglutide start getting close to fully utilized by H2 FY27, then the healthcare division itself can start reporting revenue numbers as high as INR 600-700 Cr by FY28. Of course, a remarkable scale-up like this would need a lot of things to go right for Shaily Engineering Plastics Ltd. First; they must hope that most of the generic pharma companies that have subscribed to their platform will eventually stick to them as their device supplier for commercial supplies. Second, if the clients do stick to Shaily Engineering Plastics Ltd, Shaily Engineering Plastics Ltd has to hope that their clients are able to gain significant market share for the respective products in the respective geographies, failing which Shaily Engineering Plastics Ltd pen revenues may not grow as expected through no fault of their own. So, as they say, there is still many a slip between the cup and the lip, but the possibilities of non linear growth in the healthcare segment for Shaily Engineering Plastics Ltd are indeed possible and exciting.

The other two segments are expected to grow steadily without too many fireworks – the consumer segment is expected to bounce back after a few muted years post Covid and post double-digit growth rates, and the industrial segment is expected to grow in the high teens or mid-twenties on its lower base.

Shaily Engineering Plastics Ltd Technical Analysis

We consider technical analysis to be a useful input in taking medium-term investment decisions. Many a time price action tends to lead to fundamental developments; this is too important an aspect to be ignored by retail investors who do not have access to management outside of common forums like investor calls & AGM.

At Congruence Advisers we like to consider both the long-term weekly chart and the daily chart to arrive at a view on price action. Combined with our understanding of fundamentals, we usually end up being better placed to be able to judge both the business cycle and the stock cycle. Playing the stock cycle right is extremely important for investors looking to extract significant alpha over the medium term.

Shaily Engineering Plastics Ltd Price charts

Let’s analyze Shaily Engineering Plastics Ltd.’s weekly charts over the last 3 years.

Shaily Engineering Plastics Ltd stock consolidated for a period of over two years from late 2021 to Jan 2024 between the levels of 192 and 443. In Feb 2024 it finally broke out of the range after the declaration of Q3 FY24 results where PAT increased by 150% YoY. It retested the breakout levels in March 2024. Thereafter Shaily Engineering Plastics Ltd stock kept going up as the market started acknowledging revenues from Shaily UK. After Q1 FY25 results confirmed the business momentum, institutions started entering the Shaily Engineering Plastics Ltd stock as evidenced by the skyscraper-like volume bar in June. Shaily Engineering Plastics Ltd stock price breached 1000 levels. Hereafter it pulled back to 900 levels for a couple of months before Q2 results once again sent it back on a momentum upswing.

On daily charts, over the last 1Y or so, Shaily Engineering Plastics Ltd stock appears to be very strong. During this period Shaily Engineering Plastics Ltd stock is up 4x and hasn’t breached the 50 DMA moving average (except for a brief period in Oct 2024). H2 FY25 is expected to be similar to H1 FY25 in terms of results. H1 FY26 may not see significant YoY growth as commercial revenues from teriparatide, liraglutide and semaglutide are expected to be back ended in FY26. Therefore Shaily Engineering Plastics Ltd stock may correct or consolidate for a while in 2026. Given that the long term prospects for the business are quite strong, the 100 DMA moving average levels may act as support at that time. However, since valuations are already pricing in perfect execution, any unexpected disappointment in numbers can cause a sharp correction for a while.

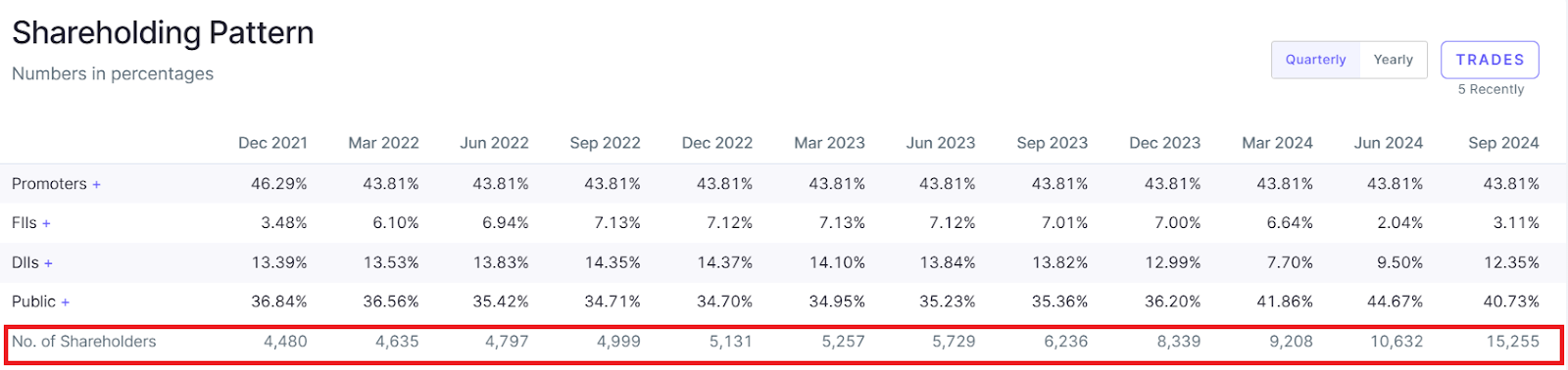

Shaily Engineering Plastics Ltd Shareholding Pattern Analysis

One very interesting aspect of Shaily Engineering Plastics Ltd is that even at ~INR 6700 Cr market cap, the number of shareholders is still around 15000. The average retail shareholding in Shaily Engineering Plastics Ltd stock is ~INR 12.5 lakhs. This indicates the possibility of large HNI shareholders who are unwilling to sell the stock at this point.

Shaily Engineering Plastics Ltd Latest Latest Result, News and Updates

Shaily Engineering Plastics Ltd Quarterly Results

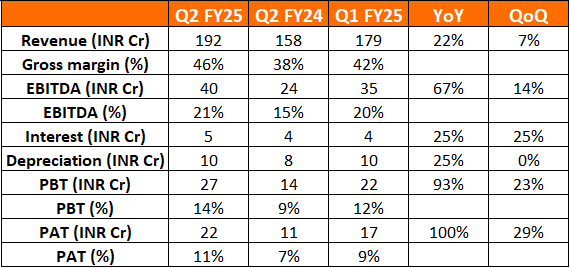

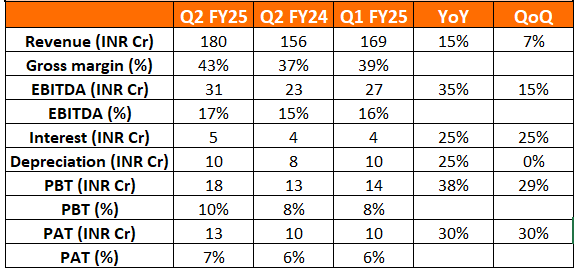

Shaily Engineering Plastics Ltd. reported very good Q2 FY25 earnings. Consolidated revenues grew by 22% YoY. EBITDA and PAT grew by 67% and 100% YoY respectively. Even on a QoQ basis, revenues, EBITDA, and PAT grew strongly by 7%, 14%, and 29%, respectively.

A large part of the YoY growth in margins was driven by a significant uptick in high-margin platform and development revenues from Shaily UK. Shaily UK reported a revenue of INR 12 Cr and an EBITDA of INR 9 Cr in Q2 FY25 as against a revenue of INR 2 Cr and an EBITDA of INR 1 Cr in Q2 FY24.

Standalone business growth was also strong, with standalone revenues, EBITDA, and PAT growing by 15%, 35%, and 30% YoY, respectively. On a QoQ basis as well, revenues, EBITDA, and PAT increased by 7%, 15%, and 30%

Final thoughts on Shaily Engineering Plastics Ltd

Shaily Engineering Plastics Ltd offers the compelling possibility of a home grown medical devices manufacturer who is able to carve a niche and compete with the global majors in a space that is likely to see aggressive growth. We have observed over the past decade that even in the API (Active Pharma Ingredient) space, players focusing on providing differentiated solutions in chronic therapies have stronger moats and better unit economics to show for the same. Shaily Engineering’s presence in the GLP-1 value chain offers tremendous potential for growth if execution is on expected lines and the anticipated scale up in healthcare revenue materializes over the next 2-3 years.

Innovators like Novo Nordisk & Sanofi are known to build sticky supply chains; with limited competition in the area of pen manufacturing the market will likely assign this business a high terminal value if things fall into place. For the longest time, Shaily Engineering’s claim to fame was that it was a long term supplier to IKEA. If the business can add marquee names in the healthcare and industrial verticals, it can drastically improve the perception of the business within the broader investor community. Even today, in spite of the steep rise in the stock price over the past 12 months, very few investors outside of the serious investing community are able to build the conviction to buy a stock that is optically very expensive.

Investors will need to do their own work and build conviction in the market opportunity and the ability of the management to deliver on the aggressive scale up plans they have lined up. The business has invested more than 600 Cr into driving the next leg of growth in an area that is exciting in terms of the possibilities, revenue scale up from here can result in operating leverage that many investors will find it tough to believe. Execution risk is probably the biggest risk facing the business right now, this will need a nuanced assessment by investors.

If not for anything else, investors should track this stock as a case study on what can happen when high operating leverage, high terminal value (if things go as planned) and healthy unit economics come together in a business that trades below a market cap of 7,500 Cr and delivers revenue of less than 1000 Cr p.a. Valuation is never a straight forward exercise, if Price to Earnings ratio were all that mattered in valuation, no one would need to do a deep dive into businesses.

Disclaimer – This note is part of a business research & analysis series on small companies, there is no BUY/SELL recommendation or target price issued as part of this. There is no assurance that this stock makes for a good investment, there is no guarantee that this stock will be included in the coverage universe of Congruence Advisers. The note contains some forward-looking statements and insights drawn from the historical results, annual reports and investor presentations; they are to be viewed only within this context and not as a prediction of future performance of the business or the stock covered.

While due care has been taken to ensure that the information here is as accurate as possible, Congruence Advisers disclaims any liability in case of any unintentional inaccuracies.

The content does not constitute investment advice.

Disclosure (Updated as of Dec 31, 2024) – No position in the stock in personal portfolio