Oriental Aromatics Ltd is one of the largest manufacturers of specialty-based aroma chemicals and camphor. Its product range includes Synthetic Camphor, Terpineols, Pine Oils, Astramusk, and other specialty aroma chemicals used in various industries, such as Cosmetics, Soaps, Pharmaceuticals, etc. Oriental Aromatics has four Manufacturing Sites across India, two R&D centres, and process Re-Engineering Labs.

Can Oriental Aromatics Ltd be a good tactical play on camphor pricing & capacity utilisation ? – Oriental Aromatics Ltd is well-placed to deliver strong growth with capex projects nearing completion. Oriental Aromatics Ltd now can generate 1200 Cr peak revenue (at current prices) this provides greater growth visibility for FY26, with operating leverage expected to improve margins. Additionally raising camphor pricing further increases the likelihood of higher profitability with management confident of achieving 10-12% EBITDA% in FY25. Oriental Aromatics Ltd has shifted its focus on increasing capacity utilisation and debt reduction.

Oriental Aromatics Ltd Company Overview

Oriental Aromatics Ltd is a publicly listed company that manufactures various terpene chemicals, camphor, specialty aroma chemicals, fragrances, and flavours. Oriental Aromatics Ltd product range includes synthetic camphor, terpineol, pine oil, resins, astromusk, perfumery chemicals, fragrances and flavours, and other chemicals used in different industries (such as pharmaceuticals, soaps and cosmetics, rubber and tires, paints and varnishes, and FMCG).

Oriental Aromatics Ltd. was founded by Mr.Keshavlal Bodani in 1955 and has been nurtured and handed down to three generations of the Bodani family. In August 2008, Oriental Aromatics Ltd. acquired a controlling stake of 57.66% in the listed entity of Camphor & Allied Products Ltd. (CAPL), a key supplier of camphor and other specialty aroma chemicals. Furthermore, in April 2017, Oriental Aromatics was fully amalgamated into the listed entity, and after that, the name of CAPL was changed to Oriental Aromatics Limited (OAL).

Oriental Aromatics Ltd. has four manufacturing plants at Nandesari (Vadodara, Gujarat), Bareilly (Uttar Pradesh), and Ambernath (Maharashtra). Oriental Aromatics Ltd is starting a new unit at Mahad, Maharashtra, under its wholly owned subsidiary, Oriental Aromatics and Sons Limited.

Some key aspects of Oriental Aromatics Ltd

- One of the leading non-spice aroma chemical producers in the country, a Top 4 player

- One of the largest camphor makers in the country, it focuses on the pharma-grade segment.

- The client base in the F&F segment consists of domestic non-MNC FMCG companies, while that in the aroma chemicals segment consists of the Top 10 global giants in the F&F space.

- One of the largest global players in astro musk, a well-known fragrance ingredient.

- 45% of revenue comes from exports, primarily from the aroma chemicals segment, which is set to grow at a healthy rate over the medium term.

- Raw material dependence on China reduced to below 10% from 60%+ 10-12 years ago.

- All acquisitions done by Oriental Aromatics Ltd so far have been for capability and not for scale. Mainly to enhance the product portfolio and derive synergies.

Oriental Aromatics Ltd Management Details

Dharmil Bodani – An elder member of the third generation, Dharmil Bodani has been involved in the business since completing his education. Has witnessed the company scale grow from 70 Cr to 800 Cr, aged ~53 years

Shyamal Bodani – Dharmil’s younger brother, aged close to 43 years, Shyamal Bodani has been involved in the business after completing his education. Both brothers were educated outside India.

Satoskar couple – Acquired during the Arofine Chemicals takeover, Parag is now the Group CEO, while Anita is the Chief Technology Officer.

Promoters have an active Page 3 lifestyle and Bollywood connections. They run no other businesses and are focused on Oriental Aromatics Ltd. As a social initiative, they run one of the best schools in Mumbai for slow learners; one of the promoters’ children is a special child.

Oriental Aromatics Ltd – Industry Overview

FRAGRANCE & FLAVOUR MARKET

The market size is around USD 32.2 Bn. The expected growth rate is 4-5% p.a. With developing markets, the industry tends to grow at a faster pace than the global average.

The industry structure is consolidated, with a 60+% market share concentrated among the top four players. Heartland European players like Givaudan, Firmenich, Symrise, and Mane have dominated the market, with IFF being the other Top five player.

Regionally, Asia Pacific continued to dominate the global F&F industry in 2023, with the largest revenue share of over 32%, led by a large population in China and India.

India’s domestic F&F market is USD 1.5 Bn, and the same global MNCs dominate it with an India-based manufacturing presence. Oriental Aromatics Ltd and SH Kelkar (Keva) are among the few Indian players, but they are nowhere comparable to the scale of the MNCs. As a thumb rule, MNC FMCG companies work with their MNC F&F counterparts since they have a large library of flavours and fragrances that can be replicated in India. The Indian F&F makers work primarily with non-MNC FMCG companies.

- F&F makers are backward integrated for in-patent molecules while following outsourced production once the molecule goes off-patent and becomes a commodity.

- M&A activity in F&F has been high across the world. Big players are becoming bigger through the inorganic route. Organic growth is hardly expected to be 4-5% for the best players.

- Leading F&F makers spend around 7-8% of sales on R&D and have access to a large library of fragrances and flavours that can be tapped into; smaller players cannot compete.

- All large F&F makers have plants in India and have invested impressive sums in recent years (2000-2500 Cr investments over the years)

AROMA CHEMICALS MARKET

The aroma segment typically accounts for 25% to 30% of the F&F market size and is estimated at around USD 5.56 Bn. Growth rates are tied to FMCG growth rates, as is the case with the F&F makers. Almost 70% of the global capacity of aroma chemicals is with leading F&F players that are also backward integrated and standalone aroma chemical makers based in China and India.

Aroma chemicals can be produced using both natural and synthetic methods. The synthetic method accounted for a 69.20% revenue share (in FY23). Many synthetic aroma chemicals are derived from terpenes (hydrocarbons commonly found in plants). The terpenes chemical segment accounts for 39%, i.e., the largest market share within aroma chemicals.

India is the market leader for spice-based aroma chemicals. It is mainly dominated by Kerala-based companies like Synthite, Plant Lipids, Kancor, and VKC Seasoning, as they have captive access to raw materials. Synthite is the largest player and has scaled to 2000 Cr of revenue in FY23, with EBITDA% at 16%.

Camphor Market

India is 2nd largest camphor importer globally and sources camphor from countries like China, Germany, and the United Kingdom.

There are two types of camphor in the market : natural camphor and synthetic camphor. Natural camphor is made from the wood and bark of the camphor tree, which is primarily found in China, Taiwan, southern parts of Japan, Korea, and Vietnam. Synthetic camphor is produced from pine trees and is more cost-effective and scalable than Natural camphor.

Although India has plenty of pine trees, it produces only 17% of its camphor needs. The majority, about 80%, is imported. This highlights the need for camphor companies to rely on imported turpentine. Camphor capacity available in India is primarily synthetic camphor (i.e Pinene into camphor), While natural camphor is imported from China it presents challenges in product handling due to its higher purity. Additionally, its binding strength complicates its use in the Indian context.

The camphor market is moderately fragmented, with several key players holding significant market share due to their well-established supply chains, technological capabilities, and large customer bases spread across various industries. Oriental Aromatics Ltd is a dominant player in the synthetic camphor market, accounting for 35-40% of the global market. Given its leadership in key categories like synthetic camphor and astride musk, Oriental Aromatics Ltd supplies over 50% of P&G’s global requirement for camphor used in Vicks.

Over the past two decades, there has been a tangible shift in the manufacturing of many chemicals from Europe and other developed regions to the APAC region. While China is the largest manufacturer of a wide range of chemicals (API, intermediates, bulk chemicals & specialty chemicals), India has been steadily emerging as an alternative to China over the past decade. Chemical manufacturing is known to be polluting and has high fixed costs, limited pricing power, and high environmental and social compliance costs. A bulk of the manufacturing shift to India and China until 2015 can be explained by the lower cost of land acquisition, manpower, and compliance costs compared to developed markets. Ever since China started clamping down on polluting manufacturing units closer to Beijing, there was a white space in the market that many Indian businesses have managed to tap into.

The COVID dislocation of 2020 and the subsequent supply chain volatility resulted in abnormal profits for the chemicals makers for 12-15 months, and the entire cycle has been reversed since then. Chemical prices since 2022 have fluctuated wildly to the downside, depressing margins and pricing for players across the value chain. While the China plus one narrative has resulted in better growth visibility for many players, the lack of pricing power and resurgence of Chinese dumping have made the journey quite volatile.

Aroma chemical makers like Privi Specialty and Oriental Aromatics have borne the brunt of the pricing dislocation, as have other chemical players. Though they are among the largest aroma chemicals makers in India, they are still small players in the global scheme of things, especially seen in the context of the scale of their customers. Global F&F players are known to be tough negotiators given that they, in turn, sell to large, concentrated buying centres. The entire value chain needs quality and reliability, but the customers wield excessive power, resulting in very limited pricing power for the suppliers. The industry mostly operates on a cost-plus margin model where 6–12-month supply agreements are signed with customers. While input prices are passed on with a lag, the ability of suppliers to preserve margins is very limited.

Oriental Aromatics Ltd Product Details

Oriental Aromatics Ltd offers a wide range of products across several categories, catering to various industries such as fragrances, flavours, aroma chemicals, and camphor products.

Key product categories:

- Fragrances: Oriental Aromatics Ltd manufactures complex fragrance compositions used in perfumes, personal care products, and household applications. Their fragrances are created from a blend of natural and synthetic ingredients.

- Flavours: Oriental Aromatics Ltd produces flavouring agents used in food and beverages. These flavours are used in various products, from bakery items to dairy, and they ensure safe, high-quality formulations.

- Aroma Chemicals: Oriental Aromatics Ltd is known for its production of several key aroma chemicals that are crucial in the perfume, food, and cosmetics industries. These chemicals form the backbone of many fragrance and flavour formulations.

- Camphor: Oriental Aromatics Ltd manufactures and supplies camphor products used for medicinal, religious, and household purposes. Camphor is a key ingredient in balms, creams, and other products used for relief from colds, coughs, and pain.

Oriental Aromatics Ltd revenue is split equally across all three of their divisions – Flavors & Fragrances, Aroma Chemicals and Camphor

In the Specialty Aroma Division, certain global RFQs contracts have fixed prices of around 6 months, after which they are renegotiated, while F&F products have offered longer price stability, and camphor and terpene chemicals are mainly sold at spot price, especially in India.

During the COVID-19 pandemic, there was a big increase in demand for camphor-based products like balms, vapour rubs (such as Vicks), and disinfectants. These products became essential as camphor is commonly used in treatments for respiratory issues.

Oriental Aromatics Ltd, being a large supplier and contributing 50% of P&G’s global Vicks requirement, Oriental Aromatics Ltd has capitalised on this industry tailwind, which led to high abnormal profitability with EBITDA% at 22% (the highest ever in its history) majorly driven by higher realisation and lower RM costs. However, this favourable environment reversed post-FY21 as prices have fluctuated wildly to the downside, along with normalised RM prices, which has resulted in lower margins for Oriental Aromatics Ltd and other players.

Oriental Aromatics Ltd announced significant capex plans in FY21 for 250-300 Cr (majorly funded by debt) spread across 3-4 years at the peak of the cycle for expanding its Vadodara for Specialty aroma chemical products and a greenfield project at Mahad (Maharashtra). While the environment started getting unfavourable, management decided to downsize its CAPEX plan. Meanwhile, Both projects have witnessed delays due to multiple reasons like residual COVID–19 impact, challenges in the global supply chains, steel prices, and geo-political situation due to the Russia-Ukraine crisis; fast forward to Q1FY25, the brownfield project at the Vadodara site was successfully commissioned (end of Q1FY25) with cost of Rs 45-50 Cr, and the greenfield project in Mahad (Maharashtra) has reached an advanced stage to start contributing to topline form H2FY24 with incurred cost of Rs 140-150 Cr under its wholly-owned subsidiary, Oriental Aromatics and Sons Limited.

In FY21, Oriental Aromatics Ltd had a debt of approximately Rs 78 Cr, which increased to 206 Cr by FY24 due to ongoing capex. Management has indicated that peak debt is expected to reach Rs 280 Cr by FY25, and the focus has now been shifted to reducing debt and increasing utilisation of recently completed capex before considering any new capex.

Post-printing higher profitability in FY21 (EBITDA at 22%), the margin has trended lower and dropped to single digits in FY24. This consistent pressure on margins was due to increased domestic capacities and an influx of camphor imports from China. Additionally, weak demand in the European and American markets has limited realisations and profitability in the specialty aroma chemicals segment.

While the depressing situation has begun to ease, and some recovery is anticipated, which will lead to improved profitability in FY25 & FY26. Even Oriental Aromatics Ltd management is confident of achieving a 10-12% margin in FY25. Meanwhile, profitability is unlikely to return to the earlier high levels, such as in FY21.

The camphor market is facing a demand-supply mismatch, where supply is exceeding the demand, leading to intense pricing pressure on products like camphor powder and other terpene chemicals. The situation got even worse in H1FY23 when pinene prices dropped to an all-time low, impacted by global headwinds. This further impacted the profitability and has led to huge inventory losses for Oriental Aromatics Ltd in its camphor division, which has resulted in PBT losses in the last few quarters.

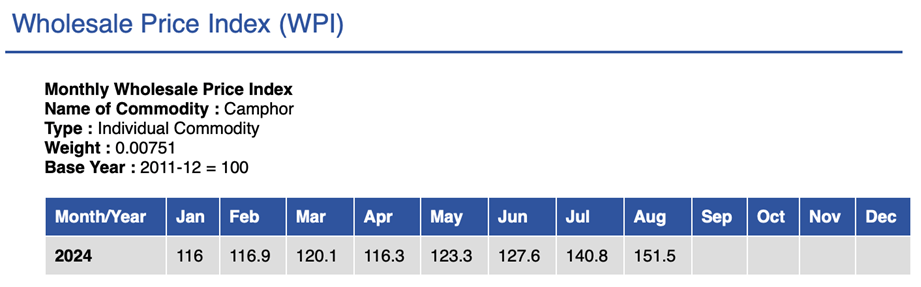

Q1FY25 has started with some positive notes as camphor pricing improved, and RM prices are increasing at a stable rate & able to pass on to customers. Oriental Aromatics Ltd managed to increase the price of camphor and passed the price increase to most of their customers. The upcoming festival season is expected to increase the demand for high-quality camphor, which will be an encouraging sign of revival.

Source: eaindustry.nic.in

Camphor prices have probably made a bottom on April 24 and have been on the rise for the last four months. Going by the commentary of Oriental Aromatics Ltd and other listed camphor players, the prices are expected to remain in a positive trend

Oriental Aromatics Ltd Manufacturing Facility

- Bareilly, Uttar Pradesh:

- Established in 1964, it is India’s first synthetic camphor plant, using DuPont technology.

- Produces approximately 7,900 MTPA of pine-based chemicals and related products.

- Focuses on camphor and specialty aroma ingredients, with WHO-GMP and USFDA certifications.

- Vadodara, Gujarat:

- This plant, established in 1999 and expanded in 2018, specialises in aroma chemicals.

- Production capacity of 6,200 MTPA, with 75% of production being exported.

- Manufactures a wide range of aroma ingredients sourced from pinene, petrochemicals, and other raw materials.

- The hydrogenation plant, a brownfield project at the Vadodara site, was successfully commissioned, and commercial production commenced on 30th July 2024.

- Capex for the brownfield project is 40-50 Cr, expected to contribute 1.7x turnover.

- Ambernath, Maharashtra:

- A highly versatile plant commenced in 2014, with a production capacity of 6,000 MTPA.

- Produces both fragrances and flavours, equipped with state-of-the-art R&D and quality assurance (QA) infrastructure.

- Ambernath, Maharashtra:

- Advanced facility focuses on aroma chemicals and aims to bolster innovation and reinforce market leadership.

- The Greenfield project in Mahad, Maharashtra, has reached an advanced commissioning stage and is expected to start contributing towards the topline from the H2FY24

- Capex for the greenfield project is 100-120 Cr, expected to contribute 1.2x turnover.

Oriental Aromatics Ltd Corporate governance

Board Composition – As of FY24, there are 9 directors on the Oriental Aromatics Ltd board, of which 2 are executive directors. The remaining 6 are independent and non-executive directors, Bringing a diverse range of expertise.

Promoter Remuneration – The total remuneration drawn by promoters of Oriental Aromatics Ltd in FY24 was ₹9.21 Cr in the form of salary, which is 100% of the FY24 Net Profit. (number has been optically higher since profitability has been lower since last few years)

Related Party Transactions – Oriental Aromatics Ltd does not have any material related party transactions that may potentially conflict with the interests of Oriental Aromatics Ltd at large.

Contingent Liabilities – As of FY24, Oriental Aromatics Ltd contingent liability amounts to ₹45 Cr (7% of net worth), which increased when compared to 13 Cr in FY23

Dividend Policy – Oriental Aromatics Ltd has consistently distributed dividends since FY18, except for FY23. For FY24, the total dividend payout will be ₹1.68 Cr. The payout has decreased over the years.

Oriental Aromatics Ltd Financial Performance

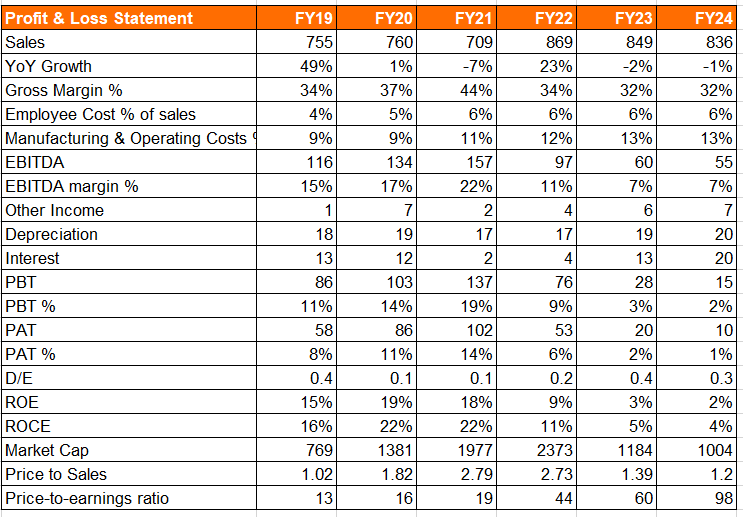

Oriental Aromatics Ltd has displayed flat performance between FY19-FY24. Revenue in FY24 was at ₹836 Cr, which remained flat since FY19 at 2% CAGR. Gross margin fluctuates in the range of 30-44%. Revenue has been stagnant for 6 years, whereas the rest of the leading players in Flavours and Fragrances and Aroma Chemicals players have managed to grow volumes and revenues & while Mangalam Organics and Kanchi Karpooram. Camphor-focused players have shown degrowth over this time frame. EBITDA margins have fluctuated between 7-22%, with a severe drop to 7% in FY23 & FY24. PAT margins have also been in the 1%-14% range. As a result, the average ROE over this period has averaged 10% respectively.

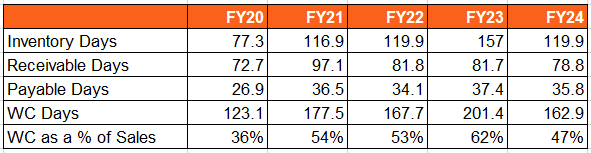

Oriental Aromatics Ltd Working Capital Analysis

Oriental Aromatics Ltd has a consistently high working capital intensity business, with the Net working capital to sales increasing in the last few years. While it has improved in FY24. Higher working capital is mainly due to higher holding periods and extended debtors’ duration. Inventory levels in the fragrance segment are generally higher, i.e. products remain in stock for approximately 5-6 months. At its facilities in Bareilly and Baroda, Oriental Aromatics Ltd generally keeps raw material inventories for 2 to 3 months. Also, Oriental Aromatics Ltd purchases RM on spot prices from suppliers, which requires immediate payment, versus long-term contracts with larger payable days. Occasionally, Oriental Aromatics Ltd utilises Letters of Credit to secure credit, which can sometimes be converted into buyers’ credit arrangements.

For its export clientele, Oriental Aromatics Ltd offers a credit period of 120 to 150 days and extends up to 180 days for certain customers involved in specialty chemicals and fragrances.

Oriental Aromatics Ltd Comparative Analysis

To understand Oriental Aromatics Ltd investment potential, we have conducted a comprehensive analysis. This analysis includes comparing Oriental Aromatics to its competitors (peer comparison) on various fundamental parameters and Oriental Aromatics Ltd share performance relative to relevant benchmark and sector indices.

Oriental Aromatics Ltd Peer Comparison

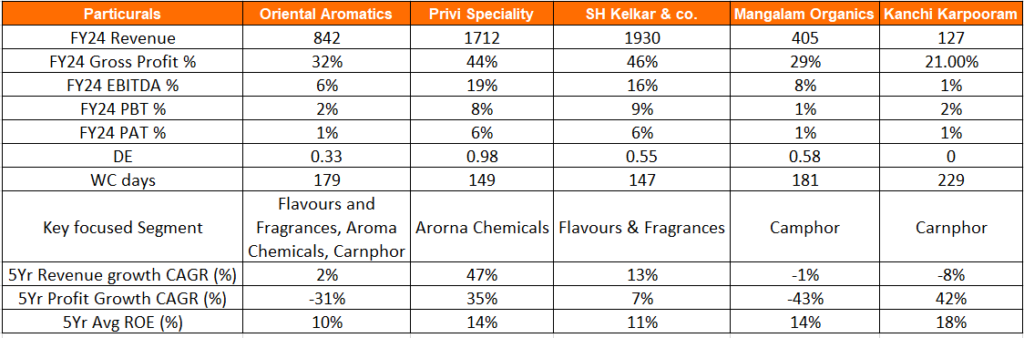

We have compared Oriental Aromatics Ltd. with its listed domestic peers like Privi Speciality Ltd, SH Kelkar Ltd, Mangalam Organics Ltd, and Kanchi Karpooram. This would give us a better understanding of where Oriental Aromatics Ltd. stands in the industry.

While the international peer group comprises behemoths like Givaudan, IFF, Symrise, Firmenich, Mane, Takasago, etc.

- Gross Margins for leading global F&F players is around 40%

- Pre-R&D EBITDA margin in the range of 25-28% for the global F&F players

- Working capital cycle of approx. 100-120 days

- For aroma chemicals makers, the gross margin is around 35-38%

- Both F&F and aroma chemicals makers operate at 2–3x gross asset turns.

- To make a pre-tax ROCE of 20% and higher, the EBIT margin has to be at least 13-14%, given that the domestic players operate at around 120-140 days of working capital.

Oriental Aromatics Ltd is significantly smaller than international players, with revenues far lower than giants like Givaudan and IFF. Margins (gross and EBITDA) are considerably lower for Oriental Aromatics, indicating it faces cost pressures or low pricing power compared to international peers.

Oriental Aromatics Ltd Index Comparison

Oriental Aromatics Ltd share performance vs S&P BSE Small cap Index as the index benchmark comparison is a fundamental tool for understanding the investment potential and making informed decisions in the context of the broader market

Why You Should Consider Investing in Oriental Aromatics Ltd?

Oriental Aromatics Ltd offers some compelling reasons to track the business closely and to consider investing if one is looking to play tactical play on increasing capex utilisation and rising camphor prices

Capex set to new growth – Since 2020, Oriental Aromatics Ltd. has navigated extreme market conditions, from pandemic-induced demand spikes to post-pandemic margin pressures due to volatile chemical prices and increased competition. However, Oriental Aromatics Ltd. is now at an inflection point, with its capex projects nearing completion. This will provide a higher runway for growth and earning visibility in FY26, with operating leverage expected to improve margins. Oriental Aromatics Ltd. is well-placed to deliver growth.

Revenue Guidance – Historically, Oriental Aromatics Ltd has generated around Rs 900 Cr in revenue before the CAPEX initiative. With the completion of current projects, the management anticipates peak contribution from these initiatives to potentially add up to Rs 1200 Cr in revenue, assuming stable selling prices and market conditions.

EBITDA Margin – The Q2FY25 and Q3FY25 results are expected to improve significantly, with management guiding for EBITDA of 10-12% in FY25 compared to single digits in FY24. If camphor prices sustain the rise, which is highly likely, EBITDA% could exceed expectations, as the camphor division (currently at EBITDA+) and 1/3 of revenue with operating leverage in play, PAT could potentially see improvement from here. Oriental Aromatics Ltd camphor division is set to contribute more positively due to the ability to pass on raw material price increases to customers and a focus on quality, which has differentiated their products in the market. The seasonal demand for camphor is also rising

Diversified Customer Base – Oriental Aromatics Ltd ensures a stable revenue base, with significant exposure to growing industries such as pharmaceuticals, personal care, and FMCG. Oriental Aromatics Ltd has over 2000+ customers across the globe.

Diversified Product Portfolio – Oriental Aromatics Ltd. has a diversified product portfolio across fragrance & flavour, aroma chemical, and camphor segments, and the current product mix contributes one-third each from all three segments.

What are the Risks of Investing in Oriental Aromatics Ltd?

Investors need to keep the following risks in mind if they choose to invest into this business. Risks needs to be weighed in combination with the advantages listed above to arrive at a decision that is optimal for your portfolio construct

Backwards integrated – F&F makers deciding to become backward integrated even in off-patent commodity raw materials is a risk that can threaten the business model of standalone aroma chemical makers. While the risk of this is low (given that Givaudan has a JV with Privi rather than doing backward integration by themselves), this needs to be monitored over time.

The volatility of raw material prices – Oriental Aromatics Ltd.profitability is vulnerable to fluctuations in raw material prices (alpha-pinene) and foreign exchange rates, though partially mitigated by natural hedging strategies. Oriental Aromatics Ltd. faces difficulty passing on price increases due to fixed-price contracts with some customers, especially in the camphor segment. Sometimes, spot sales can work for or against the business, depending on how input prices fluctuate.

High Working Capital Intensity – Oriental Aromatics Ltd. operates with high working capital intensity (NWC/sales of ~30-50%), driven by long inventory holding (5-6 months) and extended debtor days. Inventory is bulk-purchased, and payments to vendors are typically made on a spot basis or via LC.

Intense Competition – The camphor segment is affected by competition from Chinese imports and increased domestic capacities, while the aroma chemicals segment faces pressure due to demand slowdowns in Europe and the US, impacting sales and margins.

A clampdown by the Govt – any clampdown by the Govt on polluting chemical plants and forcing them to migrate to EU and US standards for effluent treatment and other safety and hazard management procedures can dent the margins of chemical makers in India. This can affect the competitiveness of Indian players across industries like bulk chemicals, speciality chemicals, and API.

The risk of inadequate safety mechanisms at any chemical plant is a well-known risk in this segment. Any accidents due to the handling of volatile chemicals and compounds can cause significant risk to plants and facilities; insurance cover will only protect the assets but not the growth that can be derived from the assets.

Oriental Aromatics Ltd Future Outlook

Oriental Aromatics Ltd. management is confident in meeting EBITDA guidance of 10~12% for FY25. Both new capex are expected to contribute significantly from FY26 as management plans to operate the new plants at full capacity within 2-3 quarters after commercialization. The brownfield project in Vadodara was successfully commissioned, and commercial production commenced on 30 July 24; management is expecting 1.7x Asset turn-on optimum utilisation, and the Greenfield project in Mahad has reached an advanced stage of commissioning and is expected to start contributing towards the topline from H2FY25, and management is expecting 1.2x Asset turn. Oriental Aromatics Ltd can have a peak revenue of 1200 Cr at current prices, including current and new capacities. Even camphor prices have been on the rise for the past four months. The newer capex and rising camphor prices can lead to operating leverage, which will significantly improve profitability from here

Oriental Aromatics Ltd Technical Analysis

We consider technical analysis to be a useful input in taking medium-term investment decisions. Many a time price action tends to lead to fundamental developments; this is too important an aspect to be ignored by retail investors who do not have access to management outside of common forums like investor calls & AGM.

At Congruence Advisers we like to consider both the long-term weekly chart and the daily chart to arrive at a view on price action. Combined with our understanding of fundamentals, we usually end up being better placed to be able to judge both the business cycle and the stock cycle. Playing the stock cycle right is extremely important for investors looking to extract significant alpha over the medium term.

Oriental Aromatics Ltd Price Charts

Given the history of the business and stock price performance, we believe that one should start with the long term chart and place the current price action in the right context.

Starting with the weekly chart (considering normal scale and not log scale to show the extent of price damage), one can see the market assessment of this business change drastically over the period starting 2020.

A ~72% from the peak to the bottom straightaway indicates that the business doesn’t have too much margin of safety when things go wrong when the price is optimistic. The business went from printing 22% operating margin in FY21 to printing 5-7% margin for a few quarters. Unit economics of the business dictate that the business needs to operate at healthy operating margins to meet the threshold of 18% ROCE over the medium term. That said, it is obvious that the bottom was well in place once the stock price started to show some upward momentum since May 2024. We would also do well to note that the current price consolidation is happening at a level of ~520 which was the false breakout level of July 2023. In the downward move post Covid, the stock also spent a lot of time in this range before making a further break to the downside. Logic dictates that a recently long base followed by healthy earnings can potentially set up the price trend for a strong rally.

Moving onto the daily chart

We would watch the price action closer to the 50 DMA like a hawk. More the instances where the price touches the 50 DMA and bounces back to the upside with a healthy volume bounce, better it would be technically. While the technical possibilities are interesting, we reckon that this is a story that cannot work without good fundamental numbers backing the price up. The only we can say with confidence right now is that a bottom appears to be firmly in place, one cannot yet be sure of a strong up move from here based purely on technicals.

Oriental Aromatics Ltd Latest Latest Result, News and Updates

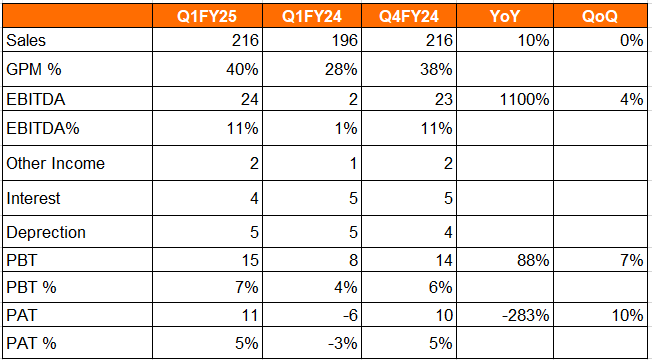

Oriental Aromatics Ltd Quarterly results

Oriental Aromatics Ltd has delivered 10% YoY growth and reported steady performance business across all verticals. In Q1FY25, overall production volume remained slightly better on a QoQ basis and marginally increased by YoY. During Q1FY25, most raw materials experienced price stability, and prices are increasing at a stable rate.

EBITDA for Q1FY25 was at 10.29% up 64 bps QoQ and 983 bps YoY. This is led by the stable availability of raw materials and the healthy demand for finished goods. The camphor division terpene chemical is showing encouraging signs of revival and started the quarter with lower demand due to off season; however, the upcoming festival season will lead to a strong demand for high-quality camphor. Oriental Aromatics Ltd. is able to pass on the price of powdered camphor to its customers; the fragrance and flavour division continues to perform strongly by acquiring new customers across the existing market.

On the Capex front, the Hydrogenation plant, a Brownfield project at the Vadodara site, was successfully commissioned in July 2024. The Greenfield project in Mahad has reached an advanced stage of commissioning and is expected to start contributing towards revenue from the H2FY25.

As per management, peak debt for FY25 will be around 285 Cr, of which 85 Cr is term loan and the rest is working capital debt. Expecting Q2FY25 & Q3FY25 to be in line with guidance while Q4FY25 outlook will be provided in Q3FY25.

Final thoughts on Oriental Aromatics Ltd

We have invested in this stock in the past and understand the business, promoters and industry dynamics quite well. We wouldn’t say that this is one the better chemicals businesses we have researched, we would rank stories like Galaxy Surfactants and Fine Organics much higher in terms of business quality compared to Oriental Aromatics Ltd. What caught our attention was the change in the management tone from “we do not know when the numbers will get better” to “we think they will get better, just that we do not want to overcommit” over the past few quarters. Even at the peak of the chemicals cycle in FY21 when the business was printing 20%+ EBITDA margin, Dharmil Bodani was always cautioning investors that 14-16% was the range to work with. We have high regard for the quality of management commentary over the years, so we are sensitive to tone changes in such businesses.

What makes the business more interesting right now is that numbers can get drastically better due to operating leverage followed by financial deleveraging over the next few quarters. If the business indeed delivers annual revenue of 1100 Cr+ in some quarters from now, PAT can easily clock 75 Cr+ at this rate which is a good 3x from the current PAT. The market always respects better financial numbers, even if they accrue from just mean reversion rather than any tangible business quality improvement. Investors should work with a conservative exit multiple for their financial calculations, we believe that the market is unlikely to trade this business at the peak multiple seen in FY22.

One should ideally invest in such stocks with a tactical frame of mind, stay till mean reversion gets priced in and then put money to work elsewhere. To extract the best results from such stocks, investors would need to demand a high margin of safety. A business with <2x gross asset turns, 14-15% operating margin and a 140+ day working capital cycle needs a dose of luck to deliver 18% ROCE over the medium term. Such stocks work best when one buys them in a sharp correction within a structural bull market, once there are clear signs of a tangible turnaround in operating numbers. Whether the market will present an opportunity like that or not, we will know over the next few weeks.

Tread cautiously but be decisive if the opportunity presents itself. And be clear about when to cut losses or to take profits home. This is not a secular business to be held for 5+ years after seeing a few good quarters. The next bad quarter in such businesses might arrive sooner than one expects and the bad run can extend for longer than one expects.

Disclaimer – This note is part of a business research & analysis series on small companies, there is no BUY/SELL recommendation or target price issued as part of this. There is no assurance that this stock makes for a good investment, there is no guarantee that this stock will be included in the coverage universe of Congruence Advisers. The note contains some forward-looking statements and insights drawn from the historical results, annual reports and investor presentations; they are to be viewed only within this context and not as a prediction of future performance of the business or the stock covered.

While due care has been taken to ensure that the information here is as accurate as possible, Congruence Advisers disclaims any liability in case of any unintentional inaccuracies.

The content does not constitute investment advice.

Disclosure (Updated as of Sep 30, 2024) – No position in the stock in personal portfolio