Mistakes don’t happen in a vacuum; you cannot win if your opponent doesn’t make mistakes.

A Magnus Carlsen quote after beating Viswanathan Anand in a game of conventional chess. Carlsen put Anand under sustained pressure for over 34 moves before Anand made a blunder under time pressure.

Watch the 2020 French Open men’s final.

Nadal beat the next best clay court player in straight sets with a rather easy looking score line. He in fact beat Djokovic 6-0 in the first set, but that was by far the best fought 6-0 I have ever seen in tennis. Each point was a dogfight, just that Nadal was marginally better in every aspect. The first set score line had a devastating impact on Djokovic’s mindset for the remainder of the match though he was playing well by any standard. Just that he was up against a machine that did nothing wrong that day.

Djokovic after the match “I was probably rushing a bit much, trying to play shorter points, probably go for winners. I probably wasn’t constructing the points well. That reflected on the result. But that was also caused by his amazing defense. He was getting a lot of balls back. Normally all the shots that I play after two, three quick exchanges from the back of the court, when I hit it against nine out of ten guys, it’s a winner, the point is done. But not against him.”

See the pattern here?

Nadal and Carlsen are masters at front running, they just don’t give an inch. The opponent is then left chasing the game which induces more mistakes, while Nadal and Carlsen are playing in a Zen like state making very few errors. The 5% quality differential they manage to produce at key moments makes their victories look much easier than they are. Djokovic would have beaten any other Top 10 player in three easy sets that day, just not Nadal.

How does this relate to investing?

- Do not make mistakes. If you can avoid mistakes, you will likely make market linked returns over the medium to long term

- Do not fall way behind in the game. One mistake may not hurt but a string of mistakes is tough to recover from

- Always stay within striking distance of the leading pack, you don’t always need to be in pole position

One of the mental constructs I find particularly useful as an investor is to view investing as a medium distance race. It isn’t a 100-meter sprint, it isn’t a half marathon either. You don’t need to be the quickest off the blocks, nor can you afford to fall behind too much. What about the long term then? Well, the long term is a series of medium terms. Unless you can do reasonably well over the medium term, it is unlikely that you will do well over the long term.

What the public media discourse harps on excessively is the long term to the extent as if the short term and the medium term do not matter at all. Easy to do this when you do not have skin in the game. They say time in the market is more important than timing the market which is partly true. What they do not tell you is that time works against you if you keep making mistakes. Imagine the plight of the disciplined long-term investor in Reliance Communication, Yes Bank, DHFL and other similar stocks. Though these were all acknowledged to be good companies at one point in time, they would have decimated your capital over the years.

While this long term gyan is being peddled, the media also hypes up stocks that have near term momentum. These hot stocks coax investors into chasing prices in the short term. This happens when you buy into a story that is running at higher than average growth at best possible margins due to a temporary phenomenon. Once the transient factors revert to their long-term averages, you are left holding something in the hope that you will recover your principal in a few years. Buy high and sell higher is not that easy to do, yet that is the segment of the market that entices most market participants.

In terms of psychology, what usually happens is that investors give themselves the rationalization of “quality business over the long term” to give themselves the permission to chase high prices. If it is a “high quality business” that some fund manager is waxing eloquent about on the TV, investors feel the inherent business quality will overcome whatever intermittent bumps the business might hit.

An optimistic market mood puts investors under a different kind of stress, it is not easy to keep your sanity and to stay the course when every stock you are researching goes up 10% higher by the time you are done researching it. It is like being a medium distance runner who likes to run at a steady pace but is being overtaken by runners who are running at a pace that has historically been unsustainable for that distance.

In such a situation, one is better off being a Nadal or a Carlsen, just buckle up and focus on not making mistakes rather than go for risky shots. Play the percentages and wait for the eventual easy game where the opponent makes a couple of unforced errors. If the history of the Indian market is anything to go by, the easy game does come along every now and then. The start stop nature exhibited by the Indian market over the past decade makes it easier not to chase prices during the odd good years where the benchmark index spikes 25%+

If one is a proven alpha generator, it makes all the more sense to focus on extracting beta from the market when the mood is optimistic. Focus on improving the average quality of the portfolio during times when the market is on a tear, the eventual bad/average year will only widen the eventual outperformance over the benchmark for good investors.

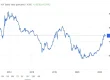

Do have a look at my legacy portfolio (Small & Micro cap approach) performance here. If I had gone the Nadal/Carlsen way in 2017, I could have avoided a good chunk of the pain I went through in 2018. Notice the two big down bars in Q2 and Q3 of CY2018. My legacy portfolio value today would have been a good 15-20% higher than what it is had I managed to execute this finer aspect well through 2017. So yes, I make my share of mistakes too.

2018 was by far the most challenging year for me as an investor, this was the year where the markets did fine but I was off by a good margin. I managed the 2020 ride better because of the 2018 experience. There is no substitute for experience and for doing your own thinking.

We live and we learn, in that order.