Salzer Electronics Ltd. is among the leading players offering customised electrical solutions in switchgear, wires & cables and energy management business. Salzer Electronics Ltd. is the largest manufacturer of CAM-operated rotary switches (25% market share) and wire ducts (20% market share). Salzer Electronics Ltd. caters to a wide range of products with 6 manufacturing facilities in Tamil Nadu. Salzer Electronics Ltd. has a vast distribution network locally and globally, exporting to more than 50 countries. Salzer Electronics Ltd. also has access to L&T’s local network via more than 350 distributors.

We believe Salzer Electronics Ltd. provides an opportunity to play the tailwinds present across a few key sectors, such as power, renewables, electric vehicles, smart metres, etc. While Salzer Electronics Ltd has grown its topline well historically, the profit growth and return on capital haven’t been nearly as impressive. Now, the management is targeting higher operating margins by venturing into new products. It is planning to reduce its working capital significantly to target a return on capital employed of 18% by FY26. Prima facie, Salzer Electronics Ltd historical track record of consistently high working capital days and deteriorating operating margins over the years doesn’t inspire much confidence in their ability to reach the target in the near term.

However, Salzer Electronics Ltd recent forays into smart meters and DC are promising. Fast charging could turn out to be a tremendous opportunity, as both areas have favourable regulatory and policy tailwinds. If Salzer Electronics Ltd is able to execute well in these new areas, it may lead to rapid growth for the next few years and change the face of Salzer Electronics Ltd. However, established players dominate both areas, making it challenging for Salzer Electronics Ltd. to carve out a meaningful space. As an investor, the key is to closely monitor the quality of management’s execution of the new initiatives.

Salzer Electronics Company Overview

Salzer Electronics Ltd is a micro-cap company that makes various electrical and electronics products for B2B and B2C applications: industrial switchgear and allied products, wires and cables, and B2C electrical products for buildings. In addition, Salzer Electronics Ltd is about to enter two new high-potential business segments: 1. DC fast charging equipment for charging 4W electric vehicles and 2. smart meters.

Mr. Rangaswamy Doraiswamy, a technocrat turned industrialist, founded Salzer Electronics Ltd in Coimbatore in 1985. Mr. Rangaswamy Doraiswamy was an electrical engineer and had worked with Lakshmi Machine Works for 15 years. He had a vision to start an electrical components manufacturing company in India which could substitute imports of electrical goods. He started Salzer Electronics Ltd in technical collaboration with a German company called M/s. Saelzer Schaltgerate Fabrik, GmbH, for manufacturing cam-operated rotary switches. In 1989, Salzer Electronics Ltd became a publicly listed company. From one product, over the years, Salzer Electronics Ltd has branched out into tens of different products and solutions and today operates 6 plants across its 3 divisions, all located in Tamil Nadu.

Salzer Electronics Ltd Management Details

Salzer Electronics Ltd. is a promoter-run and promoter-driven company. It is promoted by Mr. Rangaswamy Doraiswamy (MD), a Technocrat Entrepreneur with over 40 years of experience, and Mr. D. Rajeshkumar (Joint MD), an electrical engineer from India and holds a postgraduate degree in business management from the US. Both are supported by experienced management teams in operations, accounts and projects, corporate marketing, PR, and GST.

| Name | Designation | Experience |

| Mr. Rangaswamy Doraiswamy | Managing Director | Qualified Electrical Engineer and Technocrat Entrepreneur with over 4 decades of experience |

| Mr. D. Rajeshkumar | Joint MD | Electrical Engineer, India; Postgraduate in Business Management, US |

| M Laksminarayana | VP -Operations | B.E (Electrical) with over 2 decades of experience Responsible for Production, Planning, Inventory Management, Maintenance & General Administration |

| P. Sivakumar A | AVP –Marketing Corporate | Bachelors in Engineering with over 3 decades of experience Responsible for Sales & Marketing division |

| D. Govindaraj | Sr. Manager-Corp. Accounts & Projects | Masters in Commerce, DLL and DTL with over 3 decades of experience Responsible for project finance and corporate accounts |

| R Karunakaran | GM -PR & GST | BSc, Diploma in Marketing Management with more than 3 decades of experience Responsible for GST and Public Relations |

Salzer Electronics Ltd. Industry Landscape

Salzer Electronics Ltd has a presence in three business verticals: 1. Switchgear division, 2. Wires and Cables division, and 3. Building segment. Their presence in the building segment is very small, so for the purposes of our analysis, we will set it aside for now. In addition to these established segments, Salzer Electronics Ltd is foraying into two other new promising areas: DC fast charging for 4W EVs and smart electrical meters. Let’s look at the industry dynamics of the various business verticals briefly.

Switchgear Division

Globally, switchgear and electrical equipment manufacturing is dominated by MNCs such as Siemens, Schneider Electric, ABB, Hitachi, etc. In India, these MNCs also have a large presence via local subsidiaries. In addition, Indian companies like BHEL, CG Power, Kirloskar Electric, L&T, etc., are large players in this space. The Indian switchgear industry size is ~USD 10bn (~INR 80000 Cr) and is estimated to be growing at a CAGR of ~7% every year (Source: technavio). The key drivers of growth in the switchgear industry in India are the increasing penetration of electricity in India in households, the increasing conversion of industrial and transportation loads (railways, EV buses and cars) from other modes of energy to electrical energy and the rapid expansion of renewable energy generation.

The global focus on harnessing renewable energy generation via solar and wind power plants and the increasing penetration of electric vehicles have put unprecedented demands on national electrical grids globally. The electrical grid infrastructure in most countries is 30-50 years old. The sudden spurt in electrical generation and demand thanks to renewable energy and EVs has started to overwhelm the old grids. Hence, massive investments across the globe are being made to enhance grid infrastructure. This kind of global grid overhaul has massively increased demand for electrical equipment such as inverters, transformers, HVDC cables, relays and circuit breakers, smart meters, etc.

While Salzer Electronics Ltd is mostly into lower voltage-rated equipment, nonetheless, it has also been a beneficiary of this demand tailwind. Most of the demand for complex electrical systems is being fulfilled by the global and Indian giants such as Siemens, Schneider Electric, ABB, CG Power, L&T, etc., while smaller electrical equipment companies like Salzer Electronics Ltd are supplying sub-components to these larger companies. For example, Salzer Electronics Ltd 3-phase dry-type transformers are used to make larger inverters on solar farms.

Salzer Electronics Ltd sells a wide range of electrical equipment in this division, such as toroidal transformers, 3-phase dry-type transformers, cam-operated rotary switches, wire harnesses, contactors, relays, and more. This is Salzer Electronics Ltd largest division by revenue share and the fastest-growing division. Let’s examine the key products in this segment in more detail.

- Toroidal transformers – Toroidal transformers are a class of indoor transformers used in various applications such as medical equipment, industrial equipment, audio equipment, telecommunications and renewable energy systems. Toroidal transformers have a doughnut-shaped core, which minimises electromagnetic interference and thus provides a clean transformation of power without producing much electromagnetic noise. The power ratings for toroidal transformers usually range from as low as 10-50VA for audio equipment to as high as 10kVA for certain industrial or renewable energy applications. Toroidal transformers are normally not used for high-power use cases such as power distribution transformers.

- 3-phase dry type transformers 3-phase dry type transformers provide power in 3 separate phases to deliver more balanced power to the connected load. These transformers are “dry” because they don’t use a liquid coolant. Dry-type transformers are used where fire safety or liquid spillage is a concern. 3-phase dry-type transformers can be used for various loads in industrial use cases, commercial buildings, data centres, telecom infrastructure, healthcare, etc.

- Cam-operated Rotary switches – Cam-operated rotary switches are switching devices that use a rotating mechanism to change the configuration of electrical contacts, thus switching on or off various loads or increasing/decreasing power loads to a device. Cam-operated rotary switches are used in industrial control panels, transportation systems, electrical distribution boards, etc.

- Wire harnesses – Wire harnesses are an organised collection of wires, cables, and other components, such as connectors, for electrical systems that are bundled and secured together into one structure. Organising a complex collection of wires and cables into a harness enables seamless operation of electrical systems and prevents failure due to wires getting entangled, etc.

- Contactors and relays Contactors and relays are electrically operated switches that are used to open and close electrical circuits connected to an electrical load, such as a motor, light, heater, etc. Contactors and relays can either be electromagnetism-based or semiconductor-based.

Wires and Cables Division

The Indian wires and cables industry was estimated to be ~INR 68000-73000 Cr in size (~USD 8-9bn) in FY23 (Source Polycab Annual report). Industry participants expect the wires and cables industry in India to grow at a CAGR of 10% to about INR 90000-95000 Cr in the next 3-4 years. This rapid growth is driven by increased housing for the poor driven by Govt programs, huge investments in renewable energy and power capacity, expansion of the electrical transmission and distribution infrastructure and growing investments in telecom and data centres.

Wires comprise a single conducting core, whereas cables comprise multiple cores. Wires and cables are used to transmit electricity, data or signals. They are made of either copper or aluminium. Let’s look at a few different kinds of wires and cables.

- Control and instrumentation cables are found to be used in electrical power systems or any related process control systems.

- Telecom cables are used for voice and data transmission.

- Optical fibre cables provide high-speed data connection.

- Power cables transmit and distribute electricity from power generating plants to substations and ultimately to end-user segments, including residential, commercial, and industrial units.

- Building wires are used for electrical wiring in residential and commercial properties and are typically classified into flame-retardant (FR), fire-retardant (FR), flame-retardant low-smoke (FRLS), and Halogen-Free Flame-Retardant (HFFR) categories.

Salzer Electronics Ltd manufactures only copper wires, and Salzer Electronics Ltd is majorly present in the agri cables & wires segment. Agri cables & wires are used in the agricultural industry by farmers. The demand in this segment is seasonal. Agri cables & wires demand high weather resistance, chemical resistance and durability due to the rough nature of usage.

DC Fast Charging

DC fast chargers (DCFC) are specialised chargers that fast-charge electric vehicles by providing direct DC power to the vehicle’s battery; in contrast to AC chargers, which supply AC power from the grid to the vehicle, which is then converted to DC power by the vehicle’s onboard battery charging system. DC chargers provide much higher power, ranging from 50–350 kW to the battery, compared to AC chargers, which typically offer ~20 kW of power. Thus, EVs can be charged from 20% to 80% in a matter of 30 minutes using DC fast chargers. Therefore, DC fast chargers are suitable for public charging stations on highways or for captive use by EV fleet operators.

Since DC fast chargers are so power-intensive, they draw a lot of power from the grid. Thus, mass installations of DCFC in a country can lead to grid instability if not planned for in advance by the Government via augmentation of grid capacity. Therefore, a fast roll-out of the DCFC network around a country may not be feasible, as the grid infrastructure first needs to be ready to handle the additional loads.

Globally, DCFC is manufactured by Tesla, ABB, Siemens, Schneider Electric, Eaton, Wallbox, etc. In India, DCFC manufacturing is still in the nascent stages, as the adoption of DC charging has yet to take off meaningfully. A few companies manufacturing DC fast chargers in India are ABB, Servotech, Exicom, Delta Electronics, etc.

Salzer Electronics Ltd has formed a Joint Venture with an Austrian company called Kostad GmBH to manufacture DCFCs in India.

Smart Meters

Smart meters are programmable, digital electricity meters that provide real-time updates on the amount of electricity consumed by both the consumer and the power distribution company (DISCOM). DISCOMs are able to read and control these meters remotely. Thus, with smart meters, DISCOM billing and collection cycles can become much shorter and more accurate, with less leakage. Smart meters can also facilitate time-of-day pricing, wherein DISCOMs can price electricity at various times of the day depending on demand.

The Indian government. They launched the Reforms Based Results Linked Power Distribution Sector Scheme (RDSS) in 2021 with the aim of improving the efficiency and financial stability of power distribution companies in India. DISCOMs in India have traditionally been traditionally Government-owned, and they have been inefficient operators with large leakages in billing and delays in collections of dues from customers. This has led to huge financial strain on their balance sheets, which in turn has affected their suppliers, i.e., the power generating companies. The RDSS scheme aims to improve the efficiency of DISCOMs and thus set in motion a positive chain reaction in the traditionally ailing power sector in India.

One of the key components of the RDSS scheme is a proposal to install 25 Cr smart meters all across the country by 2027 in 3 phases. Against this target, so far, ~22 Cr smart meters have been sanctioned by DISCOMs, orders for the installation of ~11 Cr smart meters have been awarded, and only ~1.2 Cr smart meters have been installed so far. To reduce the capex burden on DISCOMs, the cost of the smart meters will be paid in instalments over 7-8 years by the DISCOMs to the service providers.

Salzer Electronics Ltd has recently announced its entry into smart meter manufacturing to capitalise on this opportunity.

Salzer Electronics Ltd Product Details

Salzer Electronics Ltd business is split into 3 business verticals

- Switchgear Division

- Wires & Cables Division

- Building Products Division

Over the last 6 years, the proportion of business coming from the switchgear division for Salzer Electronics has sharply increased from ~41% in FY21 to 55% in FY24 on the back of a 23% CAGR growth. This growth has mainly been led by growth in the transformer sub-segment of the switchgear division. Transformers have seen a lot of demand in the last few years due to the high capital expenditures on improving power infrastructure and the increase in the number of renewable power plants being set up. The wires and cables business has grown at a steadier pace of 11% CAGR during this period, and its contribution to the total revenue has dropped from ~49% in FY19 to ~40% in FY24. The building products segment has stagnated and barely grown in the last 6 years.

Salzer Electronics Ltd – Revenue split across divisions

Salzer Electronics Ltd caters to end-demand from multiple industries such as power, renewables, machine tools, healthcare, automotive, agriculture, building materials, etc. The Switchgear division manufactures products for B2B customers, whereas the wires & cables and building product segments are mostly B2C and serviced through a distribution channel. About 25% of revenues are from exports; the rest is domestic. No single customer has a 10% share of sales for Salzer Electronics Ltd, and the top 15 customers contribute to ~45% of the total sales. Salzer Electronics Ltd has 5 plants located in Coimbatore (Unit I to Unit V) and has recently set up a new plant in Hosur.

Let us look at each of Salzer Electronics Ltd business divisions in more detail.

Switchgear Division

The switchgear division revenues have grown at a very good CAGR of ~23% between FY19 and FY24. However, the growth has been EBITDA dilutive. From EBITDA margins of ~14.5% in FY21, the division’s EBITDA margins have come down to 12-13% levels in FY23 and FY24. This is because most of the growth has been driven by revenue growth from transformers, which command a lower EBITDA margin than other products in this division.

The major products in this segment are cam-operated rotary switches, wire harnesses, toroidal transformers, 3-phase dry-type transformers, contactors, and relays. Within the product segments, cam-operated rotary switches, contactors, terminal blocks, and cable ducts have higher EBITDA margins of ~15%, whereas transformers and wire harnesses have lower EBITDA margins of ~11-12%.

Salzer Electronics Ltd is the leading player in cam-operated rotary switches and wire ducts in India. It is the largest supplier of cam-operated and load break switches to the Indian Railways. In 2019, Salzer Electronics Ltd bought a 72% stake in Kaycee Industries, which was its largest competitor in cam-operated rotary switches and wire ducts. Kaycee Industries is listed on BSE, and Salzer Electronics Ltd owns a 73.5% stake in the company at present.

Salzer Electronics Ltd also manufactures toroidal transformers and 3-phase dry-type transformers. Salzer Electronics Ltd transferred technology from Plitron (now Noratel) and Trafomodern, respectively, to acquire the know-how to manufacture toroidal transformers and 3-phase dry-type transformers. The transformers manufactured by Salzer Electronics Ltd are relatively small in size (< 1000V). They are used in several applications, such as renewable energy inverters, machine tools, medical devices, etc.

Salzer Electronics Ltd has recently augmented its capacity in wire harnesses and toroidal transformers by setting up a new manufacturing facility on leased premises in Hosur. One of the reasons they set up the factory in Hosur instead of Coimbatore was the proximity to 2W OEMs, where they are trying to break through with their wire harness product.

Most of the sales in this division are B2B with sales being made to large global MNCs such as Siemens, Schneider Electric, Honeywell, GE Electric, Eaton, ABB etc. These OEMs source sub-components from the likes of Salzer Electronics Ltd and other small companies and assemble them into complex electrical systems and products for clients across industries. Salzer Electronics Ltd commands very little pricing power in this segment and has to accommodate most of the demands of its customers. Contracts in this segment are annual, and rates are agreed upon once a year. Certain products are B2C in nature and are distributed via Salzer Electronics Ltd own network of pan-India distributors. Salzer Electronics Ltd also has a tie-up with Larsen and Toubro to leverage its network of 350+ distributors pan India to distribute some of their products.

Cables and Wires Division

The cables and wires division revenues grew at a moderate CAGR of ~11% between FY19 and FY24. Since FY21, EBITDA levels in this segment have dropped from ~7-8% to ~6-7%, and the division’s contribution to overall revenues has also reduced.

The major product manufactured by Salzer Electronics Ltd in this segment is copper-based agri-cables for the agricultural segment. The products are distributed via Larsen & Toubro’s distribution network of 350+ distributors pan India. Cables and wires division is seasonal due to its dependence on agriculture. Agri wires and cables are a low gross margin business, and cables and wires division have generated 6-8% EBITDA margins in the past. Management is trying to diversify the mix away from agri cables, which will enable them to enhance EBITDA margins by 8-10%.

Building Products Division

In the building products division (B2C segment), Salzer Electronics Ltd supplies electrical components that are used in residences, such as Miniature Circuit Breakers, housing wires, smart switches, remote switches, etc., and Salzer Electronics Ltd sells products via its distribution channel here. This division has barely grown over the last 6 years. There doesn’t seem to be enough management to focus on growing this segment. It’s also a very well-penetrated segment with established branded competitors, so it’s difficult for Salzer Electronics Ltd to make headway here.

DC Fast charging

Salzer Electronics Ltd entered into a joint venture with Kostad Gmbh, an Austrian company, in 2021 to develop DC fast chargers for electric vehicles. Initially, Salzer Electronics Ltd owned 26% of the JV, which they increased to 60% in December 2023. Salzer Kostad EV Chargers Pvt. Ltd. is now a subsidiary of Salzer Electronics Ltd. While Kostad sells a fraction of the DC fast chargers that ABB sells, it is still a credible name in the DC fast charging space in Austria.

Under this subsidiary, Salzer Electronics Ltd plans to make DC fast chargers (DCFCs) for electric vehicles with power throughput ranging between 30kW-240kW. Such chargers can charge electric vehicles in around 30 minutes. These chargers are not for home usage but are to be installed on highways as a public utility. Fleet operators can also have captive networks of such chargers within city limits to keep their fleets charged. According to Salzer Electronics Ltd, initially, 60% of the charger’s value would be imported, and 40% would be domestic. As the technology gets fully transferred, this % will increase further in favour of domestic value addition. Salzer Electronics Ltd chargers are currently undergoing ARAI certification, and they’ve failed 1 out of 14 tests. Redoing the test would take a few months, and they expect to receive the certification and start an initial commercial business in FY25. In the first year, most of the sales are expected to be buybacks by the Austrian JV partner, and Salzer Electronics Ltd management is not expecting more than 50-100 units of sale.

Salzer Electronics Ltd expects the demand for DCFCs to skyrocket once EV ownership in India reaches a particular threshold. According to management, at steady state, India may need 2 Lakh such chargers. With each charger costing between INR 7-10 Lakhs, according to management, the total market size in India for DCFCs can be INR 14000-20000Cr. Management believes that Salzer Electronics Ltd can potentially get an INR 500 Cr topline from DCFCs in India with an 18-20% EBITDA margin in 3-4 years’ time.

There isn’t a lot of information available to corroborate Salzer Electronics Ltd management’s number of INR 14000-20000 Cr market size in India for DCFCs, but we can attempt a very rough back-of-the-hand calculation to see if the number is in the right ballpark. These chargers will be installed in urban centres and along highways. India today has approximately 3.5 Lakh KMs of National and State highways. Assuming chargers are installed every 25 KMs along these highways on either side, we’d need 28000 DCFCs for highway installations. Let’s assume India has 100 urban centres where chargers would need to be installed. The Tier 1 cities (~10) would probably need 500 chargers each for adequate coverage, the Tier 2 cities (~20) would probably need 300 chargers, and so on. Aggregating the nos, urban centres would probably need 25000 chargers together. Putting the numbers together, it appears the overall requirement might be closer to 50000 DCFCs than 2 Lakh. Even so, this would translate into a sizable industry size of INR 3500-5000 Cr. Salzer Electronics Ltd target of INR 500 Cr topline in this segment would translate into a market share of 10-15%. With competitors like ABB, Delta Electronics, and Servotech in India, a 10-15% market share in this segment would be a remarkable yet unlikely achievement for a company like Salzer Electronics Ltd

There is also the question of how much power these chargers would draw from the grid. Assuming an average charger is rated 100kW, then 50,000 chargers would draw close to 5GW of energy. This is about 2-3% of India’s peak power demand. So, Government policy and interventions also need to ensure that the Grid can support this additional demand.

Hopefully, we have established that while Salzer Electronics Ltd entry into DCFC looks very interesting, we may be a few months away from enough clarity on the TAM, Salzer Electronics Ltd competitive positioning in terms of price, product quality, and Government policy trajectory, to actually assign any value from DCFCs to Salzer Electronics Ltd present valuations. However, the next few quarters of development are very key in this regard and need to be closely monitored.

Smart meters

Salzer Electronics Ltd surprised investors with an announcement in Feb 2024 about its intention to get into single-phase smart electricity meter manufacturing. There was no previous indication from management that an entry into this segment was on the horizon. The smart meter factory is being set up in Coimbatore. It will be backward integrated with their other factories in the city, where they make various electrical components that may be consumed by a smart meter. They indicated that initial capacities will be 4mn smart meters in Phase 1, which can be increased to 10mn smart meters in Phase 2 if the demand is robust. The product has already received BIS certification, and they expect to start commercial operations as soon as Q1 in FY25. The total capex outlay for Phase 1 is INR 40 Cr. The major competitors in the smart meter space are Genus Power, which has a 12mn annual capacity; Schneider Electric, which has a 17mn annual capacity; and HPL Electric, which has an 11mn annual capacity.

Salzer Electronics Ltd will not directly participate in smart meter tenders. Rather, once tenders are awarded to service providers such as Genus Power, HPL Electric, Adani Transmission, and L&T, Salzer Electronics Ltd will sell them smart meters to fulfil their service obligations towards the state DISCOMs. Some of the service providers, like Genus, Schenider, and HPL, have their own smart meter manufacturing capacities, whereas others, such as Adani Transmission, L&T, ECIL, and Intellismart, don’t have their own manufacturing setups. These pure-play service providers will depend on smart meter manufacturers like Salzer Electronics Ltd to fulfil their tender commitments towards DISCOMs.

Going by management guidance, at an average unit selling price of INR 2400-2800, at full capacity, Salzer Electronics Ltd has the potential to earn INR 1000-1100 Cr revenues from the smart meter segment. Management is quite bullish on this segment and expects 12-15% EBITDA margins. Assuming the smart meter business will require 100 days of net working capital investment, on an INR 40Cr capex investment and INR 1000 Cr maximum revenues with 13% EBITDA margins, the return on capital employed in this venture turns out to be north of 40% per annum. Even at 150 days of net working capital, the return on capital capital works out to close at 30%. We feel that either management is being over-optimistic in its revenue and margin expectations, or the stellar return metrics in this industry will attract far more competition soon, which will drive down prices and margins to a much more reasonable level. As an illustration, Genus Power, one of the largest smart meter manufacturers in India, has earned an average return on capital employed of ~10% over the last 8 years.

However, if things work out as per management expectations and Salzer Electronics Ltd receives healthy orders so that it can fill up its capacity in the next 2-3 years and earn margins in the 12-15% range, in that case, this venture has the potential to be extremely value accretive for the company. However, as in the DC fast chargers case, we recommend being cautious observers here for some time. Once things play out and become more clear, even if the price runs up further, we may have better certainty regarding future cash flows at that point. The major uncertainties at this point with regards to the RDSS scheme getting implemented in its full scale over the next 5-6 years are twofold

- The ability of service providers’ balance sheets to sustain such heavy investments – Under the RDSS scheme, service providers will install meters on behalf of discoms and provide services for 7-8 years from the date of installation. DISCOMs will not pay the service providers the entire value of the smart meter upfront, but rather, the smart meter cost + service cost will be bundled together and paid in instalments over 7-8 years. This has been done keeping in mind the strained balance sheets of DISCOMs. However, this means that service providers will have to finance all investments from their balance sheets upfront while cash accrues to them over 7-8 years. This places a huge burden on service providers. While the likes of large companies like Adani Transmission may have the financial firepower to sustain such a model, smaller service providers like Genus Power may struggle to maintain such high capital demands on their balance sheets. If such service providers get into financial trouble, then the entire scheme may be disrupted to a large extent. We are still in the early days of the rollout. While Govt authorities have released a major chunk of orders on service providers, the ability of these service providers to smoothly execute the projects very much remains to be tested.

- Public resistance and political resistance in the rollout of smart metering across the country – In a developing country like India, household electricity remains a heavily politicised subject. Electricity supply, along with food, clothing, and shelter, is a basic necessity—many poor people in India bank on subsidies for their electricity bills announced by governments. Subsidised electricity is also a major tool by which state Governments attempt to solidify the support of their electorate. In such an existing environment, it is easy to imagine that there could be a lot of opposition to the installation of smart meters at a political and ground level. Smart meters, after all, are meant to reduce power leakages and enable DISCOMs to collect the correct electricity charges on time from consumers. We have already started seeing some resistance to smart meter rollouts, and governments are backing down temporarily with a view to elections. With such a hot-button issue that impacts the lives of so many people, we find the need to temper our expectations regarding the momentum of the execution of smart meter installations. Suppose we see a determined Government effort to push through the scheme even in the face of public opposition. In that case, we can always be more confident in projecting future cash flows for all related companies. Until then, we remain cautious.

Salzer Electronics Corporate Governance

Salzer Electronics operates in a capital intensive, competitive industry where players struggle to deliver healthy ROCE across cycles; hence corporate governance becomes a very important part of the business analysis.

Some of the important elements of corporate governance at Salzer Electronics –

- Board Composition – Salzer Electronics Ltd. has a large Board comprising 11 members. An Independent Director chairs the Board, and more than 50% of the Board members are independent directors. The chairman of the board is Mr. S. Rangachary, a decorated ex-IRS officer with the Government of India who is 85 years old. The other independent Directors have experience across entrepreneurship, manufacturing, and finance. Overall, almost all the Independent Directors are in their 70s and 80s. For a company trying to grow in exciting new areas of electronics, we are not sure how up-to-date their knowledge is and, therefore, to what extent they may be able to contribute towards furthering the Salzer Electronics Ltd strategic outlook.

- Promoter remuneration – The total remuneration paid to promoters and their relatives in the form of salary, commission, and Director sitting fees amounted to ~INR 1.9Cr in FY23. This amounted to ~5.4% of the total PAT for FY23, which is well within the recommended range.

- Related Party Transactions – Salzer Electronics Ltd. has a number of related parties, mostly companies over which promoter Directors exert significant control. About 3% of the Salzer Electronics Ltd top line is derived from sales to such companies. These companies also provide service services from Salzer Electronics Ltd. to the tune of ~1% of revenue, the details of which are not mentioned. Overall, we don’t see any apparent cause for concern, but the value of transactions with related companies needs to be monitored from year to year.

- Contingent Liabilities – Salzer Electronics Ltd.’s total material contingent liabilities for FY23 amounted to less than INR 1 Cr in the nature of tax liabilities. This amounts to less than 1% of the Salzer Electronics Ltd book value and hence can be completely ignored.

Salzer Electronics Financial Performance

Over the last 5 years, Salzer Electronics Ltd has grown sales at a healthy CAGR of ~16%. However, EBITDA and PAT have grown slower than sales at 12.5% CAGR and 14.4% CAGR, respectively. Margins were in decline till FY22. Since then, they have started reviving, but are still well below the levels of pre-Covid years. The return on capital record for Salzer Electronics over the last 6 years has been quite dismal at an average ROCE of 10.9% over 6 years and an average ROE of 8.3% over 6 years.

Salzer Electronics Ltd Revenue Growth

FY24 growth was 12% vs (30% in FY23), Contribution from exports was 26.93% in FY24 (vs 25.6% in FY23), Industrial Switchgear was up 13% at 637 cr vs (563 Cr in FY23), Wire & Cable up 16% at 460 Cr (vs 398 Cr in FY23) & Building Segment was down at -8% at 69Cr in FY24 vs (75 Cr in FY23) Growth has slowed down in FY24 & recent quarters due to slower offtake from end-user, elections, slowdown in exports & geopolitical issues. While management has remained cautiously optimistic for FY25 the growth is expected to improve in FY25 backed by uptick in industrial demand, healthy growth in building products segment and anticipated improvement in export markets.

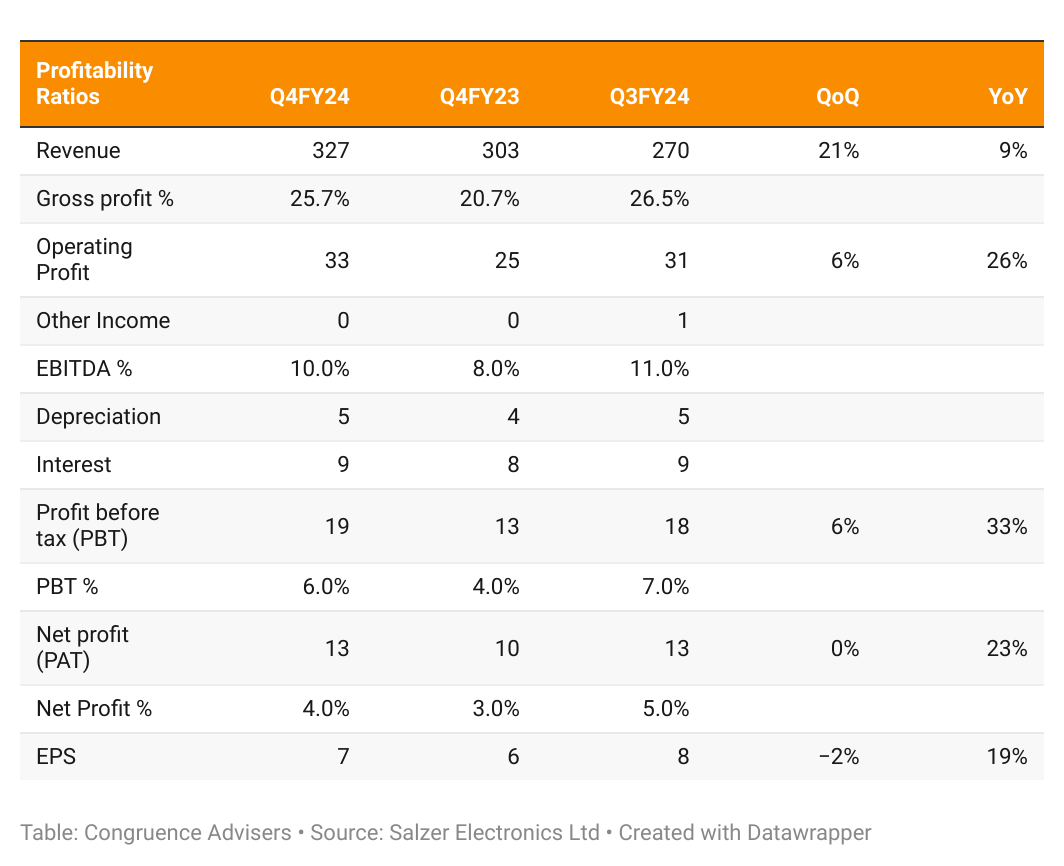

Salzer Electronics Ltd Profitability Ratios

Profitability ratios decreased from FY19 to FY22 due to inflation, geopolitical issues & global slowdowns; on top of that, Salzer Electronics Ltd switchgear division’s profitability was impacted because of a higher product mix towards transformers, which has lower margins. The cable & wires division is also struggling due to a slowdown in the rural market. Profitability improved in FY23 as Salzer Electronic Ltd started to pass on the increased cost, And FY24 saw further improvement in Profitability ratios backed by input cost moderation. While Management is guiding further improvement in Profitability in FY25, any meaningful progress will depend on how well management is able to execute & scale new segments.

Salzer Electronics Ltd Debt Levels and Cash Flow Conversion Analysis

Salzer Electronic Ltd relies on high debt & the majority of debt is short-term debt because of Working capital-intensive operations; net working capital days have been consistently high in the 150-170 days range because of high inventory as Salzer Electronic Ltd manufactures a wide range of SKUs and stocks raw materials and high receivables on account of long payment cycle extended to customers, majority of whom are OEM. As a result, the average conversion of EBITDA to cash flow from operations has been very low at an average of 30% over the last 6 years.

Salzer Electronics Ltd Comparative Analysis

To understand Salzer Electronics Ltd.’s investment potential, we have conducted a comprehensive analysis. This analysis includes comparing Salzer to its competitors (peer comparison), comparing a benchmark index, and comparing sector performance.

Salzer Electronics Ltd Peer Comparison

It is quite challenging to identify a suitable Microcap Peer for Salzer Electronics Ltd. Salzer Electronics Ltd is a rare, small market cap company that is into so many varied electrical products such as wires & cables, transformers, switches, and wire harnesses. It has a mix of B2B and B2C business segments. The building products and wires & cables segments of Salzer Electronics Ltd are similar to an extent to the business of FMEG companies. Considering Salzer Electronics Ltd size, Orient Electric seems to be the closest peer from the FMEG pack. The closest peer for Salzer Electronics Ltd switchgear business appears to be HPL Electric.

Salzer Electronics Ltd Index Comparison

Salzer Electronics Ltd share performance vs S&P BSE Small cap Index as the index benchmark comparison is a fundamental tool for understanding the investment potential and making informed decisions in the context of the broader market

Salzer Electronics Ltd Sector Comparison

Salzer Electronics Ltd shares performance vs BSE CG as We believe sector comparison helps to differentiate between industry-wide trends and company-specific factors & also helps in executing sector rotation and stock rotation strategies.

Salzer Electronics Ltd Valuation Ratios

| Ratio | As on 15/07/24 |

| Price/Earnings | 34 |

| Price/Book | 3.61 |

| Price/Sales | 1.34 |

| EV/EBITDA | 15.5 |

Why You Should Consider Investing in Salzer Electronics Ltd?

We believe that Salzer Electronics Ltd offers some compelling reasons to track the business closely and to consider investing if one is looking to play the tailwinds present across a few key sectors, such as power, renewables, electric vehicles, smart metres,etc

- Industry tailwinds – As we have discussed, there are strong tailwinds in the power sector due to global capex in grid overhaul and capacity enhancements driven by the adoption of renewable energy and electric vehicles. Salzer Electronics Ltd is present across many products in this theme

- Entry into smart meters – As discussed, there is a huge demand for smart meters in India thanks to the RDSS scheme. While the scheme rollout has been slow, and it won’t be a smooth or fast journey by any stretch of the imagination, if the Central Govt, in collaboration with State governments, is indeed able to see through the targeted installation of 25Cr smart meters over the next 5-6 years, then there is a lot of scope for earnings for many players in the industry like Salzer Electronics Ltd. Considering the opportunity size relative to Salzer Electronics Ltd current revenues, even capturing a very small chunk of this demand (~1%) can meaningfully move the needle for Salzer Electronics Ltd.

- DC fast charging – There is a high likelihood of electric vehicles commanding a significant share (~20-30%) in the 4W Indian automotive segment by the end of this decade. If that happens, then the installation of DC fast chargers at scale in India is inevitable, even though the path may not be clear right now. Thus, DC fast charging is a serious optionality for Salzer Electronics Ltd to drive future value. However, this requires patience from investors as the landscape is still very much evolving.

- Management focus on working capital control – Salzer Electronics Ltd has historically suffered from poor working capital management, which has resulted in very poor cash generation and low return on capital for the company. Recently, the management has articulated its targets of achieving 100 days of Net Working capital and 18% ROCE by FY26. We are not very optimistic about drastic improvement in working capital in the traditional business as their customers are all large OEMs who dictate terms to them. However, the new businesses – smart meter and DC fast charging – have higher margins, and there is a possibility of setting better working capital norms from Day 1 in these businesses. Again, this is an area where we have to wait and watch how management walks the talk

- Management’s focus on growth – For the last few years, management has been looking for avenues to grow their business outside of the traditional agri cables and wires and switchgear businesses. Salzer Electronics Ltd JV with Kostad and the recent foray into smart meters demonstrate that. It’s always good to invest in a company where the management has a growth mindset in a country like India, where nominal GDP itself is expected to grow by double digits. There are also some pitfalls associated with this approach, which we have covered in the risks section.

What are the Risks of Investing in Salzer Electronics Ltd ?

Investors need to keep the following risks in mind if they choose to invest into this business. Risks needs to be weighed in combination with the advantages listed above to arrive at a decision that is optimal for your portfolio construct

- Inability to deliver on working capital and ROCE targets—If Salzer Electronics Ltd is unable to improve its working capital cycle, then the return on capital employed is unlikely to improve. This will also put further pressure on its cash and debt positions and may constrain capital availability to pursue new growth opportunities.

- Inability to commercialise DC fast chargers – A large part of an investment thesis in Salzer Electronics Ltd rests on the company’s ability to succeed with its new products – DC fast chargers and smart meters. There are several potential risks associated with their DC fast-charging product, such as

- Their product does not gain acceptability in India or

- The DC fast charging ecosystem will not gain traction in India in the near future due to a slowdown in EV adoption or policy slowdown.

- Or Salzer enters into a very capital-heavy business model in DC fast chargers, which they aren’t able to sustain.

One or more of these risks can either erode future optionalities or even threaten the company’s balance sheet stability.

- Inability to secure smart meter orders—The smart meter ecosystem is seeing increasing participation from new entrants as everybody eyes the ~75000 Cr opportunity that might unfold over the next several years. Other competitors may out-compete Salzer Electronics Ltd in terms of price or capabilities, thus leading to no or low incremental revenues from this segment. Even if Salzer Electronics Ltd manages to secure orders, the unit rates may fall due to high competition, leading to sub-par return ratios on their smart meter investments.

- Limited management bandwidth and multiple product segments – For a sub-2000 Cr Mcap company, Salzer Electronics Ltd seems to have way too many product segments. The bandwidth of the management team of such a small company is usually limited, and trying to grow in 5-6 different product areas – some of which involve high technology – might strain the abilities of the management, resulting in sub-par execution and value destruction or below-potential value accretion.

- Questionable capital allocation history – Salzer Electronics Ltd decided to invest in agricultural wires and cables in 2006. This has been a low-margin segment for Salzer, with segmental EBITDAs being as low as 6-7%. It’s unlikely that this diversification has given Salzer Electronics Ltd a good return on the capital invested. Similarly, they invested time and capital into developing an EV conversion kit for 3Ws, which would allow existing ICE-based 3Ws to be transitioned to EV powertrains in the aftermarket. After completing the development cycle, management realised that the cost economics didn’t work out, and the project had been scrapped. The capital deployment track record of Salzer Electronics Ltd management has not been spotless, and therefore, new investments merit caution from investors.

Salzer Electronics Future Outlook

The management expects Salzer Electronics Ltd to be able to grow its base business revenues at the rate of ~20% for the next two years with a 50-100 bps EBITDA margin expansion to 10.5-11%. This excludes the revenues possible from the smart meter and DC fast charger segments. By FY26, Salzer Electronics Ltd wants to bring its net working capital days down to 100 from the present 150-160 levels and increase the return on capital employed to 18%. Both the net working capital and ROCE targets have never been achieved in the Salzer Electronics Ltd history. As highlighted in the rest of the business analysis section above, the future value of Salzer Electronics Ltd depends on the quality of execution of management. Management’s past execution track record has not been very robust, so as an investor, it is best to assign value to the potential of the new initiates as execution proceeds and more confidence builds in management’s aspirational numbers.

Salzer Electronics Ltd Technical Analysis

We consider technical analysis to be a useful input in taking medium-term investment decisions. Many a time price action tends to lead to fundamental developments; this is too important an aspect to be ignored by retail investors who do not have access to management outside of common forums like investor calls & AGM.

At Congruence Advisers we like to consider both the long-term weekly chart and the daily chart to arrive at a view on price action. Combined with our understanding of fundamentals, we usually end up being better placed to be able to judge both the business cycle and the stock cycle. Playing the stock cycle right is extremely important for investors looking to extract significant alpha over the medium term.

Salzer Electronics Ltd Price Charts

On weekly charts, over the last 3 years, one can clearly identify 3 distinct phases of price movement. Phase 1 was a 1 year horizontal consolidation between July 2021 and July 2022 between 150-245 levels. Phase 2 was a 1.5 year upward sloping channel from Aug 2022 to Jan 2024 when price moved from 180 to 470. The third phase started with a parabolic move in Feb 2024 with the news of Salzer Electronics Ltd entry into the smart meter segment where the stock went from 470 levels to 800.. Unless the smart meter story breaks down in some way, the stock is unlikely to fall below 680 levels anytime soon. Further positive developments in smart meters or DC fast charging or significant improvement in earnings momentum and ROCE in the upcoming quarters can enable the stock to meaningfully break out of the 870 resistance levels and sustain the up move. Right now price seems to be taking support at 875 levels, but with valuations already more than fair, 875 may not offer strong support without evidence of further execution.

On daily charts, the stock consolidated between 365 and 460 levels for 7 months between Aug 2023 and Feb 2024. In Feb 2024, Salzer Electronics Ltd announced its foray into smart meters. That caused the Salzer Electronics Ltd stock to break out of the consolidation zone with very high volumes and go on a parabolic move to ~800 levels within a few days. Salzer Electronics Ltd stock corrected to 640 levels along with the broader markets in March and then went on to make new highs at ~875. Since then Salzer Electronics Ltd stock has consolidated and nearly tested the March lows of 640 during Q4 results announcement and election volatility before bouncing back to new highs post the election results. Salzer Electronics Ltd has generally respected 100 EMA levels during the last 1 year, so it can be reasonably expected to take support at 100 EMA levels during corrections in the near future.

Salzer Electronics Latest Result, News and Updates

During FY24, Salzer Electronics achieved milestones in product development, successfully created a Smart Meter facility, and received BIS certification.

In Q4 FY24, Salzer Electronics Ltd delivered a modest revenue growth of 8% and an EBITDA margin of 10%. The switchgear division contributed ~53.5% of revenues in Q4 with an EBITDA margin of 13.3%, the wires and cables business contributed ~40.5% of revenues in Q4 with an EBITDA margin of 6.3% and the building segment contributed ~6% of revenues in Q4. Exports contributed 25% to the Q4 revenues.

Salzer Electronics Ltd expects to grow revenues by 18-23% in FY25 over FY24 with a 100 bps expansion in margins. This is excluding the new smart meter business, whose numbers will add to this growth. For the smart meter segment, Salzer Electronics Ltd hopes to be able to deliver EBITDA margins between 12-15% in FY25. It stopped short of giving guidance for FY25 revenues possible from the smart meter segment as that depends on the order flow from state DISCOMs and is difficult to predict.

HDFC Securities recently (July 2024) put out a research note on Salzer Electronics with a target price of 1080. Please note that we do not endorse their views, this is for information alone.

Final Thoughts on Salzer Electronics Share Analysis

Salzer Electronics share has witnessed a lot of investor interest over the past 18 months. Along with the rest of the pack in this market segment, Salzer Electronics share has gone on to make new highs on the back of the earnings breakout in FY23. Visibility for FY25 and FY26 appears to be healthy on the back of improved prospects for the entire sector.

However, the key parameter to track in such stories is if the business can deliver healthy ROCE across market cycles. In this regard, the business has struggled to cross 15% ROCE over the past decade due to the long working capital cycle and the average gross asset turnover ratio. While the management is sounding bullish about improving both these parameters on the back of the new smart meter product launch, it remains to be seen how well the entire ecosystem can execute while generating a healthy amount of cash in the process. The smart meter facility is scheduled to start trial production in July/August and investors should watch the scale up in revenue here through FY25 very keenly. Scale of revenue here, EBITDA margin and healthy utilisation level and conversion of profits into cash flows are the key parameters to monitor through FY25.

After the steep price rise from a level of 440 since January, investors will need to evaluate if the CMP compensates them adequately for the risks inherent in the business model. The business will need to do a lot of things right over FY25 and FY26 to meet the expectations embedded in the current stock price.

Disclaimer – This note is part of a business research & analysis series on small companies, there is no BUY/SELL recommendation or target price issued as part of this. There is no assurance that this stock makes for a good investment, there is no guarantee that this stock will be included in the coverage universe of Congruence Advisers. The note contains some forward-looking statements and insights drawn from the historical results, annual reports and investor presentations; they are to be viewed only within this context and not as a prediction of future performance of the business or the stock covered.

While due care has been taken to ensure that the information here is as accurate as possible, Congruence Advisers disclaims any liability in case of any unintentional inaccuracies.

The content does not constitute investment advice.

Disclosure (Updated as of Sep 30, 2024) – Hold a tracking allocation that is less than 2% of overall equity allocation in personal portfolio