Established in 2000, Indigo Paints Ltd. has emerged as a leading paint company in India and the fifth-largest manufacturer of decorative paints by revenue in FY24. Indigo Paints Ltd specializes in manufacturing, trading, and selling various paints and allied products, including emulsions, enamels, wood coatings, distempers, primers, putties, and cement paints.

We believe Indigo Paints Ltd can be an interesting investment opportunity in the Indian paint industry due to its strong growth trajectory, driven by differentiated products and strategic market penetration. Indigo Paints Ltd has consistently outpaced industry growth, leveraging innovation, rural penetration, and aggressive marketing. With recent capacity expansions, entry into high-growth segments like waterproofing and industrial coatings, and a robust distribution network, Indigo Paints Ltd is well-positioned for sustained growth whenever the paints industry gets its growth rate back on track.

Indigo Paints Ltd Company Summary

Established in 2000,Indigo Paints Ltd initially started manufacturing lower-end cement paints and gradually expanded the range to cover most segments of water-based paints. Indigo Paints Ltd. has now emerged as a leading paint company in India and the 5th-largest manufacturer of decorative paints by revenue in FY24. Indigo Paints Ltd specializes in manufacturing, trading, and selling various paints and allied products, including emulsions, enamels, wood coatings, distempers, primers, putties, and cement paints.

Indigo Paints Ltd. started operations by focusing on Tier-3 and Tier-4 cities. Having established its presence at the bottom of the pyramid, Indigo Paints Ltd has started focusing on growth in Tier-1 and Tier-2 cities. Indigo Paints Ltd operates 5 manufacturing units across Rajasthan (2), Kerala (1), and Tamil Nadu (2), with a combined installed capacity of ~160,000 KLPA for liquid paints and ~138,000 MTPA for putty and cement paint.

As part of its expansion strategy, Indigo Paints Ltd is increasing the capacity of its Rajasthan facility and recently inaugurated a new water-based paint facility in Tamil Nadu. The facility commenced operations in September ’23 and is running efficiently. Indigo Paints Ltd has established an extensive distribution network across India, comprising 53 depots and 18,105 active dealers, supported by 9,842 tinting machines as of FY24.

In April ’23, Indigo Paints Ltd acquired a 51% stake in Apple Chemie India Pvt Ltd to diversify and expand its operations. Apple Chemie is a rapidly growing entity within the Waterproofing and Construction Chemicals (WPCC) space, specifically focusing on the B2B segment.

Indigo Paints Ltd Management Details

Promoter and founder Hemant Jalan (a chemical engineer) bootstrapped Indigo Paints Ltd in 2000 with an initial investment of Rs 1 lakh. He was 42 when he started this entrepreneurial venture. It was in 1999 when he decided to quit his job. He was working for Vedanta’s Sterlite and heading its copper smelter unit in Tamil Nadu.

In Patna, Jalan had established a small chemical plant for manufacturing the industrial chemical calcium chloride, which was a minor chemical used in cement paint and later expanded to manufacture cement paint in Jodhpur due the raw materials availability. The entire journey until 2014 has been funded through cash flows and bank loans. In 2014, Indigo Paints Ltd. received its first investment from Sequoia (50 Cr).

Hemant Jalan has played an instrumental journey in scaling revenue from around Rs 80 lakh in sales in the first year to 1255 Cr in FY24.

Indigo Paints Ltd – Industry Overview

Indian Paint Industry

The Indian paint industry was valued at approximately Rs. 62,000 Crs in FY23, with the organized sector comprising about 75% of the market. Over the years, the Indian paint industry has experienced significant transformation, driven by rapid urbanization, increasing disposable incomes, and technological advancements. The industry is projected to grow at a CAGR of ~12.7% from FY23 to FY27, reaching a market size of approximately Rs. 1 Lakh Crs.

The organized sector market share increased from 69% in FY19 to 75% in FY24, reflecting steady growth and strengthening dominance in the industry.

The organized segment is expected to gain market share, propelled by network expansion, product innovation, the introduction of economically priced paints, pricing power, and enhanced technological capabilities.

In terms of consumption, the Indian paint industry is broadly divided into decorative and industrial paint segments.

Industrial Paint Industry

This segment constitutes ₹15,500 crore (~25% of the market) and includes paints used for industrial applications such as automotive, marine, protective coatings, and powder coatings. Demand in this sector is influenced by the growth of industries like automotive, manufacturing, and infrastructure development.

Decorative Paint Industry

The decorative paint segment dominates the market, accounting for ₹46,500 Cr (75% of the total industry). Over the years, there has been a shift from traditional whitewash to high-quality paints such as emulsions and enamels.

This segment includes water-based and solvent-based products like:

- Interior and exterior paints

- Primers, enamels, and wood finishes

- Water-based paints: Easy to clean, quick-drying, and eco-friendly, ideal for indoor use.

- Solvent-based paints: Highly durable and glossy but have stronger odors, higher chemical emissions, and longer drying times, making them suitable for tougher finishes.

The demand for decorative paint is driven by real estate growth, with residential, commercial, and institutional building applications. The rising focus on aesthetics has increased demand for interior and exterior paints. Additionally, roofing and flooring paints are gaining momentum, especially in residential construction.

Over the last decade, the average cycle of re-painting the house has gradually reduced from an interval of 7 to 8 years in 2013 to 4 to 5 years in 2023. Earlier, the primary factor for re-painting the house was the life of the paint coat, i.e., re-painting was done only when the paint withered. However, this trend has been changing gradually, with some consumers giving more importance to aesthetics and changing the looks and appearance of their premises at regular intervals even while the existing paint’s condition is good. These behavioral changes in consumer behavior have led to a reduction in the re-painting cycle.

Market Share of Top 5 Players

Despite having over 3,000 paint manufacturers in the country, the industry remained oligopolistic. Asian Paints Ltd. dominated the market with a lion’s share of 63%. The top five players account for around 95+ % of the market.

Recent Entry of New Players

The decorative paints industry was seen by investors as one with clear, well established moats that would protect incumbents from the disruptive entry of new players. Case studies were being written on the vice-like grip that Asian Paints held over the paints market and dealers in Tier 1 and metro cities in India.

This narrative got slightly dented with the entry of JSW Paints in metro India which saw heightened competition in a few clusters with Asian Paints. JSW Paints scaling up revenue to > 200 Cr within a matter of a few quarters did raise a few eyebrows, though it did not dent the narrative of the market dominance of Asian Paints. However, the entry of Grasim Industries with a ~10,000 Cr capex changed the narrative to one of industry disruption. Reports indicate that the strategy of Birla Opus was simple – poach some of the best salesmen and dealers from Asian Paints and wean them away with higher salaries and higher commissions. To put this into perspective, the gross block of Asian paints as of March 2024 was ~12,000 Cr. Grasim Industries capex into paints was announced at ~10,000 Cr which clearly has disruptive potential.

At the height of the narrative it wasn’t just paint companies like Asian Paints & Berger Paints that traded at high valuation multiples, proxy plays like Mold Tek Packaging were also trading at high multiples. Today each one of the businesses has seen growth rates taper down on the back of a muted operating environment; this muted growth outlook along with the disruptive entry of Birla Opus had beaten down the valuation multiples of players across the entire ecosystem.

It is interesting to note that the entire building materials pack has seen a similar valuation multiple derating play out, this tells us that the market might be responding more to a muted growth outlook rather than getting paranoid about loss of market share yet. One will need to see the market share number once the paints industry starts growing at a much healthier rate compared to the growth rates seen since FY24.

Indigo Paints Ltd Product details

1. Cement Paints & Putty – Major contributor: 43-47% of revenue. This category includes exterior cement paints, wall putty, and waterproofing solutions. It is used for surface preparation and long-term exterior protection. Due to high construction activity, it is in high demand in Tier-1 and Tier-2 cities.

2. Enamels & Wood Coatings – Covers enamel paints for metal surfaces and wood finishes. They are used for furniture, doors, and industrial applications. Consistently 22-24% of the product mix, steady demand.

3. Primers, Distempers & Others – Includes primers, distempers, and specialty coatings for base preparation. Used as base layers before paints. 17-20% of revenue, steady market demand.

4. Emulsions – Interior and exterior emulsions are available in various finishes (matte, satin, gloss). Market share declined but bounced back to 16% in FY24.

Product mix as % of sales

Value Growth YoY%

Indigo Paints Ltd Multi-Dimensional Approach

Through a multi-faceted strategy, Indigo Paints Ltd. has solidified its position in India’s competitive decorative paint industry. This includes launching innovative, differentiated products to create unique market demand, investing heavily in marketing to strengthen its primary consumer brand, “Indigo Paints,” strategically situating manufacturing facilities near raw material sources, developing a widespread national distribution network, and deploying tinting machines across its dealer network.

Marketing and Brand Strategy

Indigo Paints Ltd adopted a strategic approach to building its distribution network by initially focusing on Tier III & IV cities and rural markets. These areas offered easier brand penetration and strong dealer influence, allowing the company to establish a solid presence. Indigo Paints Ltd strengthened dealer relationships and brand visibility by introducing unique products in these underserved regions, paving the way for expansion into larger urban markets. This differentiated strategy set Indigo Paints Ltd apart from competitors and contributed approximately 40% revenue growth over the past decade.

Despite competing with established players with decades of presence, Indigo Paints Ltd has built significant brand equity through aggressive advertising and focused brand-building around its differentiated products under a single brand name.

Portfolio Differentiation & innovation

Indigo Paints Ltd has created a competitive advantage with its differentiated product portfolio of “category-creator” and “value-added” products for special applications. Innovations like Metallic Emulsions and Tile Coat Emulsions have set new industry norms and strengthened IPL’s brand and customer loyalty. By introducing new products consistently, Indigo Paints Ltd attracts new customers, retains existing ones, and maintains innovation leadership.

Between FY21 and FY24, Indigo Paints Ltd introduced 13 new products and focused on niche opportunities. In FY24, it forayed into the high-growth waterproofing segment by acquiring Apple Chemie and entered the industrial B2B segment. This strategic move will add to the revenue streams and position Indigo Paints Ltd for long-term growth, making it a good investment in the Indian decorative paint industry.

Distribution Network

Indigo Paints Ltd leveraged its strong relationships in smaller towns and rural areas to expand its reach and offer more decorative paints. This helped Indigo Paints Ltd to diversify its product portfolio and strengthen its presence in the market. Its ability to establish and maintain these dealer relationships is the key to success. By FY24, Indigo Paints Ltd had 18,105 active dealers, 53 depots, and 9,842 tinting machines across India. This network is a big asset for Indigo Paints Ltd to distribute its products efficiently, tap into emerging markets deep into the market, and grow sustainably.

Indigo Paints Ltd Manufacturing Plants & Future Capex Plans

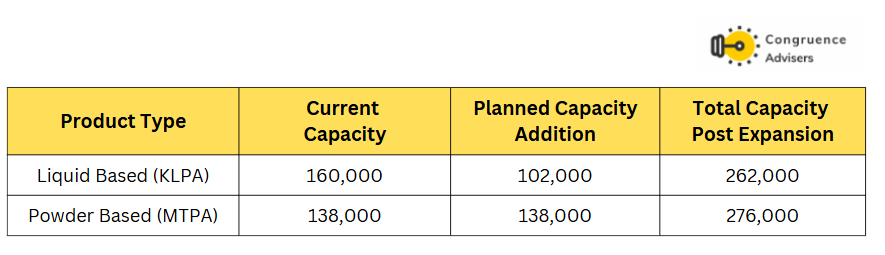

Indigo Paints Ltd operates five manufacturing units across India, including Rajasthan, Kerala, and Tamil Nadu. These facilities have a combined production capacity of approximately 160,000 KLPA for liquid paints and 138,000 MTPA for putties and cement. These facilities are strategically located near raw material sources, reducing freight costs and making procuring raw materials more cost-effective.

Jodhpur, Rajasthan – Produces water-based paints, cement-based paints, and putties. Currently expanding to include a solvent-based plant and an increase in water-based production capacity.

Kochi, Kerala – Specializes in water-based paints. Acquired through the purchase of Hi-Build Coatings Pvt. Ltd. in FY16.

Pudukkottai, Tamil Nadu – Initially focused on solvent-based paints (also acquired via Hi-Build Coatings Pvt. Ltd.). In Q2FY24, the facility was expanded to include a new water-based paint plant.

This strategic advantage combined with higher-margin differentiated products enables Indigo Paints Ltd. to consistently maintain gross margins above the industry average. While the distance between factories and sales points does lead to higher outward freight costs, Indigo Paints Ltd has been able to sustain EBITDA margins on par with competitors.

Indigo Paints Ltd Capex Plans

Indigo Paints Ltd has been steadily expanding its manufacturing capacities to meet rising demand and strengthen its market presence. In Q2FY24, a new water-based facility in Tamil Nadu with a capacity of 50,000 KLPA was commissioned.

Additionally, Indigo Paints Ltd is developing a solvent-based plant in Rajasthan with a capacity of 12,000 KLPA, and a brownfield expansion of putty is expected to be commissioned by Q1FY26. A Water-based plant with a capacity of 90000 KLPA is scheduled to be commissioned by Q3FY26.

Upon completion, Indigo Paints Ltd.’s total production capacity will be ~262,000 KLPA for liquid-based products and ~276,000 MTPA for powder-based products, sufficient to meet market demand for the next few years.

Indigo Paints Ltd is making smart moves to improve efficiency and profitability. With a new water-based facility in Tamil Nadu catering to the southern and eastern regions and a solvent-based plant in Rajasthan serving the northern and western markets. This will help Indigo Paints Ltd to cut freight costs and streamline operations.

Indigo Paints Ltd Corporate governance

Board Composition—The Indigo Paints Ltd. board of Directors has 8 members in total, with 5 independent Directors. The promoter family, the Hemant Kamala(Chairman), has extensive experience in the paints industry. His son Parag Hemant Jalan acts as a Non-Executive Director, and Narayanankutty acts as a Non-Executive Director.

Promoter Remuneration – The total remuneration drawn by promoter remuneration in salaries to ~INR 5.86 Cr in FY24. This amounted to ~3.80% of the PAT of Indigo Paints Ltd. for FY24. For FY23, the corresponding figures were INR 5.27 Cr and ~3.99% of PAT.

Related Party Transactions – Indigo Paints Ltd had no significant related party transactions in FY24.

Contingent Liabilities – Indigo Paints Ltd’s total contingent liabilities on account of GST and Income tax amount to ~INR 21 Cr, which is 2.4 % of its consolidated net worth.

Indigo Paints Ltd Financial Performance

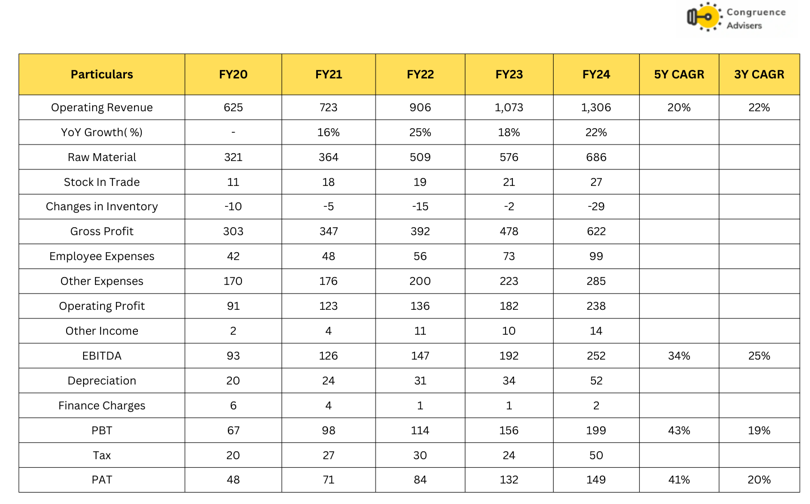

Indigo Paints Ltd.’s printed revenue growth of ~19% on a 5-year CAGR is higher than the industry and peers’ growth. This consistent growth results from Indigo Paints Ltd.’s successful market strategies, product innovation, and expanding distribution network. Additionally, its relatively small base has helped it achieve good financial performance despite intense competition from established players.

Despite this strong GPM, the EBITDA and PAT margins are in line with peers due to the Indigo Paints Ltd smaller size (economies of scale) and slightly higher freight outward & Marketing costs.

Indigo Paints Ltd Return Ratios, Working Capital, Debt, and Cash Flow Analysis.

Indigo Paints Ltd has posted impressive growth over the years, particularly in its cash flow from operations. While Indigo Paints Ltd experienced negative cash flow from operations in FY15 and FY17, it has steadily improved its cash generation, reaching ₹152 crore in FY24. Indigo Paints Ltd’s gross asset turnover has ranged between 2.7x and 3.8x from FY20 to FY24. Indigo Paints Ltd maintains a robust, debt-free balance sheet, with significant improvements in both ROE and ROCE in recent years.

Indigo Paints Ltd Comparative Analysis

To understand Indigo Paints Ltd investment potential, we have conducted a comprehensive analysis. This analysis includes comparing Indigo Paints Ltd to its competitors (peer comparison) on various fundamental parameters and Indigo Paints Ltd share performance relative to relevant benchmark and sector indices.

Indigo Paints Ltd Peer Comparison

Indigo Paints Ltd operates in the Paints Industry. In an oligopolistic industry dominated by five major players: Asian Paints, Berger Paints India, Kansai Nerolac Paints, and Akzo Nobel India, Indigo Paints Ltd is one of the few new entrants who has scaled up and captured market share. This has been a result of a patient and multi-pronged strategy focused on product differentiation, brand building, manufacturing locations, a wide distribution network, and dealer tinting machine installations.

Indigo Paints Ltd has created a space in the highly competitive decorative paints segment by offering innovative products and high-impact marketing spending. Its focus on operational efficiency, evident from improving cash flows and zero debt, has further strengthened its ability to compete with the biggies. This systematic approach has made Indigo Paints Ltd a strong challenger in the Indian paint industry.

Indigo Paints Ltd. has outperformed the peer segment due to its lower base and its focus on a market with relatively lower competition from these market leaders. Asian Paints Ltd has clearly the highest EBITDA% compared to other players, which operate on around 13-16% EBITDA%. Despite its lower scale compared to other players, Indigo Paints Ltd has a healthy PAT% of around 10%. Expect Kansai Nerolac Paints; all peers operate at a healthy ROCE at 24%+. Indigo Paints Ltd has highest A&P spends compared to peers as its focusing on brand building

Indigo Paints Ltd Index Comparison

Indigo Paints Ltd share performance vs S&P BSE Small cap Index as the index benchmark comparison is a fundamental tool for understanding the investment potential and making informed decisions in the context of the broader market

Why you should consider investing in Indigo Paints Ltd

Indigo Paints Ltd offers some compelling reasons to track closely and to consider investing if one is looking to play in the building material sector through the paints industry.

Anticipates to outperform industry growth by 3-4 times – Indigo Paints Ltd has consistently achieved growth rates of 2-3x compared to its peers. This success can be attributed to its multi-pronged strategy, including introducing differentiated products, focusing on rural and Tier III and IV markets, and investing heavily in brand building and advertising. In FY24, Indigo Paints Ltd outpaced industry growth by 2–3 times and remains confident in sustaining this momentum.

Differentiated Product Portfolio & Innovation – Indigo Paints Ltd has created a competitive advantage with its differentiated product portfolio of “category-creator” and “value-added” products for special applications. Innovations like Metallic Emulsions and Tile Coat Emulsions have set new industry norms and strengthened Indigo Paints Ltd’s brand and customer loyalty. By introducing new products consistently, the company attracts new customers, retains existing ones, and maintains its leadership in innovation.

Between FY21 and FY24, Indigo Paints Ltd introduced 13 new products and focused on niche opportunities. In FY24, it forayed into the high-growth waterproofing segment by acquiring Apple Chemie and entered the industrial B2B segment. This strategic move will add to the revenue streams and position Indigo Paints Ltd for long-term growth, making it a good investment in the Indian decorative paint industry.

Capacity expansion – Indigo Paints Ltd. is strategically expanding its manufacturing capacity to meet rising demand and strengthen its market position. In Q2FY24, it inaugurated a 50,000 KLPA water-based facility in Tamil Nadu and is developing a 12,000 KLPA solvent-based plant in Rajasthan. It plans to scale its water-based capacity to 90,000 KLPA by FY26. After completion, Indigo Paints Ltd’s total production capacity will reach ~262,000 KLPA for liquid-based products and ~276,000 MTPA for powder-based products, ensuring sufficient supply for the next five years.

Extensive distribution network and proximity to raw material sources –As of FY24, Indigo Paints Ltd.’s strong distribution network includes 18,105 active dealers, 53 depots, and 9,842 tinting machines across India. This network enables Indigo Paints Ltd. to effectively distribute its products and capitalize on emerging market trends.

Indigo Paints Ltd operates five manufacturing units in India, located in Rajasthan, Kerala, and Tamil Nadu. It strategically positions its manufacturing facilities near raw material sources, reducing inward freight costs and lowering overall raw material expenses. This cost advantage, combined with its portfolio of high-margin, differentiated products, allows it to maintain consistently higher gross margins than industry peers.

What are the Risks of Investing in Indigo Paints Ltd

Investors need to keep the following risks in mind if they choose to invest into this business. Risks needs to be weighed in combination with the advantages listed above to arrive at a decision that is optimal for your portfolio construct

Raw Material Risk – Indigo Paints Ltd.’s raw materials comprise binders, fillers, different variants of cement, etc., which are largely procured from the domestic market. Further, raw materials like pigments, solvents, Tio2, and resins are derivatives of crude oil. The volatility in crude oil prices also has a direct impact on the raw material cost.

Intense Competition – The paint industry is highly competitive, with both established players and new entrants striving for market share. Increased competition could lead to pricing pressures and affect profit margins.

Aggression by leaders in rural markets – The Increasing Focus of Market leaders like Asian Paints, Berger Paints, and Nerolac in rural and semi-urban markets poses a significant risk to Indigo Paints. These larger competitors have deeper financial resources, wider distribution networks, and strong brand recall, allowing them to undercut prices, offer better dealer incentives, and expand their product portfolios.

Indigo Paints Ltd Future Outlook

Indigo Paints Ltd Technical Analysis

We consider technical analysis to be a useful input in taking medium-term investment decisions. Many a time price action tends to lead to fundamental developments; this is too important an aspect to be ignored by retail investors who do not have access to management outside of common forums like investor calls & AGM.

At Congruence Advisers we like to consider both the long-term weekly chart and the daily chart to arrive at a view on price action. Combined with our understanding of fundamentals, we usually end up being better placed to be able to judge both the business cycle and the stock cycle. Playing the stock cycle right is extremely important for investors looking to extract significant alpha over the medium term.

Indigo Paints Ltd Price charts

On a Weekly Chart, The Big spike in volume in September indicates the exit of the venture capital firm Peak XV Partners offloaded a 22% stake through a block deal. Indigo Paints Ltd has been downtrend since its listing, with recent price action forming a downward channel. Indigo Paints Ltd stock is approaching a key support level of around ₹990, which has historically acted as a strong base. If it holds, a rebound towards ₹1,670 resistance is possible, but with this market condition, a breakdown could lead to further downside.

Indigo Paints Ltd Latest Result, News and Updates

Indigo Paints Ltd Shareholding Pattern Analysis

In September 2024, Venture capital firm Peak XV Partners (earlier known as Sequoia Capital), through its two affiliates, Peak XV Partners Investments IV and Peak XV Partners Investments V, offloaded a total of 1.05 Cr shares, amounting to a 22 % stake. After the latest transaction, Peak XV Partners Investments IV’s shareholding declined to 1.54 % from 12.14 %, while Peak XV Partners Investments V’s stake came down to 1.65% from 13.09 %.

Meanwhile, Nippon Life, HDFC Mutual Fund, New York-based consulting firm Mercer, and Morgan Stanley bought shares in a block deal.

Indigo Paints Ltd Quarterly Results

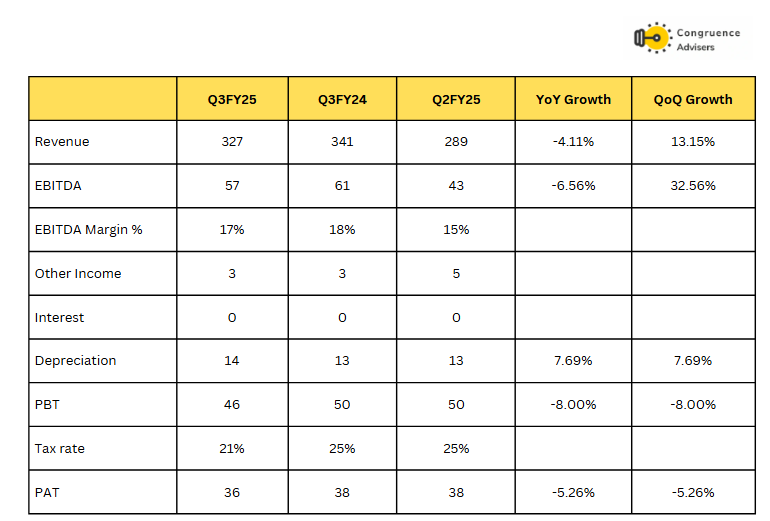

Indigo Paints Ltd’s revenue declined by -3.2 % in Q3 FY25 (First -ve growth) due to the overall demand slowdown due to the poor festive season. While the emulsion segment grew on the back of strong performance in the premium segment

GPM declined ~155 bps YoY to 46.6% due to price cuts, product mix changes, and weak margin on Apple Chemie. EBITDA% also fell 90 bps YoY, mainly due to lower GM and weak operating leverage, partly offset by lower A&P spending. Indigo Paints Ltd follows industry leaders on pricing, maintains high trade discounts, and is shifting A&P spending from TV to digital.

January showed some recovery and management is cautious for Q4FY25, Guiding for high single-digit growth and expecting margins to improve in Q4FY25 due to seasonality and product mix improvement.

Apple Chemie grew 20.6% YoY, but margins were impacted by an adverse product mix, which will improve in Q4. The contribution of the waterproofing and construction chemicals segment (7 products) to total sales is in the mid-single digits.

On capacity expansion and capex, Indigo Paints Ltd has delayed the commissioning of the Jodhpur water-based plant to Q3FY26. Jodhpur solvent-based plant will be ready by Q1FY26, and Jodhpur putty brownfield expansion will also be ready by Q1FY26. All investments are being funded through internal cash accruals.

Final Thoughts on Indigo Paints Ltd

Indigo paints has many points in its favour right now –

- Industry leading growth rate

- Niche positioning with minimal exposure to metro & Tier 1 India

- A well funded capex on the verge of completion

- Exit of incumbent large investor is already behind us

- Debt free balance sheet, good cash flow profile

- A very competent and proven management team

- Lower advertising spend as % of revenue compared to history

- Reasonable valuation multiple (<33x TTM PE) for the first time since listing

A cursory look at the numbers of 9M FY25 indicate that the higher base of depreciation is already accounted for starting from Q3 FY25, operating leverage from here can play out once growth reverts to a healthy rate. Once the entire capex is finished by Q2 FY26, Indigo paints can double its revenue without the need for more capex.

The business has the potential to grow revenue and profits at a very aggressive pace as and when the paints industry gets back on the growth trajectory. The big question right now is if the paints industry can get back to its growth trajectory in H1 FY26.

Disclaimer – This note is part of a business research & analysis series on small companies, there is no BUY/SELL recommendation or target price issued as part of this. There is no assurance that this stock makes for a good investment, there is no guarantee that this stock will be included in the coverage universe of Congruence Advisers. The note contains some forward-looking statements and insights drawn from the historical results, annual reports and investor presentations; they are to be viewed only within this context and not as a prediction of future performance of the business or the stock covered.

While due care has been taken to ensure that the information here is as accurate as possible, Congruence Advisers disclaims any liability in case of any unintentional inaccuracies.

The content does not constitute investment advice.