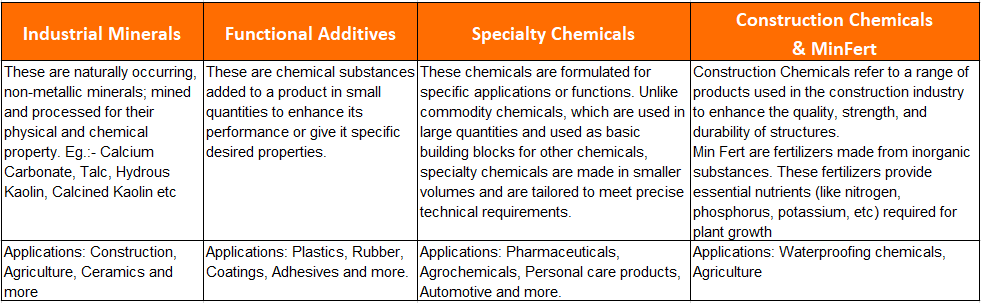

20 Microns Ltd. is a pioneering and leading industrial mineral company with rich experience spanning over three decades. 20 Microns Limited product range includes an array of nonmetallic industrial minerals such as calcium carbonate, talc, kaolin, mica, quartz, dolomite, natural red oxide, and many specialty chemicals and functional additives, like mineral fertilisers, construction chemicals, and many more, that are used as building blocks in various industries like paint, plastics, rubber, paper, ceramics, tires, and many more.

20 Microns Limited has 9 state-of-the-art manufacturing facilities and warehouses across India, with a manufacturing capacity of more than 4,50,000 metric tons per annum. Additionally, 20 Microns also operates 5 captive mines in India, collectively holding a total mining reserve of approximately 170 lakh million tons.

Can 20 Microns Ltd be a good proxy play for the paint Industry ?

20 Microns Ltd presents an interesting opportunity as a proxy for the growth of the paint industry, with every major paint company, including recent entrants, counted among its customers. Despite being a microcap, 20 Microns Ltd has delivered consistent performance over the past decade, especially on the margin front and used operating cash flows to strengthen the balance sheet. However, a key monitoring factor is whether 20 Microns can accelerate its revenue growth beyond historical trends. If 20 Microns Ltd can deliver revenue growth over 15% p.a. over the medium term, the market can rerate this microcap stock.

20 Microns Ltd. Company Overview

20 Microns Ltd. is a micro-cap company that operates in the business of industrial minerals, functional additives, and specialty chemicals. 20 Microns Ltd. was incorporated in 1987 by the late Chandresh R. Parikh by setting up an industrial space in Waghodia, Gujarat. Since then, 20 Microns Ltd. has gone through a series of mine acquisitions, expanded capacity, introduced new products, formed subsidiaries with foreign players and ventured into different markets. In 1994, 20 Microns Ltd. became a public limited company, and in 2008, its stock was listed on the NSE and BSE.

Initially, 20 Microns Ltd. operated in the commodity segment of industrial minerals. In 1999, 20 Microns Ltd. shifted their focus to value-added products like functional additives and specialty chemicals, even though the share of value-added products is close to only 20% of sales at present. The formation of strategic subsidiaries and joint ventures has provided 20 Microns Ltd. with technical know-how and access to high-quality resources. However, the value-added segment is still a small part of the total revenue, and the profit margin of one of the wholly-owned subsidiaries meant for this value-added segment is not very appealing yet. Management has said this is due to the subsidiary’s subscale operations. We will discuss this subsidiary in detail later in the report. To support its value-added segment, 20 Microns Ltd. created a new identity for the R&D centre within the organisation in 1994; its R&D centre was approved and recognised by the Government of India in 2011

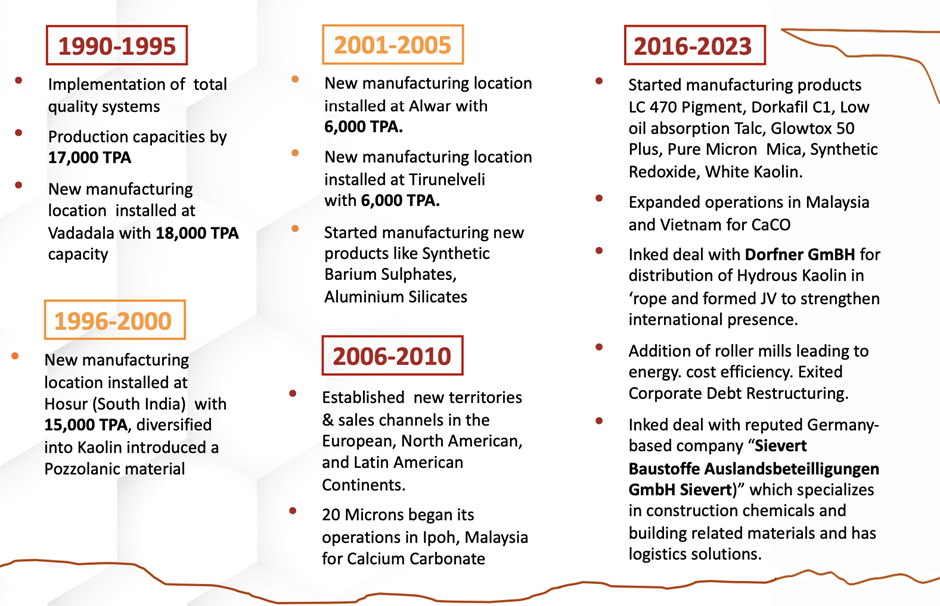

20 Microns Ltd Evolution

20 Microns Ltd evolution over time, highlighting key milestones such as their entry into new markets, the formation of joint ventures, and the establishment of new manufacturing facilities.

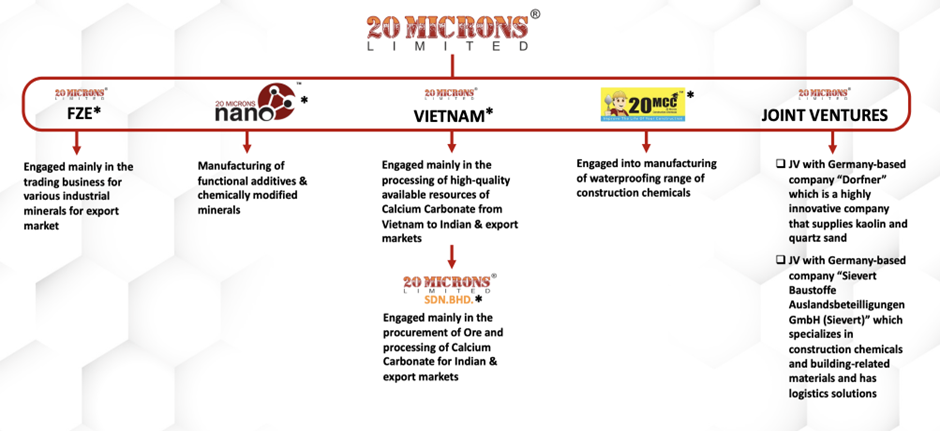

20 Microns Ltd Company Structure – Subsidiaries & Joint Ventures

20 M NANO – Indian subsidiary with 97.21% ownership, involved in the manufacturing of functional additives & specialty chemicals.

20 M SDN BHD – Foreign Subsidiary with 100% ownership, involved in the procurement of ore and processing of calcium carbonate for Indian & export markets.

20 M FZE – Foreign subsidiary with 100% ownership, engaged mainly in the trading business of industrial minerals for the export market.

20 M VIETNAM – Foreign subsidiary with 100% ownership, engaged mainly in the processing of high-quality available resources of Calcium Carbonate from Vietnam to the Indian & export markets.

20 MCC – Indian subsidiary with 100% ownership, that is engaged in the manufacturing of a waterproofing range of construction chemicals.

Dorfner – Germany-based JV partner, which is a highly innovative company that supplies kaolin and quartz sand.

Sievert – Germany-based JV partner that specialises in construction chemicals and building-related materials and has logistics solutions.

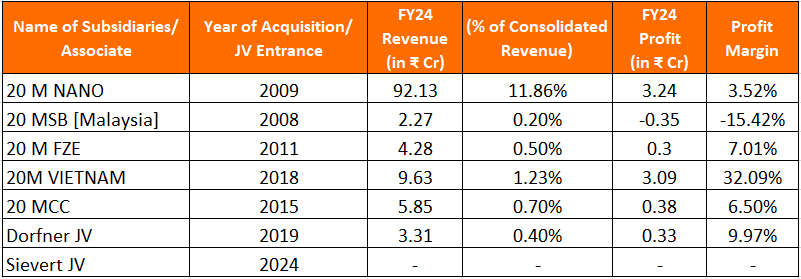

Among 20 Microns Ltd subsidiaries, 20 M NANO contributes 11.86% of revenue. The PAT margin of 20 Microns Nano is only around 3.52%, which is lower than that of the standalone business. Management speaks very highly of this segment, but the promise has yet to show up in meaningful numbers.

Since 20 Microns Ltd main focus is on this segment, we need to see how this margin will play out in the coming future. Other subsidiaries like 20 M FZE, 20 MCC and 20 M VIETNAM contribute very little to the total revenue. 20M Vietnam is in the business of processing high-quality Calcium Carbonate and has very high-profit margins, but it contributes very little to the total revenue. Revenue contribution by other subsidiaries is less than 1% of total revenues, which is not material for the business. JV with Germany-based Dorfner helps 20 Microns Ltd. with kaolin [a very important mineral for 20 Microns Ltd.], quartz sand and their technical expertise. At the same time, the recently formed JV with Sievert aims to assist 20 Microns Ltd. in their construction chemical-related retail segment, which contributes very little to their total revenue at present. In the table below, we can find the financials of the subsidiaries and JVs for FY24 with corresponding revenue contributions and profit margins.

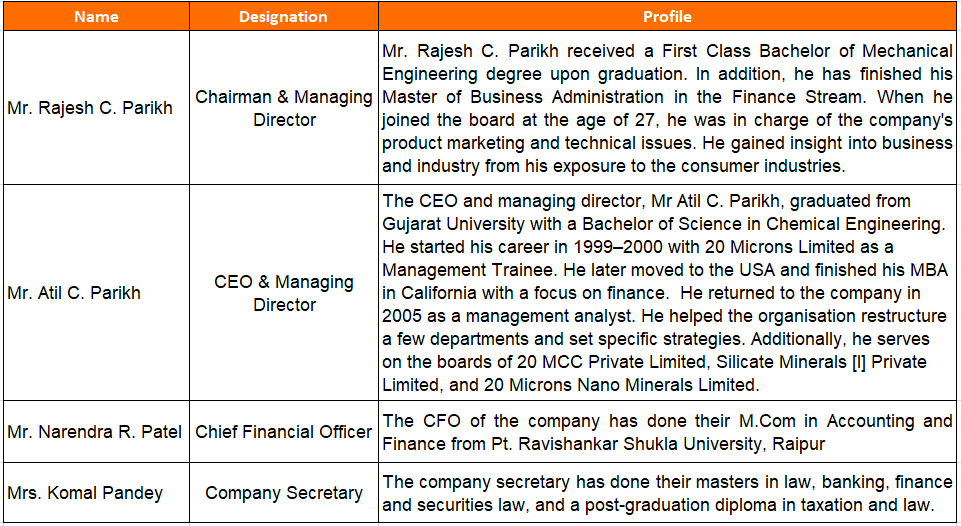

20 Microns Ltd Management details

Mr Rajesh Parikh and Mr Atil Parikh, two sons of the Late Chandresh R. Parikh from the promoter family, hold key managerial positions in the firm. Mr Rajesh oversees the development of new products and formulates marketing strategies for their launch in the market, while Mr Atil Parikh develops commercial strategy and focuses on improving the efficiency of the business.

20 Microns Ltd Industry Overview

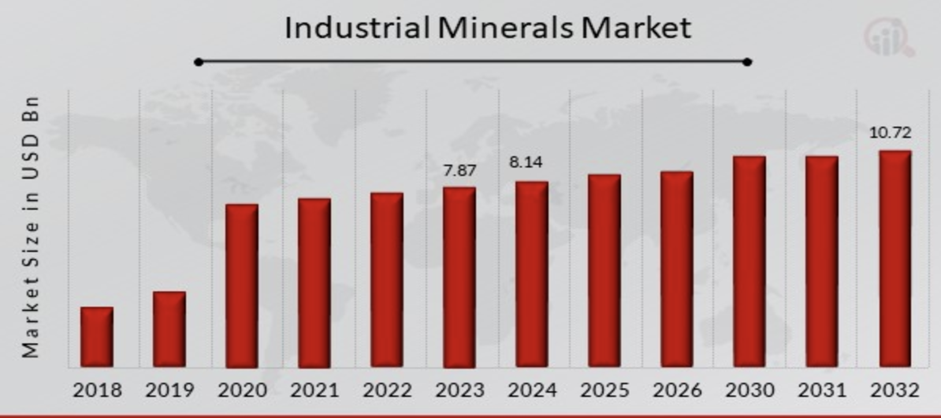

Global Industrial Minerals Market

The Industrial Minerals market was valued at USD 7.87 billion in 2023 and is expected to expand from USD 8.14 billion in 2024 to USD 10.72 billion by 2032, reflecting a compound annual growth rate (CAGR) of 3.50% over the forecast period (2024-2032).

[Source: Market Research Future (Industrial Mineral Report)]

With increased demand in the end-user industries, increasing urbanisation and infrastructure, demand for industrial minerals has risen. Limestone leads the market, contributing 58% of the total market. Limestone (CaCO3) and gypsum are crucial to various industrial applications, such as steel production, cement manufacturing, and industries like food, construction, and pharmaceuticals.

[Source: Market Research Future (Industrial Mineral Report)]

The Industrial Minerals market in India is being driven by growth in the construction sector and technological advancements. Key government initiatives, such as the PM Gati Shakti Master Plan for Expressways (2022-2023), aim to expedite transit and expand the National Highway network by 25,000 kilometres, with a budget of INR 20,000 crore (USD 2.42 billion). The Indian real estate sector is also seeing significant private investment, with USD 5 billion in institutional investments in 2020 and considerable growth in private equity investments in late 2021.

The Asia-Pacific market is expected to grow at the fastest rate from 2023 to 2032. China’s industrial minerals held the largest share, while India is the fastest-growing player in this segment due to its booming infrastructure and real estate industry, which is expected to be valued at USD 1.4 trillion by 2025.

Key players in the Industrial Minerals market are making substantial investments in research and development to diversify their product offerings and drive market growth. To remain competitive, the industry must focus on offering cost-effective products. A major strategy involves local manufacturing to reduce operational costs, benefit customers and expand market share.

India’s Stand on Mining

The government of India has generally disregarded the mining sector, enacting few significant policy or reform changes to increase investor confidence and draw in capital. India has large mineral reserves, but quick production has depleted good-grade reserves, creating an imbalance and discouraging development in new areas. In order to solve these problems, the National Mineral Policy (NMP) 2019 encourages openness, improved regulation, and environmentally friendly mining methods.

India’s mining sector, which falls into a number of categories, including fuel-related, metallic, non-metallic, atomic, and minor minerals, is anticipated to undergo substantial changes in the upcoming years as a result of the Make in India Campaign and the expansion of infrastructure.

Despite regulatory stagnation and high borrowing rates, the sector continues to play a significant role in India’s GDP. In order to draw in investment, the industry’s future depends on enhanced geological data interpretation, new technology, and distinct laws for prospecting and exploration permits. [Source: Annual Report; 20 Microns Ltd., FY20]

Some of the key minerals central to 20 Microns Ltd business include calcium carbonate, which has the lowest margins; kaolin, which is the primary focus of management due to its high margin and growth potential; and talc and quartz, which are on the commodity side of minerals.

Calcium Carbonate: Calcium carbonate is a key industrial mineral used as a filler and additive in many industries. It’s vital in making paper, plastics, paints, rubber, and adhesives, enhancing their properties. Its abundance and low cost make it popular for industrial use despite lower profit margins than specialty minerals. Calcium carbonate is also important in environmental applications like flue gas cleaning and water treatment.

Kaolin: Kaolin, primarily composed of kaolinite clay, is a crucial industrial mineral prized for its fine particles, whiteness, and chemical stability. Its natural (hydrous) form enhances smoothness, brightness, and opacity in ceramics, paper, rubber, and paints. Calcined kaolin, produced by heat treatment, offers superior brightness, opacity, and electrical insulation, making it valuable in coatings, plastics, and high-end ceramics for improved durability and reflectivity. Hydrous kaolin, the water-containing natural form, serves as a filler and coating agent in paper, ceramics, and rubber, enhancing texture and appearance with good dispersion properties.

Talc: Talc, a soft, water-repellent mineral composed of magnesium, silicon, and oxygen, serves as a versatile filler and additive across various industries. Its platy structure and lubricating qualities enhance product smoothness and processing efficiency. In plastics and rubber, talc boosts strength and heat resistance, while in paints and coatings, it improves durability. The mineral’s inertness and softness make it ideal for cosmetics, providing smooth texture and moisture absorption. Talc finds widespread use in cosmetics, pharmaceuticals, paints, plastics, and paper industries, where it serves multiple functions, including friction reduction and moisture control.

Quartz: Silicon dioxide, known as quartz, is a tough, chemically stable mineral prized for its heat and wear resistance. Its hardness and clarity make it valuable across industries. Quartz is essential in making glass, ceramics, and electronics and serves as a filler in paints, plastics, and rubber. Its durability and inert nature contribute to its widespread industrial use.

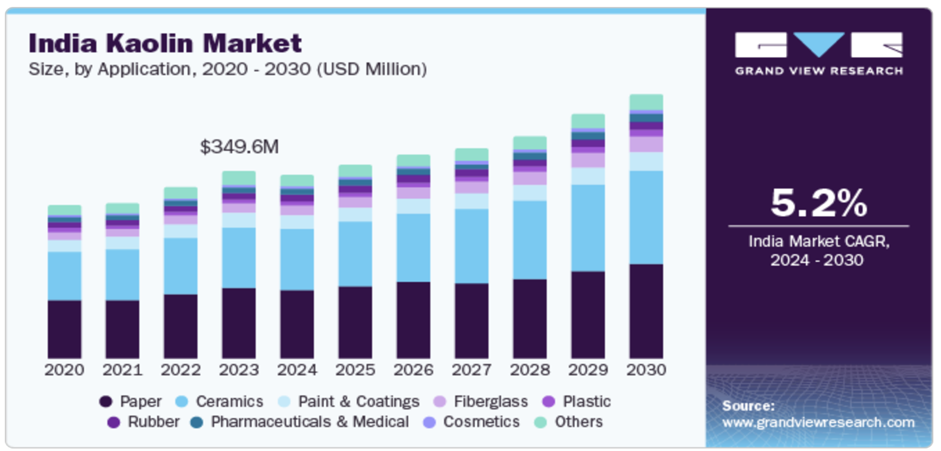

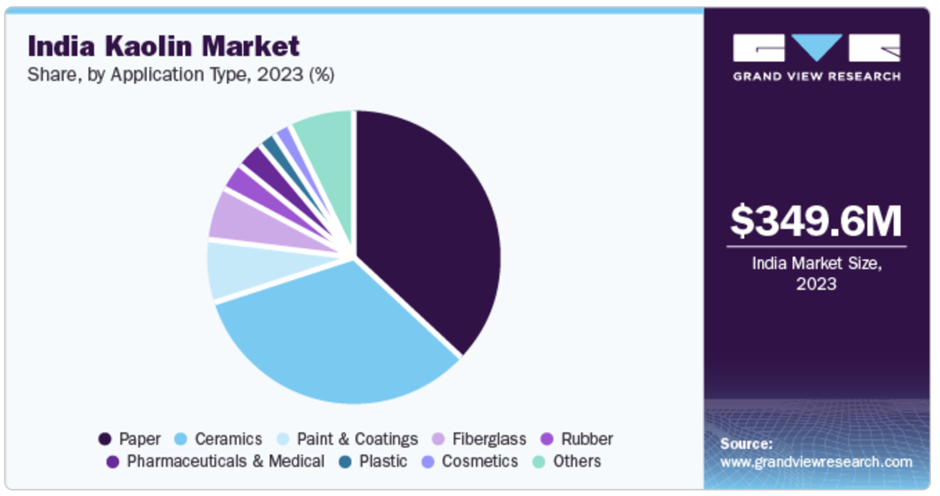

India Kaolin Market Size & Trends

Since Kaolin is such an important product for 20 Microns Ltd., let’s take a deeper look at its market. The Indian Kaolin market was valued at USD 349.6 million in 2023 and was expected to grow at a CAGR of 5.2% from 2024-2030. The Paper and Ceramics industry holds a major share of the total market. Growth in the real estate sector, with an increasing demand for tiles and sanitaryware, will drive this growth to some extent.

The Kaolin market in India is neither very fragmented nor very concentrated. The market is in a medium growth stage, but the pace of market growth is accelerating. The effect of industrial regulation on Kaolin is low and there is very little substitute for the product we obtain from Kaolin.

Industries having lion’s share in the total market are Paper, Ceramics, Fiberglass and Paints & Coatings with over 75% of the total market.

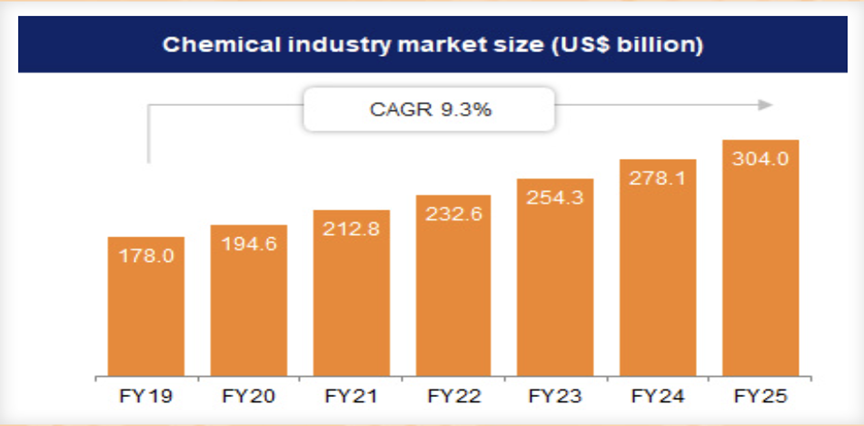

Specialty Chemical Industry

India is the world’s sixth-largest and Asia’s fourth-largest chemical producer. It accounts for approximately 2.6% of the global chemical industry, which is expected to grow at a rate of 9.3% and reach a valuation of USD 304 billion by 2025. The industry could be segmented into four main categories.

- Pharmaceuticals

- Agrochemicals

- Industrial Chemicals [Lubricant, Catalyst, etc.]

- Specialty Chemicals

Source – IBEF

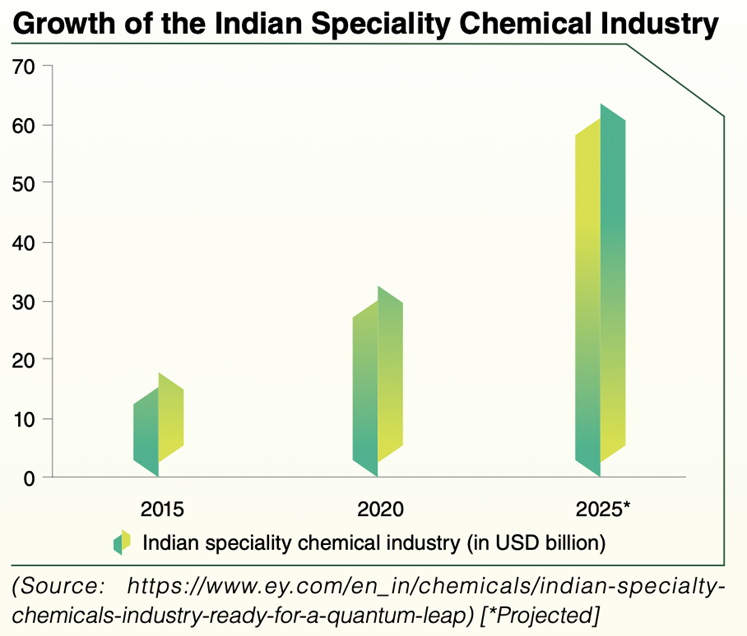

Among the four, specialty chemicals are poised for the most rapid growth and are expected to reach a market valuation of USD 64 billion by 2025. The sector is diverse, spanning over 80,000 different products.

The Indian chemical industry is expected to further grow with a CAGR of 11-12% by 2027, increasing India’s share in the global specialty chemicals market to 4% from 3%.

The specialty chemical industry in India has witnessed exponential growth. India has emerged as a preferred manufacturing hub for specialty chemicals in domestic and international markets. Of the total chemicals market in India, specialty chemicals constitute around 20% and are expected to reach a valuation of USD 64 billion by 2025. China has been losing its cost competitiveness and market supremacy due to rising environmental costs and declining government subsidies, while India is expected to double its share of the specialty chemicals market in five years.

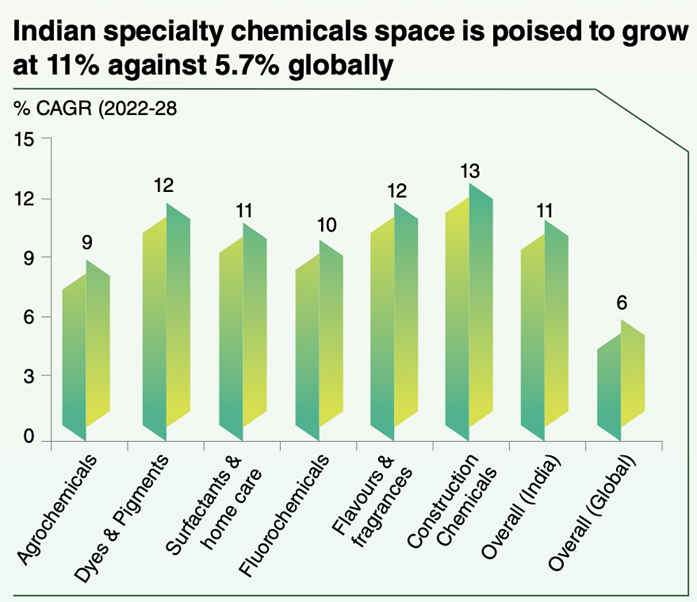

India has a meagre 3.6% market share in speciality chemicals worldwide and is poised for rapid expansion. With a predicted 11% CAGR through FY26, India is putting itself in a strong position to advance significantly.

The Indian specialty chemicals space is expected to beat the global growth rate in the segment by 530 basis points. This growth is driven by major segments like Dyes and pigments, Construction chemicals, etc., which are the major focus of 20 Microns Ltd.

As per Motilal oswal report – Specialty Chemical companies management has expressed confidence in their long-term strategies beginning in FY25, with planned capex projects progressing as per the specified timelines. Notably, for the first time in nearly a year, several management teams have acknowledged that the first half of FY25 may be challenging, particularly for companies heavily reliant on agrochemicals. However, a gradual recovery is anticipated in the second half of the fiscal year.

20 Microns Ltd Product Details

20 Microns Ltd.’s product portfolio includes industrial minerals, functional additives, specialty chemicals, construction chemicals, and mineral fertilisers. Industrial minerals, functional additives, and specialty chemicals are B2B products, whereas construction chemicals and mineral fertilisers are B2C products. The bulk of the 20 Microns Ltd revenues are derived from B2B products.

With its wide range of products, 20 Microns Ltd. has a presence in the domestic market as well as in 65 other developed and emerging countries. 20 Microns Ltd.’s management believes that American and European markets have become saturated while Middle Eastern and Southeast Asian markets are poised to grow. Thus, 20 Microns Ltd is shifting its focus to these countries while maintaining its domestic presence.

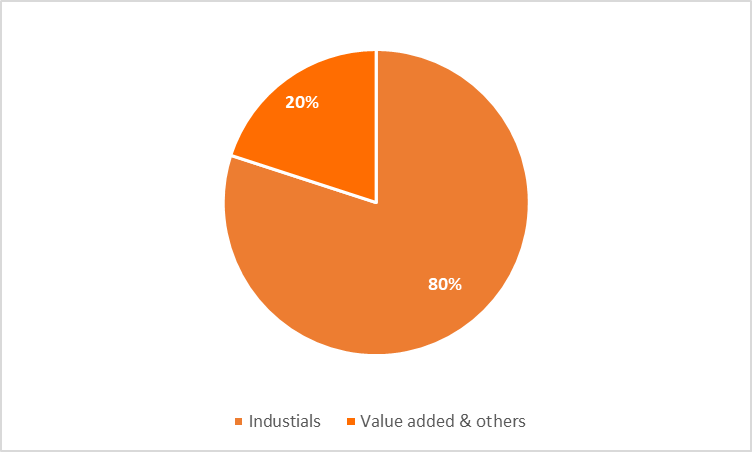

The industrial mineral segment contributes around 80% and the value-added segment and others contribute ~20% to the total revenue.

Various products are manufactured across different segments: Industrial minerals, functional additives & specialty chemicals, and Retail segments (Construction chemicals & MinFert). The functional additives and specialty chemicals segments are engineered from minerals and serve different industries.

Industrial minerals and speciality chemicals are B2B products, whereas construction chemicals and MinFert are B2C products sold via 170+ dealers in Tier 2 and Tier 3 cities in India. 20 Microns Ltd is adopting a gradual approach to market penetration in the B2C segment. They are initially targeting Tier 3 and Tier 4 markets in India, where they are building a distribution network. This strategy allows them to establish a presence in less saturated markets before expanding further. The majority of sales come from the B2B segment [99.2%], while B2C contributes 0.8%. Although the B2C sales numbers are expected to increase 5-fold in the next few years, they’ll still be a small portion of the total revenue.

Product & geography wise revenue break-up of 20 Microns ltd

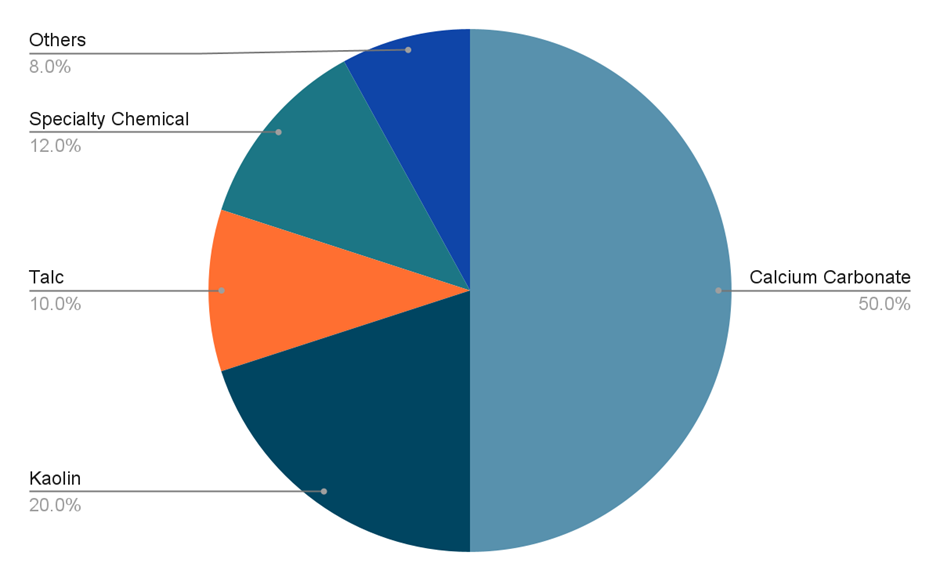

Calcium Carbonate contributes to a major chunk with a share of around 50%. Kaolin and Talc follow with 20% and 10% share of revenue respectively. Specialty chemicals segment contributes 12% of the total revenues while 8% comes from others.

|  |

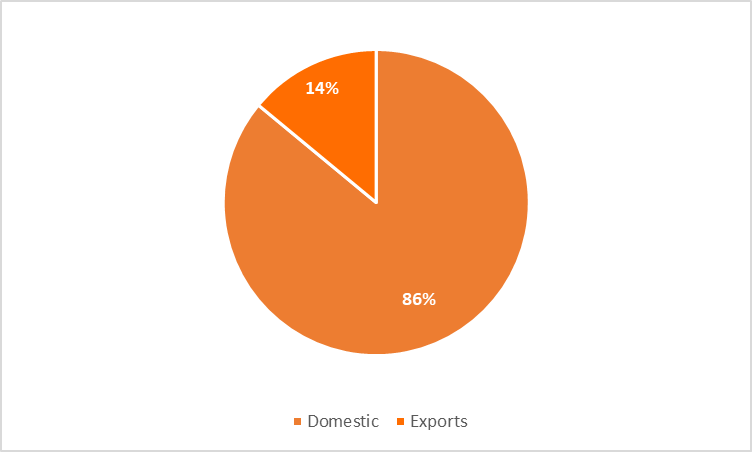

Domestic revenue dominates total revenue with 86%, while exports contribute 14%; this share has remained constant compared to FY23.

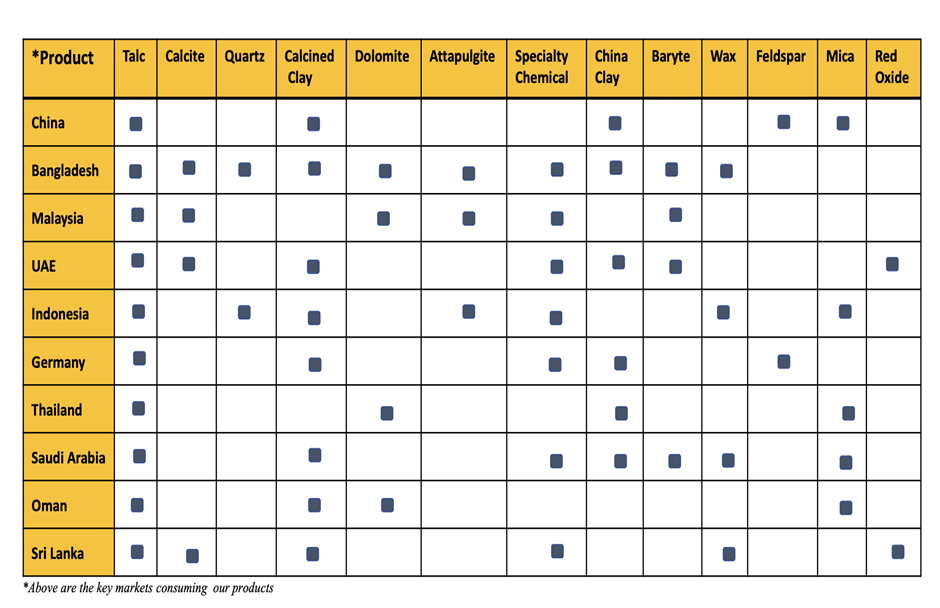

Geographic Mapping of 20 Microns Ltd Export Product Portfolio

20 Microns Ltd. has a presence in 65+ countries in terms of exports. They’re currently shifting their focus to the high-growth market of Middle-East and Southeast Asia

As per FY19 data (exports account for 17% of revenue), the Paint Industry is the major contributor, accounting for 85% of export revenue, followed by allied industries at 8%, plastics at 5%, and rubber at 2%.

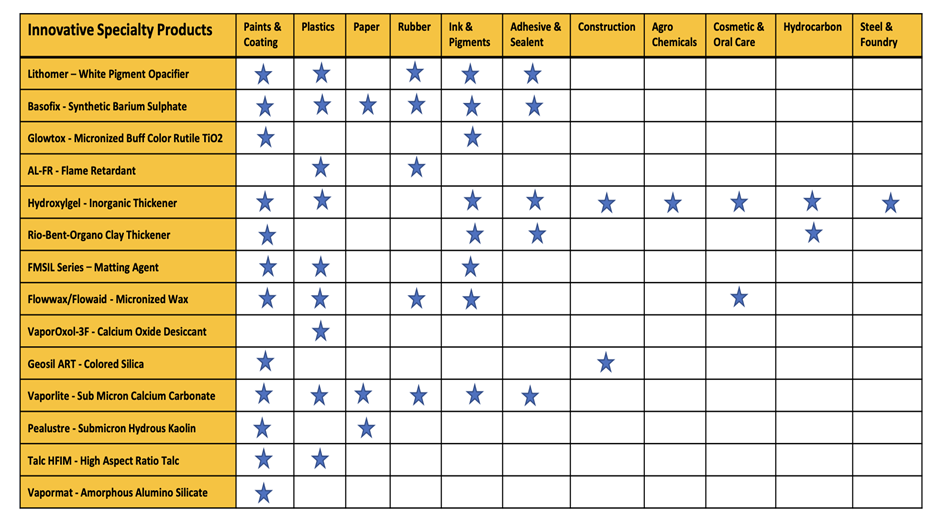

20 Micron Ltd.’s products mapping with respective industries they are used in.

20 Micron Ltd Domestic revenue breakup

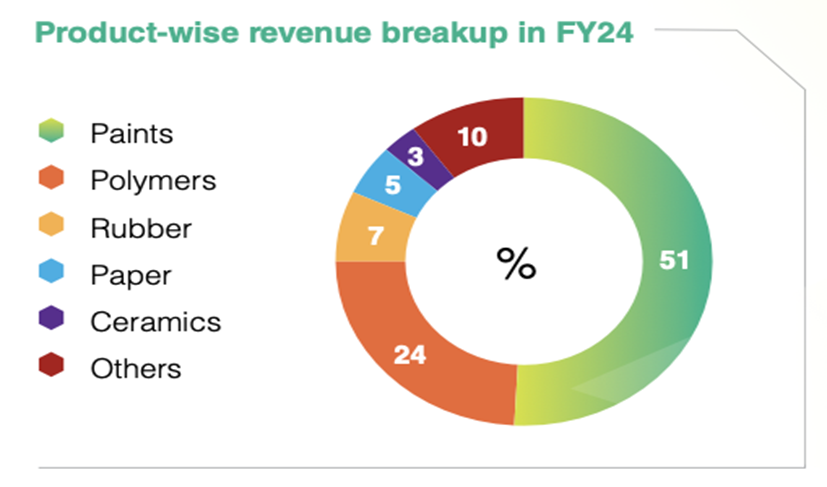

20 Micron Ltd derives a major chunk of the revenue from the Paint industry [51%] followed by Polymers [24%], Rubber [7%], Paper [5%] etc.

In Domestic market 20 microns ltd serves serves 200+ clients including some of the big players like Berger Paints, Asian Paints, Kansai Nerolac, Kajaria, Pidilite, L&T, Finolex, ONGC, JK Tyre, AkzoNobel and many more. While top Two/three players contribute more than 10% of the total aggregate sales.

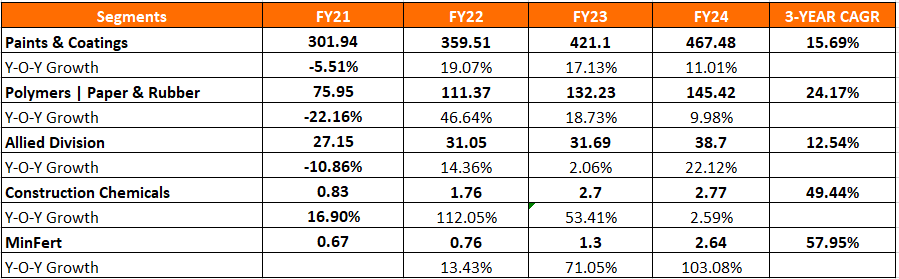

20 Microns Ltd posted a hygienic growth rate of 15%+ CAGR across major segments while new segments saw impressive growth but that is on a very small base. While FY21 was impacted by Covid & FY22 saw the benefit of pent-up demand, post FY22 growth YoY growth is 10%+ across major segments. sales numbers for construction chemicals and MinFert are expected to increase fivefold over the next few years, but they are expected to remain a relatively small portion of the total revenue.

20 Microns Ltd Contract Structure with the Customers:

20 Microns Ltd contract structure with its customers is generally flexible and varies depending on the type of customer and market segment.

Domestic Market Contracts: In the domestic market, 20 Microns Ltd typically does not enter into long-term contracts with its customers. Instead, the sales are often based on regular demand cycles, which can fluctuate depending on the customer’s needs. This allows 20 Microns Ltd to be more responsive to changes in demand and market conditions.

Pricing in the domestic market is also flexible and can be adjusted based on market conditions and the specific requirements of the customer.

Export Market Contracts:

For export customers, 20 Microns Ltd is more likely to have contracts that can be either yearly or bi-annual, depending on the relationship with the distributor or customer. These contracts might include specific terms related to pricing, volume, and delivery schedules.

Some export contracts may involve fixed pricing for a certain period, while others might allow for adjustments based on changes in raw material costs or other market factors.

Customisation and Regular Interaction: 20 Microns Ltd works closely with its customers, especially in terms of understanding their demand patterns, which can be inconsistent and vary from month to month. This close interaction helps 20 Microns Ltd to tailor its offerings and adjust production schedules accordingly.

20 Microns Ltd does not follow a one-size-fits-all approach; instead, it customises contracts and pricing strategies based on the application, product group, and specific customer needs.

Pricing strategies are not uniform across all products or customers. 20 Microns Ltd evaluates major cost components and market conditions to determine pricing, which can differ significantly from one product group to another and from one customer to another.

20 Microns Ltd Manufacturing

Currently headquartered in Vadodara, Gujarat, 20 Microns Ltd. directs its operations from a corporate office in Mumbai, supported by:

- Sales offices

- 12 strategically located warehouses

- 2 state-of-the-art R&D units

- 9 advanced manufacturing units

- 5 captive mines to source raw materials

- The human asset of 800+ comprising the in-house R&D team

20 Microns Ltd.’s operations are backwards integrated to some extent, which means it procures the raw material from the mines it owns. It also sources minerals from its internationally owned mines and imports from sourcing centres like Turkey, Egypt and China to meet international demand for specialty chemicals, as the Indian raw materials do not meet the specifications and standards needed to manufacture specialty chemicals for exports.

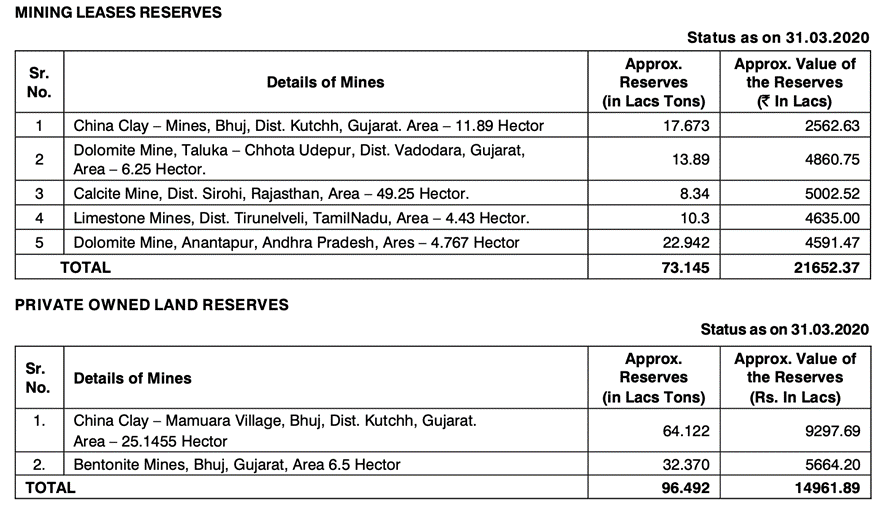

As per 20 Microns Ltd FY20 Annual Report- with the existing capacity utilisation – the mine reserve is expected to last 25 more years [Capacity utilisation in FY24 was 85%], minerals like Kaolin [China Clay], Dolomite, Calcite and Bentonite are domestically sourced. These mines are mainly situated in the states of Rajasthan, Gujarat, Tamil Nadu and Andhra Pradesh. 20 Microns Ltd does not pay rent or lease for the mines. Instead, they pay a royalty on each metric ton mined. This royalty payment is the primary cost associated with operating the mines, rather than a traditional rent or lease payment.

Manufacturing operations take place in the cities of Alwar, Makrana, Udaipur, Bhuj, Waghodia, Vadadala, Hosur and Tirunelveli with a total capacity of over 4.50.000 metric tons per annum across these 9 plants.

Manufacturing operations take place in 3 modes:

Own Manufacturing: Production is done entirely in-house by 20 Microns Ltd where they are operating at 85% of their capacity.

Toll Manufacturing: External manufacturing service using the company’s raw materials.

Contract Manufacturing: External production where the contractor may source materials and produce the goods according to the company’s specifications.

The product manufactured according to specifications goes through a development stage that spans 1-1.5 years. With the help of R&D, the formulation is decided, the product is developed, and then market development takes place.

Products manufactured are then stocked in the strategically located warehouses from where they are delivered to the customers.

20 Microns Ltd Corporate governance

Board Composition– As of FY24, there are 9 directors on the board of Microns Ltd. 6 of them are independent and are not related in any way to the promoter’s family. 3 out of 9 are executive directors [one of them being Chairman & MD, the other being CEO & MD and the last one being the Whole-time director]. Executive directors belong to the promoter’s family. Directors are equipped with experience in the chemical industry and banking sector. One of them holds an LLB degree and a Diploma in Consumer Protection Law.

Promoter Remuneration – The Total remuneration paid to the promoters in FY24 was INR 4.74 Crores, which is 8.46% of the PAT. Remuneration witnessed an increment of 20.29% as of FY23. A “short-term employee benefits” line item was added to Sejal Parikh’s expenses. She was paid an additional 25 lacs, while no amount was given to her in the precious FYs under such a line item.

Related Party Transactions – There weren’t any material related party transactions. However, relatives of the Key Managerial Personnel have begun to draw money under the line item “short-term employee expense,” which may or may not be concerning.

Contingent Liabilities- On a consolidated basis, contingent liability amounts to 11.05 Cr a little less than FY23, which is 3.41% of the net worth.

Dividend Policy- 20 Microns Ltd hasn’t paid any dividends in the last 4 years. A dividend proposal was made. 20 Microns Ltd plans to use the cash to bring down to debt level and carry out necessary Capex without relying upon debt or equity.

20 Microns Ltd Financial Performance

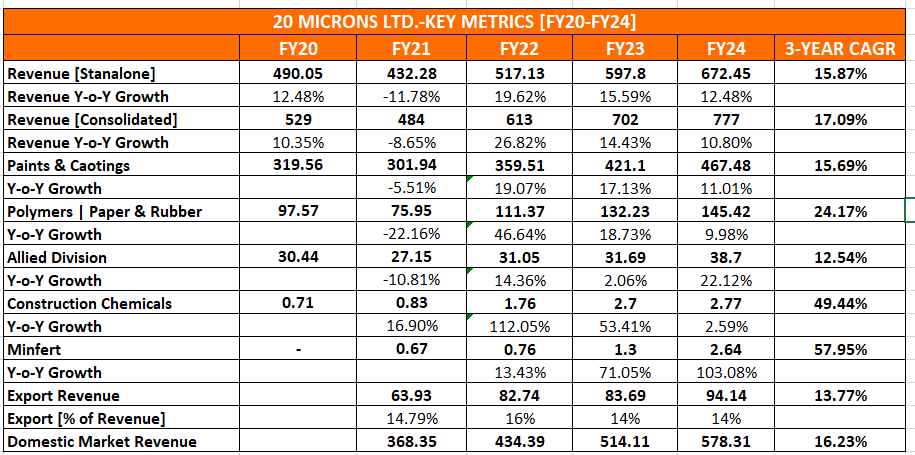

20 Microns Ltd Revenue growth

20 Microns Ltd.’s top line has experienced a growth of above 10% in every financial year except FY21. If we look at the revenue for the past 5 years, growth has been consistent except for FY21, which could be attributed to the impact of COVID. The 3-year CAGR has been close to 15.87% on a standalone basis, while the 5-year CAGR is at 9.10%.

Revenue on a consolidated basis has experienced a 3-year CAGR of 17.09%, and since FY21, growth has been above 10%. The high growth in FY22 is mainly due to the low base of FY21, as the industry faced a downturn during COVID-19, because of which FY21’s revenue was quite low.

Export share in the total revenue has remained around 14% except for FY22. However, the numbers have experienced a 3-year CAGR growth of 16.23%

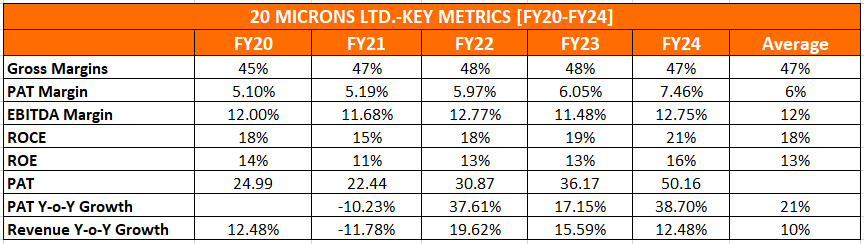

20 Microns Ltd Profitability & Return ratios

The product mix has a significant impact on 20 Microns Ltd. margins, which means that the ratio of high-value to low-value products sold directly affects profitability. 20 Microns Ltd. has a diverse range of products. If the market demand shifts toward lower-value products, the overall margins could decline, as these products tend to generate lower profits. On the other hand, if demand remains balanced across all segments or there is consistent demand for higher-value products, the margins can be maintained or even grow.

20 Microns Ltd. has been able to maintain its gross margin above 45% over the years. EBITDA margin has remained in the band of 11%-13% despite the pandemic. PAT has witnessed continuous growth over the years. PAT margin has been growing over time from 5.10% in FY20 to 7.46% in FY24. PAT growing higher than Sales indicated the presence of financial leverage in the business. The ROCE of the business has been above 15% consistently. ROE has been in the band of 13%-16%, except for FY21, when it was 11%.

20 Microns Ltd Debt and Cash Flow Analysis

Debt to Equity has been on a decreasing trend and stood at 0.30 for FY24. 20 Microns Ltd has utilised its healthy cash flows to bring down the debt level. While CFO/EBITDA has dipped in FY24. the average for 5 years remains healthy

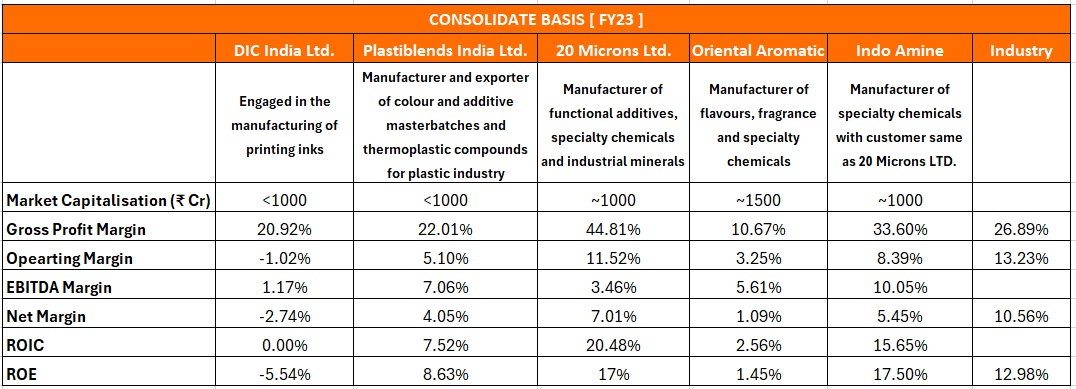

20 Microns Ltd Comparative Analysis

To understand 20 Microns Ltd investment potential, we have conducted a comprehensive analysis. This analysis includes comparing 20 Microns Ltd to its competitors (peer comparison) on various fundamental parameters and 20 Microns Ltd share performance relative to relevant benchmark and sector indices.

20 Microns Ltd Peer Analysis

20 Microns Ltd does not have a single direct competitor across all product lines but instead faces competition from different companies for each product group. 20 Microns Ltd highlighted that there are no other listed companies in India that directly compete with them in these product segments. The competitors are primarily international, and the level of competition varies by product segment.

Below is a comparison with a few listed domestic companies which manufacture products of similar profile to 20 Microns Ltd. These are not exact peers of 20 Microns Ltd, and hence, comparisons should be taken in that context

20 Microns Ltd Index Comparison

20 Microns Ltd share performance vs S&P BSE Small cap Index as the index benchmark comparison is a fundamental tool for understanding the investment potential and making informed decisions in the context of the broader market

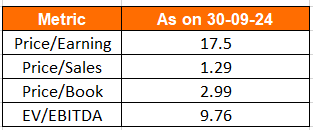

20 Microns Ltd Valuation Ratios

Why You Should Consider Investing in 20 Microns Ltd ?

We believe 20 Microns Ltd. offers some compelling reasons to track the business closely, particularly for those seeking to play proxy to the Paints industry or looking to invest in the industrial minerals and specialty chemicals sectors.

Backward Integrated: 20 Microns Ltd. has its mines and has leased a few. It controls the overall process from production to distribution, enabling the business to cater to specific customer needs and controlling the cost of production and, hence, margins.

Steady Growth: 20 Microns Ltd. has delivered good results in the past 3 years, with Y-o-Y sales growth above 12%. The management expects the sales to grow at 10-15%, and they are highly optimistic about our growth prospects for FY25, backed by a strong order book, strategic initiatives position, and collaboration with new companies.

Expansion in New Geographies: 20 Microns Ltd has expanded its global footprint by entering into new geographies like Poland, Italy, and Russia in FY24 and turning its focus into high-potential geographies like the Middle East and Southeast Asia region while maintaining its presence in the European and American markets, and we could expect an increment in the export revenue in the coming years.

New Product Development: 20 Microns Ltd has added 10+ products to their offerings during FY24, planning to add new products in the future backed by the in-house R&D team. Although contributions from newer products are not very large, this could be a future growth driver.

Stable Margin: Despite the pandemic, High inflation, and geopolitical risks, 20 Microns Ltd. has successfully maintained a stable margin profile over the years, demonstrating the efficiency of its business management. The gross margin has been above 45% in the range of 45%-48%, while the EBITDA margin remained in the band of 11%-13%. The PAT margin is on an increasing trend. These stable margins, even in tough times, are a sign of better control of business.

Strong relationship with existing customers and adding new customers: 20 Microns Ltd is strengthening its relationships with existing customers and also collaborating with new companies. In the B2B segment, 20 Microns Ltd. caters to over 8+ different industries with 200+ clients. They have already onboarded new entrants like JSW & Grasim for paints, and They’re also entering the B2C segment.

China +1: 20 Microns Ltd believes that it could benefit from the shift in supply chains as the world looks to de-risk from its dependency on China, and 20 Microns Ltd is pitching its replacement product to customers to grab some of the market share from China.

What are the Risks of Investing in 20 Microns Ltd

Shorter contract Structure: 20 Microns Ltd does not enter into a long-term contract with its customers, and sales are often based on the demand cycle. So, any volatility in the price of the final product could impact the realisations and inventory losses.

Higher Dependency on the Paints Industry: The majority of 20 Microns revenues are from the paints industry, and as per the segment reporting, a major customer accounts for more than 10% of the aggregate sale. Any disruption related to specific customers and any slowdown in the paint industry may lead to an adverse impact.

Environmental and Regulatory Compliance: Operating multiple mines involves adhering to various environmental and regulatory standards, which can be challenging and costly.

Inability to improve margins in the specialty chemicals and functional additives section: 20 Micron NANO, which focuses on the specialty chemical segment, contributes close to 12% of the total revenue, but their PAT margin is very low – close to 3.52%. The management speaks highly of this segment but its superior quality is still not evident in execution.

Import Price Volatility: 20 Microns Ltd. depends upon foreign raw material suppliers to manufacture goods for export. Major sourcing points are Turkey & Egypt, and geo-political tension around the Red Sea may increase freight costs, and 20 Microns Ltd. will have to compromise its margins.

20 Microns Ltd Future Outlook

20 Microns Ltd is guiding for 10-15% growth & expects margins to remain in the band of 13-15% depending on the product mix.

For base business they want to increase the share of value-added products in their revenue (Functional additives and Specialty chemicals). 20 Microns Ltd will continue to focus on enhancing operational efficiencies, expanding product offerings, and exploring new markets to drive sustainable growth.

For B2C, 20 Micron Ltd is focusing on new product additions along with distribution expansion across pan India, while some of these products might become household names in the future, but not immediately. The strategy here is to create niche products rather than spending very aggressively on marketing. 20 Microns has also formed a JV with Sievert to focus on the building-related chemicals centric on the Indian Market and we got to watch how this makes an impact on the top line of the company. Building a branded B2C business from scratch is not an easy job at all. It needs an extensive product portfolio and a lot of capital to be invested in brand building and setting up a distribution channel.

20 Microns Ltd has also indicated that they may be developing possible chemical solutions for EVs and semiconductors. One has to wait and see if they will deliver anything on this front.

At this point, we are sceptical about return-on-capital accretive growth in the B2C segment of the company. Success in B2C ventures hinges upon scale and building a brand, both of which require capital and a wide product portfolio. The company had ventured into the herbal space but discontinued its operation later. Although 20 Microns Ltd. has been growing well in YoY% terms in the B2C segment, the base revenues here remain too small for the growth to be of any consequence. We need to see how the JV with Sievert works out. Even at 5-fold growth in 5 years, B2C revenues will still be 50 Cr and the vertical won’t even be contributing 5% to the top line in 5 years. So, it’s not a needle mover as of now.

20 Microns Ltd Technical Analysis

We consider technical analysis to be a useful input in taking medium-term investment decisions. Many a time price action tends to lead to fundamental developments; this is too important an aspect to be ignored by retail investors who do not have access to management outside of common forums like investor calls & AGM.

At Congruence Advisers we like to consider both the long-term weekly chart and the daily chart to arrive at a view on price action. Combined with our understanding of fundamentals, we usually end up being better placed to be able to judge both the business cycle and the stock cycle. Playing the stock cycle right is extremely important for investors looking to extract significant alpha over the medium term.

20 Microns Ltd Price Charts

On daily charts 20 Microns Ltd stock formed a nice cup and handle pattern between Dec 2023 and June 2024 and broke out with strong volumes in late June. After consolidating again for a brief period in the 210-230 range in July, 20 Microns Ltd stock broke out with very high volumes and deliveries in the 3rd week of July, suggesting possible institutional entry into 20 Microns Ltd stock 20 Microns Ltd stock moved up sharply from 230 to 340 levels in the span of a month. Since then 20 Microns Ltd stock has been consolidating. At present it is taking support at the 20 DMA. Given the business quality and the forward guidance, 20 Microns Ltd stock does not seem overvalued. So the August pull back lows of 285 or the 50 DMA levels of 280 should hold for the short term.

On weekly charts, we can see that 20 Microns Ltd stock consolidated in a horizontal channel between 60 and 110 from Jan 2022 to July 2023. After that it broke out without much of a volume spike and quickly moved to 190 levels in 4 months. After that it entered a period of consolidation again for 7 months, forming a cup and handle pattern before breaking out with high volumes in June. There was significant delivery based buying in July which took 20 Microns Ltd stock to 340 levels. 20 Microns Ltd stock seems to have entered another consolidation phase since the sharp up move. The August pullback lows of 285 should act as support if the execution momentum continues and the broader market health does not deteriorate significantly.

20 Microns Ltd Latest Result, News and Updates

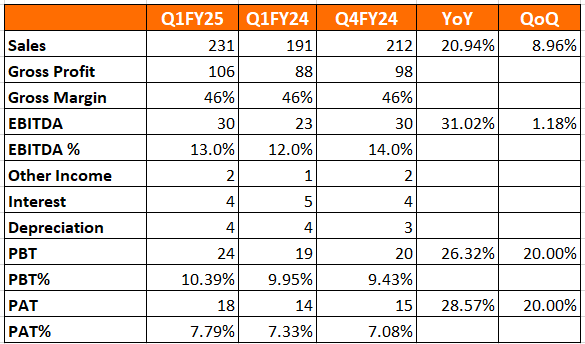

20 Microns Ltd Quarterly Result

20 Microns Ltd. posted its best-ever quarter in Q1 FY25 with sequential growth of 8.96% & 20.94% YoY (2nd consecutive quarter with 20%+ YoY growth); growth is driven by strong demand for products across key markets and a robust distribution network. 20 Microns Ltd is strengthening its capitalization on emerging opportunities and relationships with existing customers. EBITDA% is well within the guided range of 13-15%.

While the paints industry is witnessing a slowdown in growth, Management believes this is a temporary phase, and the volumes will be back in the future. Looking ahead, 20 Microns Ltd is highly optimistic about growth prospects for the remainder of FY25. Backed by a strong order book, strategic initiatives position, and collaboration with new companies

20 Microns Ltd has entered into a definitive agreement to acquire 100% equity interest in GTLQ SDN BHD and IQ Marbles SDN BHD, which owns high-quality mining reserves spanning over 23.90 acres in Ipoh Malaysia with an estimated reserve of 11 million MT, ensuring long-term supply assurance for customers, expanding footprint in Malaysia and enhancing production capacity.

Final thoughts on 20 Microns Ltd

This is a tricky one indeed! What caught our attention was the very steady growth in revenue over the past decade with just one down year in FY21. Operating margins have been very steady since 2016 and the business has used operating cash flow to reduce debt steadily over the years. This kind of financial discipline is very impressive for a sub 1000 Cr market cap business.

If so, what should stop one from becoming very optimistic about the prospects for the business? One simple and very important variable – total addressable market and the revenue growth rate of the business. The Indian market has a special love for high growth businesses that manage to double PAT every 3-4 years, even if unit economics isn’t very steady or predictable year to year. Healthy growth tends to dominate all other factors in the public markets in India across cycles, conversely the market rarely gets excited about good business that do not grow fast. Especially in the microcap segment where investors are always looking for the next big thing. From what we have observed, no investor ever buys a microcap for stability – this might explain why a good business like 20 Microns Ltd has struggled for more than a decade to trade a TTM PE of more than 20. Not surprising in a country like India where the nominal GDP growth rate is expected to be in double digits. Why would one invest in a microcap when one can get the same stability from a HUL or an ITC?

Investors looking to invest in such micro caps should do a lot of qualitative work on establishing realistic growth for such a business. The lack of listed peers and the lack of regular investor conference calls makes this a tough endeavour for the average investor. One will need to invest significant primary effort in speaking to the management, customers, vendors and employees to build a well rounded view of an industrial business.

The clinching factor would be this snapshot. Observe the trend of long term growth in revenue, profits and stock price CAGR over the past 18 months.

We believe that there is always a time and valuation to consider such businesses which are clearly doing many things right, but have not yet figured out a high growth template for itself yet. When the growth potential is hazy, businesses should be bought at the lower end of the PE range the business has traded at over the past decade. Unless the business grows at 15% p.a. over the next 3 years, we are unlikely to see a rerating of this stock. At CMP the business already trades in the 18-20 TTM PE range, a range that has acted as a ceiling in the past for the stock.

We will soon know whether the stock was just a beneficiary of the small & micro cap rerating seen over the past 12-18 months or if the business has an ace up its sleeve that we aren’t able to identify yet. We are always rooting for businesses and entrepreneurs to succeed and deliver great numbers, but the history of growth in this business is average at best.

Wait and watch would be our verdict right now.

Disclaimer – This note is part of a business research & analysis series on small companies, there is no BUY/SELL recommendation or target price issued as part of this. There is no assurance that this stock makes for a good investment, there is no guarantee that this stock will be included in the coverage universe of Congruence Advisers. The note contains some forward-looking statements and insights drawn from the historical results, annual reports and investor presentations; they are to be viewed only within this context and not as a prediction of future performance of the business or the stock covered.

While due care has been taken to ensure that the information here is as accurate as possible, Congruence Advisers disclaims any liability in case of any unintentional inaccuracies.

The content does not constitute investment advice.

Disclosure (Updated as of Sep 30, 2024) – No position in the stock in personal portfolio